How much is title insurance? Well, that number can vary quite a bit depending on where you live and the price of your home. For instance, if you’re buying a house in a bustling city like San Francisco, you might see title insurance premiums hitting around $3,000 to $4,000 on a $1 million property. On the flip side, in places like rural Texas, you might pay closer to $1,000 for the same coverage. It’s not just a one-size-fits-all deal; several factors come into play, from your property’s location to the complexity of the title itself.

Let’s not forget the different types of title insurance you can choose from. You’ll typically scoop up an owner’s policy, which protects you, and a lender’s policy, which secures the mortgage lender’s investment. The combination can range from $1,000 to over $5,000 depending on your situation. Plus, don’t overlook that some states have regulations on title insurance rates, which can make a big difference. It’s all about gathering the facts and numbers so you can plan accordingly without any surprises along the way.

Understanding Title Insurance Costs

When it comes to title insurance, understanding the costs involved helps you prepare for your home buying journey. From premiums to additional fees, knowing what to expect can save you time and money. Let’s break down the various components of title insurance costs so you can budget effectively.

Title Premiums

The title insurance premium is the foundational cost you’ll encounter. Here’s how it breaks down:

- Amount: Generally, the premium for an Owner’s Policy correlates with the property’s full purchase price, while the Lender’s Policy premium is tied to the mortgage amount.

- Payment Structure: This premium is a one-time fee paid at closing, meaning you won’t have to worry about ongoing payments.

Title Search Fees

Before title insurance is issued, a title search is conducted to uncover any potential issues.

- Cost Range: You’ll typically pay between $100 and $400 for a title search, depending on how complicated the property’s history is.

- Scope of Work: This fee accounts for the effort spent reviewing public records to uncover any liens, claims, or disputes regarding ownership.

Recording Fees

Once you have your title insurance, you’ll also need to account for recording fees.

- Cost Variation: These fees, ranging from $50 to $150, depend on your location and the number of pages that need to be recorded.

- Purpose: Recording fees ensure proper public access to the property’s title and any associated liens or encumbrances.

Endorsement Fees

For added protection, you may want endorsements on your title insurance policy.

- Typical Costs: Expect to pay an additional $50 to $200 per endorsement.

- Common Endorsements: These might cover aspects like zoning issues or property use restrictions, which can be crucial depending on your property type.

Survey Fees

Certain properties may require a survey to clarify boundaries or easements.

- Typical Cost: Survey fees generally range from $300 to $700, which can be a significant additional expense depending on the property’s size and complexity.

- Re-inspection Fees: Additional inspections could incur extra fees, particularly if the survey points out deficiencies that need to be addressed.

| Fee Type | Cost Range | Notes |

|---|---|---|

| Title Premium | Based on price | One-time fee linked to property or loan amount |

| Title Search Fees | $100 - $400 | Dependent on complexity of property history |

| Recording Fees | $50 - $150 | Varies by location and number of pages |

| Endorsement Fees | $50 - $200 | Additional coverage for specific issues |

| Survey Fees | $300 - $700 | Required for boundary confirmation or easements |

Real-world Examples

Let’s say you’re purchasing a property for $300,000 and opt for an Owner’s Policy. Your title insurance premium might be around $1,200 (depending on local rates). After paying the title search fee of $250 and a recording fee of $100, you would have already incurred $1,550 before additional costs like endorsements or surveys.

In another scenario, if your lender requires a survey and it costs you $400, and you decide to add a zoning endorsement for $100, your total title insurance-related costs could exceed $2,000.

Practical Implications

Understanding these costs means you can better plan your finances. For instance:

- Always ask for a breakdown of title insurance costs from your closing agent.

- Factor in both the title insurance premium and all additional fees when budgeting for closing costs.

Key Takeaway Facts

- Your title insurance premium is a one-time cost linked to your property’s purchase price.

- Title search fees vary because they depend on the complexity of the title history.

- Don’t overlook additional costs such as endorsements and surveys; they can add significantly to your total expenses.

Factors Influencing Title Insurance Premiums

When it comes to title insurance premiums, various factors come into play that can significantly affect your costs. Understanding these factors allows you to make informed decisions as you navigate the home buying process.

Key Factors Affecting Title Insurance Premiums

1. Property Value:

- The premium for an Owner’s Policy typically correlates with the purchase price of the property. Higher-value homes will naturally incur greater premiums. For example, if a property sells for $250,000, title insurance could range from $950 to $1,706, depending on various factors.

