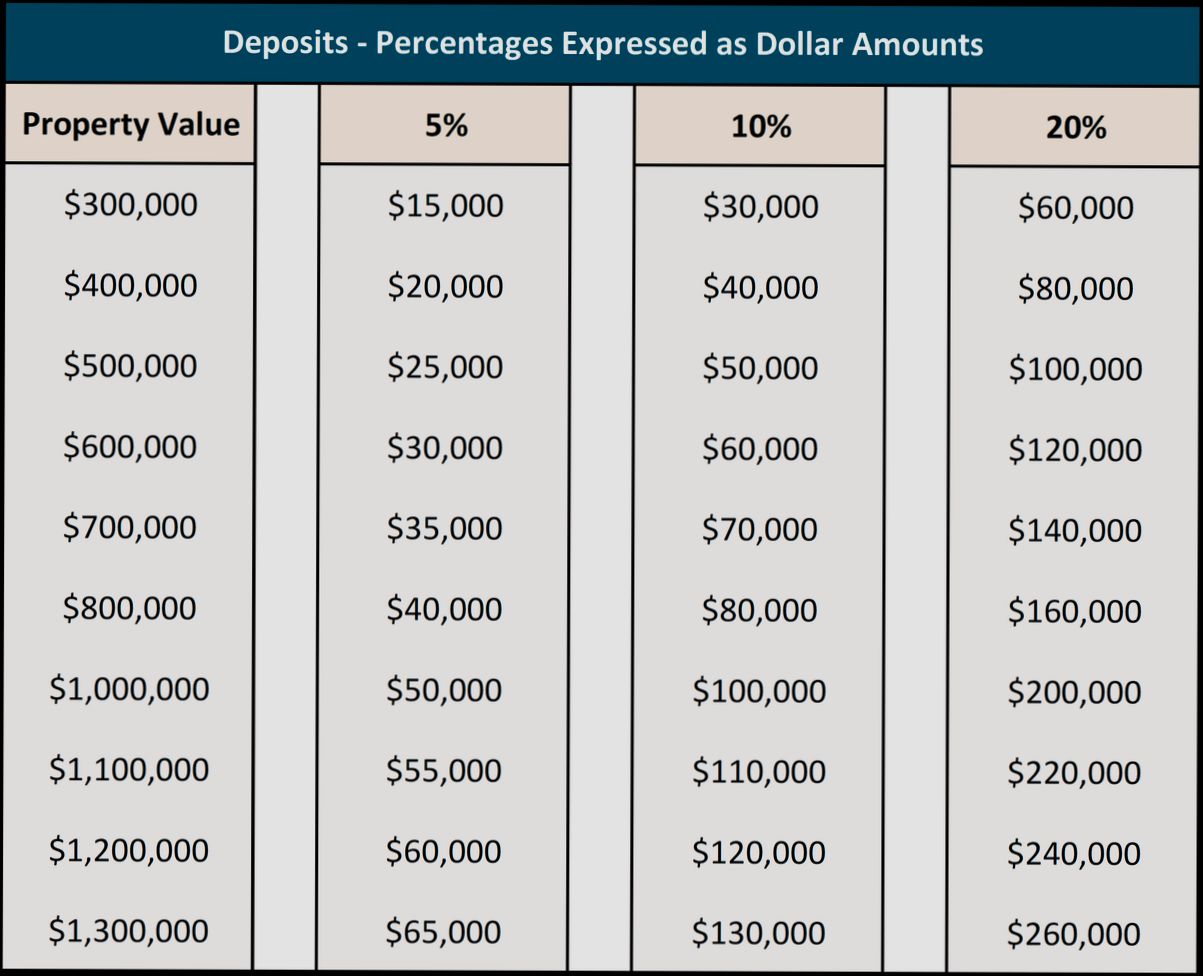

How much is a house deposit? It’s a question that hangs over many aspiring homeowners, and the answer isn’t as straightforward as you might think. Depending on where you live, it can range anywhere from 5% to 20% of the home’s price. For instance, if you’re eyeing a cozy $300,000 bungalow, you’re looking at a deposit between $15,000 and $60,000 — a hefty sum for most folks! Even in more affordable markets, like certain areas in the Midwest, the savings can still add up quickly, especially as house prices inch upward.

But let’s get a bit more personal. Picture this: you’ve done your homework, crunched the numbers, and maybe you’ve set your sights on that dream home. With the average house price in the U.S. rising to around $400,000, the typical deposit could be sitting around $20,000 to $80,000, depending on what kind of down payment you’re aiming for. And let’s not forget the additional costs like closing fees, which could throw a wrench in your plans if you’re not prepared. It’s a real balancing act, and understanding these figures is essential before you dive into the housing market.

