Blog

How Much Have House Prices Risen in United Kingdom in Recent Years

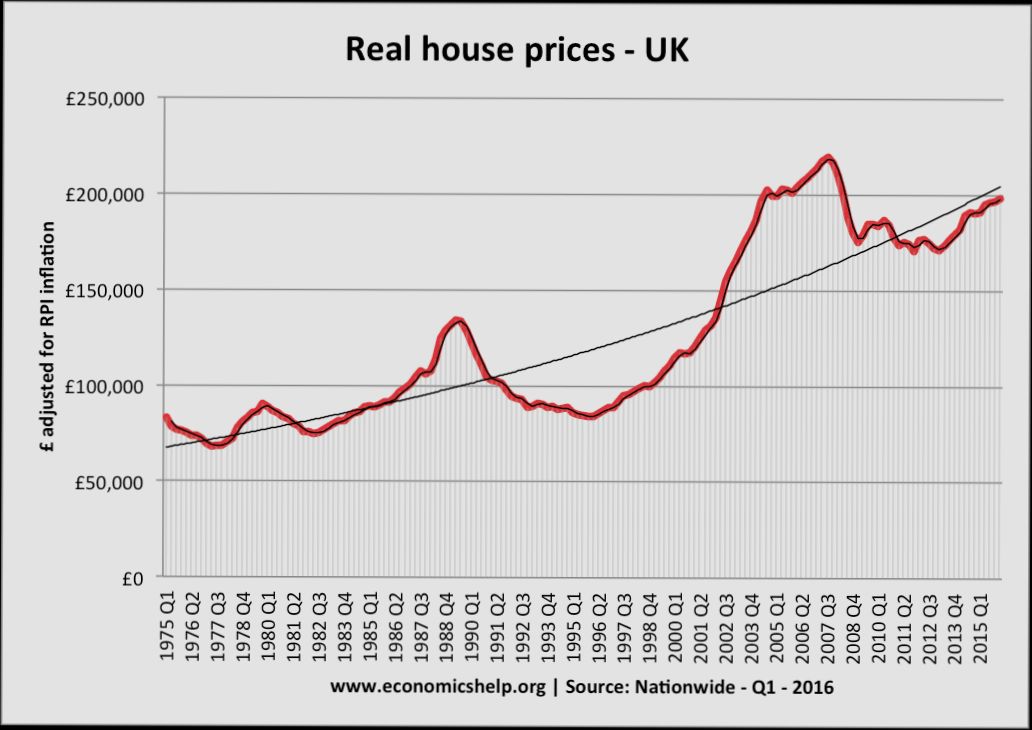

How much have house prices risen in the United Kingdom in recent years? Well, grab a cuppa because the numbers are pretty eye-opening! In 2021 alone, the average UK house price shot up to around £276,000, marking a staggering increase of about 10.2% compared to the previous year. If you think that’s crazy, the UK property market didn’t stop there; by early 2023, prices had climbed even higher, hitting an average of £287,000. Cities like Manchester and Birmingham have become hotspots, with some areas seeing increases upwards of 15% as folks scramble for a slice of the property pie.

How Much House Can I Afford Making $45,000 a Year in United States

How Much House Can I Afford Making $45,000 a Year in the United States? If you’re in the $45,000 club, you might be eyeing cozy two-bedroom homes or even a stylish condo in a lively neighborhood. With the median home price hovering around $400,000 in many parts of the country, understanding your budget is crucial. Using the general rule of thumb suggesting that your monthly housing costs should not exceed 28% of your gross income, you’re looking at about $1,050 a month. But don’t get too excited just yet; reality can vary widely based on where you’re shopping for a home.

How Much House Can I Afford with $2,500 Mortgage Payment

How much house can I afford with a $2,500 mortgage payment? That’s a question many of us ask when we start dreaming about buying a home. Let’s break it down. Generally, lenders suggest that your monthly mortgage payment should stay around 28% of your gross monthly income. If we consider a typical salary of around $100,000 a year, that gives you a monthly income of about $8,333. So, a $2,500 payment fits just right within that 28% sweet spot.

How Much House Rent Can I Afford

How Much House Rent Can I Afford? That’s the million-dollar question for so many of us diving into the rental market. If you’re in a city like San Francisco, where the average rent for a one-bedroom hovers around $3,000, you might be feeling a little queasy at the thought of your monthly budget. On the flip side, if you're in a more affordable area like Cleveland, where the average is closer to $950, you could snag a cozy place without breaking the bank. But here's the kicker: your income plays a massive role in figuring out what you can actually swing each month—think about that 30% rule, which suggests it’s best to keep your rent around 30% of your gross income. So, if you earn $5,000 a month, aiming for a rent around $1,500 makes sense.