2. Loan Amount:

- For Lender’s Policies, your premium will reflect the amount of the mortgage. The typical premium is influenced by both the loan size and the specific risks associated with the underlying title.

3. State Regulations:

- Title insurance premiums can differ significantly from one state to another due to local regulations and market environments. Some states might have more competitive pricing due to the number of providers or market dynamics, while others may reflect higher rates based on fewer participating insurers.

4. Market Conditions:

- The overall real estate market also plays a vital role. For instance, research indicates that the title insurance industry has seen revenues grow at a compound annual growth rate of 3.4%. This growth often corresponds with higher consumer demand and increased competition among title insurers, which can influence pricing strategies.

5. Settlement Costs:

- Additional charges related to settlement services, such as title search fees or closing costs, can impact the final amount you pay for title insurance. These fees can range from $250 to $325 for a title search and $450 to $650 for closing services.

Comparative Table of Title Insurance Costs

| Property Value ($) | Owner’s Policy Premium ($) | Loan Amount ($) | State Variation (%) |

|---|---|---|---|

| 250,000 | 950 - 1,706 | 200,000 | 5 - 15 |

| 500,000 | 1,500 - 2,500 | 400,000 | 3 - 10 |

| 1,000,000 | 2,500 - 4,000 | 800,000 | 2 - 8 |

Real-World Example: Sonic Title Agency, LLC

An example from Sonic Title Agency outlines that for a property worth $250,000, the title insurance policy costs range between $950 and $1,706. This variation is dependent on the state and other associated fees.

Another company, Sonic Loans, lists a loan origination charge that can be between 0% and 3% of the loan amount. Such charges contribute directly to the total costs you may incur when securing title insurance.

Practical Insights for Buyers

- Shop Around: Don’t hesitate to compare quotes from different title insurance providers to find the best rates.

- Understand the Breakdown: Familiarize yourself with how costs break down—knowing the fees involved in title searches and closing can save you money.

- Consult Local Experts: Engaging with local real estate professionals can help you understand regional variations affecting premiums.

It’s essential to grasp how these factors interact and affect your potential title insurance costs. By being aware of these elements, you position yourself to negotiate better terms and make well-informed financial decisions as you purchase your new home.

Title Insurance Price Trends and Statistics

As we dive into the specifics of title insurance price trends and statistics, it’s clear that this sector reflects significant growth tied to the overall real estate market dynamics. Understanding these price trends can help you make informed decisions when purchasing title insurance.

Key Price Trends

- The title insurance market was valued at USD 67.55 billion in 2024 and is expected to reach USD 72.85 billion in 2025. This growth trajectory is compelling, suggesting a robust demand for title insurance services.

- Forecasts predict that by 2033, the market could soar to USD 133.25 billion, showcasing a CAGR of 7.84% during the forecast period. This growth can largely be attributed to the increase in home sales, with over 6 million homes sold annually.

- The direct title insurance premiums have shown notable increases, primarily influenced by a competitive landscape where insurers are focused on enhancing service delivery and accuracy.

Market Share and Revenue Table

| Company | Market Share (%) | Revenue ($m) | Profit ($m) | Profit Margin (%) |

|---|---|---|---|---|

| Fidelity National Financial, Inc. | 30.0 | 7,024.2 | 1,277.3 | 18.2 |

| Old Republic International Corporation | 15.0 | 3,548.6 | 407.5 | 11.5 |

| Stewart Information Services Corp | 10.0 | 2,216.0 | 259.5 | 11.7 |

Real-World Examples of Price Trends

1. Impact of Low Interest Rates: The pandemic saw interest rates reach historic lows, encouraging many potential buyers to enter the housing market. As a result, title insurance premiums surged, reflecting the increased number of transactions.

2. Regional Variations: States in the West, Southeast, and Southwest regions have experienced sharper increases in title insurance costs, driven by higher real estate activity. For instance, in states like California and Florida, you might find title insurance premiums higher due to competitive markets.

3. Market Adaptations: Insurers are also innovating their offerings. Some are now bundling title insurance with other real estate services, which can influence pricing strategies and affect perceived value for consumers.

Practical Implications for You

Understanding these price trends helps you gauge not just current costs but also prepares you for future price dynamics in the title insurance market. If you’re looking to buy a home or refinance, being aware of the expected increases in premiums may prompt you to act sooner rather than later.

