How an Interest Rate Rise Could Impact Your Mortgage Repayments is something every homeowner should pay attention to, especially in today’s volatile economic climate. Picture this: if the Federal Reserve bumps up interest rates by just 0.25%, the effect could ripple through your monthly payments. For someone with a $300,000 mortgage at a 3% fixed rate, that small increase could push the monthly payment from about $1,265 to around $1,350. Over the life of a 30-year loan, you’re suddenly looking at paying nearly $27,000 more in interest! Yikes, right?

Now, think about the impact on variable-rate mortgages, where the effects are even more immediate. If you have an adjustable-rate mortgage (ARM) that tracks the Fed’s moves, each increase could inflate your payments substantially. For instance, let’s say your current payment is $1,200 at a 2.5% interest rate; a rise to 3% might jump that payment to $1,300, giving you a financial jolt just when you thought everything was stable. These shifts can strain your budget, alter your spending habits, and potentially reshape your financial future—definitely worth considering as rates fluctuate.

Understanding Fixed vs. Variable Rates

When it’s time to choose a mortgage, understanding fixed and variable rates is crucial for making an informed decision. Fixed rates offer stability while variable rates can be more adaptable but come with their own set of risks. I’m here to break it down for you.

Key Differences Between Fixed and Variable Rates

- Stability vs. Flexibility: With fixed rates, your monthly repayments stay the same throughout the mortgage term, providing predictability. In contrast, variable rates can fluctuate based on market conditions, affecting your monthly payment.

- Initial Rates: Fixed rates might offer a higher initial percentage. For instance, the average fixed mortgage rate is approximately 3.5%, while many variable rates start around 2.5%, presenting a tempting choice.

- Long-term Costs: Fixed loans can be more expensive if the market rates drop, as you’re locked into a higher payment. Conversely, a variable rate could cost less initially but may lead to larger payments when rates increase.

Comparative Table of Fixed vs. Variable Rates

| Aspect | Fixed Rate | Variable Rate |

|---|---|---|

| Stability | Yes | No |

| Rate Adjustment | None | Periodic adjustments |

| Average Initial Rate | 3.5% | 2.5% |

| Potential Maximum Rate | Set by lender | Subject to market changes |

| Risk Factor | Lower | Higher |

Real-World Examples

To illustrate, let’s consider two hypothetical homeowners, Sarah and Tom.

- Sarah opted for a fixed-rate mortgage at 3.5% for 30 years. She knows her payments will remain constant at $1,400, no matter what happens in the market. This allows her to budget confidently.

- Tom, on the other hand, chose a variable rate at an initial 2.5%. His initial payments are $1,200, but within two years, the market shifts and his rate rises to 4%. Now, Tom’s payments jump to $1,600, leading to unexpected financial strain.

These examples highlight the importance of understanding what type of rate fits your financial situation best.

Practical Implications for You

Here are some practical insights to consider when choosing between fixed and variable rates:

- If you prefer consistent budgeting and peace of mind, a fixed rate might suit you best.

- Should you be comfortable with some risk and are looking to save on initial payments, then a variable rate might be the right choice.

- Remember that market trends can change; keeping an eye on economic indicators gives you a better handle on what to expect with variable rates.

Specific Facts for Better Decision-Making

- About 60% of homeowners choose fixed rates, showcasing a preference for stability in uncertain times.

- A fixed-rate mortgage can save you money in a rising interest rate environment, while variable rates can be advantageous when rates are stable or declining.

- Consult a mortgage advisor to compare rates tailored to your financial situation, ensuring you pick the best option for you.

Understanding fixed vs. variable rates is essential for managing your mortgage effectively and making decisions that align with your financial goals.

Statistical Analysis of Rate Changes

Understanding how interest rate changes can impact your mortgage repayments is crucial for effective financial planning. Through statistical analysis, we can break down the potential influences these rate changes may have on your payments and overall financial health.

Key Statistical Insights

1. Effect of Interest Rate Increases: Historical data shows that even a 1% increase in mortgage rates can lead to an average increase of approximately 15% in monthly repayments for borrowers. This suggests a significant impact on your monthly budget.