How Much Income Do You Need to Buy a $650,000 House

How Much Income Do You Need to Buy a $650,000 House? That’s the million-dollar question—well, sort of! To get your foot in the door (literally), you’ll need to consider several factors, like your down payment, debts, and the local housing market. For instance, if you’re planning to put down 20%, you’ll need $130,000 upfront, but most people don’t have that sitting in their bank accounts. So, let’s break it down: if you opt for a lower 5% down payment, that gets you to $32,500, but then your monthly mortgage payment will be higher.

How Much Is a House Deposit

How much is a house deposit? It’s a question that hangs over many aspiring homeowners, and the answer isn’t as straightforward as you might think. Depending on where you live, it can range anywhere from 5% to 20% of the home’s price. For instance, if you’re eyeing a cozy $300,000 bungalow, you’re looking at a deposit between $15,000 and $60,000 — a hefty sum for most folks! Even in more affordable markets, like certain areas in the Midwest, the savings can still add up quickly, especially as house prices inch upward.

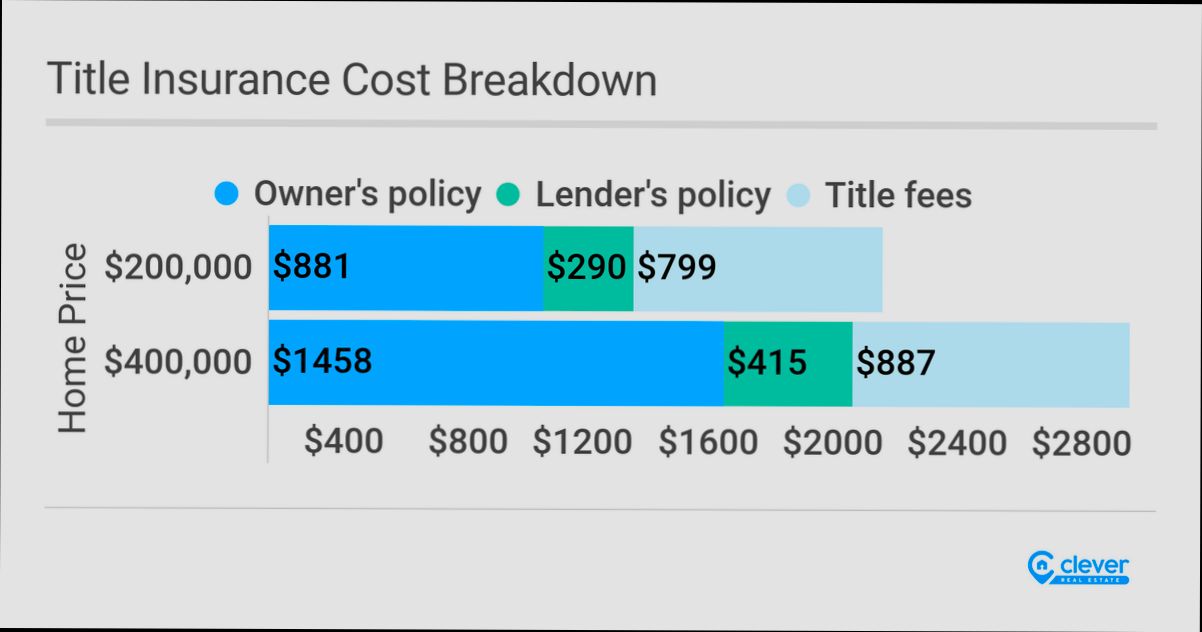

How Much Is Title Insurance

How much is title insurance? Well, that number can vary quite a bit depending on where you live and the price of your home. For instance, if you're buying a house in a bustling city like San Francisco, you might see title insurance premiums hitting around $3,000 to $4,000 on a $1 million property. On the flip side, in places like rural Texas, you might pay closer to $1,000 for the same coverage. It’s not just a one-size-fits-all deal; several factors come into play, from your property's location to the complexity of the title itself.

How Much Is Your Property Worth in United Kingdom

How Much Is Your Property Worth in United Kingdom? The answer hinges on a cocktail of factors, from location to market trends. For instance, homes in London are known to command eye-watering prices, with average properties going for around £500,000, and the trend doesn’t stop there—districts like Kensington and Chelsea are pushing the average well above £1 million. Meanwhile, if you look further afield, charming towns in Yorkshire or the North East might see averages closer to £200,000, which draws in first-time buyers eager to get their foot on the property ladder.

Tags