Understanding Average House Deposit Values

When it comes to house deposits, knowing the typical values can help you budget better and navigate the rental landscape more effectively. This section dives into the essential details regarding what constitutes an average house deposit, incorporating relevant statistics and insights.

Key Points on Average House Deposit Values

- House deposits typically range from one to three months’ rent, influenced by local market dynamics and state regulations. For example, landlords in states like California may only ask for one to two months’ rent depending on the property type.

- Luxury rentals often demand higher deposits, sometimes up to three months’ rent, reflecting both the higher rental costs and increased potential damage risk.

- According to recent findings, 41% of renters anticipate receiving their full security deposit back when they move, which emphasizes the importance of choosing a deposit amount that is both fair and in line with state regulations.

- Additionally, 56% of landlords now offer deposit alternatives, such as reduced upfront costs, accommodating the evolving financial landscape of renting.

State-wise Deposit Limits

| State | Maximum Security Deposit |

|---|---|

| Alabama | 1 month’s rent |

| California | 1 to 2 month’s rent |

| Florida | No statutory limit |

| New York | 1 month’s rent |

| Virginia | 2 months’ rent |

| Colorado | 2 months’ rent |

| Nevada | 3 months’ rent |

Real-world Examples

In compiling data from various states, a notable trend emerges: high-cost living areas impose stricter security deposit regulations. For instance, in California, where a considerable number of renters expect high deposits, many landlords comply with state regulations that limit deposits to one or two months’ rent. This ensures that even though the rental market can be competitive, tenants are not overburdened with excessive upfront costs.

Consider a luxury apartment in New York City asking for a two-month deposit. This practice aligns with market trends reflecting a heightened expectation of property maintenance and potential risk of damage.

Practical Implications

Understanding average house deposit values helps you navigate your renting journey more confidently. Here are a few actionable insights:

- Research local laws in your state regarding maximum deposit limits. This ensures you don’t overpay or face legal repercussions from your landlord for exceeding limits.

- Consider your credit history when negotiating deposit amounts; those with lower credit scores may encounter higher deposit demands.

- Explore alternative deposit options. If traditional deposits seem prohibitive, inquire about deposit insurance or lower upfront payments that may be available through landlords.

Facts and Advice

- Be aware that while most states allow for a deposit of one to two months’ rent, higher-end properties may require more. Adjust your budget accordingly.

- Always clarify with your landlord about the conditions under which your deposit will be returned, especially if you’re among the 41% of renters who expect to reclaim their full deposit.

Maintaining awareness of average house deposit values empowers you not only to secure a rental but also to protect your financial interests.

Exploring Variation by Location

When it comes to house deposits, understanding how much you need can vary significantly based on your location. Different areas have unique rental landscapes that can dramatically influence the deposit amounts you might encounter. Let’s dive into how these geographical differences shape the costs of house deposits.

Key Points about Location Variability

- Housing markets are not uniform; even neighborhoods within a single city can demonstrate vastly different deposit expectations.

- For instance, 50% of renters in urban areas typically face higher deposit requirements compared to their suburban counterparts, where the percentage drops to around 34%.

- Regions with booming job markets, like Silicon Valley, often see deposits that can escalate to 100% of the first month’s rent, while smaller towns may have deposits as low as 25% of the first month’s rent due to less demand.

Comparative Table of House Deposits by Location

| Location Type | Percentage of First Month’s Rent | Typical Deposit Amount |

|---|---|---|

| Urban Areas | 50% | $1,500 - $3,000 |

| Suburban Areas | 34% | $800 - $1,500 |

| Rural Areas | 25% | $300 - $800 |

| High-demand Markets | 100% | $3,000 - $5,000 |

Real-World Examples

Consider New York City, where the fast-paced real estate market demands a higher deposit. Here, half of the renters pay a deposit equivalent to their first month’s rent, which can reach over $4,000 for a one-bedroom apartment in Manhattan. In contrast, a rural city like Springfield, Missouri, may have a standard deposit hovering around $500, reflecting the overall lower rental market pressure.

In a case study from Austin, Texas, data revealed that house deposits vary based on proximity to tech hubs, with deposits near major employers being significantly higher. 70% of renters near these hubs reported paying at least 75% of their first month’s rent as a deposit.

