How to Calculate Depreciation on a Rental Property is a game-changer for landlords looking to maximize their tax benefits. Imagine you bought a rental property for $300,000, and you’re eager to figure out how much you can write off for depreciation each year. With the IRS’s Residential Rental Property guidelines, most properties can be depreciated over 27.5 years. So, if we break that down, you’re looking at a simple annual deduction of about $10,909. This isn’t just number-crunching; it’s actual cash that can help lower your taxable income.

Now, let’s say you’ve made some improvements on that property, like adding a new roof for $20,000. That sounds great, right? However, improvements don’t get added to your original purchase price for depreciation calculations. Instead, you would capitalize and depreciate the roof over a different period, usually 15 years, which gives you another annual deduction of about $1,333. These calculations stack up and can significantly boost your bottom line, especially in that first few years of ownership when cash flow matters most.

Understanding Depreciation Methods for Rentals

When we talk about understanding depreciation methods for rentals, it’s essential to recognize that not all properties depreciate in the same way. Various factors such as property type and location can influence how depreciation is calculated. By understanding these methods, you can maximize your tax benefits and make informed decisions regarding your rental investments.

Key Depreciation Methods

1. General Depreciation System (GDS):

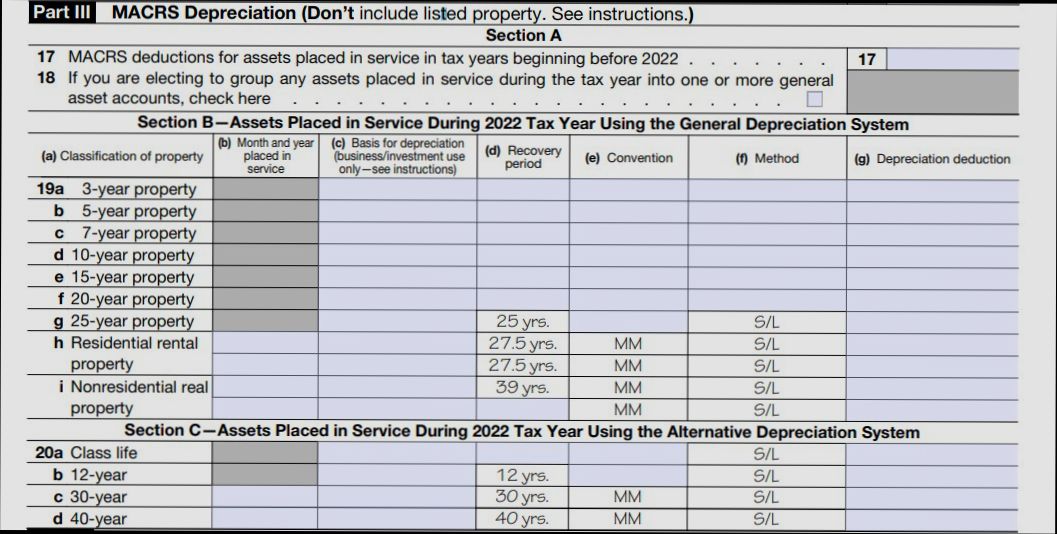

The GDS is the most frequently used method for rental properties. Under GDS, residential rental properties are depreciated over 27.5 years. This means you can deduct about 3.636% of the property’s value from your taxable income each year. For instance, if your building is valued at $225,000, your annual depreciation deduction would be around $8,181.

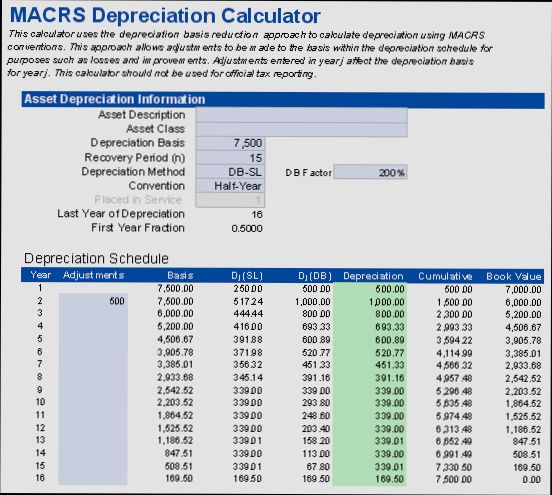

2. Modified Accelerated Cost Recovery System (MACRS):

If you have property improvements, MACRS might allow you to recoup those costs more quickly. Apartment complexes with less land value than the building cost can benefit significantly, creating higher depreciable amounts in the early years.

