How Much Equity Can I Have in My Home and Still File Chapter 7? It’s a question that many homeowners facing financial struggles wrestle with. Imagine you own a home valued at $300,000, and you’ve paid off $150,000 of your mortgage—this gives you $150,000 in equity. But here’s the kicker: Chapter 7 bankruptcy has certain exemptions that can protect some of that equity. For example, in many states, you might find a homestead exemption of $25,000 to $75,000, depending on where you live. So, if you’re sitting on a tidy sum of equity, it’s crucial to understand how much of that can actually be shielded while you navigate this tricky situation.

Let’s say you’re in California, where that exemption is higher—up to $600,000 if you’ve lived in the home for over two years. Now, picture yourself in a scenario where you live in a state with a smaller exemption, limiting you to, say, $50,000. If you’re looking at a chunk of equity closer to $100,000, it gets a bit complicated. You might have to think about what to do with that extra equity before filing. There are real-life cases that highlight the importance of understanding these nuances, like homeowners who lost their assets due to uncalculated equity. It’s all about knowing where you stand with your home before you take that leap into Chapter 7.

Understanding Chapter 7 Bankruptcy Equity Limits

Navigating through the equity limits in Chapter 7 bankruptcy can feel quite complex. Understanding these limits is essential when considering how much equity you can have in your home while still qualifying for bankruptcy relief. Let’s dive into the critical aspects of equity limits in Chapter 7.

Key Equity Limits to Consider

When considering Chapter 7 bankruptcy, each state has its equity limits that dictate how much home equity you can protect. Here are some key points to keep in mind:

- Exemption Amounts: Individual states specify how much equity in your home you can exempt. For example, in California, the exemption can be as high as $600,000 in certain counties.

- Federal Exemption: If your state does not provide a more favorable exemption, the federal exemption allows for $27,900 for a single filer, meaning you may need to watch your equity closely.

- Variability by State: A state like Florida offers a $0 cap on the homestead exemption for protected properties, potentially allowing unlimited equity protection in some scenarios.

Comparative Table of Equity Limits

| State | Homestead Exemption (Single) | Homestead Exemption (Married) |

|---|---|---|

| California | Up to $600,000 | Up to $1,200,000 |

| Florida | Unlimited | Unlimited |

| Texas | Unlimited | Unlimited |

| New York | $170,825 | $170,825 |

| Illinois | $15,000 | $30,000 |

Real-World Examples

Consider John, who resides in California with a home valued at $800,000 and an outstanding mortgage of $500,000. His equity stands at $300,000. Utilizing the California exemption, he can protect up to $600,000 of that equity. Thus, John is safe under Chapter 7.

On the other hand, we have Sarah from Illinois with a home valued at $250,000 and an outstanding mortgage of $200,000, giving her $50,000 in equity. With Illinois’ exemption of $15,000 for a single filer, Sarah faces a shortfall if she does not adjust her financial situation sooner.

Practical Implications

When contemplating Chapter 7 bankruptcy, it’s crucial to assess your equity against the exemption limits set by your state. Here are actionable steps:

- Research your state’s exemptions: Understanding your local laws can provide valuable insights regarding your specific situation.

- Consult a Bankruptcy Attorney: They can help you navigate the complexity of state-specific exemptions and advise on strategies to protect your equity.

- Reassess your mortgage debt: If your home’s market value spikes or mortgage balances decrease, it might change your exemption eligibility.

Specific Facts and Actionable Advice

- Always keep an eye on current market conditions as housing prices fluctuate. They can directly impact your home equity and therefore your bankruptcy options.

- If you believe your equity exceeds your state’s exemption limit, consider selling your home before filing to mitigate equity that could be seized.

- Utilize the median household income requirements for your state to determine if filing under Chapter 7 is possible given your financial landscape.

Average Home Equity Levels Among Filers

Understanding average home equity levels among those filing for Chapter 7 bankruptcy can provide critical insights into financial health and options. Home equity is a significant asset, and knowing where you stand can influence the decisions you make during bankruptcy proceedings.

Recent data shows that the average mortgage-holding homeowner has approximately $311,000 in equity. This figure emphasizes the potential protective measures you might have in place, depending on your state’s exemption limits.

