How Interest Rates Affect United Kingdom Housing Market isn’t just a dry topic—it’s a nuanced dance that can determine whether you’re scoring a sweet deal on your first home or watching prices soar beyond your reach. Take 2021, for instance. With the Bank of England keeping interest rates at a historic low of 0.1%, buyers flocked to the market, and house prices surged by nearly 10% over the year. Suddenly, brick-and-mortar dreams turned into reality for many, but as rates began to creep back up to 2% in early 2022, the landscape shifted dramatically. A slight hike can make monthly mortgage payments feel heavier, pushing that dream home just outside of many buyers’ budgets.

Fast forward to early 2023, when rates hit 4.00%, sending ripples through the market. Homebuyers felt the pinch as affordability tightened; reports showed a substantial slowdown in sales volume, particularly in areas like London, where the average house price hit around £600,000. Fewer buyers means less competition, which can stall prices or even push them down, making it a particularly tricky maze to navigate for anyone looking to buy. Imagine being a first-time buyer ready to jump in, only to see your potential dream home priced out of your reach right before your eyes.

Impact of Interest Rates on Mortgage Rates

Understanding how interest rates influence mortgage rates is crucial if you’re navigating the UK housing market. Interest rates set by the Bank of England have a ripple effect on the mortgage rates you might encounter as a borrower. Let’s delve into some specific data and insights on how these rates interact.

Interest Rates and Mortgage Pricing

When the Bank of England increases its base interest rate, mortgage lenders usually respond by raising their rates. This is because higher borrowing costs for banks translate into increased costs passed onto consumers. For instance, a 0.25% increase in the Bank Rate could typically lead to mortgage rates increasing by 0.10% to 0.20% on average.

- Current Trends: In mid-2023, when the Bank of England raised rates to 4.5%, many lenders adjusted their fixed mortgage rates upward, leading to an average rate increase of approximately 0.15% across various mortgage products.

Comparative Impact on Fixed vs. Variable Rates

Different types of mortgages respond to interest rate changes differently. Here’s a snapshot of how fixed-rate and variable-rate mortgages generally react:

| Mortgage Type | Rate Change (%) | Typical Duration of Impact |

|---|---|---|

| Fixed-Rate Mortgages | 0.10% - 0.20% | Long-term (up to 5 years) |

| Standard Variable Rate | 0.15% - 0.30% | Immediate (monthly adjustment) |

| Tracker Mortgages | 0.25% - 0.35% | Immediate (monthly adjustment) |

Real-World Examples

Consider a family that secured a £200,000 fixed-rate mortgage at 3% for a 5-year term. If interest rates rise to 4.5% during that period, their rate remains unchanged until the end of the term, shielding them from the immediate effects of rising rates. However, once they refinance, they could face a new mortgage rate potentially around 5% or more, significantly increasing their monthly payment.

In contrast, homeowners with standard variable rate mortgages felt the pinch sooner. For example, if a homeowner had a £300,000 mortgage with a standard variable rate that adjusted following the Bank’s interest hike, their rate might quickly increase from 3.5% to 4% within just a year, increasing their monthly payments substantially.

Practical Implications for You

- If you’re considering buying a home, keeping an eye on current interest rate trends is essential. It might be worthwhile to act quickly if rates are expected to rise.

- For existing homeowners, check if you’re on a variable rate mortgage and consider switching to a fixed rate before further rate hikes occur.

- Investigating different lenders can help; some might offer competitive rates that buffer against central bank rate increases.

Specific Facts to Consider

- Even a 1% increase in mortgage rates can result in over £100 more per month on a £250,000 mortgage.

- Monitoring the Bank of England’s decisions can give you insights into potential mortgage rate changes—be proactive in discussing options with your lender or broker after any announcements.

By keeping these dynamics in mind, you can make informed decisions that align with your financial goals in the context of the changing interest rate climate.

