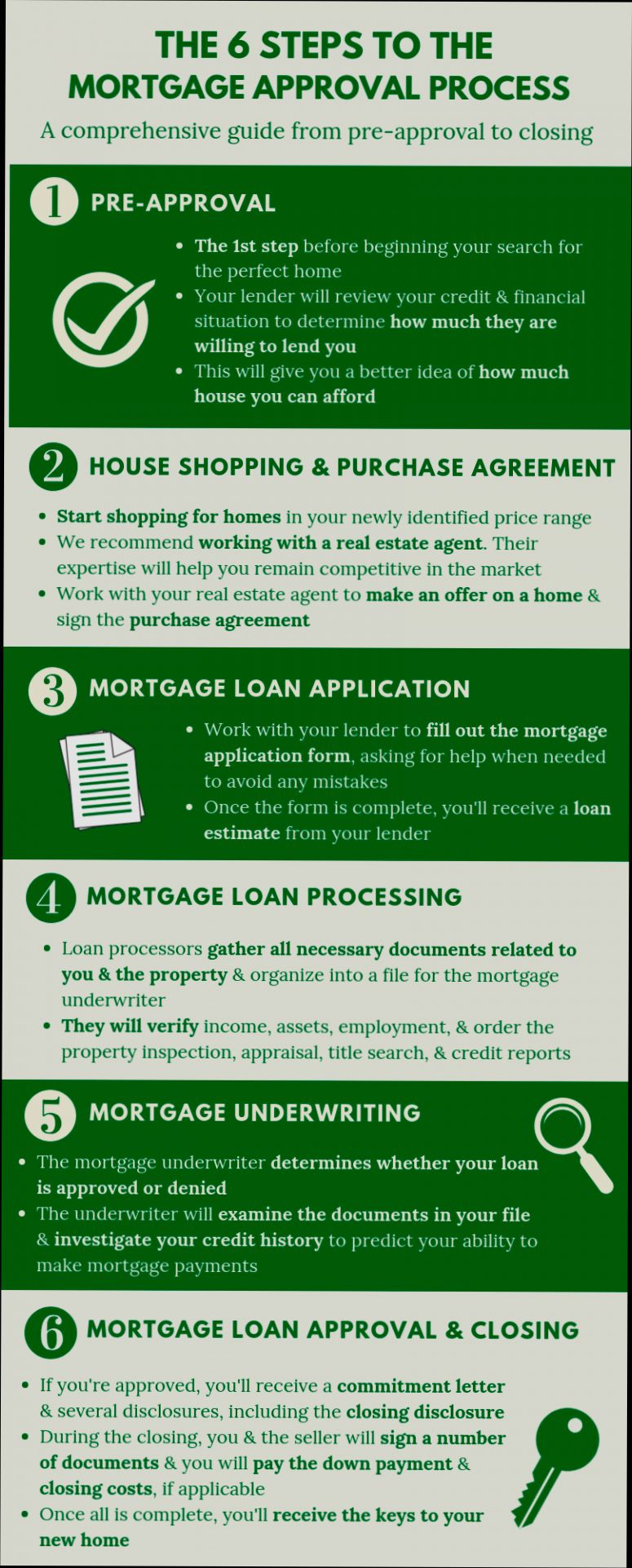

How Can I Get a Mortgage Approval? That’s the million-dollar question for countless first-time homebuyers out there. You might have heard that over 40% of mortgage applications get denied, which is a reality check for many. Imagine finding your dream home only to be turned away by the bank because of a low credit score or insufficient income. In 2022, the average credit score for approved loans was around 751, so if yours isn’t in that ballpark, it’s time to pay attention.

And it’s not just about your credit score; lenders also look at your debt-to-income (DTI) ratio. Ideally, you want your monthly debts to be no more than 36% of your gross income. If you’re making $5,000 a month but struggling with student loans and credit card debt that gobbles up $2,000, you might be on shaky ground. A friend of mine found this out the hard way when he applied for a mortgage but couldn’t get through because his DTI ratio was a whopping 45%. Knowing the numbers and what lenders care about can help you avoid heartache down the road.