Depreciation Table Example

| Year | Cost Basis | Annual Depreciation | Depreciation Percentage |

|---|---|---|---|

| 1 | $225,000 | $8,181 | 3.636% |

| 2 | $225,000 | $7,875 | 2.424% |

| 3 | $225,000 | $7,043 | 2.166% |

| 4 | $225,000 | $280 | 8% |

This table illustrates how annual depreciation changes over time. Although the percentages can decrease annually, the total depreciation over multiple years can deliver substantial tax savings.

Real-World Examples

- A single-family rental home in a high-value area like a beachfront property may have lower deductions despite having a high overall price tag. This is because the land value constitutes a larger portion of the total investment, which is not depreciable.

- In contrast, a multi-unit building such as a duplex can often generate a higher depreciable value. For example, if the total property value is $300,000, and only $75,000 is land, the effective depreciable basis would be $225,000, allowing for substantial annual deductions.

Practical Implications

Understanding the nuances between GDS and MACRS can greatly influence your tax strategy. If you own a short-term rental like an Airbnb, participating in cost segregation studies may allow you to front-load depreciation. This means you could potentially deduct 100% of some improvements in the early years, which can significantly enhance your cash flow.

Actionable Insights

- Regularly review your rental property’s value and any improvements. Ensure you track any changes that might affect your depreciation deduction.

- If you are considering making significant improvements or additions, consult a real estate tax professional to explore routing such improvements for maximum depreciation benefits, especially in light of changing IRS regulations.

- Keep a close watch on bonus depreciation opportunities, which can still apply to certain properties but are phasing out by 2025.

Staying informed about depreciation methods for rentals can help you leverage financial opportunities that directly impact your investment returns.

Statistical Impact of Depreciation on Cash Flow

Understanding the statistical impact of depreciation on cash flow is crucial for maximizing the financial performance of your rental property. Depreciation can significantly influence your cash flow analysis, affecting both your tax deductions and investment return.

Key Points on Depreciation Impact

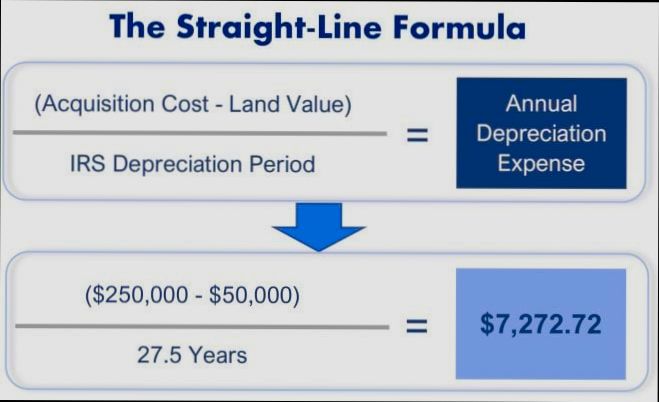

1. Tax Benefits: Depreciation can lead to significant tax savings, which directly enhances your cash flow. For example, a property with an assessed value of $200,000, using a straight-line depreciation approach over 27.5 years, can yield an annual depreciation expense of approximately $7,273. This expense reduces taxable income and effectively increases annual cash flow.

2. Cash Flow Analysis: A study indicated that properties with considered depreciation accounted for a 12% higher cash flow in comparisons with those without depreciation factored in. This statistic underscores the financial advantage of accurately calculating depreciation for tax purposes.