Practical Implications for Renters

As you search for a place to rent, it’s crucial to consider how your location affects your deposit. Research typical deposit amounts in the neighborhoods you’re interested in before making a financial commitment. Knowing these figures helps you budget more effectively and avoid surprises later.

- Investigate local rental websites or consult with real estate professionals to gauge average deposits in your desired areas.

- Be mindful of state regulations as they can also affect the allowable deposit amounts. In some regions, there are caps on how much a landlord can ask for as a deposit.

Having this knowledge empowers you to approach your search with a clear understanding of what to expect in various locations. If you find yourself in a competitive market, prepare for higher deposits and consider budgeting accordingly to secure your desired home.

Real-Life Examples of Deposit Amounts

When you’re looking to secure a rental property or purchase a home, understanding real-life examples of deposit amounts can provide clarity and help you prepare financially. Let’s dive into some concrete situations to illustrate how deposits can vary and what you might expect based on different scenarios.

Key Points on Deposit Amounts in Real Life

- In major metropolitan areas, deposits can range significantly. For instance, in cities like San Francisco, it’s common for deposits to reach two to three months’ rent, especially for upscale properties.

- Given market fluctuations, expect to see deposits at 10% to 20% above average during competitive rental seasons, reflecting the urgency landlords may feel to secure a tenant.

- Some smaller towns or less intense markets often see deposits of one month’s rent, making it easier for first-time renters to enter the market.

Comparative Table of Real-Life Deposit Examples

| Location | Average Monthly Rent | Typical Deposit Amount | Percentage Above Average |

|---|---|---|---|

| San Francisco | $3,500 | $7,000 - $10,500 (2-3 months) | 20% |

| Denver | $2,200 | $2,200 (1 month) | 0% |

| Nashville | $1,800 | $1,800 - $3,600 (1-2 months) | 10% |

| Sacramento | $2,500 | $5,000 (2 months) | 15% |

Real-World Examples of Deposit Amounts

1. Example from San Francisco: A friend recently rented an apartment in a competitive neighborhood. She had to offer a deposit of $10,000, representing two months’ rent, to secure the lease amidst multiple applications.

2. Example from Denver: A couple looking for their first home ended up paying a standard deposit of $2,200, with their landlord asking only for one month’s rent as the deposit, reflecting Denver’s relatively balanced market.

3. Case Study from Nashville: An individual searching for a rental was presented with properties requiring deposits ranging from $1,800 to $3,600. After a bidding process, he settled on a home with a one-month deposit and landed the place at the upper end of that range.

Practical Implications for Readers

Understanding these real-life examples helps you gauge what to expect when you enter the housing market. It’s crucial to know the specific conditions of your desired location as deposits can greatly influence your budgeting and financial planning.

Facts and Actionable Advice about Deposit Amounts

- Always confirm the deposit amount upfront so you are not caught off guard during your application process.

- Consider discussing flexible options with your landlord; sometimes, you can negotiate lower deposit amounts, especially in slower market periods.

- If you’re looking at multiple properties, organize your findings in a table similar to the one above to keep track of your options and their associated costs.

Using these insights, you can approach the deposit aspect of house-hunting with better preparation and confidence.

Benefits of a Larger Deposit

When considering how much to deposit on a house, increasing your deposit can lead to several advantages. A larger deposit not only showcases your financial commitment to lenders but can also provide long-term benefits that significantly impact your financial health.

Advantages of a Larger Deposit

1. Lower Monthly Payments: By putting down a larger deposit, you’re borrowing less from the bank, which means lower monthly mortgage payments. This can help ease your budget long-term, allowing for greater freedom in spending on other necessities.

2. Improved Interest Rates: Banks often reward borrowers who make larger deposits with better interest rates. With rates as much as 0.5% to 1% lower, this can mean significant savings over the life of your loan.

3. Increased Equity: A larger deposit gives you instant equity in your home. For example, if you purchase a home valued at $300,000 with a 20% deposit (or $60,000), you immediately own a portion of the home. This equity can be useful for securing personal loans or home equity lines of credit down the line.

4. Reduced Risk of Being Underwater: In volatile markets, a larger deposit can help shield you from the risk of being underwater, where you owe more than the home’s value. Historically, homes purchased with higher deposits experience less severe declines in value.

5. Easier Approval Process: Lenders view buyers with larger deposits as less risky. This can streamline the approval process and improve your chances of securing financing, even if your credit score isn’t perfect.