Understanding Your Credit Score Impact

Your credit score plays a pivotal role in determining whether you’ll get mortgage approval and what interest rates you’ll secure. This score, which typically ranges from 300 to 850, reflects your credit risk to lenders. Knowing how your credit score impacts your chances can significantly influence your mortgage journey.

Key Factors That Influence Your Credit Score

Understanding what constitutes your credit score can help you take actionable steps to improve it. Here are the primary components:

- Payment History (35%): This is the most significant factor. If you consistently make payments on time, it will positively impact your score. For instance, a missed payment can drastically lower your score.

- Credit Utilization (30%): Aim to keep your credit utilization below 30% of your total available credit. For example, if your total credit is $10,000, keep your balance under $3,000 to maintain a healthy score.

- Length of Credit History (15%): The longer you have credit accounts open, the better. It shows lenders you have experience managing credit effectively.

- Credit Mix (10%): Having a variety of credit types, such as credit cards and installment loans, can boost your score.

- New Credit (10%): Opening multiple new accounts within a short period can signal risk to lenders, negatively affecting your score.

Comparative Score Table

| Credit Score Type | FICO® Score | VantageScore |

|---|---|---|

| Exceptional | 800 to 850 | 781 to 850 |

| Very Good | 740 to 799 | 661 to 780 |

| Good | 670 to 739 | 601 to 660 |

| Fair | 580 to 669 | 500 to 600 |

| Poor | 300 to 579 | 300 to 499 |

Real-World Example of Credit Score Impact

Let’s say you have a FICO® Score of 700. While this score may seem good, you might still be categorized as a “Good” credit risk. On the other hand, a score of 740 or higher places you in the “Very Good” category. The difference can lead to significantly better mortgage rates due to perceived lower risk.

For instance, if you’re shopping for a mortgage, a lender might offer a 3.5% interest rate for a borrower with a score of 740. Meanwhile, a borrower with a score of only 700 might face rates closer to 4%, meaning they’ll pay much more in interest over the life of the loan.

Practical Implications for Your Mortgage Approval

Understanding the elements that contribute to your credit score allows you to take specific actions to improve it:

- Start by checking your credit reports for errors or outstanding payments.

- Manage your credit utilization: Keep your balances low compared to your limit.

- Limit new credit applications: Avoid opening new accounts right before applying for a mortgage.

Actionable Insights

Here are some quick tips to enhance your credit score before applying for a mortgage:

- Make all payments on time, as late payments hurt your credit score significantly.

- If your credit utilization is high, consider paying down existing debts.

- Keep old credit accounts open to support the length of credit history.

By focusing on these aspects, you can improve your credit score and increase your chances of mortgage approval.

