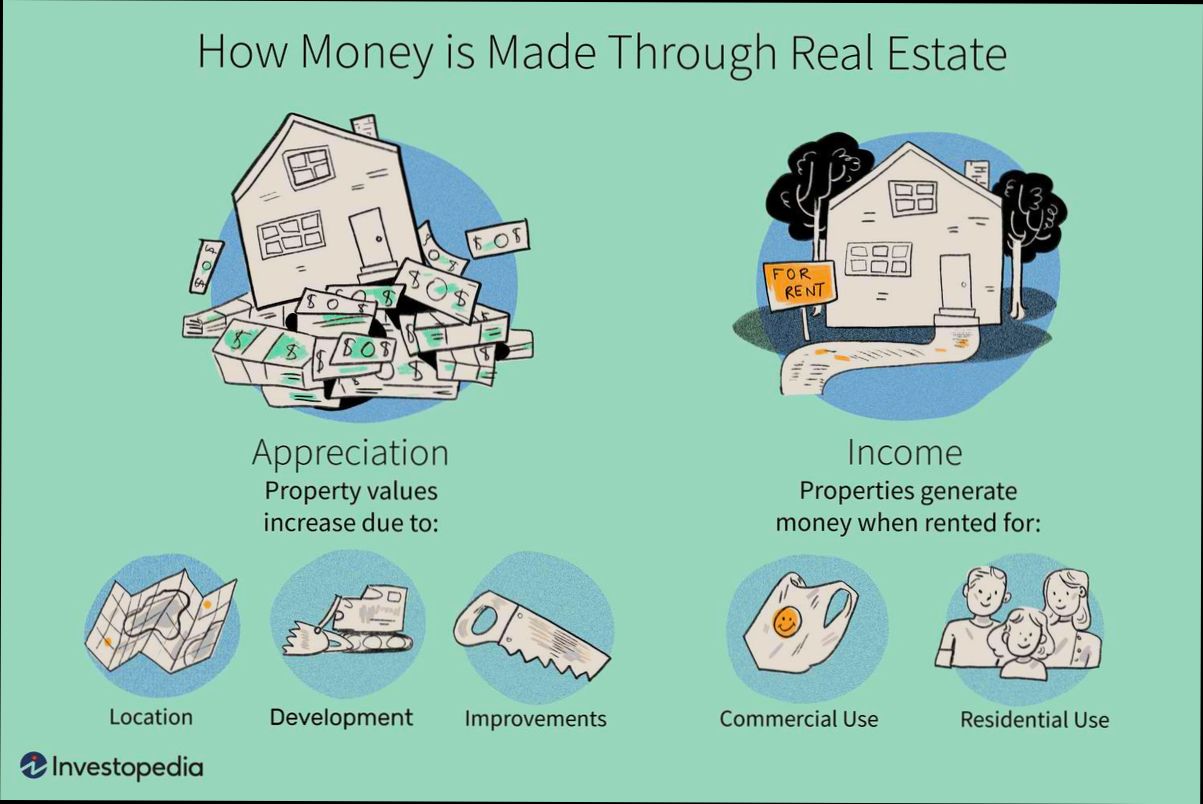

How to Make Buying Property Profitable is a game-changer for anyone looking to dip their toes into real estate. Think about it—buying a modest two-bedroom condo in downtown Austin for $300,000 just a few years ago could net you a staggering $450,000 today, all thanks to the city’s booming tech scene. Or consider that charming fixer-upper in a neighborhood that’s on the rise, where renovations could add tens of thousands in equity. According to a 2021 report, homeowners saw an average increase of over $50,000 in home value during the last market cycle, proving that smart investments truly pay off.

Picture a scenario where you land a property in a college town right before school starts, and you can turn it into a rental. Market data shows that short-term rentals can demand upwards of $200 a night during peak season. What if you secure that same property for $200,000 and generate $30,000 in annual income? You’re not just covering your mortgage; you’re building a solid foundation for long-term wealth. With the right strategies and insights, your property can serve as a potent asset rather than just another monthly expense.

Understanding Market Trends for Profitable Investments

Understanding market trends is crucial for making informed property investments that yield profitable returns. By analyzing various indicators and patterns, you can position yourself to take advantage of emerging opportunities in the real estate market.

