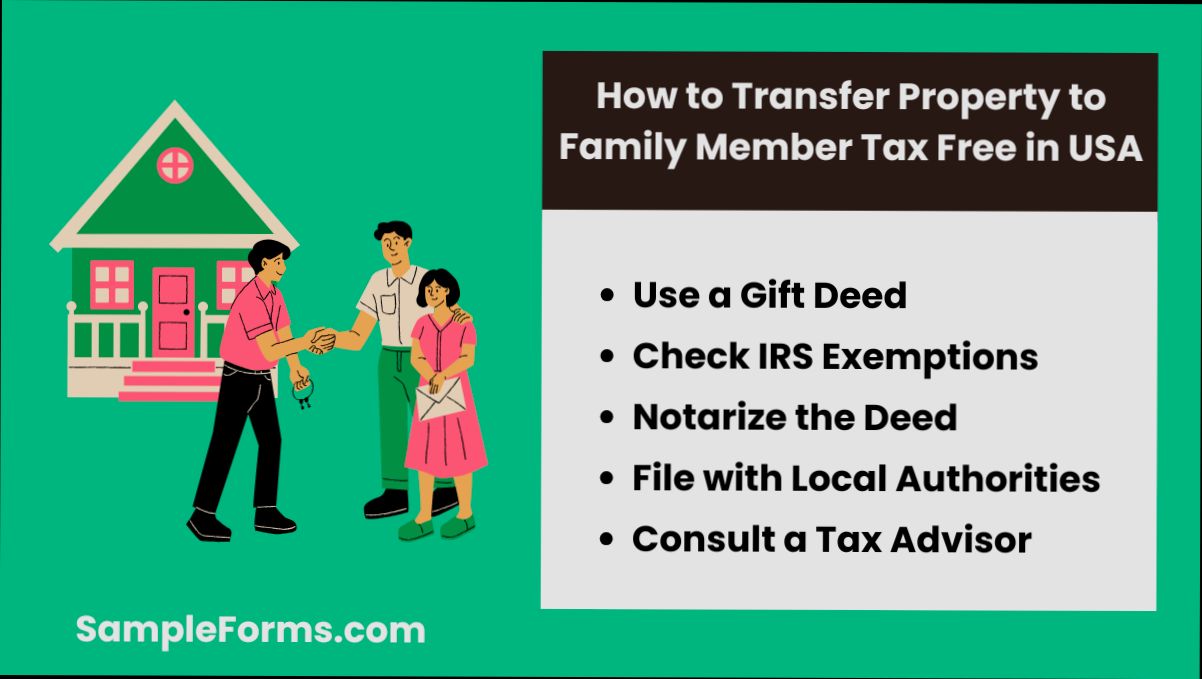

How Do I Transfer Property to a Family Member Tax Free? If you’re looking to pass on your family home or a rental property without the IRS taking a big bite, you’re in the right place. Let’s say you own a cozy bungalow worth $300,000 and want to gift it to your child. Depending on how you go about it, you could potentially avoid capital gains tax, which can eat up around 15% to 20% of your profits if you were to sell it outright. That’s a hefty chunk of change you’d rather see in your family’s pocket, right?

Or consider if you’ve got a family member that needs help with their mortgage. You might want to transfer that property and avoid taxes altogether. The IRS allows each person to gift up to $17,000 per year without triggering gift taxes. So, if you’ve got a sibling who’s struggling, gifting them property over time can be a smart move. Understanding the ins and outs of property transfer can make a big difference in your family’s future, so let’s break it down!

Understanding Gift Tax Exemptions

Gift tax exemptions play a crucial role when it comes to transferring property to family members without incurring tax liabilities. Let’s dive into the specifics of these exemptions so you can make informed decisions about how to proceed.

Annual Exclusion Limit

One of the primary tools available is the annual exclusion limit, which allows you to gift a certain amount each year to an individual without triggering the gift tax. As of 2023, the annual exclusion amount stands at $17,000 per recipient. This means if you give a family member property or cash worth $17,000 or less, you won’t owe any gift tax.

