“How Much Money Do You Need to Buy a House” is a burning question for anyone dreaming of homeownership. Imagine walking into your favorite café, grabbing a latte, and casually chatting with friends about the local real estate market. You hear stories about first-time buyers who snagged a cozy three-bedroom for $300,000, while others are left scrambling for cash to cover closing costs and down payments. In many cases, having at least 20% saved for that down payment makes a significant difference—do the math, and that’s a cool $60,000 on a $300,000 home. But don’t forget about other expenses like inspection fees, appraisals, and those pesky closing costs, which can add another 2% to 5% of the home’s purchase price, easily pushing your upfront costs north of $75,000.

Let’s not gloss over the fact that regional differences play a huge role here too. A house in San Francisco can easily cost over a million bucks, meaning you’ll need a jaw-dropping $200,000 just for that down payment alone! Conversely, if you’re eyeing a charming bungalow in a small town, you might get lucky and find a place for under $200,000, making your down payment a much more manageable $40,000. Plus, with flexible loan programs available, some buyers can get away with as little as 3% down, opening up the opportunity for those who might have saved less. Whether you’re aiming for your dream home or a more budget-friendly option, understanding these numbers can help you envision how much cash you’ll really need to get started on this exciting journey.

Understanding Down Payments and Fees

When you’re preparing to buy a house, understanding down payments and associated fees is crucial. You may feel overwhelmed by all the financial jargon and percentages, but I’m here to break it down for you in a friendly way. Let’s dig into the essentials that can change your home buying experience.

What is a Down Payment?

A down payment is the upfront cash you put toward the purchase of your home. It shows your commitment to the purchase and can largely affect your mortgage terms. Most lenders require a down payment to ensure you have a stake in the property.

Here are some key figures:

- The average down payment amount in the U.S. is around 12% of the house price.

- For first-time homebuyers, a down payment can be as low as 3%, depending on the financing options available.

Understanding Fees

In addition to a down payment, you’ll encounter several fees throughout the buying process. These fees vary widely based on factors like location, type of loan, and lender. Key fees to be aware of include:

- Closing Costs: Typically range from 2% to 5% of the loan amount.

- Home Inspection Fees: Usually between $300 and $500, essential for uncovering potential issues.

- Appraisal Fees: Typically cost about $300 to $700, necessary for determining the value of the home.

Here’s a quick look at how these fees stack up:

| Fee Type | Percentage of Home Price | Average Cost Range |

|---|---|---|

| Closing Costs | 2% - 5% | $4,000 - $10,000 |

| Home Inspection Fee | N/A | $300 - $500 |

| Appraisal Fee | N/A | $300 - $700 |

Real-World Examples

Consider a scenario where you’re buying a home for $300,000:

- With a 3% down payment, you need to put down $9,000.

- If you factor in closing costs (let’s say 4%), the costs can add another $12,000.

So, you would need approximately $21,000 in total, just for the down payment and closing costs alone.

Practical Implications

It’s vital to prepare accordingly:

- Save up for the down payment early; aim for at least 5% to 20% if you can.

- Shop around for lenders to find the best rates on fees and closing costs.

- Consider whether you qualify for assistance programs that help with down payment or closing costs.

Actionable Advice

- Start budgeting for all potential fees no later than 6 months before you intend to buy.

- Keep your documents organized to streamline the closing process and potentially tackle costs that you’ve overlooked.

- Use an online mortgage calculator to estimate down payments and fees tailored to your unique situation.

By nailing down these aspects of down payments and fees, you’ll gain confidence as you move closer to homeownership.

Exploring Mortgage Options and Requirements

Navigating the world of mortgages can be overwhelming, especially with various options available and specific requirements to consider. Understanding these aspects is key to successfully financing your home purchase.

Types of Mortgage Options

You have multiple mortgage options to choose from, each catering to different financial situations and preferences. Here’s a quick rundown:

- Fixed-Rate Mortgages: The interest rate remains the same throughout the life of the loan, providing predictable monthly payments. Common terms are 15 or 30 years.

- Adjustable-Rate Mortgages (ARMs): The interest rate starts low but adjusts based on market indices after an initial fixed period, potentially leading to lower initial payments but greater long-term costs.

- FHA Loans: Insured by the Federal Housing Administration, these loans often require lower down payments and are suitable for first-time homebuyers with lower credit scores—typically starting from 3.5%.