Actionable Insights

- Keep an eye on market reports and local trends to better understand when to purchase title insurance.

- Be proactive in discussing your options with your title company; ask for insights on how current market conditions could affect your premiums.

- Explore bundling options offered by some companies that could provide savings along with necessary coverage.

By focusing on these price trends and statistics in the title insurance landscape, you can make more strategic decisions in your real estate endeavors.

Real-World Scenarios for Title Insurance

When thinking about title insurance, it’s essential to understand how it plays a role in actual home buying scenarios. Title insurance isn’t just a bureaucratic formality; it can significantly influence your real estate experience, from securing financing to protecting your investment.

Common Scenarios Where Title Insurance Matters

1. Hidden Liens: Imagine you discover after closing that there’s an unpaid tax lien on your property. Without title insurance, you could be responsible for settling that debt, costing you thousands of dollars.

2. Ownership Disputes: Picture a situation where a previously unknown heir emerges, claiming rights to the property. This could lead to costly legal battles. Title insurance protects you from these disputes, ensuring your title remains clear and defensible.

3. Forged Documents: In rare cases, you might find that someone forged a signature on previous property transfers. Title insurance would cover legal fees related to proving your ownership, providing peace of mind that your investment is secure.

Financial Implications of Title Insurance in Scenarios

To give you a clearer understanding of how these scenarios can impact finances, here’s a comparative look at potential costs in different situations:

| Scenario | Potential Cost Without Title Insurance | Title Insurance Coverage |

|---|---|---|

| Hidden Lien | $15,000+ | Full coverage on liens |

| Ownership Dispute | $10,000 - $50,000 | Legal defense & settlement costs |

| Forged Document | $5,000 - $30,000 | Legal fees for ownership verification |

Real-World Examples

- Case Study 1: The Unforeseen Tax Lien

A couple purchased a home for $250,000. Three months post-purchase, the couple received a notice of a $20,000 tax lien from the previous owner. Thanks to their title insurance, they didn’t have to pay out of pocket for the lien—saving them a significant financial burden.

- Case Study 2: Long-Lost Heir Claim

A homeowner, who invested $300,000 in their home, faced a claim from a long-lost sibling of the deceased previous owner. The legal battle lasted over a year, but their title insurance covered legal fees amounting to $25,000, allowing them to retain ownership without financial distress.

Practical Implications for Homebuyers

When purchasing a home, consider the financial risks associated with potential title issues. By investing in title insurance, you can mitigate these risks. Here are some practical tips:

- Always request a title search: This gives you an initial overview of any potential issues before purchasing.

- Review your policy: Make sure you understand what’s covered and any exclusions.

- Consider the area’s history: High turnover neighborhoods may present more risks due to prior ownership disputes.

Actionable Advice

Always factor in the costs of title insurance when budgeting for your new home. Besides the premium for the insurance, it’s important to think about hidden expenses like liens or legal challenges. This foresight will empower you to make informed decisions and protect your investment like a pro.

Comparing Costs Across Different States

Understanding title insurance costs can greatly vary based on where you live. Each state has its own regulations, market conditions, and average premiums, which can lead to significant differences in what you pay. Let’s dive into how these variations impact your overall expenses.

Title Insurance Premiums by State

The premium for title insurance often reflects the state you’re purchasing in. Here are some key points to keep in mind:

- State Regulations: Some states regulate title insurance premiums, leading to less variability, while others allow more freedom, resulting in wide-ranging costs.

- Market Influences: Local real estate conditions, such as demand and supply, can cause premiums to fluctuate.

Comparative Title Insurance Rates

Here’s a quick breakdown of average title insurance premiums across a few states:

| State | Average Title Insurance Premium | Regulation Type |

|---|---|---|

| California | $1,500 | Regulated |

| Texas | $2,200 | Regulated |

| New York | $3,200 | Partially Regulated |

| Florida | $1,800 | Unregulated |

| Illinois | $1,600 | Regulated |

This table illustrates not just the average costs but also the type of regulation in place for each state. For instance, states like California and Texas have regulated rates that can provide some predictability compared to Florida, where costs might vary more widely due to less strict regulations.

