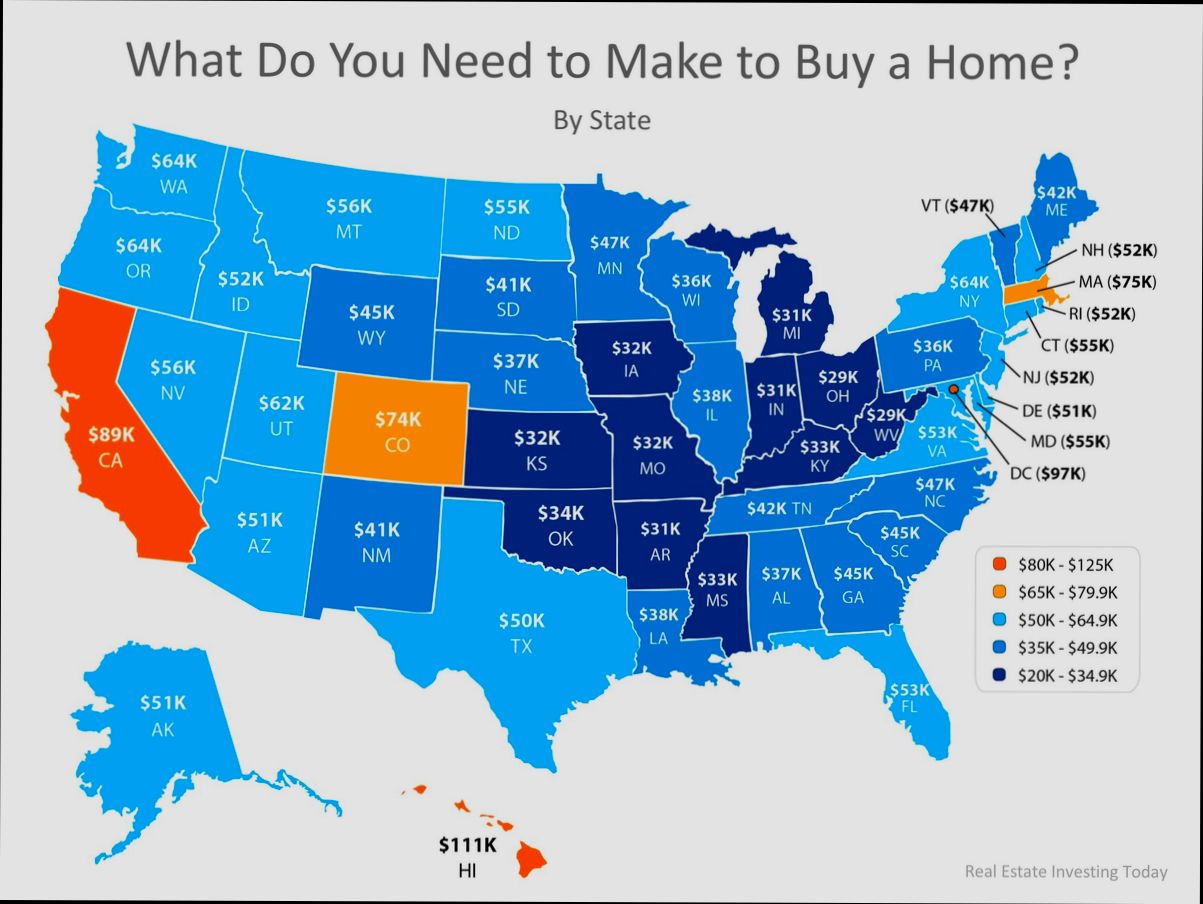

How Much Income Do You Need to Buy a $650,000 House? That’s the million-dollar question—well, sort of! To get your foot in the door (literally), you’ll need to consider several factors, like your down payment, debts, and the local housing market. For instance, if you’re planning to put down 20%, you’ll need $130,000 upfront, but most people don’t have that sitting in their bank accounts. So, let’s break it down: if you opt for a lower 5% down payment, that gets you to $32,500, but then your monthly mortgage payment will be higher.