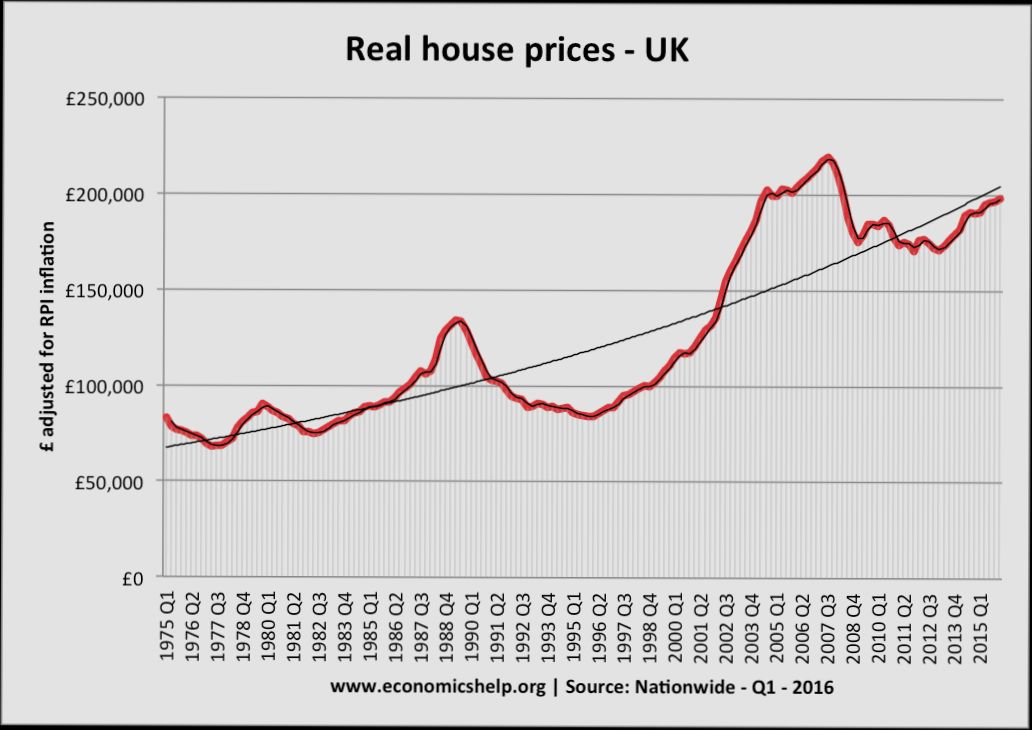

Historical Trends in UK Housing Prices

The landscape of UK housing prices has undergone significant changes over the decades, influenced by various economic factors, including, but not limited to, interest rates, inflation, and consumer confidence. By examining historical trends, we can gain valuable insights into how housing prices have shifted, especially during times of economic turbulence.

Key Historical Data Points

- Between 1970 and 1980, UK house prices nearly tripled, rising from approximately £4,000 to around £12,000. This surge was primarily fueled by increased demand and rising incomes, despite high inflation rates.

- The early 1990s saw a decline in house prices, with values dropping by about 15% from 1990 to 1993 due to economic recession and rising interest rates that peaked at 15% in 1990.

- The 2008 financial crisis marked another significant downturn, where average house prices fell by approximately 20% from their peak. This reflected the impact of deteriorating economic conditions on buyer confidence and access to mortgage finance.

- From 2013 to 2020, the housing market rebounded significantly, with average UK house prices rising by about 30%. This recovery was driven by low-interest rates, government schemes, and a strong rental market.