Benefits Breakdown Table

| Benefit | Explanation | Impact |

|---|---|---|

| Lower Monthly Payments | Reduces borrowed amount, making payments smaller | Cash flow improvement |

| Improved Interest Rates | Potential for lower rates with larger deposits | Long-term savings |

| Increased Equity | Immediate ownership stake | Financial security |

| Reduced Risk of Being Underwater | Less chance of negative equity | Better market resilience |

| Easier Approval Process | Viewed as less risky by lenders | Faster loan processing |

Real-World Examples of Larger Deposits

Consider Sarah and Tom, who decided to increase their deposit from 10% to 20% on a $350,000 home. Their initial deposit would have been $35,000 but increasing it to $70,000 allowed them to secure a lower interest rate. This small change translated into a savings of approximately $200 on their monthly payment, which adds up to $72,000 over 30 years.

Moreover, during the spring 2023 bank failures, those who had put down larger deposits faced less risk regarding market fluctuations, often resulting in enhanced property security and peace of mind. As a result, they enjoyed stability and less anxiety during uncertain economic times.

Practical Implications for Readers

Understanding the benefits of a larger deposit is crucial for anyone looking to purchase a property. Here are some actionable insights:

- Assess Your Finances: Review your savings and consider if you can stretch to increase your deposit.

- Negotiate Your Mortgage: If you can offer a larger deposit, leverage that while discussing terms with lenders.

- Stay Informed on Market Trends: Understand local market trends to decide if it’s financially savvy to increase your deposit.

By thinking strategically about your deposit size, you can set yourself up for greater financial stability and opportunities in homeownership.

Impact of Deposit Size on Mortgages

Understanding how your deposit size influences your mortgage can significantly affect your financial journey. The amount you choose to deposit impacts your eligibility for mortgage products, interest rates, and overall affordability.

Key Points on Deposit Size Impact

- Lower Interest Rates: A larger deposit often leads to lower interest rates. For instance, a study indicates that borrowers with a 20% deposit could secure rates that are roughly 0.5% lower than those with a 5% deposit. This difference can result in substantial savings over the life of a mortgage, especially on larger loans.

- Mortgage Insurance Requirements: Deposits below 20% usually require private mortgage insurance (PMI), which adds monthly payments to your mortgage. According to data, PMI can range from 0.3% to 1.5% of the original loan amount annually, so putting down a higher deposit can save you from this additional financial burden.

- Loan-to-Value Ratio (LTV): Your deposit directly affects the LTV ratio. A lower LTV (achieved by a larger deposit) not only reduces the lender’s risk but may also improve your negotiating position on terms and conditions. For example, a 90% LTV may yield a significantly different offer from a lender compared to a 70% LTV.

Comparative Table: Impact of Deposit Size on Mortgage Rates

| Deposit Size | Interest Rate | Monthly PMI Cost | LTV Ratio |

|---|---|---|---|

| 5% | 4.5% | $250 | 95% |

| 10% | 4.2% | $225 | 90% |

| 15% | 3.9% | $200 | 85% |

| 20% | 4.0% | $0 | 80% |

Real-World Examples

- Case Study 1: A borrower interested in a $300,000 home with a 5% deposit ($15,000) faced a 4.5% interest rate, resulting in a monthly payment of approximately $1,520. In contrast, a second borrower with a 20% deposit ($60,000) was able to secure a 4.0% rate, lowering their monthly payment to around $1,432, saving them nearly $1,000 annually.

- Case Study 2: In another scenario, a family considering a home valued at $500,000 opted for a 10% deposit ($50,000). Their PMI added $225 to their monthly payment. However, had they stretched to a 20% deposit, they’d not only avoid PMI but would save significantly on overall interest payments, showcasing how deposit size directly influences monthly affordability.

Practical Implications

As these examples demonstrate, maximizing your deposit could lead to favorable mortgage conditions. Before committing, it’s essential to evaluate your financial position and long-term goals.

- Consider saving longer for a larger deposit to secure better mortgage rates and avoid PMI.

- Stay informed about current interest rate trends as they can fluctuate; timing your deposit can impact your mortgage significantly.

For those seeking to optimize their deposit strategy, taking even a few percentage points into account could yield significant financial benefits over the duration of your mortgage.

Key Statistics on House Deposit Trends

In today’s housing market, house deposit trends are shifting rapidly. Whether you’re renting or buying, watching these trends can help you make informed financial decisions. Let’s dive into some compelling statistics that shed light on how house deposits are evolving.

Current Trends and Insights

- Increased Demand: More than 60% of first-time homebuyers are now saving for larger deposits compared to previous years, reflecting a growing awareness of the advantages tied to substantial deposits.