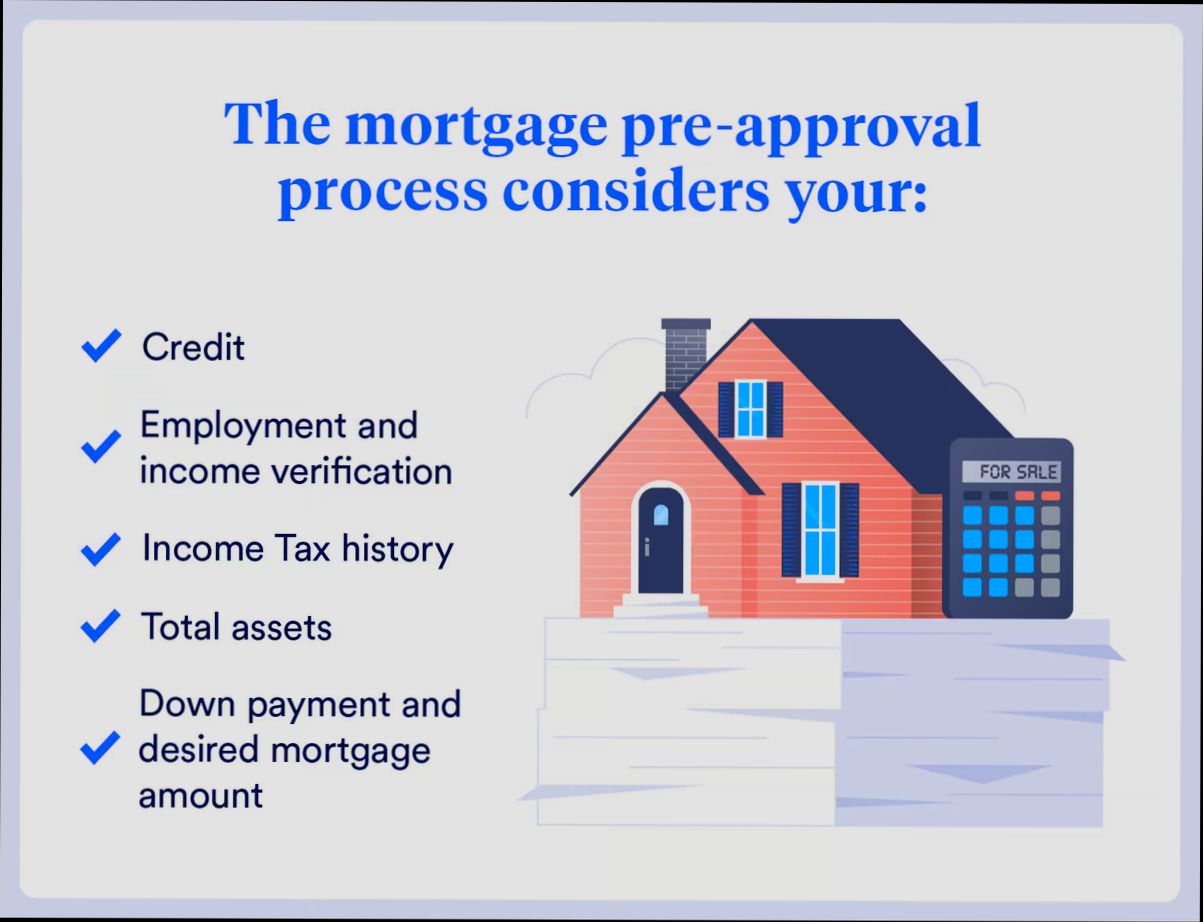

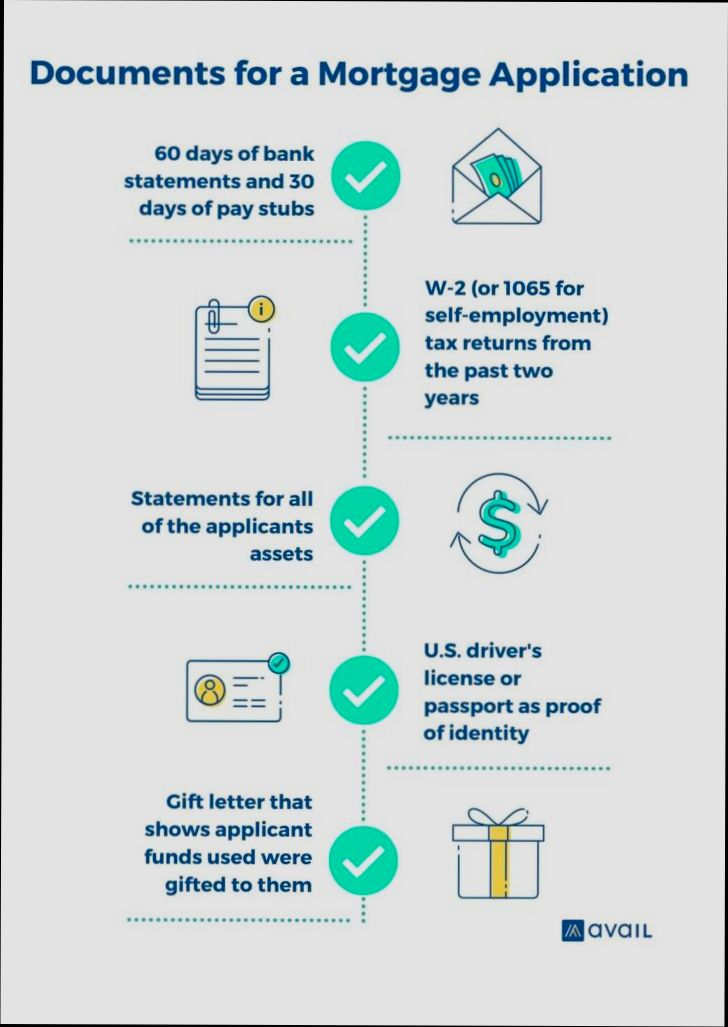

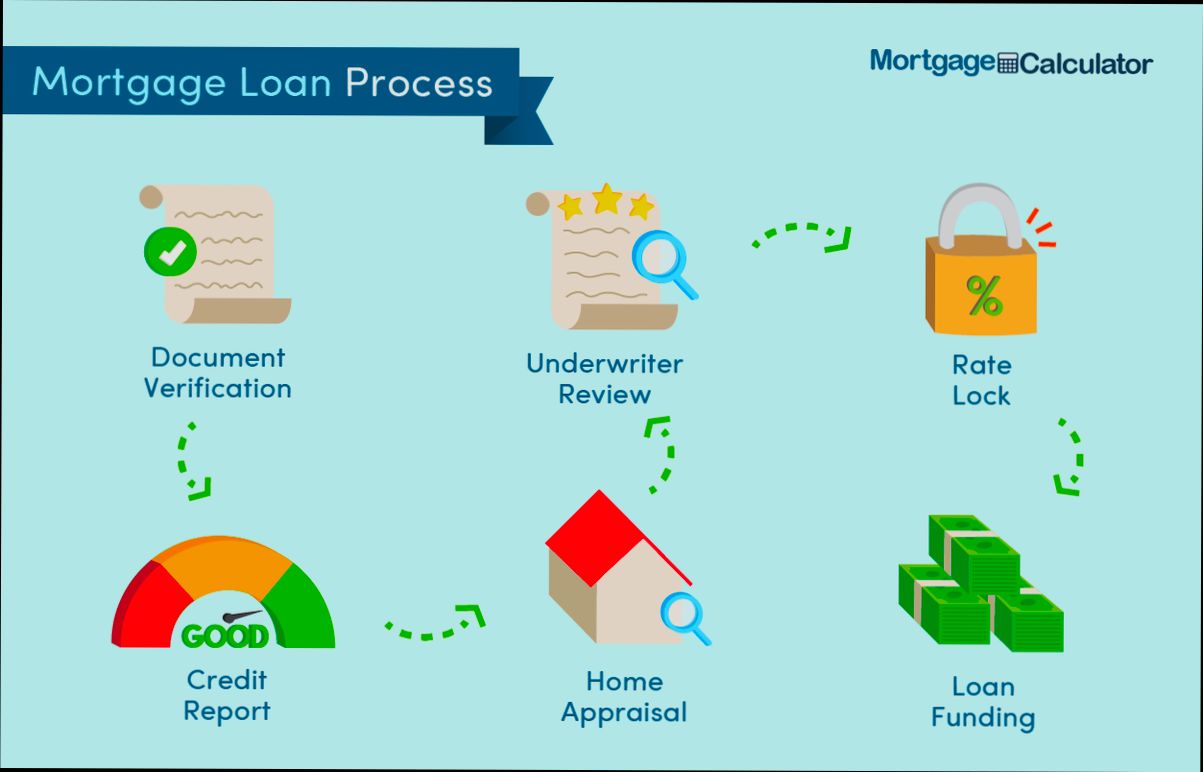

Essential Documentation for Loan Application

When you’re gearing up to apply for a mortgage, having the right documentation can make all the difference in your approval journey. Essential documentation lays the groundwork for your financial profile, assisting lenders in evaluating your creditworthiness, financial health, and capability to repay the loan. Let’s explore the critical documents you need to gather before taking that big step toward homeownership.

Key Documentation Requirements

To navigate the loan approval process smoothly, you’ll need to prepare several key documents:

- Proof of Identity: This can include:

- A government-issued passport

- A driver’s license

- A national ID card

- Proof of Address: Ensure you submit recent utility bills or rental agreements verifying your current residence.