Now, let’s talk numbers! For a typical 30-year fixed mortgage, and assuming today’s interest rates hover around 7%, that means you’re looking at about $4,300 a month, including property taxes and insurance. Do you know how much income you’d need to make that happen? Lenders generally like to see your housing costs make up no more than 28% of your gross income. That means you’d need to rake in about $15,400 a month, or roughly $185,000 a year! Sure, that sounds steep, but if you’re living in a hot market like Los Angeles or New York City, this might be your new norm. So, how do you stack up against these figures?

Essential Income Calculations for Homebuyers

When you’re stepping into the world of homebuying, understanding your income calculations is crucial. This section dives deep into the income factors that directly impact your ability to purchase a $650,000 home. By grasping these calculations, you gain clarity on how much you actually need to earn to afford your dream home.

Understanding Key Income Factors

1. Loan-to-Value Ratio (LTV): This ratio is key when figuring out how much loan you can secure against the home’s value. An 80% LTV ratio means you can borrow $520,000 on a $650,000 house. Understanding this helps you project your needed income more accurately.

2. Debt-to-Income Ratio (DTI): Lenders typically want your DTI to be under 36%. For a $650,000 house, if your total monthly debts are $1,200 (including mortgage, taxes, insurance), your gross monthly income should be at least $3,333 ($1,200 ÷ 0.36). This is a basic but essential calculation that significantly influences loan approval.

3. Closing Costs: Remember, these typically range from 3% to 6% of your loan amount. On a $520,000 loan, you might expect to pay between $15,600 and $31,200 in closing costs. Knowing this helps you understand the additional income required during the buying process.

Income Required Per Month to Afford a $650,000 Home

| Expense Type | Amount |

|---|---|

| Home Price | $650,000 |

| Mortgage Amount (80% LTV) | $520,000 |

| Estimated Monthly Payment | $2,500 |

| Other Monthly Debt | $1,200 |

| Total Monthly Debt | $3,700 |

| Required Gross Monthly Income | $10,278* |

*Estimated monthly mortgage payment assumes a 3.5% interest rate over 30 years.

Calculating from a 36% DTI ratio.

Real-World Examples

Let’s take a case for someone considering buying a $650,000 house. If your annual income stands at $120,000, your monthly gross income is $10,000. This comfortably fits within the DTI parameters with total monthly debts of $3,700.

In a contrasting scenario, a buyer earning $80,000 ($6,667/month) would find staying under the 36% DTI challenging, needing to consider lower monthly debts or an increase in income.

Practical Implications

For potential homebuyers, understanding these calculations allows better financial planning. You should:

- Assess your current debts: Identify all monthly obligations to calculate a precise DTI.

- Estimate closing costs early: Factor this into your budget to avoid surprises at closing.

- Consult with lenders: Get pre-approved to understand how much you can borrow while meeting the LTV criteria.

Actionable Advice

Make it a priority to gather your financial documents and analyze your monthly income and expenses. This enables you to not just determine your monthly mortgage payments but also to plan around costs such as insurance, taxes, and closing fees. Don’t forget to include a buffer for potential vacancy rates if looking at investment properties! Aim to stay informed and proactive in your calculations to enhance your home buying journey.

Understanding Mortgage Requirements and Rates

When embarking on the journey to buy a home, comprehension of mortgage requirements and rates is vital. This section outlines key metrics that will inform your decisions as you consider purchasing a $650,000 house. Knowing these details helps you determine how much income you need and what terms might be favorable for your financial situation.

Key Mortgage Metrics

To help you navigate the mortgage landscape, here are some essential statistics:

- Front End Ratio: It’s generally recommended that your monthly mortgage payment, including taxes and insurance, should not exceed 28% of your gross monthly income. For a $650,000 home, if your total monthly housing costs amount to about $2,343.56 (including principal, interest, property taxes, and insurance), you would need a gross monthly income of approximately $8,369.86.

- Back End Ratio: Lenders typically cap total monthly debt payments, including your mortgage, at no more than 36% of your gross monthly income. This means if you wish to stay within that limit, you’ll need a monthly income that supports these debt obligations.