Key Statistics on Home Equity Levels

- About 48.3% of mortgaged residences are classified as “equity rich,” meaning their outstanding loan balance is less than half the home’s value.

- On average, homeowners in this group gained roughly $5,700 in equity between Q3 2023 and Q3 2024.

- If you were to look at the tappable equity for homeowners, around $203,000 can be accessed while still keeping a healthy stake in the property.

- Underwater properties, or those where homeowners owe more than their home is worth, account for only 1.8% of all residential mortgages, marking a decrease in negative equity scenarios.

| Metric | Value |

|---|---|

| Average Home Equity (Mortgage-Holding Homeowners) | $311,000 |

| Tappable Equity Available | $203,000 |

| Percentage of Equity Rich Homes | 48.3% |

| Average Home Equity Gain (2023-2024) | $5,700 |

| Percentage of Underwater Mortgages | 1.8% |

Real-World Examples

Consider the recent figures from various states, highlighting how homeowners in certain regions fared over the last year. For instance, homeowners in Rhode Island experienced an equity gain of approximately $43,000, while those in New Jersey also saw similar improvements. In contrast, homeowners in Hawaii faced an equity loss of about $34,000, underscoring regional variations in real estate value and equity levels.

These examples illustrate how geographic disparities can impact the average home equity levels among filers, and therefore the options available to them during bankruptcy.

Practical Implications for Filers

For anyone contemplating filing for Chapter 7, it’s crucial to assess your current home equity relative to your state’s exemptions. Recognizing where you stand can help guide your decisions. Here’s what you can do:

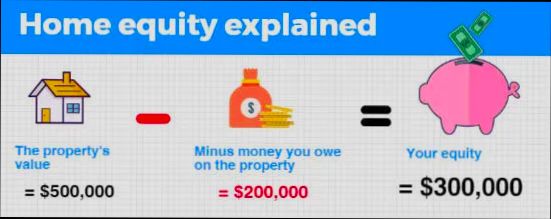

- Evaluate your home’s current market value and subtract your mortgage balance to determine your equity.

- Investigate your state’s specific exemptions regarding home equity, as this can directly affect how much you can preserve during bankruptcy.

- If you belong to the equity-rich category, you may have options to leverage that equity, potentially affecting your bankruptcy filing strategy.

Important Facts to Keep in Mind

- As you work through your financial situation, aware that the average homeowner, right now, enjoys an equity balance that might offer more options than they realize post-bankruptcy.

- Whether you’re considering filing soon or just reviewing your financial landscape, understanding these equity levels can help you make informed decisions.

Let your equity work for you, but ensure you’re educated about the limits and protections available in bankruptcy scenarios before making any big moves.

Implications of Home Equity in Bankruptcy

Understanding the implications of home equity when filing for Chapter 7 bankruptcy is crucial for anyone considering this path. The amount of equity you have can significantly affect the bankruptcy process, your ability to keep your home, and your overall financial situation.

Factors Affecting Home Equity in Bankruptcy

When we discuss home equity in bankruptcy, it’s essential to recognize how it can directly influence your bankruptcy case. Here are some key implications:

- Exemption Limits: The amount of equity you can protect is determined by state exemption laws. For instance, in some states, the homestead exemption may allow protection of up to $150,000 in home equity, while in others, it may be considerably higher or lower.

- Non-Exempt Equity: If your home equity exceeds your state’s exemption limit, that non-exempt equity becomes part of your bankruptcy estate. This means creditors may be allowed to claim that excess value, possibly leading to the sale of your home to satisfy debts.

Comparative Insight on Equity Implications

| State | Homestead Exemption Limit | Average Home Equity Among Filers | Implication of Excess Equity |

|---|---|---|---|

| California | $600,000 | $311,000 | Potential loss of home if equity exceeds exemption by a significant margin. |

| Texas | Unlimited | $325,000 | Strong protection against losing home, as there’s no limit. |

| New York | $170,000 | $310,000 | High chance of losing home if equity exceeds exemption; potential for asset liquidation. |

Real-World Examples

Consider the case of a debtor in California who has $800,000 in home equity. Given California’s homestead exemption limit of $600,000, the $200,000 non-exempt equity could lead to the sale of the home to pay creditors. In contrast, a homeowner in Texas with a $450,000 equity can file for Chapter 7 without risking their home due to the unlimited exemption.