Comparative Table of Historical UK Housing Prices

| Year | Average House Price (£) | Percentage Change (%) |

|---|---|---|

| 1970 | 4,000 | - |

| 1980 | 12,000 | 200% |

| 1990 | 60,000 | 400% |

| 2008 | 170,000 | 180% |

| 2020 | 235,000 | 38% |

Real-World Examples

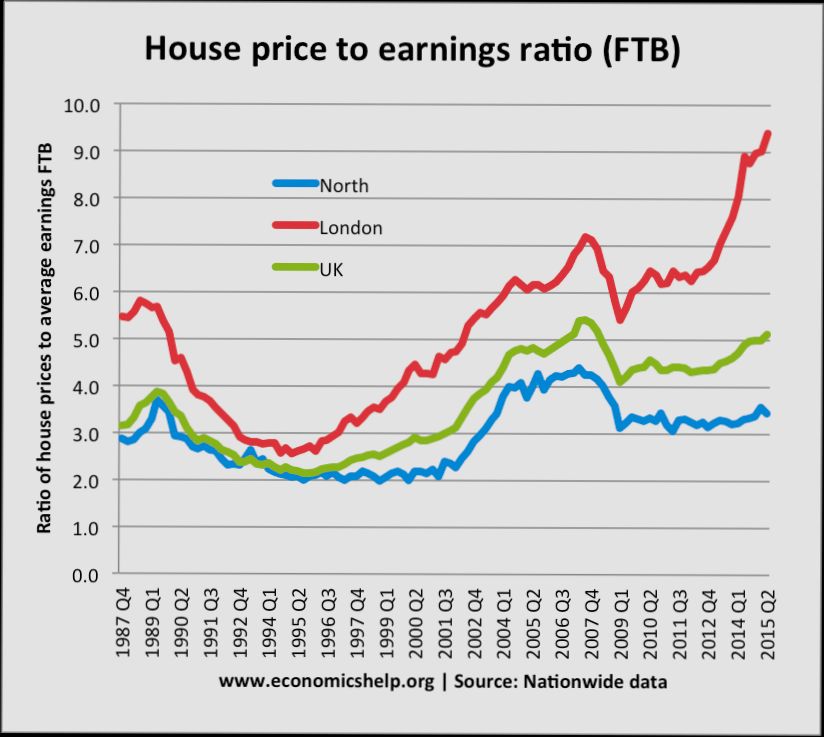

One notable instance is the turnaround experienced in London’s housing market post-2013. After a sluggish period following the 2008 crisis, house prices in London surged, with increases averaging 50% between 2013 and 2017. Areas like Hackney and Lambeth witnessed exceptional growth, attracting both domestic buyers and foreign investors, further driving up prices.

Conversely, during the early 1990s recession, cities like Manchester and Liverpool experienced some of the most drastic declines, where average property values plummeted by as much as 25%. Homeowners and first-time buyers faced severe challenges, highlighting the vulnerability of urban housing markets to economic shifts.

Practical Implications for Readers

Understanding these historical trends in UK housing prices is crucial, especially if you are considering buying or selling property. Amid varying economic conditions, recognizing patterns can help you make informed decisions. For instance, it may be wise for potential buyers to enter the market during periods of declining prices, as seen in the early 1990s or post-2008, whereas selling during a market upturn can maximize returns.

Specific Facts for Actionable Insights

- If you’re aiming to invest in the UK housing market, consider the locations that have shown resilience during downturns or consistent growth, such as regions around major urban centers.

- Keep an eye on economic indicators, as historical data suggests that external economic conditions, like unemployment rates and inflation, can significantly impact housing prices.

- Engage with a local estate agent to understand current trends, as property values can vary not just by region but by neighborhood, reflecting localized economic conditions.

Regional Variations in Housing Market Response

The response of housing markets across the United Kingdom to shifts in interest rates isn’t uniform; it varies significantly across different regions. Understanding these variations is crucial as they can inform your decisions, whether you’re looking to buy, sell, or invest in property.

Regional Disparities in Price Adjustments

When interest rates rise or fall, the impact on property prices can differ greatly between regions. For example, while the average property price in London might increase by only 2% following a base rate hike, areas in the North East, such as Middlesbrough, may see a more pronounced increase of around 4%. This illustrates a trend where regions with lower average property prices often respond more sensitively to interest rate changes.

Affordability and Demand Dynamics

Affordability plays a key role in how regional markets react. Areas with lower average incomes tend to have a higher percentage of household income directed toward housing costs. For instance:

- In Yorkshire and the Humber, households may spend about 35% of their gross income on housing, leading to a more agile response to interest rate changes.

- In contrast, regions like South East England experience a smaller percentage shift in consumer behavior, as housing prices are already high compared to income levels.