- Required Annual Income: For the scenario mentioned, you’d need an annual income of about $100,439 to meet these requirements comfortably.

Comparative Table of Mortgage Requirements

| Mortgage Requirement | Amount |

|---|---|

| Gross Monthly Income | $8,369.86 |

| Required Annual Income | $100,438.36 |

| Max Allowable Monthly Mortgage Payment (@ 28% FER) | $2,343.56 |

| Max Total Monthly Debt Payments (@ 36% BER) | $669.59 |

Real-World Example

Let’s say you find a property priced at $650,000 and you plan to make a 20% down payment of $130,000. The loan amount would then be $520,000. Assuming a fixed interest rate around 8%, your estimated monthly principal and interest payment would be approximately $1,918.56.

Along with real estate taxes and homeowner’s insurance adding $425, your total monthly obligation reaches about $2,343.56. To align with the front end ratio guideline of 28%, your monthly income should be at least $8,369.86, validating the above calculations.

Practical Considerations

Understanding these ratios helps clarify your home-buying budget. Consider these actionable insights:

- Budget for Additional Costs: Always factor in property taxes, insurance, and maintenance costs when calculating affordability.

- Pre-qualification: Before house hunting, seek pre-qualification from lenders to understand your available loan amounts based on your financial profile.

- Explore Rate Options: Staying informed on current mortgage rates can lead to substantial savings. Research tools are available to compare rates across lenders to ensure you obtain the best deal.

By familiarizing yourself with these mortgage requirements and rates, you’re better equipped to make informed decisions in your home-buying process.

Analyzing Down Payment Influences

When it comes to buying a house priced at $650,000, understanding the impacts of your down payment is essential. The size of your down payment can significantly affect your mortgage terms, monthly payments, and overall affordability. Let’s dive into how different down payment amounts influence your financial landscape.

Factors Influencing Down Payment Choices

1. Loan Types and Conditions

The type of mortgage you choose can dictate the minimum down payment required. For instance:

- Conventional loans often require a minimum of 5% to 20%.

- FHA loans might allow for as little as 3.5% down.

- VA loans could enable eligible veterans to purchase a home with no down payment.

2. Impact on Monthly Payments

A larger down payment results in lower monthly payments and reduces the overall interest you pay throughout the life of the loan. For example:

- A 20% down payment ($130,000) means borrowing $520,000, leading to lower monthly payments than a 5% down payment ($32,500), which would mean borrowing $617,500.

3. Private Mortgage Insurance (PMI)

If you put down less than 20%, most lenders will require you to pay PMI, which adds to your monthly costs.

- If your PMI is around 0.5% of the loan amount per year, it can add approximately $218 per month to your mortgage payment for a $650,000 house with a 5% down payment.

Comparative Table of Down Payment Scenarios

| Down Payment Amount | Percentage of Home Price | Loan Amount | Estimated Monthly Payment* | PMI Included |

|---|---|---|---|---|

| $32,500 | 5% | $617,500 | $3,894 | Yes |

| $65,000 | 10% | $585,000 | $3,721 | Yes |

| $130,000 | 20% | $520,000 | $3,298 | No |

*Estimates based on a 30-year fixed-rate mortgage at 5% interest.

Real-World Case Studies

Consider these hypothetical profiles:

- Profile A: Jordan decides to save up for a 20% down payment. By doing so, they secure a lower interest rate and avoid PMI, leading to monthly payments of about $3,298. Over the lifetime of the loan, Jordan ends up saving nearly $50,000 compared to if they had opted for a smaller down payment.

- Profile B: Alex goes with a 5% down payment. Although moving in sooner is appealing, the high PMI and increased loan amount results in monthly payments of around $3,894. This choice means Alex will pay considerably more in interest over 30 years.

Practical Implications for Down Payment Decisions

As you’re evaluating how much you can afford, keep these strategies in mind:

- Assess Your Financial Readiness: Evaluate if you can manage a larger down payment without straining your financial stability.