- VA Loans: Available to veterans and active-duty service members, VA loans offer favorable terms such as no down payment and no private mortgage insurance (PMI).

- USDA Loans: These are designed for rural properties and offer zero down payment options for eligible borrowers meeting income criteria.

Mortgage Requirements

Mortgage requirements vary significantly among lenders, but here are some common factors you’ll encounter:

- Credit Score: Generally, a score of 620 or higher is desirable for conventional loans, while FHA may allow scores as low as 580 with a 3.5% down payment.

- Debt-to-Income Ratio (DTI): Most lenders prefer a DTI of 36% or less, although some may allow up to 43% for certain programs.

- Employment History: Lenders typically look for at least two years of consistent income in the same field, as stability can impact your lending decision.

- Assets and Reserves: Having additional savings to cover several months of mortgage payments can improve your chances of approval and prove your reliability as a borrower.

| Mortgage Type | Minimum Down Payment | Average Interest Rate | Ideal Credit Score |

|---|---|---|---|

| Fixed-Rate | 3% | 4.5% | 620+ |

| FHA | 3.5% | 3.5% | 580 (3.5% down) |

| VA | 0% | 3.25% | No minimum |

| USDA | 0% | 3.375% | 640+ |

Real-World Examples

Consider Jane, a first-time homebuyer seeking an FHA loan. She had a credit score of 600 and a stable job history but was initially worried about her down payment. With the FHA option, she could purchase her home with only a 3.5% down payment.

On the other hand, Mark, a veteran, qualified for a VA loan, allowing him to buy a home without any down payment. He appreciated this option because it made homeownership more attainable without the burden of monthly PMI.

Practical Implications for Buyers

When exploring mortgage options, it’s crucial to assess what aligns with your financial situation. Here are actionable tips:

- Assess Your Credit Score: Check your score and consider taking steps to improve it if necessary, as better scores can yield lower interest rates.

- Consider Your Long-Term Plans: A fixed-rate mortgage might be preferable if you plan to stay in your home long-term, while an ARM might be suitable if you expect to move within a few years.

- Get Pre-Approved: This can give you clarity on how much you can afford and streamline the buying process. Pre-approval letters can also strengthen your position when making an offer.

Understanding your mortgage options and requirements can make a significant difference in your home-buying journey. Consider the long-term implications of your choice and how each option aligns with your financial goals.

Local Housing Market Statistics Overview

Understanding local housing market statistics is crucial for anyone considering buying a home. These statistics not only reflect the current state of the housing market but also help you gauge how much money you’ll actually need to secure your dream home.

Key Market Indicators

Several key indicators influence the local housing market:

- Median Home Prices: This statistic indicates the middle value of homes sold, which can show if the market is leaning towards higher or lower price points. For example, the median home price in many metropolitan areas has surged, often exceeding $400,000.

- Inventory Levels: The number of available homes for sale can directly impact home prices. A market with low inventory (for instance, below 3 months of supply) typically leads to increased prices as buyers compete for fewer homes.

- Days on Market (DOM): This figure reveals how long homes stay on the market before selling. A lower DOM, such as 30 days or fewer, indicates a strong seller’s market and can signify that you may need to act quickly when making offers.

| Market Indicator | Current Value | Previous Year Value |

|---|---|---|

| Median Home Price | $420,000 | $385,000 |

| Inventory Levels (Months) | 2.5 months | 4 months |

| Average Days on Market (DOM) | 29 days | 45 days |

Real-World Examples

Let’s take a closer look at how these statistics play out in different regions:

- Urban Centers vs. Suburbs: In major cities like San Francisco, the median home price is currently around $1.2 million, much higher than the national average. Conversely, suburban areas such as Phoenix have seen stronger growth, with home prices climbing to approximately $500,000 as families seek more space.

- First-Time Buyers: Many first-time homebuyers are facing challenges due to rising prices and low inventory. A recent survey indicated that 65% of these buyers reported struggling with affordability, directly correlating to median prices exceeding their budget.

Practical Implications

As you consider purchasing a home, it’s important to analyze local market statistics closely. Here are some actionable insights:

- Research Local Trends: Keep an eye on specific neighborhoods instead of broader markets. Cities may have pockets where home prices vary significantly.

- Adjust Your Budget: If the local median price is beyond your reach, consider looking in areas with higher supply or homes needing minor renovations.