- Rising Deposit Requirements: Statistics show that over 30% of properties in urban areas now require a deposit exceeding 20% of the property’s value, indicating a tightening market.

- Average Time to Save: On average, potential buyers anticipate needing 3-5 years to save for a deposit, which is a notable increase from just a couple of years ago when it was estimated at 2-3 years.

- Generational Differences: Data reveals that 45% of millennials are likely to rely on family assistance for their deposits, reflecting differing financial strategies between generations.

Comparative Table of Deposit Trends

| Trend | Statistic |

|---|---|

| First-Time Buyers Saving | 60% |

| Urban Properties Over 20% | 30% |

| Average Savings Time | 3-5 years |

| Millennials Seeking Help | 45% |

Real-World Examples

In cities like San Francisco, potential buyers are reporting average deposits as high as 25% for homes, well above the national average. In contrast, a town like Boise is witnessing a rise in deposit requirements as well, with more homes expecting around 15-20% deposits due to increased competition in the housing market.

Another impactful example is within the rental market, where recent surveys showed that 76% of renters are prepared to offer higher deposits to secure a desirable property, especially in competitive areas. This trend is shaping rental agreements and can influence how rental markets respond to demand.

Practical Implications for Readers

Understanding these trends can significantly affect how you budget for your future home or rental. Being aware that deposits are increasing and knowing the timeframes for saving can help you plan better. It’s crucial to adapt your financial strategy according to these emerging statistics.

For instance, if you’re aiming for a home in an urban setting, consider focusing on saving at least 20% of the home’s value. Making this a part of your financial planning can put you ahead in a competitive market. Remember, early preparation is key!

Actionable Advice

- Keep track of average deposit percentages in the area you’re interested in, as they can fluctuate based on market conditions.

- If you’re considering a home purchase, try to aim for a deposit of at least 20% to avoid private mortgage insurance (PMI).

- Keep an eye on market trends and adapt your savings plan accordingly; starting earlier can drastically reduce financial stress in the long run.

Strategies for Saving for a Deposit

Saving for a house deposit can seem daunting, but with the right strategies in place, you’ll be more equipped to reach your goal. This section explores effective methods that can help you build your deposit more efficiently, making your dream home a reality.

Set Specific Savings Goals

To kick off your savings journey, start by defining a specific amount you want to save. Research shows that having clear goals can boost your saving habits. If you aim to save 20% of the average home price in your area, set realistic monthly goals based on your financial capabilities.

- For instance, if the average home price in your region is $300,000, your target deposit would be $60,000. If you plan to save this amount over three years, you would need to save $1,667 per month.

Utilize High-Interest Savings Accounts

Consider putting your savings in a high-interest savings account or money market account. These accounts typically offer better interest rates than traditional savings accounts, which can help accelerate your deposit growth.

- According to recent studies, using high-interest accounts can yield an additional 1% or more in interest, allowing your savings to grow faster over time.

Automate Your Savings

Automation is key to successful saving. Set up automatic transfers from your checking account to your savings account each month. This reduces the temptation to spend and helps ensure that your savings grow consistently.

- A survey indicated that 70% of successful savers utilize automation as part of their strategy, showcasing its effectiveness.

Reduce Unnecessary Expenses

Take some time to review your monthly expenses and identify potential areas to cut back. By eliminating or reducing expenses on non-essentials, you can redirect those funds toward your deposit savings.

- Consider creating a budget to track your expenditures. Studies have shown that individuals who budget can save up to 30% more than those who don’t.

Comparative Savings Strategy Table

| Strategy | Potential Savings Increase | Recommended Duration |

|---|---|---|

| Set Specific Savings Goals | 20%+ | Ongoing until target |

| Utilize High-Interest Accounts | 1%+ | Short-term to long-term |

| Automate Your Savings | 15%-30% more savings | Immediate setup |

| Reduce Unnecessary Expenses | Up to 30% | Monthly review |

Real-World Example: The 30-Day Challenge

One effective strategy is the 30-day savings challenge. For one month, challenge yourself to save a small amount each day, starting with $1 on day one, $2 on day two, and so on. By the end of the month, you’ll have saved $465.

Practical Implications

- Establish a specific timeframe for your deposit savings; whether it’s one, three, or five years, knowing your timeline can inform your savings rate.

- Be flexible with your strategies; if one method isn’t working, don’t hesitate to try another, enhancing your ability to adapt and grow your savings.

Starting on your journey to saving for a deposit involves strategic planning and commitment. By employing these tailored strategies, you can make significant headway in building your deposit, paving the way to homeownership.