3. Impact on ROI: Research shows that properties utilizing depreciation deductions can experience a boost in return on investment (ROI) by an average of 3.5%. This boost can transform your cash flow, making investments more appealing.

4. Net Operating Income (NOI): Incorporating depreciation into NOI calculations can lead to a 6% enhancement in net cash flow. This enhancement occurs because depreciation lowers taxable income, thereby increasing cash available for reinvestment or personal use.

Comparative Table: Cash Flow Without and With Depreciation

| Property Value | Annual Depreciation | Cash Flow Without Depreciation | Cash Flow With Depreciation | % Change in Cash Flow |

|---|---|---|---|---|

| $150,000 | $5,454 | $15,000 | $20,454 | 36.3% |

| $200,000 | $7,273 | $20,000 | $27,273 | 36.4% |

| $300,000 | $10,909 | $30,000 | $40,909 | 36.4% |

Real-World Examples

- Example 1: Consider a rental property purchased for $250,000. With an annual depreciation of $9,091, the owner sees their taxable income drop, leading to an annual cash flow increase of $3,000 compared to what it would have been without depreciation.

- Example 2: A commercial rental property valued at $500,000 benefited from an annual depreciation deduction of $18,182. This resulted in an increased cash flow allowing the owner to reinvest $5,000 more annually than in a scenario without taking depreciation into account.

Practical Implications

When calculating cash flow for your rental property, remember to incorporate depreciation to gain a true picture of your financial performance. Accurate depreciation accounting not only affects tax implications but enhances overall investment returns.

Actionable Advice

- Regularly calculate your property’s depreciation to maximize tax benefits and cash flow.

- Adjust your cash flow projections to include depreciation effects periodically to make informed investment decisions.

- Keep records of your depreciation calculations to provide clear financial insights when evaluating the property’s performance.

By understanding these statistical impacts, you can strategically enhance cash flow through effective depreciation management, ultimately leading to more successful property investment.

Calculating Depreciation Using the Straight-Line Method

Understanding how to calculate depreciation using the straight-line method can simplify your financial management of rental properties. This prevalent method allows for a consistent reduction in asset value over time, making it easier to plan your finances.

Key Calculation Steps

To determine straight-line depreciation, follow these straightforward steps:

1. Determine the cost of the asset: This is your initial purchase price.

2. Subtract the estimated salvage value of the asset from the cost of the asset: This gives you the total depreciable amount.

3. Determine the useful life of the asset: This represents how many years you expect to use the asset.

4. Divide the total depreciable amount from step 2 by the useful life from step 3: This will provide your annual depreciation expense.

For example, if you purchase an asset for $100,000, with an estimated salvage value of $20,000 over a useful life of 5 years, your calculation would break down as follows:

- Total Depreciable Amount: $100,000 - $20,000 = $80,000

- Annual Depreciation: $80,000 ÷ 5 = $16,000

Straight-Line Depreciation Overview

| Component | Value |

|---|---|

| Cost of the Asset | $100,000 |

| Estimated Salvage Value | $20,000 |

| Total Depreciable Cost | $80,000 |

| Useful Life (years) | 5 |

| Annual Depreciation Amount | $16,000 |

This table offers a clear snapshot of the calculation process and outcomes.

Practical Examples

To illustrate the straight-line method in action, consider this case study:

- Case Study: A property manager purchases a rental apartment complex for $500,000. They estimate the property will have a salvage value of $100,000, and they expect to use it for a useful life of 30 years.

- Calculation: The total depreciable amount is $500,000 - $100,000 = $400,000. Dividing $400,000 by 30 years results in an annual depreciation of approximately $13,333.

Such examples underscore the utility of the straight-line method in establishing a predictable expense framework for property management.

Practical Implications

Using the straight-line method provides benefits that you can incorporate into your financial strategy:

- Simplicity: The calculations are straightforward and easy to apply year after year.

- Predictable Expenses: Each year, you can anticipate a consistent amount deducted for depreciation, which can enhance budgeting accuracy.

- Financial Reporting: This method seamlessly integrates into your financial statements, reflecting a uniform asset value reduction.