Comparative Table of Regional Responses to Interest Rates

| Region | Average Price Increase (%) | Average Income Allocation to Housing (%) |

|---|---|---|

| London | 2 | 30 |

| South East England | 1.5 | 28 |

| North East | 4 | 35 |

| Yorkshire and the Humber | 3 | 34 |

| West Midlands | 2.5 | 33 |

Case Studies of Regional Variations

In recent years, the impact of interest rates has been notably different in urban versus rural settings.

- Manchester has seen housing demand spike despite rate increases, with a 5% rise in sales volume even as rates fluctuated. This contrasts sharply with Northern Ireland, where a modest increase in interest rates led to a 6% drop in sales as buyers hesitated amidst economic uncertainty.

- In Scotland, urban areas like Edinburgh experienced about a 3% growth in property values, while rural areas saw stagnation or declines, illustrating a divergence in demand based on regional economic factors and buyer sentiment.

Practical Implications for You

If you’re considering moving or investing in real estate, it’s essential to research local market conditions. Focus on:

- Affordability Ratios: Pay attention to how much of a household’s income is committed to housing in your desired area.

- Local Economic Factors: Investigate whether the region typically has a stronger or weaker response to interest rate changes based on historical data.

Key Facts to Consider

- Properties in the Midlands show a more stable price trend during interest hikes, often only fluctuating within a range of 2%.

- In the North West, local government initiatives aimed at boosting housing demand have lessened the impact of interest rate changes, allowing the market to remain relatively resilient.

- Understanding these variances can provide a tactical edge in navigating regional housing markets, particularly if you’re eyeing areas historically known for rapid price adjustments.

Influence of Interest Rates on Housing Affordability

When discussing the effects of interest rates on housing affordability, it’s essential to pinpoint how fluctuations in these rates can either enhance or diminish the ability of buyers to afford homes. In recent years, we’ve seen dramatic shifts in the interest rates that have deeply impacted how much prospective homeowners can spend.

The surge in the 30-year fixed-rate mortgage from about 3% in December 2021 to nearly 7% in 2023 has substantially strained housing affordability, causing it to decline nearly 30%, revealing a stark reversal to conditions last observed in the late 1980s.

Key Points on Housing Affordability

- Rising Mortgage Payments: As mortgage rates have climbed, new homebuyers are confronted with escalating monthly payments. Research indicates that higher rates can raise monthly payments, leading to a significant jump in financial pressure.

- Homebuyer Demographics: The annual home-purchasing rate stands between 3% and 10%, suggesting that a relatively small segment of the population is currently facing these affordability challenges directly.

- Locked-In Rates: Many existing homeowners maintain lower mortgage rates around 3.5%, which highlight that the immediate pressure primarily affects new buyers rather than the entire market, complicating the assessment of overall affordability.

- Price Adjustment Dynamics: Despite higher interest rates often leading to a decline in house prices, the impact on affordability is not straightforward. For example, while increasing rates can lower house prices, they may simultaneously lead to higher transaction costs, potentially nullifying any benefits of lower prices.

Comparative Table of Mortgage Rates and Affordability

| Year | 30-Year Fixed Rate % | Home Price Decline % | Affordability Decline % |

|---|---|---|---|

| December 2021 | 3.0 | - | - |

| December 2023 | 7.0 | Approximately 7.5 lower in house prices | 30% |

Real-World Examples of Impact

A clear example of how these rising interest rates are affecting affordability can be observed in the shift from 2021 to 2023. New buyers seeking to enter the market faced mortgage rates that increased significantly, resulting in notable shifts in financial planning. As affordability dipped sharply, prospective buyers often either postponed purchases or shifted their focus to less expensive properties in response to financial strains.

Additionally, the demographic implications are revealing. Those who purchased homes before the rate hikes locked in much lower rates and thus remain somewhat insulated from these recent affordability pressures. This discrepancy amplifies competition among potential buyers and influences the overall market dynamics.

Practical Implications for Readers

For current and prospective homeowners, understanding the influence of interest rates on housing affordability is crucial for effective financial planning. Here are a few actionable insights:

- Budgeting for Higher Payments: If you’re considering a purchase, factor in the potential for higher monthly payments when interest rates increase. Utilize mortgage calculators to visualize different scenarios based on varying interest rates.