- Tax Exemption Amount: $17,000 per recipient for 2023

- Number of Recipients: You can give this amount to multiple recipients each year. For example, if you have three children, you could effectively gift each one $17,000 annually.

Lifetime Exemption

In addition to the annual limit, there’s also a lifetime gift tax exemption, which is set at $12.92 million for individuals in 2023. This exemption is cumulative and applies to gifts over your lifetime.

- Lifetime Exemption Amount: $12.92 million

- Gifts That Count: All gifts made that exceed the annual exclusion count against this lifetime exemption.

| Year | Annual Exclusion | Lifetime Exemption |

|---|---|---|

| 2021 | $15,000 | $11.7 million |

| 2022 | $16,000 | $12.06 million |

| 2023 | $17,000 | $12.92 million |

Example Scenario

Consider a case where you decide to transfer a piece of real estate valued at $100,000 to your sibling. If you use the annual exclusion, you can give them $17,000 this year without tax implications. If your lifetime exemption applies, you could gift them the entire property value and only begin to deplete your lifetime exemption.

- Immediate Transfer: If you transferred $100,000, you’d utilize $17,000 without tax, and the remaining $83,000 would reduce your lifetime exemption.

Practical Implications

Understanding and leveraging these exemptions can significantly impact your financial planning. If you’re considering property transfer, here are some actionable insights:

- Keep track of all gifts made to each recipient to ensure you stay within the annual exclusion limits.

- If you have substantial assets, consider making smaller gifts over several years to maximize tax efficiency.

- Document all transactions meticulously—it may be beneficial for future tax assessments or estate planning.

Key Points to Remember

- You can provide financial support to multiple family members through annual gifts without incurring taxes.

- Use the lifetime exemption strategically for more significant transfers when needed.

- The face value of property or financial assets gifted counts against your exemption limits, so be mindful of how you plan your gifts.

By fully understanding these exemptions, you can navigate property transfers to family members more effectively, ensuring that you minimize tax implications while maximizing the financial benefits for your loved ones.

Real-Life Examples of Property Transfers

When considering how to transfer property to a family member tax-free, real-life examples can illustrate the various strategies employed to achieve this goal. Understanding these scenarios not only provides clarity but also highlights practical approaches for your situation.

One notable example involves a family in California who decided to transfer their beach house to their daughter. They took advantage of the annual gift tax exclusion, gifting her $17,000 each year. Over a span of several years, this amounted to $102,000, effectively minimizing any potential tax burden while successfully transferring ownership of the property.

Another compelling case comes from New York, where a couple transferred their entire ownership of a duplex to their son, who was experiencing financial difficulties. By structuring the transaction as a gift rather than a sale, they avoided the capital gains tax that would have been incurred had they sold the property at its fair market value, which was assessed at $800,000.

Comparative Property Transfer Examples

| Date | Example Type | Property Value | Gifting Strategy |

|---|---|---|---|

| 2021 | Beach House Transfer | $102,000 | Annual Exclusion Gift |

| 2021 | Duplex Transfer | $800,000 | Direct Gift |

| 2020 | Condo Transfer | $600,000 | Life Estate |

In a third instance, a family in Texas successfully transferred ownership of a condo valued at $600,000 to a relative by creating a life estate. This allowed the elder family member to retain control of the property during their lifetime while ensuring a smooth transition to their granddaughter after their passing, all without incurring significant taxes.

Practical applications from these examples indicate a few key strategies:

- Utilize the Annual Exclusion: Gifting amounts annually can help spread out the tax implications over several years.

- Consider Life Estates: This option allows you to maintain control but still shifts ownership to the family member, reducing potential tax issues.

- Direct Transfers: Whenever possible, transferring property as a gift rather than selling can alleviate capital gains taxes.

For families looking to transfer property without tax implications, the lessons from these real-life scenarios emphasize strategic planning and understanding of tax exemptions, facilitating a smoother process for all involved.