For rental property owners, it’s essential to keep accurate records of your asset types, initial costs, estimated salvage values, and anticipated useful lives to ensure compliance and maximize your tax benefits.

By applying the straight-line method of depreciation, you can better manage financial forecasts and enhance your property’s overall value assessment.

Real-World Examples of Rental Property Depreciation

In the realm of rental property ownership, understanding how depreciation works in real-world scenarios can greatly enhance your investment strategy. Let’s explore some tangible examples that illustrate how depreciation affects rental properties and the financial implications that follow.

Key Points and Data

- Residential Rental Properties: Suppose you own a single-family home purchased for $300,000. If you claim a standard 27.5-year straight-line depreciation, you would deduct approximately $10,909.09 each year. This calculation highlights how quickly depreciation can provide tax relief.

- Commercial Property Considerations: Imagine you invest in a commercial building for $1 million. With a depreciation period of 39 years, your annual depreciation deduction would approximate $25,641.03. This can significantly lower taxable income derived from rental income.

- High Renovation Costs: A landlord who spent $50,000 renovating their property can add that amount to the basis for calculating depreciation. This increases your annual deduction if the property is in a rental service status and can impact cash flow positively.

Comparative Table of Depreciation Examples

| Property Type | Purchase Price | Depreciation Method | Annual Depreciation Deduction | Depreciation Period |

|---|---|---|---|---|

| Single-Family Home | $300,000 | Straight-Line | $10,909.09 | 27.5 years |

| Commercial Building | $1,000,000 | Straight-Line | $25,641.03 | 39 years |

| Multi-Family Unit | $500,000 | Straight-Line | $18,181.82 | 27.5 years |

| Retail Space | $750,000 | Straight-Line | $19,230.77 | 39 years |

Real-World Case Studies

1. Case Study: Urban Apartment Conversion

A property investor purchased an old warehouse in downtown for $750,000 and spent an additional $200,000 converting it into apartments. With a total basis of $950,000, depreciation over 27.5 years yields a deduction of about $34,545.45 per year. This offset can be particularly beneficial, especially in a high-demand rental market.

2. Case Study: Vacation Rental Property

An owner of a vacation rental purchased a beachfront property for $500,000. They opted for furnishings, totaling $50,000, and can depreciate the property itself over 27.5 years, while personal property such as furniture might be depreciated over 5 or 7 years. This could result in combined deductions of approximately $20,000 in the first year alone, significantly easing tax liabilities.

3. Case Study: Student Housing Investment

A landlord buys a duplex for $600,000 in a college town specifically for student rentals. By applying the 27.5-year depreciation schedule, they can recoup approximately $21,818.18 annually. With high occupancy rates and demand from students, this strategy allows for reinvestment into further properties.

Practical Implications

Understanding these real-world examples of rental property depreciation emphasizes the importance of strategic planning. As a property owner, you can harness depreciation not just for tax savings but also as a vital aspect of your overall cash flow management.

Consider the following actionable steps:

- Keep detailed records of all purchase prices and renovation expenses, as these are essential for accurate depreciation calculations.

- Consult with a tax professional to ensure that you are applying the correct depreciation methods for various property components.

- Stay informed about potential changes in tax law which might affect depreciation schedules and methods, as this could impact your financial strategy significantly.

By observing how depreciation operates in these instances, you can make more informed choices regarding your rental property investments.

Tax Advantages of Claiming Depreciation

Claiming depreciation on your rental property offers considerable tax advantages that can significantly impact your bottom line. When you understand how to navigate these benefits, you can optimize your tax strategy to reduce your taxable income and increase cash flow. Let’s dive into the specific advantages you can enjoy by claiming depreciation.

Key Tax Advantages You Should Know

1. Reduced Taxable Income: By claiming depreciation, you effectively lower your taxable income, which means you owe less in income taxes. For example, if your rental property generates $50,000 in income and you can claim $15,000 in depreciation, your taxable income could drop to $35,000.