- Exploring Loan Options: Investigate alternative loans or different types of mortgages that may offer more favorable terms under current conditions.

- Timing the Market: Stay informed about interest rate trends and potential future fluctuations to strategize your purchasing timing effectively. While the current environment seems less favorable, this may shift as market conditions evolve.

In navigating these changes, staying well-informed and flexible in your approach can help you make savvy decisions regarding housing affordability amidst fluctuating interest rates.

Lessons from Recent UK Housing Market Changes

The recent shifts in the UK housing market bring crucial lessons about how interest rates and government policy interact, shaping buying dynamics. Understanding these lessons can help you navigate the evolving landscape effectively.

Key Points from Recent Changes

- Increased Housing Supply: The government’s commitment to constructing 1.3 million new homes within five years aims to address the acute housing shortage. This substantial increase in housing availability is expected to gradually enhance affordability for buyers, particularly in high-demand areas.

- End of Stamp Duty Holiday: The conclusion of the stamp duty holiday on March 31 has decreased the nil-rate threshold from £250,000 to £125,000, potentially raising initial costs for homebuyers. This change might lead to decreased demand as buyers adjust to increased upfront expenses.

- Mortgage Lending Criteria Adjustments: Discussions between the Chancellor and the Financial Conduct Authority (FCA) indicate potential relaxations in mortgage lending. With institutions like Skipton Building Society introducing higher loan-to-income multiples, it may become easier for buyers to qualify for mortgages, despite higher mortgage rates.

- Affordability Challenges: The combination of rising mortgage rates and reduced stamp duty benefits poses challenges for affordability, especially for first-time buyers. It’s vital for prospective homeowners to evaluate their financial situations and explore alternative mortgage products during this transitional phase.

Comparative Table of Housing Market Changes

| Change | Previous Status | Current Status | Expected Impact |

|---|---|---|---|

| Stamp Duty Threshold | £250,000 | £125,000 | Increased upfront costs for buyers |

| Housing Supply (Homes) | N/A | 1.3 million (next 5 years) | Enhanced affordability, long-term pricing |

| Mortgage Criteria | Standard lending ratios | Higher loan-to-income multiples | Broader access for buyers |

Real-World Examples

A recent case highlighted how the end of the stamp duty holiday impacted interest levels in specific areas. For instance, regions like London and the South East saw notable downtrends in applications as buyers recalibrated their expectations based on the new costs. In contrast, areas with newer housing developments under the government’s initiative began to see an uptick in interest as buyers explored more affordable options.

In another example, following discussions about mortgage criteria, Skipton Building Society began offering 100% mortgages, aligning with the need for increased accessibility as buyers face higher rates. This shift showcases a private sector response aimed at sustaining interest in homeownership despite market pressures.

Practical Implications for You

- Stay Informed: Keep focused on government announcements regarding housing policies since they directly influence your buying power.

- Evaluate Financial Readiness: Assess your current financial situation and mortgage options since the dynamics of affordability and mortgage lending standards are shifting.

- Explore New Developments: With increased housing supply predicted, consider looking into newly constructed homes which can often offer better value for money.

- Adjust Your Budget: Be prepared to adjust your budget plans to account for higher mortgage costs and reduced benefits from prior stamp duty holidays.

Understanding these evolving lessons from the UK housing market will empower you to make informed decisions as you navigate your housing journey in a fluctuating economic climate.