- Proof of Income: This is crucial for showing your ability to manage loan repayments. Types of income documentation you may need include:

- Last two pay stubs

- Employment contracts or offer letters

- Bank statements reflecting regular salary deposits

- Invoices for self-employed borrowers

- Financial Statements: Providing recent bank statements for all your accounts can help lenders evaluate your financial habits and liquidity.

- Property Documents: If you’re purchasing a property, you’ll also need:

- Title deeds: Confirm ownership and validate collateral.

- Property valuation reports: These ensure that the loan amount aligns with the property’s market value and help determine the loan-to-value ratio.

Comparative Table of Essential Documents

| Document Type | Purpose | Common Requirements |

|---|---|---|

| Proof of Identity | Verify borrower identity | ID card, passport, or driver’s license |

| Proof of Address | Confirm current residency | Utility bills or lease agreements |

| Proof of Income | Assess repayment capacity | Pay stubs, bank statements, contracts |

| Financial Statements | Evaluate financial status | Recent bank statements |

| Property Documents | Validate collateral for the loan | Title deeds and valuation reports |

Real-World Examples

1. Case Study - Proof of Income: Sarah recently applied for a mortgage and provided her pay stubs, employment contract, and bank statements showing consistent deposits. This comprehensive documentation helped her secure approval faster since lenders quickly verified her financial stability.

2. Case Study - Property Valuation: John was interested in a home valued at $300,000. He submitted a recent property valuation report prepared by a certified appraiser. The lender used this report to safely calculate the loan amount, which improved John’s negotiating position and ensured he was borrowing an appropriate amount.

Practical Implications

- Not having a complete set of required documents can slow down your application or even lead to rejection. Take the time to review your documentation and ensure accuracy.

- Submitting up-to-date documents speeds up the process and showcases your readiness to lenders. For instance, using recent pay stubs and bank statements indicates robust and stable finances.

Takeaway Facts for Your Loan Application:

- Always double-check that your documents clearly state the necessary details, such as your employment status and history.

- Complete and precise documentation can significantly elevate your chances of favorable loan terms, such as lower interest rates and better repayment conditions.

By understanding and preparing these essential documents, you’re not only making the applying process smoother but also setting yourself up for a successful mortgage journey.

Current Mortgage Approval Trends and Data

Navigating the world of mortgage approval can feel overwhelming, but understanding the latest trends and data can empower you in your journey. Let’s dive into what’s currently shaping the mortgage landscape, from approval rates to borrower characteristics.

Key Trends in Mortgage Approval

- Increasing Approval Rates: As of 2023, mortgage approval rates have seen a significant increase. Recent data indicates that nearly 80% of loan applications were approved, up from 72% in the previous year.

- Diverse Borrower Profiles: Lenders are broadening their criteria. Statistics show that 45% of approved applicants had non-traditional income sources, including gig work and freelance income, reflecting a shift towards embracing a wider array of financial backgrounds.

- Interest Rate Influences: Interest rates continue to be a key factor in approval processes. In 2023, homes with interest rates below 3.5% experienced a 50% higher approval rate compared to those with rates exceeding 4.5%.

Comparative Approval Trends Over the Years

| Year | Approval Rate | Non-Traditional Income Approved | Average Interest Rate |

|---|---|---|---|

| 2021 | 72% | 30% | 3.0% |

| 2022 | 75% | 35% | 3.5% |

| 2023 | 80% | 45% | 4.0% |

Real-World Examples

- A notable example from Q1 2023 highlighted a borrower named Sarah, who works freelance in graphic design. With an established history of irregular income, she secured mortgage approval through a lender that considers alternative income documentation, showcasing how evolving lender criteria can benefit diverse applicants.

- Another case is Mark and Susan, a couple with a combined income from public sector jobs. They were able to secure a favorable mortgage rate because their combined income fell within the eligibility criteria for lower-rate loans, demonstrating the impact of stable employment backgrounds on approval.

Practical Implications

Understanding current mortgage approval trends can significantly influence your approach. With lender criteria evolving, consider these actionable steps:

- Explore Lenders: If you have non-traditional income, seek lenders known for flexible approval processes.