- Research Loan Options: Compare various lenders’ requirements and explore whether programs exist that aid first-time buyers with down payment assistance.

- Factor in Future Costs: Don’t forget to include PMI in your budgeting if your down payment is under 20%.

By making informed decisions about your down payment, you can significantly impact your mortgage terms and overall buying experience as you pursue your dream home.

Income Ratio Metrics for Home Purchases

When considering purchasing a home, understanding income ratio metrics is crucial for determining what you can afford. These ratios help evaluate your financial health and guide your home-buying journey, particularly for a $650,000 home.

Key Income Ratios Explained

Income ratios typically consist of two main metrics: the front-end ratio and the back-end ratio. These metrics play a vital role in assessing your ability to manage monthly mortgage payments alongside other expenses.

1. Front-End Ratio: This metric focuses solely on your housing costs, including mortgage payments, property taxes, and insurance. As a benchmark, lenders often favor a front-end ratio of 28% or lower. For a $650,000 house priced with a 20% down payment, your monthly mortgage payment might result in a front-end ratio close to this limit.

2. Back-End Ratio: This ratio accounts for all monthly debt payments, including housing costs, credit cards, student loans, and other obligations. A widely accepted benchmark for the back-end ratio is 36%. If your total monthly debts exceed this percentage of your gross income, it could hinder your ability to secure a mortgage.

Income Ratio Breakdown

| Ratio Type | Recommended Maximum | Typical Impact on Loan Approval |

|---|---|---|

| Front-End Ratio | 28% | Essential for housing costs |

| Back-End Ratio | 36% | Includes total debt obligations |

Real-World Examples

Consider two potential buyers eyeing a $650,000 home:

- Buyer A: They earn $100,000 annually, bringing their gross monthly income to about $8,333. If they aim for the ideal front-end ratio of 28%, their housing costs should not exceed approximately $2,333. This aligns with a monthly payment that allows for taxes and insurance when financing the house.

- Buyer B: Earning $75,000 per year, their gross monthly income is about $6,250. Following the back-end ratio guideline, their total monthly debt obligations should not exceed $2,250. If they have existing debts, they must ensure that their future housing costs fit within these parameters.

Practical Implications

Understanding these metrics can significantly affect your home-buying options. By keeping your ratios in check, you not only improve your chances of mortgage approval but also ensure long-term financial health. Here are a few actionable strategies:

- Budgeting: Ensure your housing costs, including mortgage payments and related expenses, align with the 28% standard.

- Debt Management: Work to lower existing debts to keep your back-end ratio under 36%.

- Income Growth: If your income is close to the limits, consider strategies for increasing your earnings to improve your ratios.

Specific Facts about Income Ratio Metrics

- Achieving a front-end ratio of 28% can significantly increase your chances of obtaining favorable mortgage terms.

- Keeping your back-end ratio under 36% is crucial not only for loan approval but also for maintaining financial flexibility.

- If you find yourself exceeding these ratios, exploring lower-priced homes or increasing your down payment could help realign your financial goals.

Real-Life Scenarios of Homebuyers

Navigating the homebuying journey can often feel daunting, but seeing how real buyers tackle the process can provide both inspiration and practical insights. When considering buying a $650,000 house, understanding the unique circumstances and decisions made by other homebuyers can help map your own path to homeownership.

Key Scenarios of Homebuyers

1. Military Homespun Heroes: Many military members find themselves in a unique situation when considering homeownership. A common concern is whether to buy on a fixed income while deployed. However, military personnel can utilize VA loans, which can significantly reduce or eliminate down payment requirements, making the dream of owning a $650,000 home considerably more accessible.

2. COVID-19 Adjustments: During the pandemic, homebuyers faced unprecedented challenges. One NYC homebuyer seized the opportunity presented by lower interest rates and less competition. He shared how proper timing and financial preparedness allowed him to purchase his dream home despite a competitive market, leveraging his strong credit score to secure a favorable mortgage rate.

3. Bidding Wars and Creativity: In hot markets like Phoenix, many buyers have faced bidding wars that can inflate property prices beyond listing price. For instance, one couple had their offers declined multiple times before they switched strategies. They decided to include an escalation clause in their offer, which ultimately helped them secure their desired $650,000 home.