Real-World Examples

Consider the case of a homebuyer in New York versus one in Texas. A buyer in New York purchasing a $500,000 property may face a title insurance cost of about $3,200, whereas a buyer in Texas for a similar priced property might only need to pay around $2,200. This $1,000 difference can significantly affect your closing costs and budget planning.

Another example is in Florida. Here, the lack of stringent regulations means that premiums can vary significantly from one title company to another, meaning you could see rates ranging from $1,500 to $2,200 for the same property value.

Practical Implications for Homebuyers

When you’re comparing costs across different states, consider the following:

- Research Local Rates: Investigate title companies in your chosen state to find competitive pricing.

- Understand Regulations: Be aware of whether your state has regulated or unregulated title insurance markets. This knowledge can help in negotiating and shopping for the best rates.

- Total Cost Assessment: Look beyond premiums; consider other fees that may be associated with the title insurance process, as these can add to your costs.

Actionable Advice

- Get Multiple Quotes: Always obtain quotes from different title companies in your state to ensure you’re getting the best price for comparable coverage.

- Be Aware of State Differences: Knowing the pricing trends in your home state will empower you to make informed decisions during your home purchase process.

Advantages of Investing in Title Insurance

Investing in title insurance provides significant benefits that protect both your property rights and financial interests. Knowing the key advantages can help you make a more informed decision when contemplating this one-time premium expense.

Financial Security and Risk Mitigation

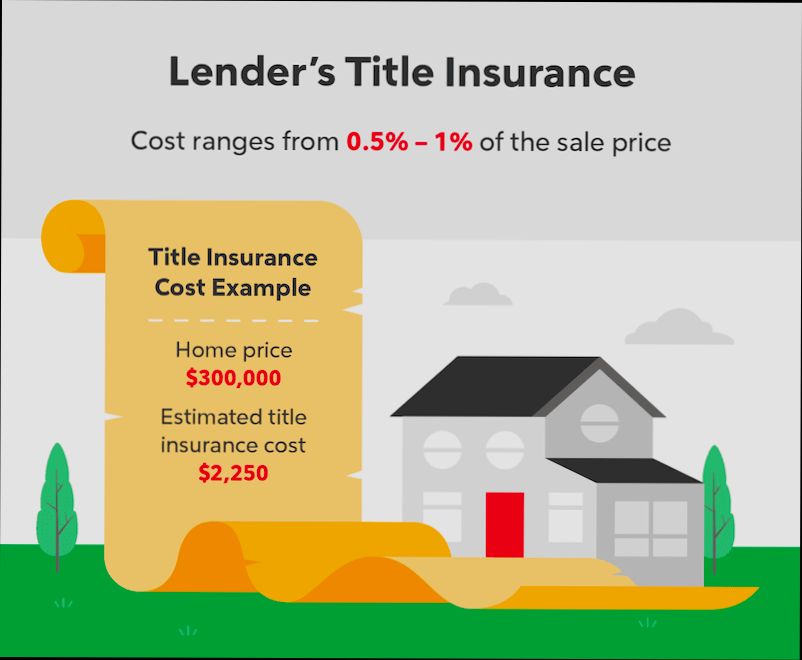

One of the most compelling reasons to invest in title insurance is the financial security it provides. Your one-time premium, generally ranging from 0.5% to 1% of the property’s value, can save you from potential financial disasters. Here’s how:

- Undisclosed Liens: Title insurance protects you from any unpaid debts tied to the property by previous owners. If you discover a lien after your purchase, title insurance covers your financial obligations, ensuring you don’t pay the price for someone else’s debts.

- Ownership Disputes: With title insurance, you’re shielded from claims by unknown heirs or third parties challenging your ownership. Without it, these disputes could lead to prolonged legal battles, costing you both time and money.

- Public Record Errors: Mistakes in public records can occur, leading to ownership complications. Title insurance acts as a safeguard against these clerical errors, ensuring your title remains clear and undisputed.

Providing Legal Defense

When challenges arise regarding your property title, title insurance is designed to provide legal defense against claims. This is crucial because:

- Protection Against Claims: If someone claims they have a right to your property, title insurance covers the legal costs associated with defending your ownership. This defense could save you thousands of dollars in legal fees and potential damages.

- Peace of Mind: Knowing that you have coverage for legal disputes gives you confidence in your investment. This peace of mind allows you to enjoy your property without the looming worry of past issues undermining your ownership.