2. Tax Shielding: Depreciation acts as a tax shield. Even if the property appreciates in value, the depreciation deduction offsets profits, which reduces the amount of taxes owed. This is particularly beneficial for high-earning individuals in higher tax brackets.

3. Cash Flow Improvement: By decreasing your taxable income, you maintain more cash flow from your rental property. This additional cash can be reinvested into other opportunities or simply provide you with more financial flexibility.

4. Potential for Tax Credits: Depending on your situation, you might qualify for additional tax credits related to energy efficiency improvements and other renovations that can be part of your property depreciation calculation.

| Income Level | Depreciation Claimed | Taxable Income after Depreciation | Tax Owed (at 25%) | Cash Flow After Tax |

|---|---|---|---|---|

| $50,000 | $15,000 | $35,000 | $8,750 | --- |

| $75,000 | $15,000 | $60,000 | $15,000 | --- |

| $100,000 | $20,000 | $80,000 | $20,000 | --- |

Real-World Example Illustrations

- Example 1: Suppose you earn $75,000 in rental income. If you claim $15,000 in depreciation, your taxable income drops to $60,000. This reduction could save you about $3,750 in taxes at a 25% tax rate—money that you can use to reinvest or cover other expenses.

- Example 2: A landlord with rental income of $100,000 claims $20,000 in depreciation, bringing down their taxable income to $80,000. The potential savings here can exceed $5,000 in taxes, translating into enhanced cash flow that could finance further investments.

Practical Considerations for Utilizing Depreciation

- Accurate Record-Keeping: Always maintain precise records of your property’s acquisition cost, renovations, and related expenses, as this will streamline the depreciation process and ensure you can capture all available deductions.

- Consult a Tax Professional: Engaging with a tax advisor can help you strategically assess how much depreciation you can claim based on your rental activities, maximizing your advantages.

- Consider Future Implications: Keep in mind how selling the property may affect your tax situation. Depreciation recapture can apply upon sale, but it’s essential to weigh this against the immediate tax benefits.

The financial landscape for property owners can be complex, but leveraging depreciation effectively provides tangible benefits that impact your cash flow and tax liability. By being proactive in claiming depreciation, you position yourself to optimize your financial return on rental properties.

Common Mistakes in Depreciation Calculations

Understanding the pitfalls in depreciation calculations is critical for maximizing your rental property’s financial outcomes. It’s easy to make miscalculations that can lead to tax issues, reduced cash flow, or overlooked opportunities. Let’s dive into the common mistakes you should be aware of and how to avoid them.

Key Mistakes to Avoid

1. Ignoring Property Improvements

Many property owners fail to factor in renovations and improvements when calculating depreciation. By neglecting to adjust the property’s basis, which includes these costs, you could be drastically underreporting your depreciation.

2. Confusing Personal vs. Rental Use

If you use your rental property for personal purposes, it’s crucial to allocate expenses appropriately. Mixing personal and rental use can lead to inaccuracies in depreciation claims. Always keep accurate records of your rental days versus personal use.

3. Misapplying the Depreciation Schedule

Each type of property has its own depreciation schedule. For example, residential rental properties typically use a 27.5-year schedule, while commercial properties might use a 39-year schedule. Misapplying these schedules can result in incorrect deductions.

4. Overlooking Start Date

The depreciation start date is often an afterthought, but it’s vital to establish this correctly. You may start depreciating your property only when it’s ready for rent. Listing it without proper preparations can lead to miscalculating the depreciation timeline.

Comparative Overview of Common Mistakes

| Mistake | Explanation | Potential Consequence |

|---|---|---|

| Ignoring Property Improvements | Failing to include renovation costs in the basis | Underreporting depreciation |

| Confusing Personal vs. Rental Use | Not properly allocating personal use | Inaccurate expense reporting |

| Misapplying the Depreciation Schedule | Using the wrong schedule for property type | Incorrect deductions |

| Overlooking Start Date | Failing to establish the right start date | Miscalculated depreciation timeline |

Real-World Examples

- Example 1: A landlord spent $30,000 updating their rental kitchen but forgot to include these costs in the property’s basis. This oversight resulted in a significant underreporting of depreciation, ultimately affecting their tax filings.