Another example is of a New York homeowner with $320,000 in equity. Since they have only $170,000 exempt, they might face the challenging situation of losing their home unless they can find another way to manage that excess equity.

Practical Implications for Your Bankruptcy Strategy

- Assess Your Equity: Before filing, take a close look at your home equity and state exemptions. Knowing where you stand can help you avoid surprises during the bankruptcy process.

- Consider Chapter 13: If you have substantial non-exempt equity, you might want to consider filing for Chapter 13 bankruptcy instead. This option allows you to keep your home while paying off debts over time.

Additional considerations include:

- Determine if you can convert non-exempt equity into exempt assets before filing, such as making necessary improvements that raise the home’s value in line with the exemption.

- Engage with a bankruptcy attorney who understands state-specific laws about home equity and can guide you based on your unique situation.

Being aware of the implications of home equity can empower you to make informed choices that align with your financial goals during the bankruptcy process.

Real-World Scenarios for Homeowners

Navigating Chapter 7 bankruptcy can be a daunting experience, particularly when it involves understanding how much equity you can retain in your home. Let’s explore some real-world scenarios that illustrate how equity limits affect homeowners who are considering or have filed for Chapter 7 bankruptcy.

Home Equity and State Variations

Homeowners across different states face varying limits when it comes to exempting equity during bankruptcy. Here are key factors to consider:

- State-specific Exemption Limits: For example, a homeowner in Texas can exempt up to $100,000 of home equity, whereas a homeowner in Florida has an unlimited exemption if the home is their primary residence.

- Homestead Exemptions: Some states provide homestead exemptions that enable you to retain more of your home’s equity even if it exceeds typical limits.

Potential Equity Scenarios

If you’re wondering if you can keep your home when filing for bankruptcy, consider the following scenarios:

1. Scenario A: You own a home with $250,000 equity in a state with an exemption limit of $100,000. You would need to consider alternative strategies to either eliminate or reduce your equity before filing.

2. Scenario B: You have a home valued at $300,000 with $150,000 equity and reside in Massachusetts, where the exemption limit is $125,000. Here, you may need to contemplate selling the home or creatively financing the equity to make your home more affordable.

| State | Home Value | Equity | Exemption Limit | Scenario Impact |

|---|---|---|---|---|

| Texas | $400,000 | $100,000 | $100,000 | Full exemption allowed |

| Florida | $250,000 | $200,000 | Unlimited | Full exemption allowed |

| Massachusetts | $300,000 | $150,000 | $125,000 | Partial exemption (sell or finance) |

| California | $450,000 | $200,000 | $75,000 | Partial exemption (need to reduce equity) |

Real-World Examples

- Example 1: Meet Sarah, who owns a home valued at $350,000 with $200,000 equity in Ohio, where the exemption is $150,000. To protect her home, she decides to use some savings to pay off a part of her mortgage, thereby lowering her equity to $120,000, which falls beneath the exemption limit.

- Example 2: John in California owns a home with $450,000 value and $200,000 equity. He opts to sell the home before filing for bankruptcy, clearing his debts and triggering a lower price point to start fresh.

Practical Considerations

When considering options as a homeowner facing bankruptcy, keep these actionable tips in mind:

- Consult an Attorney: A bankruptcy attorney can provide tailored advice based on your state laws and individual circumstances.

- Assess All Assets: Review all your assets, not just home equity, as other exemptions may significantly impact the bankruptcy process.

- Explore Alternatives: Seek financial counseling to evaluate whether you can negotiate for lower loan terms or explore other debt relief options before considering bankruptcy.

Understanding your state’s exemption laws and preparing accordingly can empower you to retain as much of your equity as possible. By being proactive and strategic in your approach, you can navigate the complexities of bankruptcy more effectively.