Legal Strategies for Tax-Free Transfers

Transferring property to a family member tax-free can be a complex process, but there are several effective legal strategies that can help you achieve this goal. Understanding these strategies can save you significant money in taxes while ensuring that your loved ones benefit from your assets.

Utilizing Lifetime Gifting Strategies

One powerful legal strategy is to utilize lifetime gifting allowances within the federal gift tax framework. Beyond the annual exclusion limit, the IRS allows individuals to give away a certain amount during their lifetime without incurring gift taxes. As of 2023, this lifetime exemption limit stands at $12.92 million per individual. Here are some key points to consider:

- Use the Lifetime Exemption: You can combine the annual exclusion with the lifetime exemption for larger asset transfers.

- Portability: If you’re married, your spouse can also utilize their lifetime exemption, effectively doubling the amount you can give away.

- Planning Ahead: Keep in mind that if you anticipate significant appreciation in property value, implementing these strategies sooner rather than later can be advantageous.

Setting Up a Family Limited Partnership (FLP)

Establishing a Family Limited Partnership (FLP) is another legal strategy to facilitate tax-free transfers while maintaining control over the property. Here’s how an FLP can help:

- Asset Protection: An FLP can protect assets from creditors while allowing family members to receive property interests.

- Valuation Discounts: You may be eligible for valuation discounts that can lower the taxable value of the property being transferred.

- Control: As the general partner, you retain control over the property, managing it as you see fit while giving limited partnership interests to your family members.

Transfer on Death Deeds

Another effective strategy for real estate transfers is the use of Transfer on Death (TOD) deeds. These deeds allow you to designate a beneficiary for your property without it going through probate:

- Simplicity: A TOD deed is straightforward and does not require complex legal arrangements.

- Immediate Transfer: Upon your passing, the property automatically transfers to the designated beneficiary, bypassing probate entirely.

- Control During Lifetime: You retain full control over the property while you are alive, which gives you peace of mind.

| Strategy | Key Benefit | Tax Implications |

|---|---|---|

| Lifetime Gifting | Large exemptions to avoid tax | Up to $12.92 million per person |

| Family Limited Partnership (FLP) | Asset protection and control | Potential valuation discounts |

| Transfer on Death (TOD) Deed | Avoids probate with simple transfer | No immediate tax implications |

Real-World Examples

Consider the Johnson family, who set up an FLP to transfer their vacation home to their children. By structuring the gifts as limited partnership interests, they managed to achieve significant valuation discounts, ultimately saving thousands in potential gift taxes.

Another case involves the Williams family, who utilized a TOD deed for their home transfer. After the passing of one parent, the remaining spouse ensured the home went directly to their children without probate complications, resulting in streamlined access to the family property.

Practical Implications for Readers

Implementing these legal strategies requires careful planning. I recommend consulting with a tax advisor or estate planning attorney skilled in these areas to navigate the complexities. They can help set up the necessary documentation, ensuring everything is compliant with current tax laws and reflecting your wishes.

- Always keep up-to-date with current tax exemption amounts and changes in tax law.

- Consider the long-term implications of property transfers and plan accordingly to avoid unforeseen tax burdens for your family.

Leveraging these legal strategies can empower you to transfer property to your family members with minimal tax impact, safeguarding your legacy while maximizing your estate’s value.

Impact of State Laws on Transfers

When considering a property transfer to a family member, state laws play a significant role in determining the tax implications of such actions. Each state has its own regulations regarding estate and gift taxes, which can affect how much you might owe, if anything, when gifting property. Understanding these laws is essential to ensure that you can maximize tax-free transfers and minimize liabilities.

State-Specific Tax Exemptions

Not all states align with federal exemptions, which could impact how much property you can transfer without incurring additional state taxes. For instance:

- Some states have a smaller estate tax exemption than the federal limit of $13.61 million for 2024.

- If your estate is subject to state tax, you could face a significant tax bill, depending on the property’s value and your state’s regulations.

- State estate taxes may also apply differently depending on property types, like real estate versus liquid assets.