Comparison of Coverage Types

| Coverage Type | Purpose | Benefits |

|---|---|---|

| Owner’s Title Insurance | Protects buyer’s ownership rights | Financial safeguard, legal defense against claims |

| Lender’s Title Insurance | Protects lender’s interest | Generally required for financed transactions, reduced risk for lenders |

Real-World Examples

Consider a scenario in Texas, where a homeowner discovers a lien from a previous owner that wasn’t disclosed during the title search. Without title insurance, the homeowner would ultimately be responsible for that debt. However, with title insurance in place, the insurer covers the lien, allowing the homeowner to avoid financial loss.

In California, imagine purchasing a home and later facing a legal claim by an unknown heir. If you had invested in an owner’s title insurance policy, the insurer would handle the legal defense, ensuring that your investment remains secure and your financial obligations are protected.

Actionable Insights

Before closing on a property, it’s vital to think about the risks you may encounter without title insurance. The investment safeguards against future problems that could arise from past issues, saving you money and stress in the long run. Here are a few tips to keep in mind:

- Always Opt for Owner’s Title Insurance: If you’re purchasing a property with cash, be proactive and secure your ownership rights by opting for an owner’s title insurance policy.

- Assess Your Risk Tolerance: Consider the age of the property, the likelihood of past disputes, and your own financial ability to handle unexpected issues when weighing the decision to invest in title insurance.

- Consult Experts: Speak with real estate professionals or title companies to better understand the specifics of title insurance in your state and the potential risks that could affect your property.

Investing in title insurance is not just about complying with requirements; it’s about protecting your home, your finances, and your peace of mind.

Common Misconceptions About Title Insurance Rates

When it comes to title insurance rates, several misconceptions can lead to confusion and potentially impact your financial decisions in real estate. Understanding these common myths helps clarify what you should expect in terms of costs associated with title insurance.

Misconception 1: All Title Insurance Rates Are the Same

One prevalent misconception is that title insurance rates are standardized across the board, regardless of geography. In reality, title insurance premiums can vary significantly based on state regulations. For example:

- In some states, the rates are tightly regulated, which results in less variability.

- In other states, you might find rates that differ by as much as 50%, depending on the provider and the complexity of the transaction.

Misconception 2: Title Insurance Costs Are Always High

Many homeowners believe they will always face exorbitant title insurance costs. While it’s true that certain factors influence the premium—such as property value and the type of policy—there are also considerable price ranges to consider. In fact, according to research, some homeowners have paid premiums as low as 0.5% of the property value, especially in competitive markets or due to promotional discounts from title companies.

Misconception 3: Paying More Means Better Coverage

Another common myth is that a higher premium ensures better protection. However, most title insurance policies offer similar coverage, regardless of price variations. Policy terms often include protections against the same types of risks. Therefore, paying a higher rate doesn’t necessarily equate to superior coverage.

Example Title Insurance Rates Comparison Table

| State | Average Rate (Owner’s Policy) | Average Rate (Lender’s Policy) | Regulation Type |

|---|---|---|---|

| California | $1,500 | $1,000 | Highly Regulated |

| Texas | $900 | $600 | Less Regulated |

| New York | $1,200 | $800 | Highly Regulated |

| Florida | $1,000 | $700 | Variable Rates |

Real-World Examples Highlighting Misconceptions

Consider a recent case in Florida where a homebuyer anticipated paying upwards of $2,000 based on hearsay. Upon consultation with their title insurer, they discovered a competitive rate of $1,000 due to the current promotional offer and market conditions, debunking the “high cost” myth.

Similarly, a buyer in California assumed their premium would be higher because they were purchasing in an upscale neighborhood. After checking various title companies, they managed to secure rates lower than expected by exploring options that provided comparable coverage without the presumed cost.

Practical Implications for You

It’s essential to engage in thorough research before settling on a title insurance provider. Don’t hesitate to seek quotes from multiple companies, as this can lead to significant savings. Here’s what you can do:

- Compare policy coverage in detail, not just rates.

- Ask about any discounts or promotions that could apply.

- Understand the regulations in your state, as they can impact your costs.

Specific Facts to Keep in Mind

- Always obtain multiple quotes and ask detailed questions about what’s included in the policy.

- Remember that rates can vary by as much as 50% based on location and regulation type.

- Title insurance is often a one-time premium; considering your long-term real estate investment, finding an optimal rate is worth the effort.