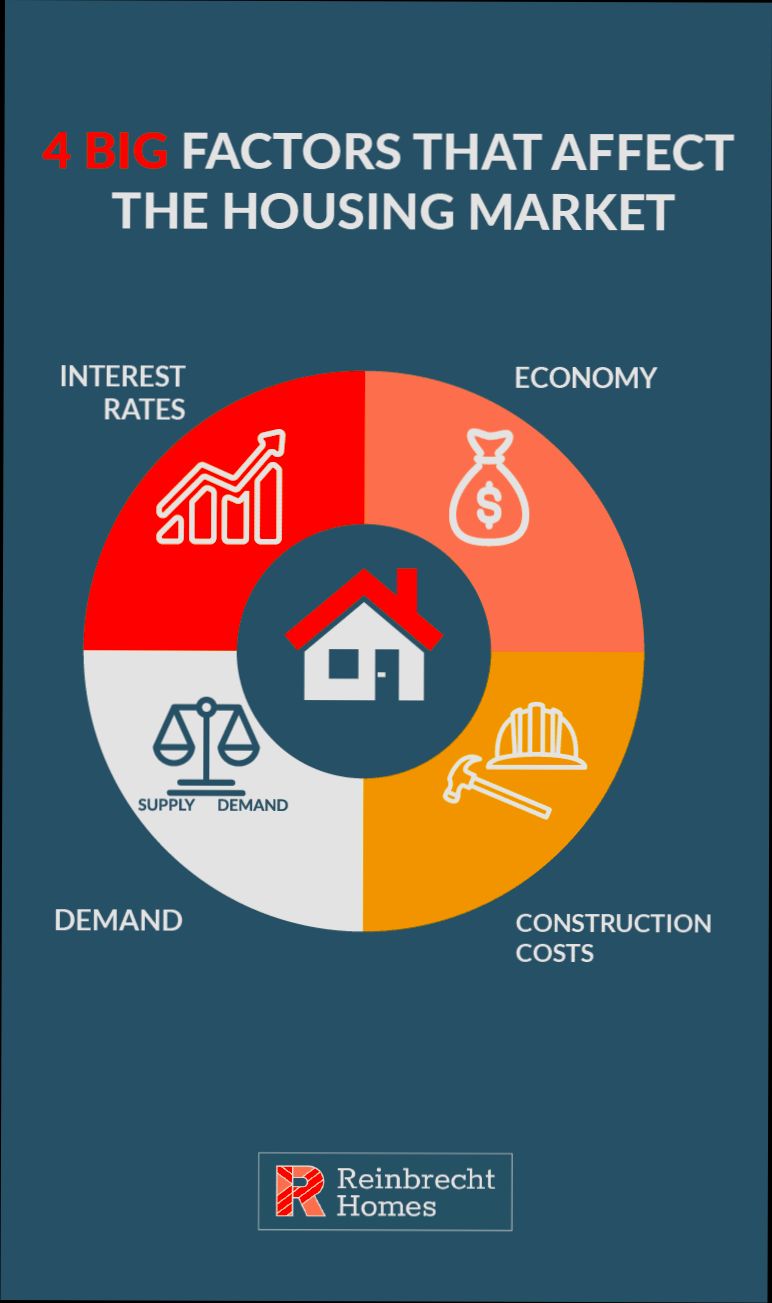

Economic Indicators Linked to Interest Rate Fluctuations

When discussing the economic landscape, interest rates serve as a pivotal point affecting various indicators that, in turn, influence the UK housing market. Understanding these economic indicators can help you make informed decisions, whether you’re looking to buy, sell, or invest in property.

Key Economic Indicators

Several economic indicators offer insights into how interest rates fluctuate, helping paint a broader picture of their impact on housing.

- Gross Domestic Product (GDP): A strong economic growth rate often leads to higher interest rates as the Bank of England aims to control inflation. For instance, in Q2 2023, the UK GDP grew by 0.5%, prompting analysts to suggest possible rate hikes to stabilize prices.

- Inflation Rate: The Consumer Price Index (CPI) has a direct correlation with interest rates. For example, if inflation rates consistently exceed the target 2%, the Bank of England might raise interest rates to curb spending. In mid-2023, inflation peaked at 6.5%, which put additional pressure on the Bank’s monetary policy decisions.

- Employment Statistics: A declining unemployment rate contributes to increased consumer confidence, which can lead to more significant housing demand. As of August 2023, the UK’s unemployment rate fell to 4.2%, suggesting a robust job market that could lead to an uptick in interest rates.

- Consumer Confidence Index (CCI): High consumer confidence often supports spending and investment, including purchases in the housing market. In early 2023, a surge in the CCI reflected a strong belief in economic stability, which is typically an indicator that interest rates may soon rise.