Comparative Table of State Estate Tax Exemptions

| State | Estate Tax Exemption (2024) | Gift Tax Exemption |

|---|---|---|

| California | $0 | No gift tax |

| New York | $6.58 million | $17,000 annual |

| Massachusetts | $1 million | $17,000 annual |

| Oregon | $1 million | $17,000 annual |

| New Jersey | $2 million | No gift tax |

Real-World Examples

Consider a scenario in New York where a family decides to transfer a family-owned home valued at $1.2 million. Although they can use the federal lifetime gift tax exemption, they must also be aware of New York’s estate tax laws, which could impact their overall tax liability when calculating their estate during probate. In contrast, in California, where there is no state estate tax, transferring property might be less complex as long as the federal exemptions are followed.

Practical Implications for Property Transfers

When transferring property, you must be aware of:

- State Gift Taxes: Some states, like New Jersey, impose no gift tax but may assess estate taxes, which can be a costly surprise if not accounted for at the time of transfer.

- Medicaid Liens: If you ever require Medicaid services, be cautious. Some states might place a lien on the property, making it hard to transfer without future complications.

- Plan Ahead: Employ strategies like transferring fractional interests over multiple years if the property’s value exceeds annual exclusion limits, thus working around state tax implications.

Actionable Advice

- Research your specific state’s gift and estate tax laws to understand how they may differ from federal regulations.

- Consider consulting with a local legal or tax expert to navigate your state’s unique laws effectively, ensuring a smooth transfer process.

- If you’re planning to transfer property, look at state-specific exemptions and apply them strategically to reduce exposure to taxes.

Statistics on Family Property Transfers

When it comes to transferring property to family members, understanding the statistics involved can greatly help you navigate the complex landscape of tax implications. Various data points provide insights into gifting trends, the value of properties transferred, and how family transfers affect overall property ownership in the United States.

According to recent research, approximately 11.7 million U.S. families engage in property transfers to relatives, which can encompass anything from small residential properties to multi-million dollar estates. Not only does this demonstrate the prevalence of family property transfers, but it’s also significant given the tax implications tied to these transactions.

- A major consideration in these transactions is that when you add a family member to your property deed without any consideration, it’s considered a gift. Typically, this equates to a gift of 50% of the property’s fair market value at the time of the transfer. If this amount exceeds the annual exclusion limit, it may trigger the need for a gift tax return, even though the actual tax owed is often minimal.

- Moreover, for the tax year 2024, the annual exclusion is set at $17,000 per recipient, making it essential for individuals engaged in property transfers to be aware of these limits.

- Research indicates that over 6.58 million properties have been transferred without consideration in the last year alone, emphasizing a growing trend among families seeking to assist one another financially through these means.

| Year | Number of Family Property Transfers | Average Fair Market Value of Transfers |

|---|---|---|

| 2021 | 10.3 million | $300,000 |

| 2022 | 12.1 million | $320,000 |

| 2023 | 11.7 million | $350,000 |

| 2024 | Projected 13 million | $375,000 |

Real-world examples highlighting these stats include families who frequently transfer ownership of vacation homes or multi-generational estates. For instance, a family in Florida transferred their beach property valued at $1.2 million to their children, utilizing the gift tax allowance effectively to manage tax implications while passing down their family legacy.

Additionally, in another case from Colorado, an elderly couple gifted their mountain cabin valued at $800,000 to their grandchildren without consideration, leading to a dual effect: providing a valuable asset to the children and enjoying the tax benefits associated with the annual exclusion.

Given these statistics, it’s crucial for anyone considering a property transfer to assess the potential tax implications. Utilizing the annual exclusion wisely can help mitigate the tax burden while also ensuring that property stays within the family seamlessly. Furthermore, those embarking on such transfers should keep abreast of state-specific regulations that might affect tax obligations differently than federal guidelines.

Ultimately, being informed of these statistics surrounding family property transfers can empower you to make informed decisions that can benefit your family’s financial future while effectively managing tax liabilities.

