Blog

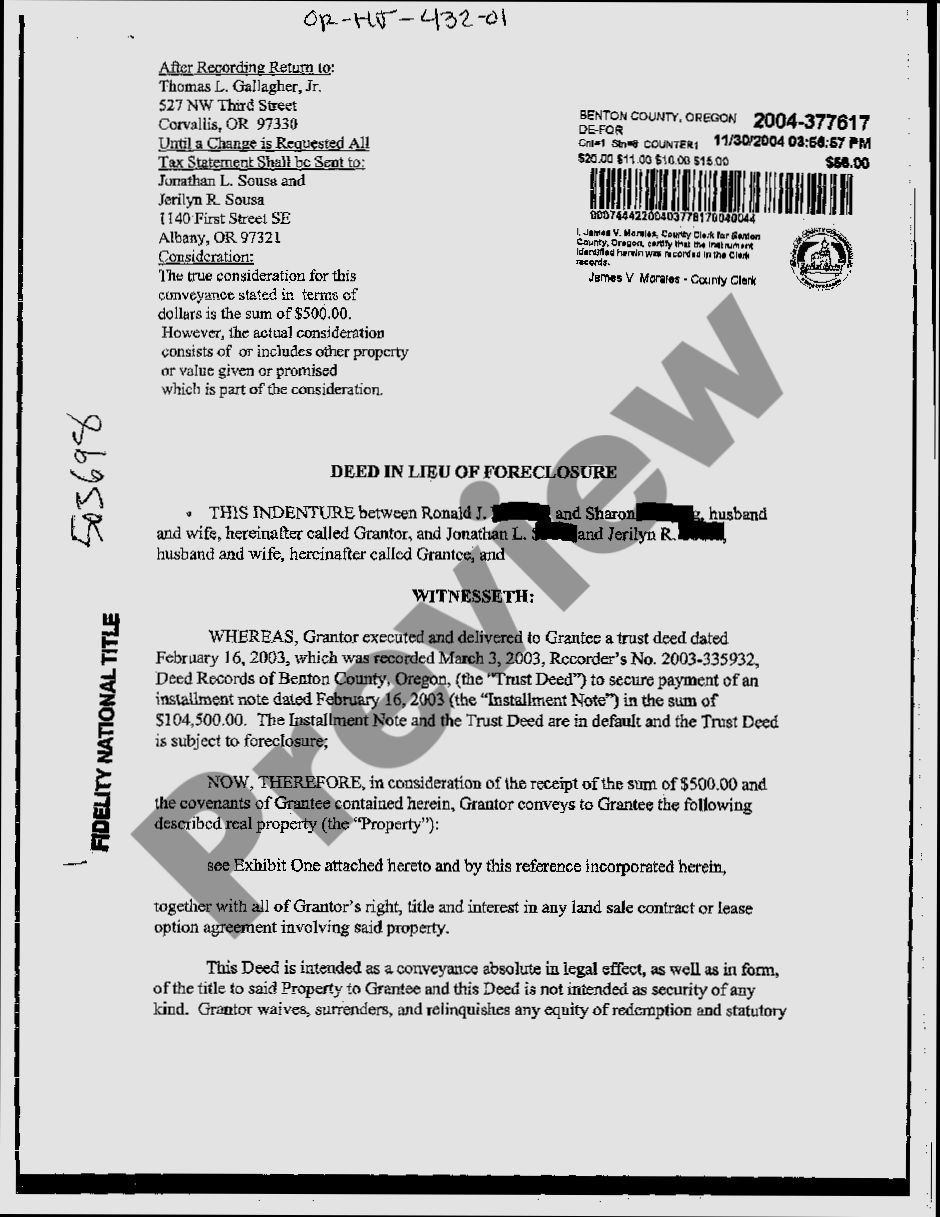

What is a Deed in Lieu of Foreclosure

What is a Deed in Lieu of Foreclosure? Simply put, it’s when a homeowner hands over their property deed to the lender, essentially trading the house for relief from their mortgage debt. Imagine you’re in a tight spot, maybe you’ve lost your job or faced unexpected medical expenses that made your mortgage payments impossible. You owe $200,000 on your home, but it’s only worth $150,000 in today’s market. Instead of dragging out the ordeal through a lengthy foreclosure, a deed in lieu lets you and the bank settle things more amicably.