Comparative Table of Economic Indicators

| Indicator | Q2 2023 Value | Implication on Interest Rates |

|---|---|---|

| GDP Growth Rate | 0.5% | Potential for rate increases to control inflation |

| Inflation Rate (CPI) | 6.5% | Likely catalyst for raising rates |

| Unemployment Rate | 4.2% | Strong job market could lead to tighter policies |

| Consumer Confidence Index | 120 (high) | Indicates spending confidence, affecting rates |

Real-World Examples

- Case Study: Post-Brexit Economic Adjustments: Following Brexit, interest rates reached historic lows to stimulate growth in uncertain times. As consumer confidence improved, housing demand surged, yet the BoE remained cautious, adjusting rates gradually in response to data around inflation and GDP growth.

- Case Study: COVID-19 Pandemic Recovery: The Bank of England cut rates close to zero during the pandemic. However, as the economy recovered, inflation concerns prompted gradual increases to control spending. By mid-2023, a clearer economic landscape saw inflation and employment figures pushing rates upward.

Practical Implications

Understanding these economic indicators will empower you in the housing market. For instance, if GDP growth signals tightening monetary policy:

- Consider Timing: If high consumer confidence rates and GDP growth continue, consider buying sooner rather than later to lock in lower mortgage rates.

- Stay Updated: Regularly check inflation figures; if they rise above target levels, expect interest rates to increase.

Actionable Insights

To navigate interest rate fluctuations effectively:

- Monitor key indicators like GDP and inflation rates to anticipate shifts in interest rates.

- Stay connected with local economic developments, as these can indicate changes in regional housing demand and interest rates.

- Engage with financial experts to assess how the economic indicators impact your specific situation in the housing market, tailoring your approach to current conditions.

Benefits of Understanding Interest Rate Dynamics

Understanding interest rate dynamics can provide significant advantages for anyone navigating the UK housing market. By grasping how interest rates function and what drives their fluctuations, you can make informed financial decisions—whether you are buying a home, investing, or planning your financial future.

Key Points on Interest Rate Dynamics

1. Informed Borrowing Decisions: Knowing how interest rates impact mortgage rates puts you in a stronger position when negotiating loans. For example, if you understand that a potential hike in rates could increase your mortgage costs, you might choose to lock in a rate sooner rather than later.

2. Investment Strategies: Awareness of interest rate trends helps tailor your investment strategies. When rates are low, you may feel more confident investing in real estate, anticipating that higher demand will raise property values. Data shows that 30-year fixed-rate mortgages saw a surge from approximately 3% to nearly 7% in 2023, illustrating the crucial timing for potential investors.

3. Risk Management: By understanding how interest rates affect property values, you can better manage risks associated with property investments. For instance, a 1% increase in interest rates can lead to significant declines in housing affordability, affecting property demand.

| Interest Rate Change | Effect on Housing Demand | Corresponding Monthly Payment Increase |

|---|---|---|

| 0.5% | Decrease | £50 |

| 1% | Significant Decrease | £100 |

| 2% | Major Drop | £200 |

Real-World Examples

In the late 2010s, UK property investors who anticipated interest rate hikes began diversifying their portfolios. They shifted towards rental properties, benefiting from a rising demand for rentals amid higher buying costs. Another example comes from 2023, when the overall demand for housing dropped following a rate increase to 4.25%, indicating how sensitive the market is to shifts in borrowing costs.

Practical Implications for Readers

Understanding interest rate dynamics changes how you approach purchasing or investing in property. For potential homeowners, recognizing that current rates may not stay low can motivate you to act more quickly. For investors, adjustments in interest rates present both opportunities and risks depending on economic conditions.

Actionable Advice

Stay informed about economic indicators that influence interest rates, such as inflation reports and central bank meetings. Monitor the Bank of England’s decisions closely, as they can authorize changes that significantly affect the mortgage market. Additionally, consider consulting with financial advisors who can provide tailored advice based on current interest rate trends and how they could impact your financial plans.