Blog

Forecast of the Investment Climate in Europe for 2025

Forecast of the Investment Climate in Europe for 2025 is looking more dynamic than ever. With the EU’s Green Deal pushing for a massive transition to renewable energy, we’re seeing a surge in investments projected to hit around €1 trillion by mid-decade. Sectors like solar and wind energy are booming, fueled by government incentives and corporate sustainability goals. For instance, Germany is ramping up its green tech investments, aiming for renewable sources to satisfy 80% of its energy needs by 2030. That’s not just good for the environment; it's creating countless opportunities for investors.

Guide to Property Rental Laws for Landlords in Germany

Guide to Property Rental Laws for Landlords in Germany dives into the intricacies of managing rental properties in a country famous for its robust tenant protections. Did you know that around 45% of Germans live in rented homes? This statistic highlights just how vital it is for landlords to understand their responsibilities and rights. For example, the German Civil Code (BGB) offers extensive regulations around rent increases, with limits typically tied to inflation rates. If you’re considering adjusting your rent, you’ll need to navigate rules around what’s possible and when you can do it—miss a step and you could be looking at a lot more than just a friendly chat with your tenant.

Guide to Property Rental Laws for Landlords in Spain

Guide to Property Rental Laws for Landlords in Spain lays the groundwork for navigating the vibrant yet sometimes tricky rental landscape. Did you know that as of 2023, about 20% of Spain's population rents their homes? That’s a staggering figure, especially in cities like Barcelona and Madrid, where property demand can feel more like a rollercoaster. It's not just about putting up a For Rent sign; understanding your rights and responsibilities is crucial. For instance, did you know that landlords are required to provide specific documentation, like energy performance certificates, before renting? It’s one of those details that can trip you up if you’re not in the know.

Hotel License Revoked at Malaga Haunted House

Hotel License Revoked at Malaga Haunted House – talk about a jaw-dropper! This quirky spot, famous for its spooky gimmicks and spine-tingling tours, just lost its hotel license due to a series of safety violations. Local authorities discovered multiple fire code violations, including blocked emergency exits and outdated smoke detectors, during a routine inspection. Seriously, who thought it was a good idea to let guests stay over in a haunted house without proper safety measures? With an average of 500 visitors a month, this place was raking in the cash but neglecting basic safety standards.

How to buy house in Spain for 1 euro

How to buy a house in Spain for 1 euro is one of those eye-catching headlines that makes you stop scrolling and wonder if you’ve stumbled upon the deal of a lifetime. Yes, you read that right—some towns across Spain are actually selling homes for just a single euro! These incredible offers often pop up in rural areas struggling with depopulation. The local governments are eager to attract new residents, which means you can potentially snag a charming fixer-upper in a picturesque village for the price of a coffee.

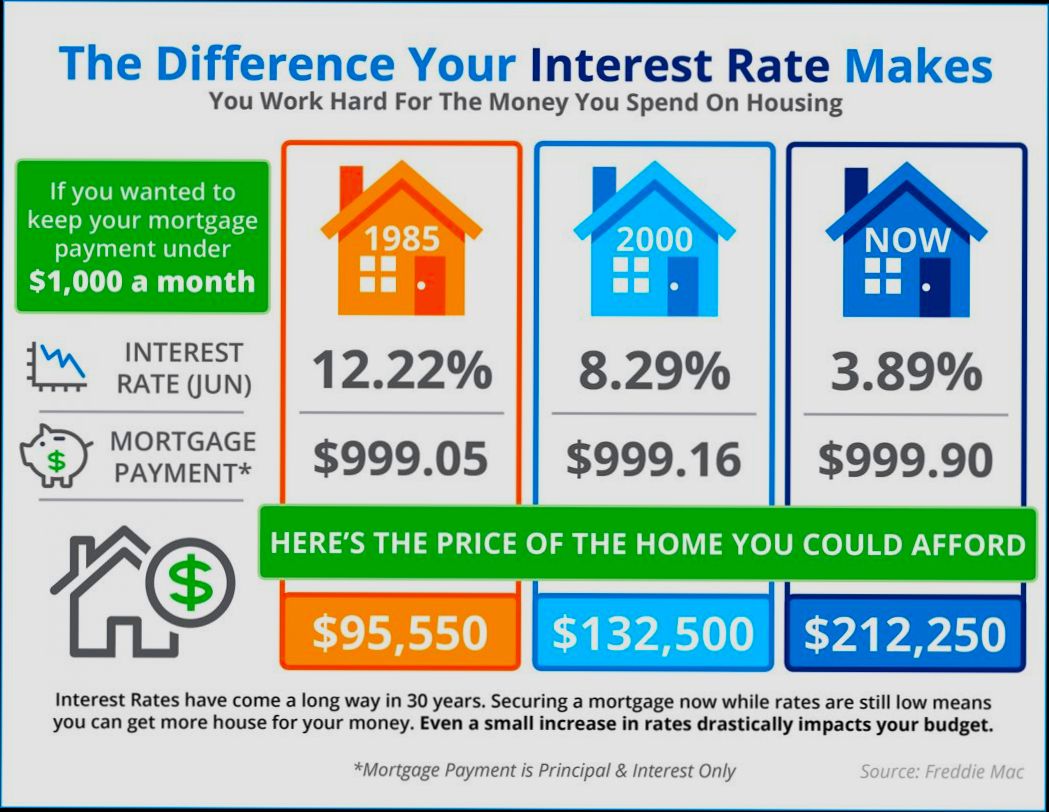

How an Interest Rate Rise Could Impact Your Mortgage Repayments

How an Interest Rate Rise Could Impact Your Mortgage Repayments is something every homeowner should pay attention to, especially in today’s volatile economic climate. Picture this: if the Federal Reserve bumps up interest rates by just 0.25%, the effect could ripple through your monthly payments. For someone with a $300,000 mortgage at a 3% fixed rate, that small increase could push the monthly payment from about $1,265 to around $1,350. Over the life of a 30-year loan, you’re suddenly looking at paying nearly $27,000 more in interest! Yikes, right?

How Can I Get a Mortgage Approval

How Can I Get a Mortgage Approval? That's the million-dollar question for countless first-time homebuyers out there. You might have heard that over 40% of mortgage applications get denied, which is a reality check for many. Imagine finding your dream home only to be turned away by the bank because of a low credit score or insufficient income. In 2022, the average credit score for approved loans was around 751, so if yours isn’t in that ballpark, it’s time to pay attention.

How Can You Encourage People to Buy Your Home

How Can You Encourage People to Buy Your Home? Imagine your listing sitting pretty among countless others, yet it still feels like yours is the only one grabbing attention. With the right strategies, you can create that buzz. Did you know that homes staged effectively sell for an average of 17% more than their unstaged counterparts? That’s real money talking! Consider that homes with high-quality photos receive 70% more views online than those with dark, blurry images. You want potential buyers scrolling through their feeds to stop in their tracks and envision their life in your space.

Tags