What is a Liveable Salary in Málaga

What is a Liveable Salary in Málaga? Well, if you’re dreaming of sunny beaches, vibrant culture, and delicious tapas while working in Spain, you’ll want to know what it takes to make ends meet here. On average, a liveable salary for a single person in Málaga floats around €1,400 to €1,800 per month after taxes. This figure lets you enjoy a comfortable lifestyle, covering essentials like rent, groceries, and transportation without feeling strapped for cash. For example, a decent one-bedroom apartment in the city center typically costs about €800 a month, while eating out at a local café usually runs around €10 for a satisfying meal.

What is a Mortgage Loan Originator

What is a Mortgage Loan Originator? Imagine you're gearing up to buy your first home, and suddenly you find yourself buried under a mountain of paperwork, interest rates, and terms like amortization that sound like a foreign language. That's where a mortgage loan originator (MLO) comes into play. These professionals are your go-to guides in the mortgage maze. According to the Bureau of Labor Statistics, there were about 324,000 loan officers in the U.S. as of 2021, each of them playing a key role in helping buyers navigate the often-confusing landscape of home financing.

What is a Real Estate Broker

What is a Real Estate Broker? Think of them as your go-to guide in the wild world of buying and selling property. They’re licensed professionals who connect buyers and sellers, and they know the ins and outs of the market like the back of their hand. For example, in 2022, 88% of home buyers used an agent or broker to navigate their purchase. These folks don’t just post listings; they provide strategic advice, negotiate deals, and can even help determine the right price for a property based on local trends and recent sales.

What is a Real Estate Estoppel

What is a Real Estate Estoppel? Imagine you've just signed a lease for your new apartment, all those exciting plans buzzing in your mind. But before everything settles, the landlord hands you an estoppel certificate. This legal document confirms the specifics of your lease, including rental terms, security deposits, and any potential disputes between you and the landlord. For instance, if you’re paying $1,500 a month and have a pet policy that allows Fido on the premises, the estoppel certifies these terms—crucial if disputes arise later or if the property changes hands.

What is a Real Estate Syndication

What is a Real Estate Syndication? Picture this: a group of investors joins forces to pool their money and buy a multi-family apartment building or commercial property, something most of them couldn’t afford alone. For example, if a building costs $2 million, a syndication might include 20 investors each contributing $100,000. This setup not only lowers the financial barrier to entry for individuals but also opens the door to potentially lucrative real estate deals that can generate rental income and appreciation.

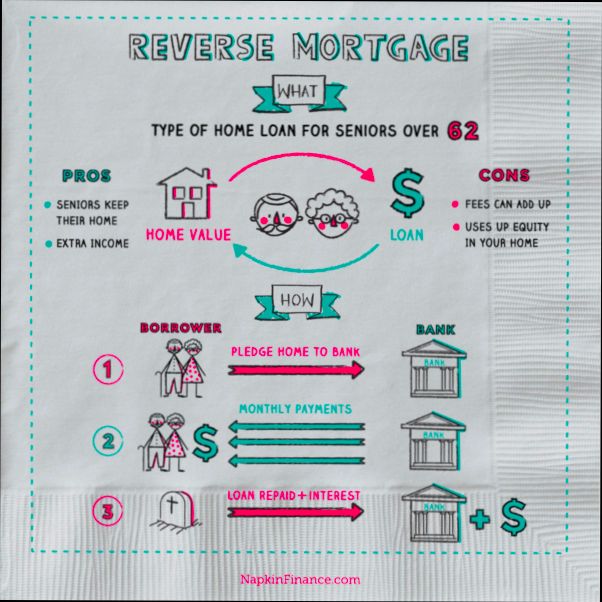

What is a Reverse Mortgage Loan

What is a Reverse Mortgage Loan? Picture this: you're in your golden years, enjoying retirement, but your budget feels tighter than ever. A reverse mortgage could be a way to tap into the equity of your home, allowing you to turn part of that ownership into cash without selling your beloved abode. For example, according to the National Reverse Mortgage Lenders Association (NRMLA), the average reverse mortgage borrower is around 72 years old and can access anywhere from $50,000 to $100,000 or more, depending on their home’s value and age.

What is a Tax Credit Apartment

What is a Tax Credit Apartment? It’s a pretty cool option for renters looking for affordable living. These apartments are part of the Low-Income Housing Tax Credit (LIHTC) program established back in 1986 to help tackle the affordable housing crisis. With this program, developers get tax breaks for building or renovating properties, which in turn allows them to keep rents lower—often at around 30% of a tenant’s income. For example, if you’re earning $40,000 a year, you could be looking at rent around $1,000 a month, significantly less than the market average in many urban areas.

Tags