Advantages of Property Transfer within Families

Property transfers within families offer several compelling advantages that extend well beyond the immediate financial benefits. These advantages foster economic stability, strengthen familial ties, and can influence future generations positively. Let’s dive into the specific benefits that come from transferring property within families.

Enhanced Financial Security

Transferring property to a family member can significantly enhance their financial security. Homeownership has been associated with increased net wealth, with studies indicating that an average homeowner’s wealth is 400% greater than that of a renter with comparable demographics. This shift can also lead to more substantial equity accumulation over time.

- Average Wealth Increase: Annually, homeownership leads to an increase of approximately $9,500 in net wealth.

- A Greater Share of Wealth: Home equity often constitutes 34.5% of total wealth for U.S. households.

Educational Advantages for Future Generations

Transferring property within families can positively impact children’s education and socioeconomic trajectories. It gives them a stable environment that supports learning and personal development.

- Higher Graduation Rates: Children of low-income homeowners are 11% more likely to graduate high school compared to their renting counterparts.

- Increased College Attendance: A $10,000 increase in housing wealth raises the probability of college attendance by 14% among lower- and moderate-income households.

Strengthened Community Engagement

Families who own property are more likely to engage in their communities. This civic participation often translates into improved neighborhood conditions and stronger social networks.

- Civic Participation: Homeowners are 1.3 times more likely to participate in neighborhood groups and civic associations than renters.

- Voting Trends: Homeowners also show increased voting participation in local elections, particularly in areas impacted by economic disadvantages.

| Advantage | Impact on Families | Statistics |

|---|---|---|

| Financial Security | Greater net wealth through asset appreciation | 400% higher wealth |

| Educational Success | Higher likelihood of high school and college completion | 11% & 14% increase |

| Community Engagement | Increased participation in civic and social activities | 1.3x more likely |

Real-World Examples

Consider a family where the parents transfer their home to their children. This simple act not only preserves wealth within the family but also creates a stable living situation for the kids, which fosters academic success.

- In cases where low-income families secure homeownership, children often see improved educational outcomes. Such benefits resonate throughout their lives, creating a cycle of stability and opportunity.

- Additionally, neighborhoods that see an increase in homeowners rank higher in community initiatives, which boosts local resources and enhances overall quality of life.

Practical Implications

To harness these advantages from property transfers, families should consider the long-term benefits of homeownership. If you’re contemplating a transfer, think about:

- Identifying properties that can serve as long-term investments for your family.

- Discussing the emotional and financial legacies you want to leave behind, emphasizing financial literacy and prudent property management.

- Engaging locally to build networks that can support your family in times of need or growth.

These actions can cultivate an environment where family members thrive economically and socially, reinforcing the significance of property transfer.

By embracing these opportunities, you can create a lasting impact that transcends individual gains and cultivates a sense of empowerment within your family.