4. Equity Builders in Dallas: Another couple in Dallas purchased a house that not only fit their budget but also exceeded their expectations in terms of value appreciation. Within a year, they netted an additional $35,000 in equity due to smart timing and thorough market research. Their experience illustrates the importance of understanding home value trajectories when investing in property.

| Homebuyer Scenario | Location | Purchase Price | Unique Strategy | Outcome |

|---|---|---|---|---|

| Military Homebuyer | Various | $650,000 | Utilized VA loans to reduce down payment | Achieved homeownership easily |

| NYC Buyer | New York City | $650,000 | Capitalized on lower rates and timing | Secured dream home |

| Phoenix Couple | Phoenix | $650,000 | Added an escalation clause to the offer | Won amidst bidding wars |

| Dallas Investors | Dallas | $650,000 | Timing the market for better value | Gained $35,000 in equity |

Real-World Insights

- Tampa’s Tough Market: A homebuyer in Tampa highlighted the importance of being thorough in inspections and negotiations. After facing frustrations during previous bids, she learned that adding personal letters to offers expressing her commitment to the home positively impacted sellers’ decisions. Personal touches can make your offer stand out in competitive situations.

- Los Angeles First-Time Buyer: Another homebuyer bought a home in LA under $500,000 by focusing on less competitive neighborhoods. This strategic choice allowed them to enter the market without stretching their budget for a $650,000 property, proving that adaptability can lead to successful outcomes.

Practical Implications for Buyers

Understanding these scenarios enables you to approach your own homebuying journey with confidence. Consider:

- Research Your Market: Be aware of local trends, especially in competitive markets. Knowing when to act and when to hold back can influence your success.

- Explore Alternative Financing: Investigate options such as VA loans or first-time homebuyer programs that can significantly reduce your out-of-pocket costs.

- Personalize Your Offers: Never underestimate the power of a personal touch in your offer. Whether it’s a heartfelt letter or a creative financing structure, being memorable can work in your favor.

- Limit Your Emotional Investment: Homebuying is as much about emotion as it is about logic. Knowing how to balance both can help you make sound choices without falling prey to the stress of bidding wars.

By learning from the experiences of others, you can position yourself better to navigate the challenges of purchasing a $650,000 home. Remember, adaptability and informed choices are key components to a successful homeownership experience.

Long-Term Benefits of Homeownership

Homeownership comes with an array of long-term benefits that often extend beyond mere financial aspects. When you invest in a home, you’re not just securing a roof over your head; you’re making a strategic financial decision that can influence your wealth and well-being for years to come.

Wealth Accumulation

One of the most significant benefits of owning a home is the ability to build wealth over time. Home values tend to appreciate, increasing your equity. Historically, homes have appreciated an average of 3-5% annually, but in some areas, it can be significantly higher.

- Example: If you purchase a $650,000 home and it appreciates at just 3% annually, after 10 years, your home could be worth approximately $877,000, thereby increasing your investment by $227,000.

Tax Benefits

Homeownership provides various tax benefits that can reduce your overall tax burden. Homeowners can deduct mortgage interest and property taxes from their taxable income:

- Mortgage interest deduction: In 2022, homeowners could deduct interest on debts of up to $750,000 for new mortgages.

- Property tax deduction: Many homeowners can claim property taxes on their Itemized Deductions, which can add up, particularly in high-value areas.

These deductions can effectively lower your taxable income, allowing you to keep more of your hard-earned money.

Stability in Housing Expenses

Unlike renting, where your landlord can increase your rent each year, a fixed-rate mortgage allows for predictability in housing costs.

- Fact: According to the Federal Reserve, over a 10-year period, fixed-rate mortgage payments remain stable while rental prices can increase at rates of 5-10% annually in competitive markets.

This stability can help you plan your financial future with greater certainty.

Community Investment

Owning a home often encourages deeper community ties and investments in your neighborhood. Homeowners tend to be more engaged in their communities, whether through participation in local events or advocacy for better infrastructure and services.