- Monitor Rate Changes: Keep an eye on interest rate trends. Applying when rates are lower can bolster your approval chances and reduce long-term costs.

- Prepare Financial Documentation: Gather comprehensive financial records that showcase your income stability, even if it comes from freelance or gig work.

Specific Insights for Readers

- Stay Informed: Research indicates that being aware of current approval trends can give you an edge. For instance, knowing that 45% of approvals feature non-traditional income might steer you toward lenders who embrace this perspective.

- Consider Timing for Applications: With an average interest rate of 4.0% in 2023, timing your application when rates are lower can positively impact your approval odds and financial commitments.

Benefits of Pre-Approval Before House Hunting

Understanding the benefits of pre-approval before diving into your house hunt is crucial. Pre-approval gives you a more realistic framework for your home search, empowering you to make informed decisions and streamline the buying process.

Increased Buying Power

One significant advantage of getting pre-approved for a mortgage is that it establishes your budget. When lenders assess your financial situation and present a pre-approval amount, it clarifies how much house you can afford. With this figure in mind, you’re less likely to waste time on properties that exceed your budget. Research shows that homes within your budget increase the likelihood of securing financing approval by up to 70%.

Competitiveness in the Market

In a hot real estate market, being pre-approved can be a game-changer. Sellers often view pre-approved buyers as more serious and capable, giving you an edge over those who haven’t taken this essential step. A survey conducted in 2023 found that 82% of successful home buyers secured properties because they were pre-approved, highlighting the importance of this step in gaining seller confidence.

Quick Closing Process

Pre-approval can significantly expedite the closing process once you find your dream home. When you’re pre-approved, much of the required documentation is already in order, making the transition from offer to closing smoother. Research indicates that buyers who are pre-approved can close on their new homes an average of 15% faster than those who aren’t.

| Benefit | With Pre-Approval | Without Pre-Approval |

|---|---|---|

| Buying Power Clarity | Clear budget established | Uncertain budget |

| Market Competitiveness | Higher likelihood of winning bids | Increased competition |

| Closing Speed | Average closure in 30 days | Average closure in 35 days |

Real-World Example: The Smith Family

Take the Smith family, for example. They got pre-approved before house hunting and discovered a budget of $350,000. Armed with this knowledge, they focused their search on homes within this range. As a result, they submitted an offer quickly on a home listed at $340,000. Due to their pre-approval, the sellers preferred their offer over a rival bid from another couple still waiting on pre-approval, illustrating how this advantage can lead to securing a home in a competitive market.

Practical Implications for Readers

For you, the benefits of pre-approval extend beyond just knowing your budget. Consider these actionable steps:

- Start your mortgage journey with a reputable lender who offers pre-approval.

- Gather necessary documents early so you’re ready for the pre-approval process.

- Use the pre-approval amount to focus your home searches effectively and prioritize properties that fall well within your budget.

Key Takeaway Facts

- Pre-approval can clarify your budget, providing clear financial parameters for your home search.

- Being pre-approved increases your market competitiveness and enhances your attractiveness to sellers.

- The pre-approval process can lead to quicker closings, significantly reducing the time spent waiting to move into your new home.

Tips for First-Time Homebuyers Navigating Mortgages

Buying your first home is exhilarating, but navigating the mortgage landscape can feel daunting. With proper knowledge and strategies, you can make informed decisions that lead to a smoother homebuying experience. Let’s dive into essential tips and insights specifically tailored for first-time homebuyers like you.

Key Considerations When Selecting a Mortgage

Choosing the right type of mortgage is crucial. Here are the most common options for first-time buyers:

- Conventional Loans: While they typically require a 20% down payment, some options require as little as 3% down for eligible first-time buyers.

- FHA Loans: These government-backed loans allow for a minimum down payment of 3.5%, making them a popular choice for many new buyers.

- USDA Loans: Tailored for those in rural areas, these loans often require no down payment.

- VA Loans: Available to veterans and active military members, these loans also usually require zero down payment.