- Stay Informed: Utilize resources like the National Association of REALTORS® to access up-to-date reports and local statistical insights.

By understanding these local housing market statistics, you can prepare more effectively for your home-buying journey. Monitoring these metrics will empower you with the knowledge needed to make smart, informed decisions.

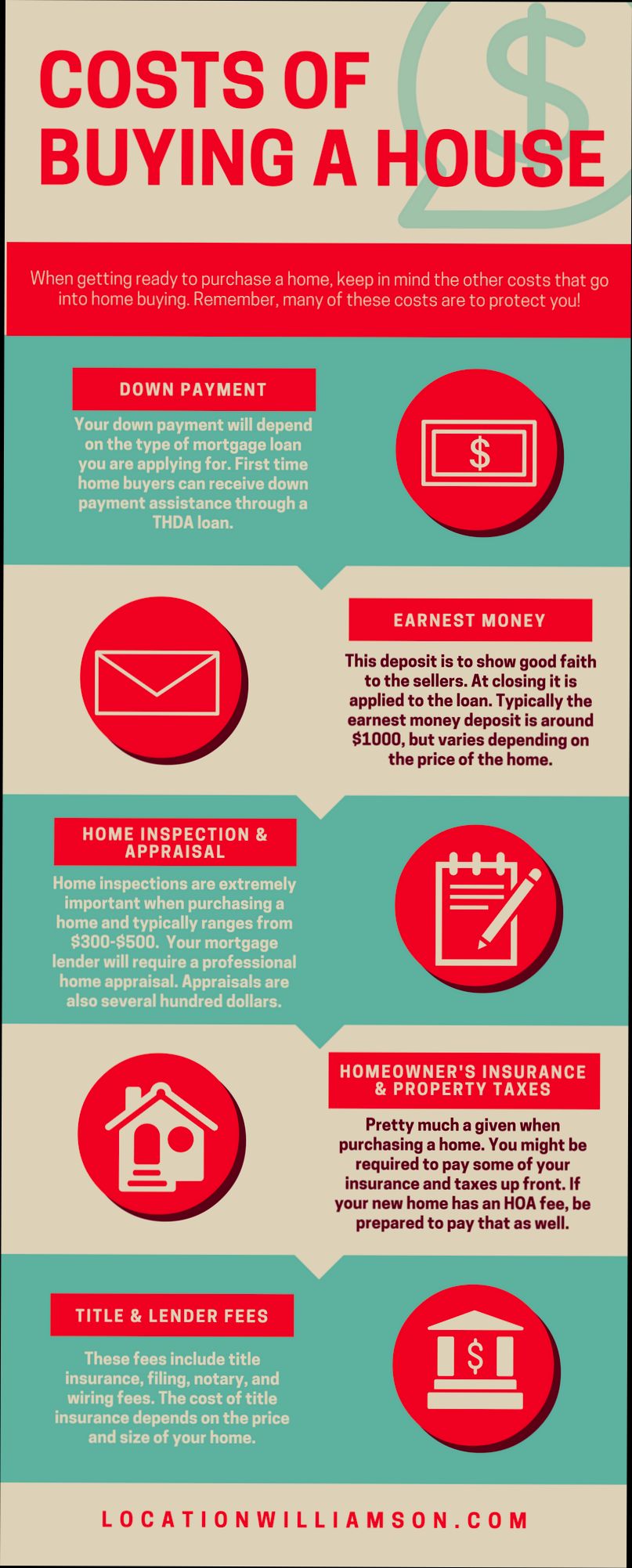

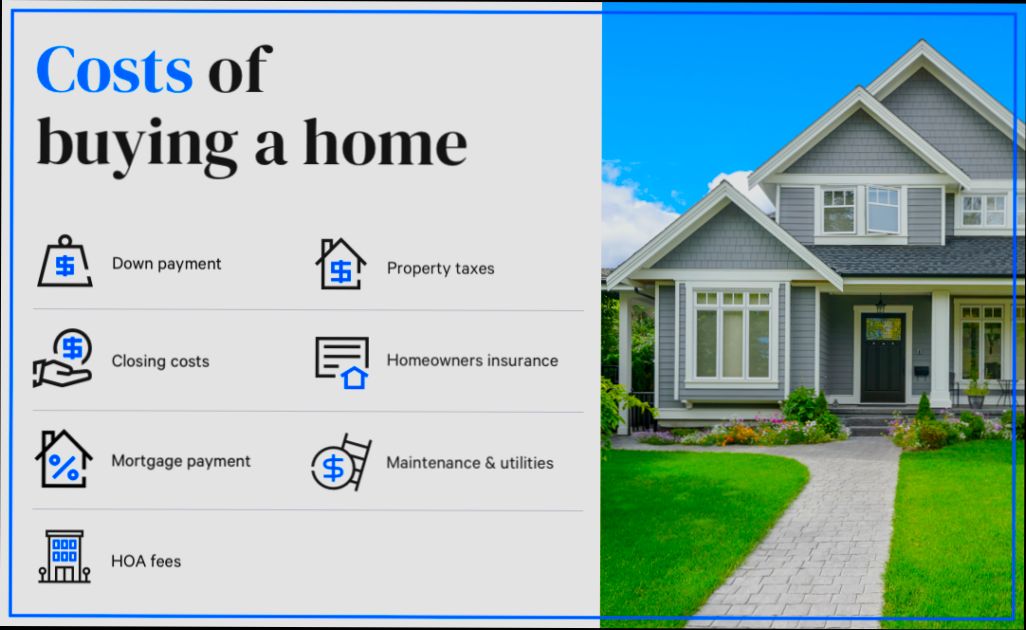

Hidden Costs of Home Ownership

Understanding the hidden costs of home ownership is essential as you prepare to buy your dream home. While you may have budgeted for the purchase price and mortgage payments, several additional expenses can catch you off guard. Let’s explore some of these costs in detail and how you can prepare for them.

Key Hidden Costs to Anticipate

1. Property Taxes: Depending on where you live, property taxes can be a significant ongoing expense. On average, homeowners in the U.S. pay about 1.1% of their home’s value in property taxes annually. Depending on the market value, this could mean thousands of dollars each year.

2. Homeowners Insurance: Not only is this a crucial protection for your home, but it can also add substantially to your monthly expenses. The national average for homeowners insurance hovers around $1,500 annually, but this can vary widely based on location and the specific coverage you choose.

3. HOA Fees: If you purchase a home in a community governed by a homeowners association, you may be responsible for monthly or quarterly fees. These fees can range from $200 to over $1,000 monthly, depending on the community and the amenities provided.

4. Maintenance: Regular maintenance is vital to keeping your home in good condition. A common recommendation is to budget about 1% of your home’s purchase price annually for maintenance costs. This figure could represent hundreds of dollars that you need to set aside.