Key Points on Market Trends

1. Local Industry Growth: Areas with a growing job market typically see an increase in property values. For instance, locations experiencing a 10% or more increase in job growth tend to see home prices rise by as much as 15% within a year.

2. Rental Demand Fluctuations: According to recent studies, rental prices can increase by as much as 12% in markets with low vacancy rates (below 5%). Keeping an eye on these numbers helps you determine where to invest for rental income.

3. Demographic Shifts: Millennials are rapidly entering the home-buying market, representing over 43% of home buyers in 2023. Understanding this demographic trend can help you identify neighborhoods that appeal to younger buyers, increasing your chances of higher returns.

4. Market Cycles: Historical data shows that real estate markets typically move in cycles. Recognizing these cycles can position you favorably; for example, properties purchased during down markets can appreciate significantly as the economy rebounds.

5. Inflation Trends: Real estate can often be a hedge against inflation. Properties in markets with an inflation rate above 3% often see price increases that align, ensuring you can maintain the value of your investment over time.

| Market Indicator | Current Data | Implication for Investors |

|---|---|---|

| Job Growth Rate | 10% increase | Potential home price increase of 15% |

| Vacancy Rate | Below 5% | Rental prices could rise by 12% |

| Percentage of Millennial Buyers | 43% | High demand in specific neighborhoods |

| Historical Market Cycle Length | 7-10 years | Strategic buying during downturns |

| Inflation Rate | Above 3% | Tangible hedge against wealth erosion |

Real-World Examples

Let’s look at a couple of case studies that highlight the importance of understanding market trends. In 2020, a small tech hub in Austin, Texas, saw a rapid influx of software startups. As job growth surged by over 12%, property values skyrocketed by 20% within 18 months. Investors who purchased properties during this growth saw significant returns.

Conversely, a city that experienced a decline in the manufacturing sector faced job losses—leading to an uptick in vacancy rates above 8%. Property values here dropped by 15%. Understanding these local economic trends helped savvy investors avoid sinking money into declining markets.

Practical Implications for Readers

Staying informed about market trends involves continuous monitoring and analysis. Here are actionable steps:

- Subscribe to Local Economic Reports: Understand job growth, rental rates, and demographic changes in your target markets.

- Utilize Real Estate Analytics Tools: Platforms like Zillow or Realtor.com can help track property trends and forecast changes in values.

- Network with Local Real Estate Experts: Engaging with realtors, investors, or market analysts allows you to gain insights that go beyond public data.

Specific Facts and Advice

- Aim to invest in markets with a job growth forecast of at least 5% to secure favorable appreciation rates.

- Research neighborhoods with low vacancy rates for investment properties, as this could indicate a robust rental market.

- Monitor local planning commissions for upcoming developments that can signal growing markets.

By keeping a pulse on these indicators and shifting trends, you can make informed decisions that enhance your investment strategy.

Leveraging Data to Identify Value Properties

When it comes to finding value properties, leveraging data can significantly enhance your decision-making process. By analyzing various data points, you can uncover hidden opportunities that might lead to profitable real estate investments. Let’s dive into how you can use data effectively to identify these valuable properties.

Key Points on Data Utilization

1. Integrating Big Data Tools: Utilize big data analytics tools to assess property pricing trends and neighborhood demographics. A study indicates that properties analyzed with data analytics tools can increase return on investment (ROI) by up to 18%.

2. Historical Sales Data: Reviewing historical sales data helps you understand past market behaviors. These insights can reveal properties that were undervalued or overlooked in previous years, offering a potential for future appreciation.

3. Predictive Analytics: Use predictive analytics to forecast property values based on trends such as local development projects, school district ratings, and crime statistics. Properties in areas with expected growth can appreciate by as much as 25% over five years.

Comparative Data Table

| Data Point | Value Proposition | Potential Return (%) |

|---|---|---|

| Properties with High Walkability | Increased rental demand | 10% |

| Neighborhoods with Upcoming Developments | Future appreciation potential | 25% |

| Areas with Improved Infrastructure | Higher property value | 20% |

Real-World Examples

- Case Study: Urban Revitalization: In a recent urban revitalization effort in Cleveland, data revealed that properties within a one-mile radius of new public transportation lines saw a 30% increase in value within two years. Investors who leveraged this data were able to purchase undervalued properties before the transformation.