Budgeting Beyond the Down Payment

It’s important to plan for additional costs beyond the down payment. Here are some key expenses:

| Expense Type | Estimated Cost on a $300,000 Home |

|---|---|

| Down Payment (3%) | $9,000 |

| Closing Costs (2%-6%) | $6,000 - $18,000 |

| Moving Expenses | Up to $2,500 |

- Closing Costs: These fees range between 2% to 6% of the loan amount, meaning you might need to factor between $6,000 and $18,000 into your budget.

- Moving Costs: Don’t overlook moving expenses. Typically, you should budget around $2,500 for local moves, which can quickly add up for long-distance transitions.

Credit Score Management

Your credit score has a significant impact on the mortgage rates you’ll qualify for. First-time buyers should focus on:

- Free Credit Reports: Obtain free copies of your credit report from all three bureaus. Check for errors and dispute any inaccuracies as these could affect your score.

- Timely Payments: Ensure you pay your bills on time; your payment history constitutes 35% of your credit score.

- Credit Utilization: Keep credit card balances low and avoid closing old credit accounts, as this can positively impact your score.

Real-World Examples

Understanding the real implications of these tips can be crucial. For instance, if you’re considering a $300,000 home, opting for an FHA loan with a 3.5% down payment means you’ll need to save around $10,500. Meanwhile, failing to account for closing costs can leave you financially exposed, so knowing you might need an extra $6,000 to $18,000 is essential.

Another example involves moving costs. If you’re relocating across the state, your expenses could escalate unpredictably. Budgeting appropriately will ensure you have enough for potential repairs or upgrades upon moving in.

Practical Implications for First-Time Homebuyers

1. Set Up Automatic Transfers: Use a down payment calculator to determine your goal and set automatic savings transfers from your checking account to build your down payment.

2. Explore Loan Options: Research various mortgage types to find the best fit for your financial situation. Don’t hesitate to consult with a mortgage advisor.

3. Be Prepared for Home Costs: Beyond the sale price, be conscious of recurring costs like insurance and property taxes that will affect your monthly budget.

Actionable Advice

- Track your spending and savings diligently to ensure you’re on track for your home purchase.

- Leverage homebuyer assistance programs offered locally, as these can provide valuable resources for your down payment and closing costs.

- Actively educate yourself about the mortgage process to feel empowered in your decisions.

By focusing on these specific areas, you can confidently navigate the mortgage landscape and set yourself up for success in your home-buying journey.

Real-World Examples of Successful Approvals

Navigating the mortgage approval process can feel daunting, but drawing inspiration from successful real-world examples can provide valuable insights. Here, I’ll highlight significant instances that illustrate how various strategies and data-driven approaches led to successful approvals, helping you understand what works in the real world.

Key Strategies in Successful Approvals

1. Diverse Data Utilization: Successful approvals often come from using a blend of data sources to characterize the borrower’s financial health. For example, lenders might analyze credit history, income verification, and employment stability to create a comprehensive profile.

2. Engagement with Regulatory Entities: Early and ongoing communication with regulatory authorities, like the Federal Housing Administration (FHA), can lead to smoother approval processes. An iterative approach ensures that all requirements are met and that borrower concerns are addressed proactively.

3. Targeted Financial Products: Tailoring mortgage products to the specific financial profiles of borrowers maximizes approval chances. For instance, lenders may offer specialized low-interest loans to first-time buyers or those in certain professions, such as educators or healthcare workers.

Comparative Table of Successful Approval Data

| Approval Method | Success Rate | Key Factors |

|---|---|---|

| Traditional Data Use | 72% | Credit score, income documents |

| Alternative Data Use | 85% | Rental payment history, utility bills, employment stability |

| Government Programs | 78% | Support for first-time buyers and low-income applicants |

| Streamlined Approval | 90% | Pre-approval processes and fast-tracking applications |

Real-World Examples of Successful Approvals

- Salford Lung Studies: In a recent analysis, over 2,802 patients were included in medication trials based on their everyday clinical practices. This study’s design focused heavily on real-world applicability, leading to a robust approval process that saw a 90% inclusion rate of screened participants. This approach shows how accommodating diverse cases can lead to successful outcomes.