5. Utilities: Your monthly utility bills, including electricity, water, gas, and internet, can also add up quickly. On average, homeowners can expect to pay around $400-$500 monthly on utilities, depending on the size of your home and the local rates.

| Cost Category | Average Estimated Cost |

|---|---|

| Property Taxes | 1.1% of home value annually |

| Homeowners Insurance | $1,500 per year |

| HOA Fees | $200 to $1,000/month |

| Maintenance | 1% of home value per year |

| Utilities | $400 to $500/month |

Real-World Examples

Imagine that you bought a $300,000 home. Here’s a breakdown of potential hidden costs:

- Property Taxes: $3,300 annually (1.1% of $300,000).

- Homeowners Insurance: About $1,500 annually.

- HOA Fees: If applicable, that could be around $4,800 annually ($400/month).

- Maintenance: Another $3,000 annually (1% of $300,000).

- Utilities: Roughly $6,000 annually ($500/month).

Adding these hidden costs could mean an additional approximate total of $18,600 per year, or about $1,550 per month, on top of your mortgage payment.

Practical Implications for Readers

As you navigate the process of homeownership, it’s vital to accurately calculate these costs in your overall budget. Failing to account for these hidden expenses can lead to financial strain after you’ve moved in.

Consider setting aside a separate savings account dedicated to these costs, so you’re prepared when they arise. Additionally, researching local rates for utilities and insurance can help you estimate realistic expenses specific to your situation.

Finally, keep in mind that the condition of your home can also significantly impact maintenance costs. If you opt for an older property, you might face larger repair bills down the line.

By being proactive and aware of these hidden costs, you’ll be in a stronger position to manage your finances successfully as a homeowner. Prepare for the unexpected!