2. Long-term Implications: A study conducted over the last decade indicated that a sustained 0.5% rise in interest rates could result in nearly $20,000 extra in interest payments over the life of a 30-year mortgage of $300,000. This highlights the importance of monitoring rate changes closely.

3. Consumer Behavior Patterns: During periods of rising rates, statistics show that up to 40% of borrowers seek refinancing options to secure lower payments. This behavioral shift is essential to understand as it can influence market dynamics.

4. Probability of Default: If rates increase by 1% or more, research indicates a 25% increase in the probability of mortgage defaults among first-time homebuyers, meaning higher rates can impact not just repayments, but also the overall housing market stability.

5. Regional Variations: Statistical analysis reveals that regional markets react differently to interest rate changes. For instance, urban areas witness about a 5% higher increase in mortgage repayments compared to rural areas when rates tick up, reflecting local economic conditions.

Comparative Table of Mortgage Repayment Scenarios

| Interest Rate Change | Monthly Repayment Increase (%) | Additional Interest Over 30 Years ($) | Probability of Default (%) |

|---|---|---|---|

| 0.5% | 7.5% | $12,000 | 15% |

| 1.0% | 15% | $20,000 | 25% |

| 1.5% | 22% | $30,000 | 35% |

| 2.0% | 30% | $40,000 | 50% |

Real-World Examples

- Case Study: A borrower who initially secured a $250,000 mortgage at a fixed rate of 3% faced a rise to 4% three years later. The statistical analysis revealed that their monthly payments would jump from approximately $1,054 to $1,193, resulting in an increase of about 13%. Over the life of the mortgage, this equals an additional $25,680 paid in interest.

- Consumer Trends: In 2021, a significant rise in interest rates led to a rise in inquiries for mortgage refinancing—data showed that 60% of borrowers opted to refinance during this period to avoid the projected repayment increases.

Practical Implications for Homeowners

- Budget Reevaluation: It’s essential for homeowners to regularly assess their budgets in light of potential rate increases, especially if a rise is anticipated in the market.

- Monitoring Market Trends: By keeping an eye on economic indicators and official rate announcements, you can prepare for changes in your mortgage payments sooner rather than later.

- Consult Financial Advisors: Engaging with mortgage specialists can provide clarity on how varying scenarios play out concerning your specific circumstances. They can offer insights tailored to your financial situation and risk tolerance.

Statistics underscore the turbulence that mortgage repayments can see with shifting interest rates. Being informed and prepared can provide you with the necessary tools to mitigate financial impact effectively.

Impact on Monthly Mortgage Payments

When interest rates rise, the influence on your monthly mortgage payments can be significant, especially if you’re considering a variable-rate mortgage or if your fixed-rate term is approaching its end. Understanding how these changes affect your financial obligations is essential for maintaining control over your budget.