Evaluating the Advantages of Filing

When considering filing for Chapter 7 bankruptcy, evaluating the advantages can empower you to make informed decisions about your financial future. It’s essential to understand the potential benefits you may gain by filing, especially related to your home equity.

Key Advantages of Filing for Chapter 7

1. Debt Erasure: One of the most compelling advantages of filing for Chapter 7 is the ability to discharge unsecured debts. Around 72% of filers report significant relief from debts like credit cards and medical bills, which can allow you to focus on maintaining your home without the burden of overwhelming financial pressure.

2. Keep Your Home: Depending on your equity and the state laws, you can often retain your home even while discharging other debts. If your equity falls within the state exemption limits, you can protect your asset. For instance, states like Texas offer protection for equity up to $100,000, providing reassurance for homeowners.

3. Fresh Financial Start: Filing for bankruptcy can offer a fresh start. A common sentiment among filers is liberation from debt, with about 63% stating they feel an immediate relief to move forward. This can lead to improved mental health and financial stability.

4. Automatic Stay: Once you file, an automatic stay goes into effect, halting creditor actions including foreclosure and collections. This means you can temporarily halt any anxiety about losing your home while resolving your financial situation.

Comparative Table: Advantages of Filing for Chapter 7

| Advantage | Description | Percentage Impacted |

|---|---|---|

| Debt Erasure | Discharge of unsecured debts | 72% of filers |

| Retain Home | Potentially keep home if equity is exempt | Varies by state |

| Fresh Financial Start | Improved financial outlook and mental relief | 63% feel liberated |

| Automatic Stay | Prevents creditor actions and collections | Instant effect |

Real-World Examples

Consider Sarah, a homeowner from Florida who filed for Chapter 7 with $50,000 in unsecured debts. With home equity protected due to Florida’s unlimited exemption rule, she was able to retain her home while eliminating her debts. Sarah reports now having the breathing room to manage monthly expenses without the former stress.

In contrast, John from Maryland had $30,000 in equity, which was protected by the state’s exemption limits. By filing, he not only discharged credit card debt but also halted a pending foreclosure action, allowing him to restructure his financial life.

Practical Implications for Readers

As you evaluate the advantages of filing, consider how debt discharge can directly impact your financial health. Take stock of your current debts against your home equity and state exemption limits. Knowing what you can protect can guide your decision to file for bankruptcy.

- Assess Your Debts: Calculate your total unsecured debts. If they exceed your income and you foresee challenges in repayment, bankruptcy may offer the relief you need.

- Research State Laws: Understand your state’s exemption limits regarding home equity to determine what assets you can preserve.

- Seek Professional Advice: Consulting a bankruptcy attorney can help navigate the complexities of filing and uncover the advantages specific to your situation.

Achieving financial stability through Chapter 7 bankruptcy could be a step toward regaining control of your life, provided you carefully evaluate and act on the available advantages.

State-Specific Exemptions for Home Equity

Understanding state-specific exemptions for home equity when filing for Chapter 7 bankruptcy is vital for homeowners seeking relief from financial distress. Each state’s laws dictate how much equity you can protect in your home during bankruptcy proceedings, which allows you to retain some or all of your assets.

Key Points on State-Specific Exemptions

- Variability Across States: Home equity exemptions vary significantly. For example, California offers up to $600,000 in equity protection for homeowners aged 55 and older who meet specific criteria.

- Absolute Limits: Some states like Florida provide an unlimited exemption for your primary residence, ensuring complete protection of home equity if it’s your primary dwelling.

- Local Laws Impacting Protection: In New York, exemptions can be substantially lower, generally capping at $170,825, making it critical for residents to understand their local rules.

Comparative Table of Home Equity Exemptions

| State | Exemption Limit | Notes |

|---|---|---|

| Texas | Up to $100,000 | No cap if the home is the primary residence and has no encumbrances. |

| Florida | Unlimited | Complete protection for primary residences. |

| California | Up to $600,000 | Enhanced protections for seniors (55+). |

| New York | $170,825 | General homestead exemption; varies with local laws. |

| Ohio | $145,425 | Combined with other exempt assets. |

Real-World Examples

In Texas, a homeowner with $150,000 in equity can protect all of it by claiming the homestead exemption since there is no limit if it is the primary home. Conversely, in New York, a homeowner with $250,000 in equity would only be able to exempt $170,825, leaving them at risk of losing the remaining equity during the bankruptcy process.