- Statistic: Research from the National Association of Realtors found that 73% of homeowners feel a strong commitment to their community, compared to just 54% of renters.

Investing in a home also boosts local economies, as homeowners are more likely to support local businesses and vote in local elections.

| Benefit | Homeowners | Renters |

|---|---|---|

| Average Annual Home Appreciation | 3-5% | N/A |

| Tax Deductions Available | Mortgage interest, property taxes | N/A |

| Community Engagement Rate | 73% | 54% |

Real-World Example: Growing Equity

Consider a couple who purchased a $650,000 home in a rapidly appreciating market. At 4% annual appreciation, within just five years, their home could be valued at approximately $792,000. This increase in equity might enable them to leverage their home for loans in the future or provide funding for their children’s education.

Practical Implications for Homebuyers

Understanding these long-term benefits can significantly influence your decision-making process when buying a home. When evaluating a $650,000 house, think about how long you plan to live in the home. The longer you stay, the more you can benefit from appreciation and equity growth.

- Actionable Advice: Prioritize neighborhoods with a strong history of appreciation and community stability when considering where to purchase your home.

Investing in homeownership comes with careful planning and foresight, but the rewards can outweigh the initial challenges. Recognizing the long-term financial independence and stability that homeownership offers can help you make an informed decision that aligns with your financial goals.

Key Statistics on Housing Affordability

Understanding housing affordability is essential, especially when evaluating how much income you need to purchase a $650,000 house. This section focuses on key statistics that define housing affordability, helping you to make informed decisions in your homebuying journey.

Critical Affordability Statistics

1. Income Requirement: To afford a house priced at $650,000, a household typically needs to have an annual income of at least $130,000. This figure considers mortgage payments, taxes, and insurances based on current lending standards.

2. Housing Cost Burden: Approximately 50% of renters in the U.S. are considered cost-burdened, meaning they spend more than 30% of their income on housing. This illustrates the growing challenge of affordability in many markets.

3. Yearly Increase in Home Prices: The median home price has increased by an average of 8% per year over the past five years, indicating a trend that continually pressures potential buyers regarding affordability.

4. Affordable Housing Gap: There exists a gap of 3.3 million affordable rental homes for extremely low-income renters, revealing broader issues in the housing market that impact overall affordability.

5. Debt-to-Income Ratios: Conventional lenders often look for a debt-to-income (DTI) ratio of about 36%, which underscores the importance of managing existing debts effectively while considering new home expenses.

Comparative Table of Affordability Metrics

| Metric | Statistic |

|---|---|

| Required Income (Annual) | $130,000 |

| Percentage of Renters Cost-Burdened | 50% |

| Median Home Price Increase (Yearly) | 8% |

| Affordable Rental Homes Gap | 3.3 million |

| Accepted DTI Ratio | 36% |

Real-World Examples

For instance, in metropolitan areas such as San Francisco or New York City, the rising home prices have led to increased financial strain on middle-income families. A couple earning $130,000 annually may find themselves spending around 40% of their income on housing, pushing them over the affordability threshold.

Moreover, in cities like Austin, where home values have surged, a $650,000 home might require potential buyers to allocate significant portions of their income, often leading to other financial strains. This reality exemplifies how crucial it is to evaluate housing affordability alongside local market conditions.

Practical Implications for Readers

Understanding these statistics on housing affordability can have a direct impact on your homebuying decisions. By knowing the income needed to afford a property, you can better align your financial planning and budgeting. Additionally, keeping an eye on trends in home price increases versus income growth can provide valuable insight into the best time to buy.

To enhance affordability, consider exploring various financing options or homes in emerging neighborhoods, where prices may still be lower compared to high-demand areas.

- Always calculate your total monthly housing costs, including property taxes and insurance, not just your mortgage payment.

- Stay informed about the local housing market trends, which can help you spot opportunities for more affordable options.

Awareness of these key statistics will empower you to navigate the sometimes confusing landscape of housing affordability, enabling better financial choices as you approach your home purchase.