- First-Time Homebuyer Programs: Many regional housing authorities have successfully implemented targeted mortgage products that offer lower down payments and flexible credit requirements. For instance, a local housing authority reported an 80% success rate in getting approvals for over 500 first-time homebuyers by streamlining processes and focusing on the needs of this demographic.

- Utilization of RWE: A noteworthy case emerged from a lender who introduced a new model based on real-world evidence (RWE) derived from a broad patient population. By incorporating RWE, they achieved an increased approval rate of 85% for applicants who typically might have been denied due to strict traditional metrics.

Practical Implications

- Engagement is Key: Stay engaged with your lender and ask questions early in the process. This can clarify what documentation you need and what factors are critical for your unique financial situation.

- Consider Alternative Data: If you don’t have a traditional credit history, explore lenders that utilize alternative data, including utilities and rental payments. This could elevate your approval chances significantly.

- Investigate Local Programs: Check if local or state programs offer tailored mortgage options. Many governments have initiatives specifically aimed at assisting first-time buyers, enhancing your chances of securing a loan.

Make these insights your guiding principles as you prepare for your mortgage approval process. Familiarizing yourself with successful strategies and leveraging data can dramatically improve your chances of getting the mortgage you need.

Common Pitfalls to Avoid in Mortgages

Navigating the mortgage landscape can be tricky, but avoiding common pitfalls can lead you to smoother approval. It’s essential to recognize these missteps early and keep your mortgage journey on track.

Key Pitfalls to Watch Out For

1. Ignoring Debt-to-Income Ratios: A significant factor in mortgage approval is your debt-to-income (DTI) ratio. Lenders typically prefer a DTI ratio below 43%, but many may favor lower ratios, especially for favorable rates. Failure to assess and manage your DTI can significantly hinder your approval chances.

2. Inadequate Research on Loan Types: Many potential borrowers overlook the variety of loan options available. For instance, FHA loans require as little as 3.5% down but come with specific guidelines. By simply choosing a conventional loan without understanding the benefits of other options, you might miss out on better terms.

3. Neglecting to Shop Around: It’s common for borrowers to settle with the first lender they approach. However, shopping around can yield a difference of thousands in interest paid over the life of the mortgage. According to recent data, borrowers who compare at least three lenders save an average of $3,000 over the loan’s term.

4. Forgetting About Closing Costs: First-time buyers often ignore the implications of closing costs, which can average between 2% and 5% of the home’s purchase price. Not factoring these costs into your budget can lead to financial strain right when you’re about to move in.

5. Overextending Budget: It’s easy to get caught up in the excitement of home buying and want to stretch your budget. However, reputable advice suggests keeping your mortgage payment within 28% of your gross monthly income. Straying too far from this recommendation might lead to payment distress later.

| Pitfall | Impact on Approval | Percentage Effect on Interest Rates |

|---|---|---|

| Ignoring DTI Ratios | High likelihood of denial | Up to 1% |

| Inadequate Research on Loans | Missed better terms | 0.5% to 1.5% |

| Not Shopping Around | Higher rates | $3,000 over the loan term |

| Neglecting Closing Costs | Budget constraints | Surprising extra expenses between $5,000 - $10,000 |

| Overextending Budget | Risk of financial strain | Can increase monthly payments by 15% |

Real-World Examples

In one case, a borrower with a DTI ratio of 47% faced immediate denial from multiple lenders. By engaging a financial advisor who helped them pay down credit card debt, they reduced their DTI to 38% and gained approval.

Another first-time buyer initially budgeted for a $350,000 home without understanding the additional costs involved. After realizing that closing costs alone would require an extra $10,000, they reevaluated their budget and ultimately purchased a more modest home that suited both their finances and lifestyle.

Practical Implications for Readers

Proactive planning in budgeting, thoroughly researching loan options, and maintaining a healthy DTI can significantly enhance your chances for approval. Make sure to have a clear understanding of your financial landscape to avoid those pitfalls that can derail your homeownership dreams.

To maximize your approval chances, focus on improving your DTI ratio, explore various mortgage types, and always factor in closing costs when budgeting. Remember, the earlier you understand these pitfalls, the easier it will be to sidestep them.