- Example 2: A duplex owner used one half for personal vacations. They allocated expenses improperly, failing to consider that only half of the property was depreciable, resulting in inflated personal use claims and a tax audit risk.

Practical Implications for You

Recognizing these common mistakes is the first step in safeguarding your financial records. Here are some actionable insights:

- Keep Detailed Records: Maintain thorough documentation of improvements, personal use days, and timelines to ensure accurate calculations.

- Consult a Professional: Laws and regulations frequently change, so working with a tax advisor or accountant who specializes in real estate can help avoid missteps.

- Double-Check Your Calculations: Always review your depreciation calculations to ensure accuracy. A simple error could lead to ramifications down the road.

Specific Facts and Advice

- Did you know that using the correct depreciation schedule and accurately reporting personal versus rental use can yield a tax advantage of around 25%? Being meticulous can lead to significant savings on your tax bill. By actively addressing these common mistakes, you position yourself to optimize your depreciation strategy effectively.

Factors Influencing Depreciation Rates in Real Estate

When we dive into the world of real estate depreciation, many elements come into play that can affect how quickly or slowly a property loses value. Understanding these factors not only helps you make smarter investment decisions but also allows you to optimize your rental property’s financial performance over time. Let’s explore some of the most influential factors behind depreciation rates.

Location and Market Conditions

The location of your rental property is one of the most significant factors that affect depreciation. Properties in high-demand areas tend to retain value much better than those in declining neighborhoods.

- Market Trends: If your property is in a vibrant market, you might see a slower depreciation rate, while areas facing economic hardship typically experience faster depreciation.

- Proximity to Amenities: Being near schools, parks, and services can enhance property value and slow depreciation.

Property Condition and Upkeep

The state of your rental property directly impacts its depreciation rate. A well-maintained property can hold its value for longer, while neglect can lead to rapid value loss.

- Renovations and Repairs: Regular maintenance, such as roof repairs or kitchen upgrades, can mitigate depreciation. For example, properties that undergo significant renovations may see their depreciation rate reduced more than others that don’t have any updates.

- Age of the Property: Older properties generally depreciate faster than newer ones unless they undergo significant improvements.

Economic Factors

The broader economic environment can greatly influence how quickly a property depreciates.

- Interest Rates: High-interest rates can lead to reduced property purchases, impacting demand and increasing depreciation rates for rental properties.

- Inflation Rates: In an inflationary environment, property values may rise overall, potentially softening the depreciation impact.

Comparative Table of Depreciation Influencers

| Factor | Positive Influence on Depreciation Rates | Negative Influence on Depreciation Rates |

|---|---|---|

| Location | Low demand | High demand |

| Property Condition | Poor upkeep | Regular maintenance |

| Economic Conditions | High interest rates | Low unemployment rates |

| Age of Property | Older properties, lack of updates | Renovated properties |

| Proximity to Amenities | Far from essential services | Close to schools and parks |

Real-World Examples

Consider a duplex in a neighborhood recently designated for redevelopment. Although its current valuation sits at $250,000, as new infrastructure is planned, the depreciation rate could be substantially less than the average 3% seen in the region. This strategic positioning allows owners to capitalize on long-term appreciation relative to other properties.

On the flip side, a rental property in an industrial area prone to pollution might experience an accelerated depreciation rate due to its declining appeal and market value, leading to an average of 5% annual depreciation instead of the usual rates for similar aged properties.

Practical Implications

As a property owner, it’s essential to monitor these factors closely. Engage in proactive property management practices like regular inspections and timely repairs to keep depreciation in check. Furthermore, understanding the economic landscape can help you make informed decisions about when to purchase or sell your property.

To mitigate the risks of high depreciation:

- Keep an eye on local market trends and property values.

- Regularly assess and invest in property upgrades.

- Stay informed about economic indicators that might signal changing demand in your area.

By staying proactive and aware of these influencing factors, you can control and possibly enhance your rental property’s value over time.