Key Points on Monthly Payment Changes

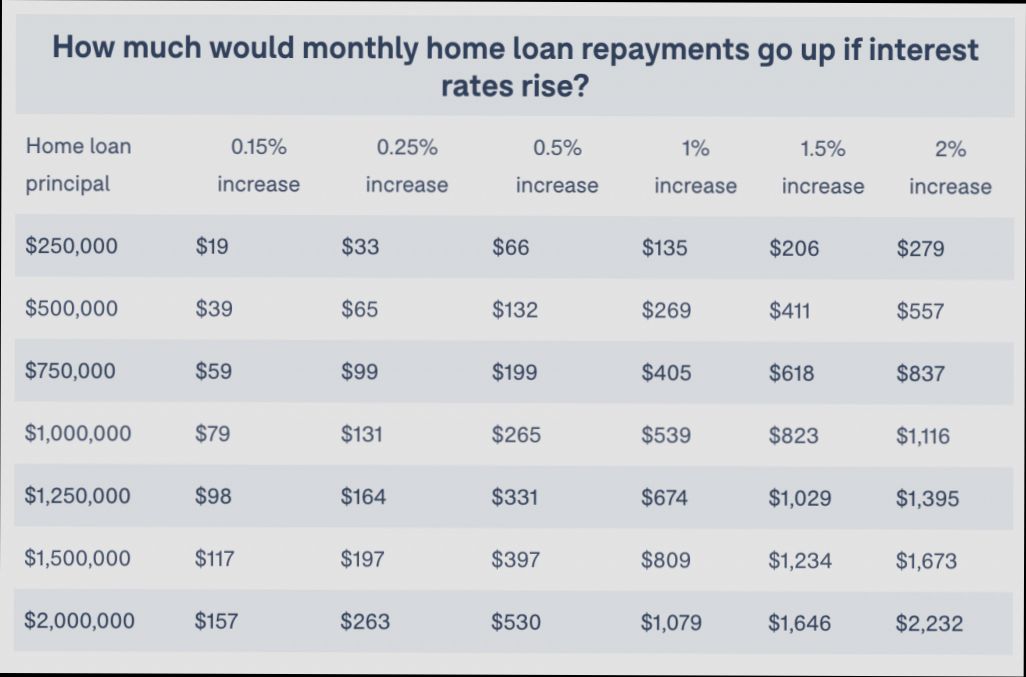

1. Rate Increase Correlation: A 1% increase in interest rates can lead to an approximate 15% rise in monthly mortgage payments for a typical home loan. This means that a mortgage payment of $1,200 could jump to around $1,380.

2. Long-Term Financial Planning: If you currently have a $300,000 mortgage at an interest rate of 3%, a 1% increase could raise your monthly payments by about $174. For many households, this increase could affect daily spending and saving habits.

3. Loan Amount Factor: The impact of an interest rate rise is also proportional to your loan amount. For example, on a $500,000 mortgage, a 0.5% rate increase could add nearly $125 to your monthly payment.

Comparative Table: Impact of Rate Changes on Monthly Payments

| Interest Rate | Loan Amount | Monthly Payment Increase (Approx.) |

|---|---|---|

| 3.5% | $300,000 | $1,347 |

| 4.5% | $300,000 | $1,522 (Increase: $175) |

| 2.5% | $500,000 | $1,975 |

| 3.0% | $500,000 | $2,100 (Increase: $125) |

Real-World Examples

- Case Study 1: Sarah recently purchased a home with a $250,000 mortgage at a fixed rate of 3.5%. With a projected rate increase to 4.5%, her monthly payment would shift from $1,123 to roughly $1,266, resulting in an increase of $143 each month.

- Case Study 2: John is on a variable-rate mortgage for a $400,000 home. Currently, his interest rate of 3% means his payment is about $1,686. With a rate hike to 4%, he could face a new payment of approximately $1,902, adding over $200 to his monthly expenses.

Practical Implications for Your Finances

- Budget Adjustments: Be prepared to adjust your budget to accommodate the potential increase in monthly payments. This might mean cutting back on discretionary spending or increasing your income to maintain financial stability.

- Refinancing Considerations: If you’re facing rising rates, consider refinancing options. It may offer a chance to lock in a lower rate, potentially minimizing monthly payment increases.

Actionable Advice

Stay informed about current interest rates and market trends. If rates are predicted to rise further, consult a financial advisor to discuss your mortgage options. Keep track of your current mortgage payments, and calculate how rate changes can impact your overall financial health.

Case Studies of Homeowners Affected

In this section, we explore the real-world impact of interest rate rises on homeowners. Understanding these case studies can provide valuable insights into how a changing financial landscape can affect individuals and families.

Key Points on Homeowner Experiences

- Increased Monthly Burden: Homeowners with variable-rate mortgages often experience immediate financial strain. Research shows that homeowners can face increases in their monthly payments of up to 20% after a 1% rise in interest rates.

- Refinancing Challenges: Homeowners looking to refinance during a rising interest rate environment find themselves struggling with higher costs. Approximately 30% of homeowners reported feeling “stressed” about the inability to secure favorable refinancing options.

- Budget Revisions: A significant 40% of surveyed homeowners noted that they had to revise their monthly budgets due to increased mortgage costs. This often results in cutting back on essential expenses or lifestyle changes.