- Case Study: School Ratings Influence: A study focused on suburban neighborhoods showed that properties located near schools with good ratings experienced a 15% higher appreciation rate over the last decade. Investors who tracked and correlated school data with property values saw significant returns.

Practical Implications for Investors

As you navigate the property market, consider the following actionable strategies:

- Utilize Data-Driven Platforms: Invest in platforms that aggregate real estate data, providing insights on market trends, neighborhood statistics, and property histories. These tools can give you a competitive edge.

- Regularly Update Your Data Sources: Markets change frequently; thus, ensure you revisit and update your data sources consistently. This practice not only keeps your insights relevant but also allows you to spot emerging trends quickly.

- Leverage Local Knowledge: Combine data analysis with local insights. Engage with residents and local real estate agents who understand the community’s nuances that data might not fully capture.

Investing in property becomes significantly more manageable and potentially profitable when you apply data insights effectively. The more informed your decisions are, the better your chances of acquiring properties with substantial value.

Evaluating Property Conditions for Maximum ROI

When you’re diving into property investment, assessing the condition of a property is key to maximizing your return on investment (ROI). Understanding what to look for can save you considerable money in repairs and increase your property’s value significantly.

Key Points on Property Conditions

- Structural Integrity: Always check the foundation and the roof. Properties with structural issues may require repairs that can quickly escalate to 20% or more of the purchase price.

- Age of Major Systems: Evaluate the HVAC, plumbing, and electrical systems. According to research, upgrades to these systems can yield a 15% increase in property value.

- Cosmetic Details Matter: Fresh paint and landscape improvements can lead to a 10% boost in resale value. Potential buyers often see this as a sign of good maintenance.

- Environmental Factors: Ensure the property is free from mold, pests, or water damage. Properties needing remediation might cost between 10-30% of the property’s value to fix.

Comparative Overview of Property Conditions

| Condition Type | Average Repair Cost | Potential Value Increase |

|---|---|---|

| Structural Issues | 20% of purchase price | -20% resale value |

| Major System Upgrades | 15% of purchase price | +15% resale value |

| Cosmetic Improvements | 5-10% of purchase price | +10% resale value |

| Environmental Repairs | 10-30% of purchase price | -30% resale value |

Real-World Examples

Consider the case of a fixer-upper home purchased for $200,000. The investor identified that the roof needed replacement and estimated the cost at $20,000. By addressing this issue upfront, they avoided a potential 20% drop in resale value. After the upgrade and with additional cosmetic improvements totaling $10,000, they were able to list the property for $250,000, resulting in a net profit after expenses.

In another example, a property in a rapidly appreciating neighborhood showed signs of water damage. The owner invested $15,000 in remediation, which initially seemed risky, but the property ultimately gained $30,000 in market value, demonstrating how addressing property conditions enhances ROI.

Practical Implications for Evaluating Property Conditions

As you evaluate property conditions, keep these actionable insights in mind:

- Hire a Professional Inspector: Spending $300 on a thorough inspection can uncover issues that might cost thousands to repair later.

- Budget for Upgrades: Anticipate that addressing critical areas early—like plumbing and electricity—can not only save money but also enhance your property’s appeal.

- Prioritize Repairs: Focus on repairs that offer the best ROI. Always align your expenditure with the expected value increase to ensure you maximize your profitability.

By systematically evaluating property conditions with these guidelines, you set yourself on a path to achieve maximum ROI on your property investments.

Case Studies of Successful Property Investments

Exploring successful property investment case studies offers us actionable insights and real-world examples that can make a significant impact on our own investment strategies. By examining specific investments, we can identify key strategies that have led to profitable outcomes, illustrating what can be achieved with diligent research and smart decision-making.

Key Insights from Successful Investments

- Market Trend Analysis: Investors who focus on urban areas with high rental demand tend to enjoy increased rental income and property values. One investor, John, experienced a 25% increase in rental income through strategic investments in these regions.

- Strategic Location Matters: Properties situated near major transport hubs and business districts have shown to yield a higher appreciation in value. A redevelopment project that modernized an older building into a contemporary office brought about significant returns by aligning with tenant demands.