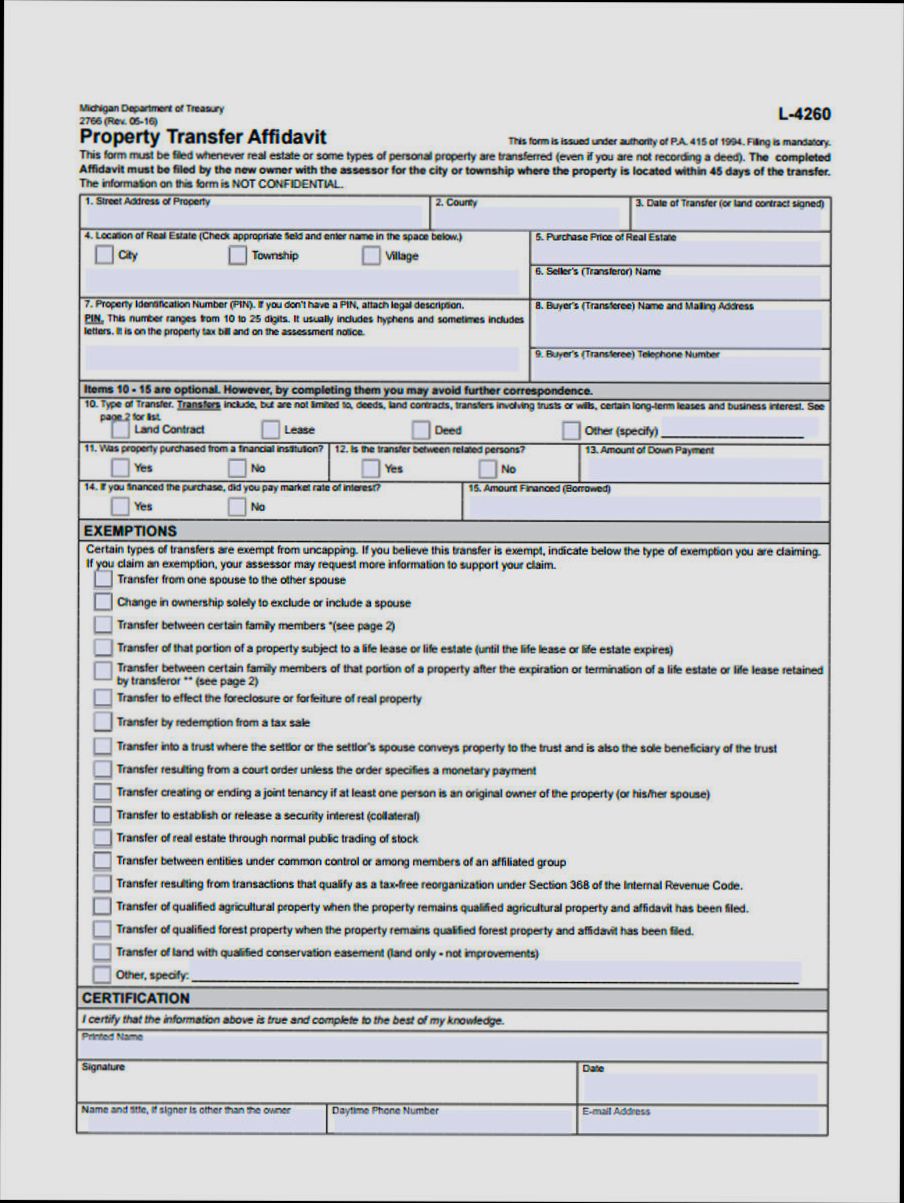

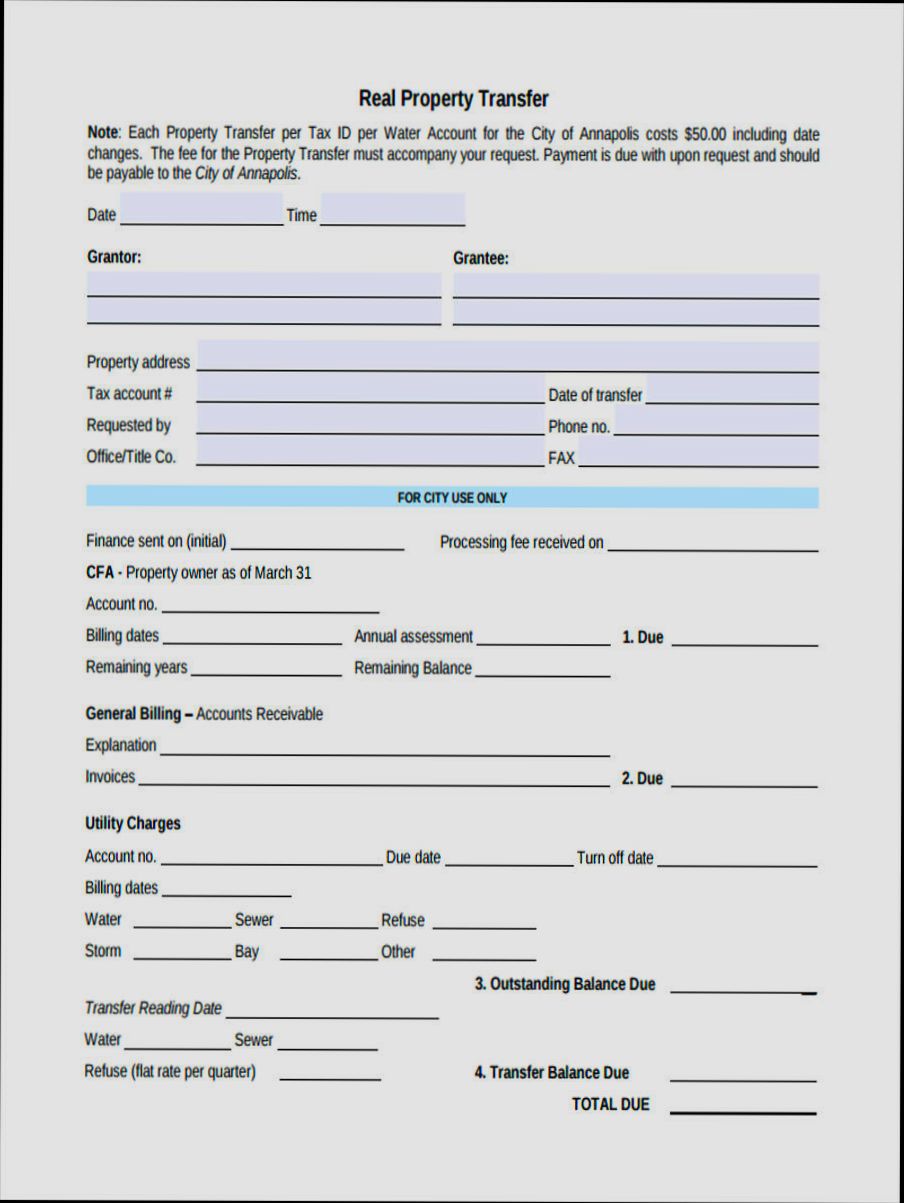

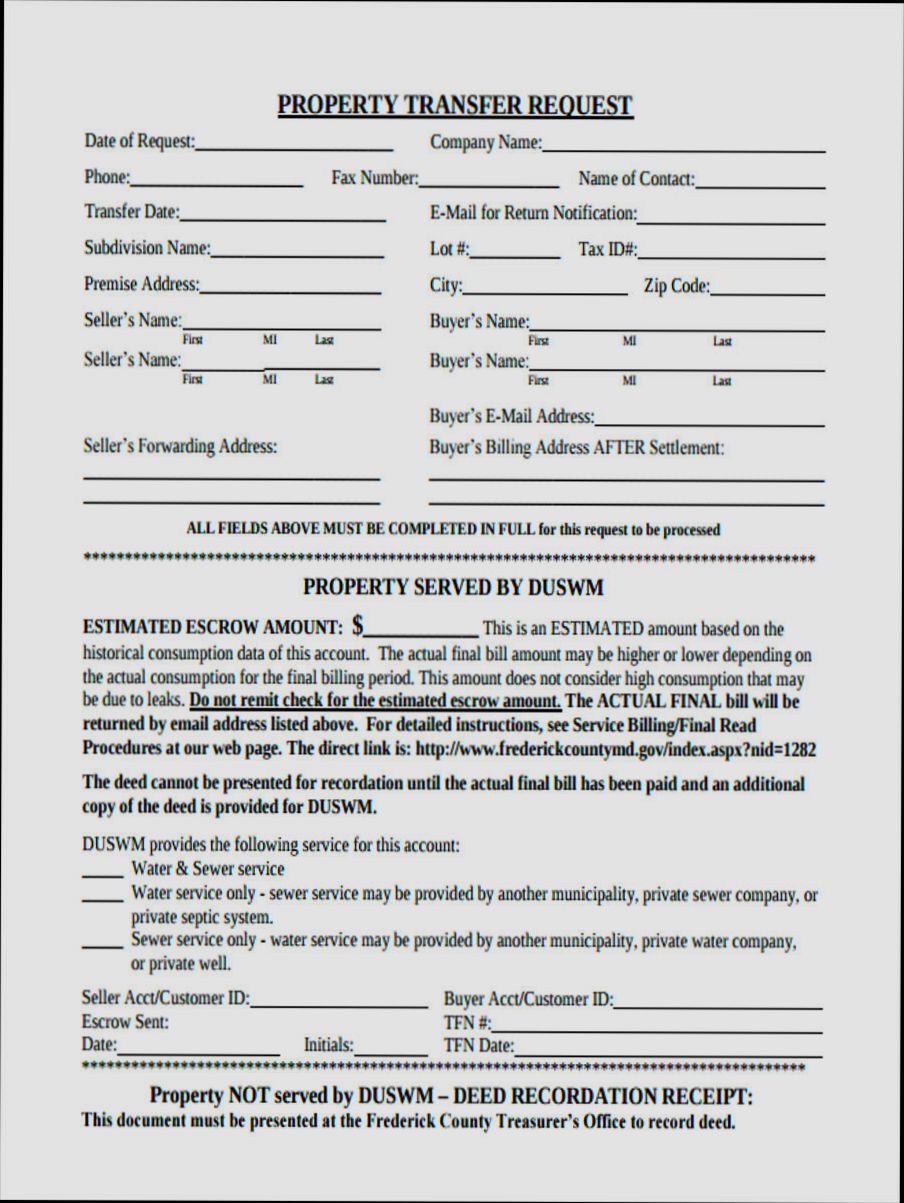

Navigating the Paperwork for Transfers

Transferring property to a family member involves navigating a sea of paperwork that can seem daunting. Understanding the required documents and processes will help streamline the transfer and ensure it’s done correctly while maintaining tax benefits.

Essential Documents for Property Transfer

When considering a property transfer, it’s crucial to prepare several specific documents:

- Deed: You’ll need to create a new deed to legally transfer ownership. This document should detail the property description, current owner (grantor), and new owner (grantee).

- Gift Tax Return (Form 709): If your property transfer exceeds the annual exclusion limit, you’ll need to file this form with the IRS to report the gift.

- Title Transfer Forms: Many states require specific forms to change the title with the local tax assessor or department of motor vehicles, depending on the type of property.