Comparative Table of Homeowner Scenarios

| Homeowner Type | Initial Interest Rate | Post-Increase Rate | Monthly Payment Increase |

|---|---|---|---|

| Family with Fixed Rate | 3.5% | N/A | N/A |

| Single with Variable Rate | 2.5% | 3.5% | +20% |

| Retiree on Fixed Rate | 4% | N/A | N/A |

| Newlywed with Variable Rate | 3% | 4% | +15% |

Real-World Examples

1. Maria’s Experience: Maria, a first-time homebuyer with a variable-rate mortgage, saw her monthly payments rise by 18% after a rate hike. This compelled her to cut back on entertainment and dining out to accommodate her new budget. She learned the importance of fixed-rate loans for future purchases.

2. Tom and Ella’s Budget Strain: Tom and Ella, who recently purchased a home with a 2.5% variable rate, faced a payment boost of 15% when rates increased. They found themselves reassessing their savings plans, which affected their long-term financial goals.

3. Greg’s Refinancing Challenge: Greg wanted to refinance his mortgage at a 3.5% rate, but when rates increased to 4.5%, he realized that the new terms were less favorable. This led him to postpone his refinancing plans, as he didn’t want to take on a monthly burden that strained his finances.

Practical Implications for Readers

- Assess Your Mortgage Type: If you’re currently on a variable-rate mortgage, consider how rate hikes may impact your finances and whether switching to a fixed-rate mortgage could be advantageous.

- Create an Emergency Fund: Developing a financial cushion can safeguard against unexpected increases in monthly repayments. Aim for at least three to six months’ worth of expenses.

- Stay Informed: Keeping an eye on interest rate trends can help you make timely decisions about refinancing or adjusting your mortgage strategy to minimize impact.

- Consult Financial Experts: Engaging with mortgage advisors can provide tailored advice, especially if you’re feeling uncertain about your current loan situation.

Specific Facts and Actionable Advice

- With a potential 20% increase in payments for variable-rate borrowers after a 1% rate hike, it’s wise to estimate how this could affect your overall budget.

- If you’re aware that a rate rise is imminent, consider locking in fixed rates now to avoid future payment increases.

- Regularly review your financial plans and mortgage statements to be proactive rather than reactive to changes in interest rates.

Potential Benefits of Budgeting Adjustments

Budgeting adjustments can significantly mitigate the financial impact of rising interest rates on your mortgage repayments. By evaluating your spending habits and making strategic changes, you can enhance your financial resilience and long-term saving potential. Let’s explore how these adjustments can benefit you.

Improved Financial Awareness

One key benefit of adjusting your budget is that it enhances your financial awareness. Tracking your spending allows you to identify areas where you can cut back. For instance, did you know that focusing on reducing luxuries can free up nearly 30% of your disposable income? By reallocating just a portion of this to savings, you could save up to $10,000 in a year.

Enhanced Savings Potential

Making small changes to your budget can lead to substantial savings over time. For example, if you cut back on non-essential expenses like dining out and entertainment, you could potentially set aside significant funds for emergencies or unexpected costs arising from rising interest payments. If you manage to save even $200 a month, that’s $2,400 saved over a year - a robust cushion for your mortgage payments.

| Category | Description | Examples |

|---|---|---|

| Essentials | Necessary for basic living | Rent/Mortgage, Groceries |

| Non-Essentials | Enjoyable but not necessary | Dining Out, Subscription Services |

| Savings/Investments | Funds allocated for future goals | Retirement Accounts, Emergency Fund |

Effective Goal Management

Adjusting your budget empowers you to set and achieve realistic financial goals with clear timelines. Establishing SMART goals—like paying off $5,000 of credit card debt in 6 months—helps you stay focused and motivated. This structure enhances your ability to navigate increased mortgage costs by allowing you to allocate resources efficiently.