Consider a couple in California, both aged 62. Given their age, they qualify to exempt up to $600,000 of their $700,000 home equity, allowing them to retain most of their investment while discharging unsecured debts.

Practical Implications for Homeowners

It’s imperative to understand your state’s specific exemptions as they can drastically affect your financial recovery through Chapter 7 bankruptcy. Knowing these numbers allows you to strategize on how much equity you can safely retain and informs your path forward. For instance:

- If you reside in a state with low exemptions, consider the impact of selling your home before filing for bankruptcy, freeing up additional cash and reducing what you risk losing.

- Consult with a bankruptcy attorney familiar with your state’s laws to maximize your exemptions and potentially restructure your debts, especially if laws favor you for age or other qualifiers.

With these insights, it becomes easier to navigate the complexities of home equity and Chapter 7 bankruptcy, ensuring you make informed decisions that align with your circumstances and state-specific laws.

Financial Planning After Chapter 7 Filing

After filing for Chapter 7 bankruptcy, it’s essential to rethink and manage your finances carefully. The impact of bankruptcy on your financial situation can be profound, so having a solid plan moving forward is crucial for rebuilding your financial health. Let’s explore some key considerations to help you navigate this period effectively.

Understanding Your New Financial Landscape

Once you file for Chapter 7 bankruptcy, your financial situation transforms. Here are several important factors to consider:

- Credit Score Impact: Your credit score may drop by as much as 200 points after filing, which can impede your ability to secure loans, credit cards, and even housing rentals.

- Rebuilding Credit: Many individuals report that they can improve their credit scores by 100-150 points within a year of filing by practicing responsible credit usage.

- Budgeting Post-Bankruptcy: Developing a detailed monthly budget allows you to track your income and expenses, ensuring you live within your means while you recover.

Essential Steps for Financial Recovery

Here are actionable steps to help you regain financial stability:

1. Establish an Emergency Fund:

- Aim to save at least $1,000 for unexpected expenses. This buffer can prevent you from falling back into debt.

2. Monitor Your Credit Report:

- You can access your credit report for free once a year. Use this to identify any inaccuracies and track your rebuilding progress.

3. Limit Unsecured Credit Use:

- After bankruptcy, consider limiting the use of credit cards or loans to essential purchases, contributing to responsible financial behavior.

4. Seek Financial Guidance:

- Consulting with a financial advisor can provide personalized strategies for rebuilding your financial health and managing post-bankruptcy challenges.

Budgeting Strategies

Creating a budget that works for you post-bankruptcy involves identifying your essential expenses and income sources. Consider this example budget framework:

| Category | Estimated Monthly Amount |

|---|---|

| Housing (Rent/Mortgage) | $1,200 |

| Utilities | $200 |

| Groceries | $300 |

| Transportation | $150 |

| Insurance | $100 |

| Savings | $150 |

| Discretionary Spending | $100 |

| Total | $2,250 |

Real-World Examples of Financial Planning

Case Study 1: Sarah filed for Chapter 7 bankruptcy due to medical debt. Post-filing, she focused on improving her credit score and saved $500 within six months for emergencies. She monitored her credit report regularly, noticing a 30-point increase in her score after six months.

Case Study 2: James, after his Chapter 7 filing, created a strict budget that allocated 70% of his income to essentials and 30% for savings and discretionary spending. Within a year, he qualified for a secured credit card, allowing him to rebuild his credit responsibly.

Practical Implications for Your Financial Future

- Initiating new savings habits and sticking to a budget can significantly reduce financial stress after bankruptcy.

- By understanding your credit landscape and having a plan, you can navigate potential pitfalls and improve your financial standing within a few years.

- It’s realistic to target a credit score recovery of 100 points or more within a year if you manage your finances wisely.

By actively engaging in financial planning after your Chapter 7 filing, you set a foundation for a more secure financial future. Aim to build a positive relationship with your finances, which can lead to improved credit opportunities down the road.