Real-World Case Studies of Homebuyers

When it comes to understanding how much money you need to buy a house, real-world case studies of homebuyers can provide insightful perspectives. By analyzing different scenarios, you can better grasp the financial dynamics involved in home purchasing.

Key Insights from Homebuyer Case Studies

1. Diverse Financial Backgrounds: Homebuyers come from varied financial situations and often bring unique challenges. An estimated 35% of first-time buyers relied on family gifts to cover down payments, illuminating how supportive financial networks can impact affordability.

2. Impact of Location: In case studies from 2023, it was noted that a buyer in Austin, Texas, needed approximately $45,000 for a down payment on a $300,000 home due to the city’s rapidly escalating home prices, compared to a buyer in a less competitive market like Indianapolis, who needed just $20,000 for the same down payment on a $200,000 home.

3. Securing Assistance: Approximately 50% of buyers reported using government-backed loans or assistance programs that significantly reduced the financial burden. In real scenarios, first-time buyers benefited from an average reduction of $15,000 due to such programs, enhancing their purchasing potential.

4. Budgeting Challenges: A survey revealed that 60% of homebuyers underestimated hidden costs, such as maintenance and property taxes. For example, a family that purchased a home in Denver for $450,000 found themselves with an additional $5,000 in unanticipated costs in the first year alone.

Comparative Case Study Table

| City | Home Price | Down Payment Required | Additional Costs | Family Assistance Utilized |

|---|---|---|---|---|

| Austin | $300,000 | $45,000 (15%) | $12,000 | Yes (25% of buyers) |

| Indianapolis | $200,000 | $20,000 (10%) | $5,000 | No |

| Denver | $450,000 | $67,500 (15%) | $10,000 | Yes (30% of buyers) |

Real-World Examples

- Example 1: Sarah and John, a young couple in Austin, utilized a $25,000 gift from their parents to make a 15% down payment. Their decision was influenced by the competitive nature of the market. They realized they could have opted for a government program but were unfamiliar with the options available to them.

- Example 2: In Indianapolis, Mike, a first-time homebuyer, used a FHA loan, allowing him to secure his home with just a 3.5% down payment. He consciously saved an additional $5,000 for hidden costs, which helped cover closing costs and minor repairs after moving in.

- Example 3: The Thompsons, buying in Denver, faced an 18% increase in property taxes within their first year of ownership. Despite receiving a $15,000 grant from a local program, they learned to budget for unexpected expenses that come with homeownership, like maintenance costs since they moved into an older home.

Practical Implications for Readers

Understanding these case studies is crucial as you navigate your own homebuying journey. Consider exploring family assistance options or local government programs that could ease your financial burden. Also, be sure to overestimate your additional costs to avoid surprises after your purchase.

Specific Advice for Future Homebuyers

- Research local assistance programs that could substantially lower your upfront costs.

- Set aside extra funds for unexpected expenses associated with homeownership; assuming an additional 10-15% of your home price can safeguard you against budget shocks.

- Connect with other homebuyers in your community to share experiences and gather practical insights.

Advantages of Saving for a Larger Deposit

When it comes to buying your dream home, having a larger deposit can significantly enhance your financial position. It’s not just about impressing lenders; the advantages can lead to considerable savings and greater peace of mind when you take on a mortgage. Let’s explore these benefits together!

Key Advantages

1. Lower Monthly Repayments: A larger deposit directly reduces the amount you need to borrow. For instance, on a property priced at $700,000:

- With a 20% deposit ($140,000), your loan amount is $560,000.

- If you save for a 30% deposit ($210,000), your loan amount decreases to $490,000.

- This translates to monthly repayments dropping from $2,069 to $1,811—a saving of $258 each month!

2. Avoid Lenders Mortgage Insurance (LMI): Typically, if your deposit is less than 20%, you may be required to pay LMI, which protects the lender if you default on the loan. Saving for a larger deposit can help you sidestep this additional cost entirely, resulting in significant savings.

3. Access to Better Interest Rates: Lenders often offer more favorable interest rates for borrowers who present larger deposits, viewing them as lower-risk. For instance, data indicates that buyers with a 25% deposit or more could qualify for much better mortgage terms compared to those with only 5% or 10%. This increase in deposit percentage can impact your overall borrowing cost dramatically.

4. Greater Acceptance of Loans: Homebuyers with a larger deposit often find it easier to get mortgage approvals, as lenders see them as more financially stable. This can be particularly helpful if you have other factors, like a less-than-ideal credit history.