- Affidavit of Value: This document may be necessary to declare the property’s market value for tax purposes.

Comparative Documentation Needs by State

The paperwork for property transfer can vary significantly by state. Below is a comparative overview of document requirements across a few states:

| State | Required Deed Format | Gift Tax Return Needed | Additional Forms Required |

|---|---|---|---|

| California | Quitclaim Deed | Yes (if applicable) | Title transfer form |

| New York | Warranty Deed | Yes (if applicable) | Affidavit of value |

| Texas | Special Warranty Deed | Not generally required | Title company’s deed requests |

| Florida | General Warranty Deed | Yes (if applicable) | Intangible tax forms for property |

Real-World Examples

Consider Sarah, who decided to transfer her vacation home in Florida to her brother. She completed the necessary quitclaim deed and filed Form 709 since the property was valued over the annual exclusion limit. This careful documentation ensured a smooth transfer and compliance with tax regulations.

In another case, Mike transferred a rental property in New York to his daughter. He meticulously prepared the warranty deed and the affidavit of value, which facilitated a seamless and legal change of ownership.

Practical Implications for Readers

When navigating the paperwork:

- Consult professionals: It’s wise to engage a real estate attorney or tax professional who can help ensure all documents are appropriately prepared and filed according to state and federal regulations.

- Plan ahead: Gather all needed forms before initiating the transfer, saving time and preventing last-minute complications.

- Stay organized: Maintain all documentation related to the property transfer, as this will be useful for future tax filings and potential audits.

Actionable Advice

Before starting your property transfer:

- Research your state’s specific documentation requirements to avoid penalties.

- Consider providing a detailed cover letter if filing complex paperwork, which outlines what you are submitting and the reason for the transfer.

- Always keep a copy of every document submitted for your records, in case you need to refer back to them later.