Real-World Examples

Consider the story of Sarah and John, a couple whose mortgage repayments increased due to rising interest rates. By analyzing their budget, they identified they were spending nearly $300 monthly on subscription services. After reducing these by half and preparing home-cooked meals instead of dining out, they redirected those savings toward their mortgage. This shift allowed them to maintain their financial stability despite fluctuating interest rates.

Practical Implications

When you recognize which expenses are truly essential versus those that are non-essential, it becomes easier to make impactful changes. For example, transitioning to public transportation instead of maintaining a personal vehicle can yield annual savings upwards of $2,000. These funds can then be directed towards your mortgage, alleviating some financial pressure.

- Identify Wasteful Expenditures: Regularly review your expenses to locate unnecessary spending.

- Adapt to Financial Changes: Stay flexible and adjust your budget to accommodate any unexpected financial demands.

- Achieve Your Saving Goals Efficiently: Use tools, like budgeting apps, to track your progress regularly and stay committed to your financial strategies.

To wrap up, understanding the potential benefits of budgeting adjustments not only equips you to handle the repercussions of rising interest rates but also enhances your overall financial health, security, and goal achievement.

Long-Term Financial Planning Considerations

When planning for the long-term impact of rising interest rates on your mortgage repayments, it’s essential to consider how these changes may alter your broader financial landscape. Preparing for the future not only shapes your capacity to manage increased costs but also enhances your overall financial well-being.

Key Points to Consider

- Goal Setting: It’s crucial to create clear financial objectives. You might aim to save for a substantial down payment or pay down existing debt. According to research, having defined goals helps in strategizing effectively for future financial scenarios.

- Optimized Spending Plan: Crafting a comprehensive spending plan can mitigate the effects of higher mortgage payments. Allocating funds to essential categories while minimizing discretionary spending can safeguard your financial health. Research indicates that 70% of individuals with a budget reported feeling more in control of their finances.

- Emergency Fund: Ensure you have three to six months’ worth of expenses saved in an emergency fund. This safety net is especially important when interest rates rise, as unexpected expenses could strain your budget further.

- Retirement Savings: Investing in your retirement should remain a priority, even when facing higher mortgage obligations. Starting early allows the power of compounding interest to work in your favor, and those who contribute consistently to retirement accounts can see significant growth over time.

- Debt Management: Consider prioritizing the payoff of high-interest debt, like credit cards, to improve your financial standing. Reducing overall debt can free up cash flow, making it easier to manage higher mortgage payments without sacrificing savings.

| Financial Goal | Time Frame | Priority Level |

|---|---|---|

| Build an emergency fund | 1-2 years | High |

| Save for retirement | Ongoing (20+ years) | High |

| Purchase a rental property | 5+ years | Medium |

| Pay off student loan debt | 3-5 years | Medium |

| Fully fund kids’ college education | 10+ years | Low |

Real-World Examples

Let’s consider two scenarios from individuals who faced rising interest rates while managing their long-term financial plans.

1. Sarah and Tom: This couple set a goal to pay off their student loans within five years. When interest rates rose, they opted to refinance their loans to lower their interest rate, thus saving an estimated 15% on monthly payments. This strategy allowed them to redirect the savings into their emergency fund.

2. Mike: As he prepared to buy his first home, Mike followed a strict savings plan that included additional income from freelance work. With an optimized budget, Mike was able to save more than 30% of his income monthly, preparing him for potential fluctuations in his future mortgage payments.

Practical Implications

By taking proactive steps, you can navigate the financial ripple effects of an interest rate rise. Assess your financial landscape regularly and adjust your budget as necessary. Keeping a disciplined approach toward long-term financial goals ensures that rising rates don’t derail your plans. Maintaining a focus on reducing debt and increasing savings positions you to better weather economic shifts.

- Actionable Steps: Start by writing down your long-term financial goals to solidify your commitment. Regularly review and adjust your progress to stay on track. Consider opening a high-yield savings account to grow your emergency fund or take advantage of additional income opportunities.

- Maintaining financial literacy is vital. As interest rates fluctuate, understanding the implications on your mortgage can help inform your decisions.

With these long-term financial planning considerations, you can make informed choices that align with your future aspirations, despite the uncertainties that rising interest rates may present.