Comparative Table of Loan Scenarios

| Deposit Percentage | Property Price | Deposit Amount | Loan Amount | Monthly Repayment |

|---|---|---|---|---|

| 20% | $700,000 | $140,000 | $560,000 | $2,069 |

| 30% | $700,000 | $210,000 | $490,000 | $1,811 |

Real-World Examples

Consider two potential homebuyers. Buyer A has a 20% deposit of $140,000 and secures a loan of $560,000. Buyer B, after saving diligently, manages to put together a 30% deposit of $210,000, reducing their loan to $490,000. Over 30 years, while Buyer A will pay approximately $2,069 monthly, Buyer B enjoys reduced monthly payments of $1,811. This difference results in an annual saving of $3,096, which can significantly ease financial pressure.

Practical Implications

When you’re in the home-buying process, keeping your focus on saving for a larger deposit could lead to long-term financial benefits. Having a solid savings plan can allow you to navigate the mortgage landscape more effectively. Consider setting specific savings goals and automating your deposits into a high-interest savings account dedicated to your home purchase.

Actionable Advice

- Set a Target: Determine what percentage deposit works for your situation and save aggressively. Aiming for at least a 20% deposit can eliminate LMI costs.

- Budget Wisely: Track your spending and identify areas where you can cut back to boost your savings.

- Utilize Assistance: Look into government schemes and programs that may help boost your deposit through grants or bonuses.

Advancing towards a larger deposit may require discipline and patience, but the financial advantages can be substantial when purchasing a home.

Budgeting Strategies for Home Purchase

When preparing to buy a home, having a solid budgeting strategy can make a significant difference in your readiness and ability to afford the costs associated with homeownership. Let’s explore effective strategies that will help you navigate the financial landscape of purchasing a house.

Understanding Your Income and Expenses

To start, you need a clear understanding of your after-tax income and how it fits into your home-buying budget. Follow these steps for a comprehensive assessment:

1. List All Your Expenses: Document every expense you incur each month. This includes not only your basic needs but also discretionary spending.

2. Calculate Your After-Tax Income: Make sure to account for your actual take-home pay after taxes to devise a realistic budget.

3. Subtract Your Total Expenses from Your Income: This will give you a clear picture of what you have available for savings or investment towards your future home.

The 50/30/20 Rule

One practical budgeting method you might consider is the 50/30/20 rule. This rule can help you prioritize your spending effectively:

- 50% Needs: Allocate half of your after-tax income to essential expenses like groceries, utilities, and insurance.

- 30% Wants: This portion can go towards lifestyle choices and non-essential items, but remember that minimizing this can help you save for your house.

- 20% Goals: Contribute this segment to your financial goals, like saving for a down payment or paying off credit card debt.

By adhering to this rule, you ensure you are not only taking care of immediate needs but also planning for your future home purchase.

| Expense Category | Percentage of After-Tax Income |

|---|---|

| Needs | 50% |

| Wants | 30% |

| Goals | 20% |

Real-World Case Studies

Let’s look at how effective budgeting strategies have helped individuals in their journey toward homeownership:

- Case Study 1: A couple decided to follow the 50/30/20 rule, primarily focusing on increasing their savings by reallocating funds from their “wants” category. They found that by cutting back on dining out and entertainment, they could save an additional $500 each month toward their down payment fund.

- Case Study 2: A single professional used a spreadsheet to manage her expenses more closely. By identifying unnecessary subscriptions and reducing spending on non-essentials, she managed to save $300 per month, directing those funds to her emergency savings in preparation for unexpected homeownership costs.

Actionable Insights

As you consider your budgeting strategy for a home purchase, keep these practical implications in mind:

- Emergency Fund Preparation: Aim to increase your emergency fund by around $500 to $1,000 to cover any unexpected costs that may arise during the homebuying process.

- Debt Repayment Focus: Prioritize paying off high-interest debts. For example, if you can pay off $300 on a credit card each month, it can free up funds for savings towards your down payment.

- Flexible Savings Options: Consider separating your savings into long-term and short-term categories. Use a high-yield savings account for long-term goals to make accessing your funds a bit more challenging, while keeping necessary funds for urgent purchases easily accessible.

Remember, every dollar saved brings you closer to your goal of homeownership, so consistently evaluate and adjust your budget to maximize your savings and investments.