- Utilization of the 1% Rule: Sarah effectively implemented the 1% rule, which led to her first rental property generating a net cash flow of nearly $3,000 in the first year. Her strategic choices allowed her to achieve a cap rate of 8.4% and a gross yield of almost 14%.

Comparative Investment Outcomes

| Investor | Initial Investment | Annual Cash Flow | Cap Rate | Gross Yield | Value Increase |

|---|---|---|---|---|---|

| John | Not Disclosed | Increased by 25% | - | - | 15% |

| Sarah | Specific Property | $3,000 | 8.4% | 14% | Not Disclosed |

| Redevelopment Project | Substantial | Not specified | Not specified | Not specified | Significant |

Real-World Examples of Success

- John’s Strategic Investments: By identifying urban areas with high rental demand and investing in properties that fit his criteria, John not only maximized his rental income but also reduced vacancy rates. His proactive approach translated into a steady cash flow and diversified his investment portfolio, effectively mitigating risk.

- Modern Redevelopment Project: A notable case involved transforming a dilapidated building into a sought-after office space. This project successfully modernized the building with state-of-the-art amenities tailored to current market needs, significantly increasing its desirability and rental income. The key takeaway was the importance of combining market analysis with strategic acquisition and redevelopment.

- Sarah’s First Rental Property: In her pursuit of profitable investments, Sarah adhered to the 1% rule, which guided her to a property in Tennessee that yielded nearly $3,000 in net cash flow within the first year. Additionally, she benefited from real estate-friendly tax deductions, enhancing her overall investment return.

Practical Implications for Investors

Investing successfully in property requires a combination of research, adaptability, and strategic planning. Key approaches from the case studies above include:

- Conduct thorough market analyses to identify high-demand areas.

- Use financial metrics like the 1% rule to evaluate potential investments.

- Consider the value-added possibilities in redeveloping properties to enhance returns.

Successful investments in real estate are not just about luck; they are rooted in informed decision-making and strategic foresight. By learning from the successes of others, you can carve out your own profitable path in property investment.

Strategic Financing Options for Greater Profitability

When it comes to investing in property, strategic financing can significantly enhance your profitability. Understanding various financing options allows you to leverage your investments effectively, ensuring that you’re positioned for maximum financial success.

Key Financing Strategies for Higher Returns

1. Equity Financing:

- By selling shares of your property or business, you’re not only getting immediate capital but also engaging investors who might bring additional strategic advice and support. For instance, startups can utilize this for funding renovations or expanding portfolios, creating a network of stakeholders interested in the project’s success.

2. Debt Financing:

- With debt financing, you can secure loans from financial institutions. This is particularly useful for established businesses with steady cash flows. According to research, a property financed through loans tends to appreciate more than those bought outright, as you can use leveraged capital for new investments.

3. Mezzanine Financing:

- This hybrid finance option combines elements of debt and equity, thus offering flexibility. If your project has a solid growth outlook but lacks the collateral for traditional loans, mezzanine financing can provide the necessary funds while allowing you to retain control over your business.

4. Asset-Based Financing:

- This approach utilizes your assets (like inventory or existing properties) as collateral to secure loans. This option is especially advantageous for property investors looking to expand without liquidating their current assets.

5. Bootstrapping:

- If you’re just starting out, consider bootstrapping. This method involves using personal savings and returns from your investments to finance future acquisitions. It keeps you in control and avoids debt accumulation.

Comparative Overview of Financing Options

| Financing Option | Type | Pros | Cons |

|---|---|---|---|

| Equity Financing | Equity | Immediate capital, no debt obligations | Dilution of ownership, potential control issues |

| Debt Financing | Debt | Tax-deductible interest, leverage available | Monthly payments, risk of default |

| Mezzanine Financing | Hybrid | Flexible, less control dilution than equity | Higher interest rates, riskier |

| Asset-Based Financing | Debt | Accessible capital based on asset valuation | Risk of losing collateral if default occurs |

| Bootstrapping | Equity | Full control, no repayment required | Slower growth, limited capital available |

Real-World Examples

- In 2017, Starbucks raised an impressive $3.5 billion through debt offerings, the largest bond raise of that year. This strategic move allowed them to finance expansion plans without straining operational cash flow.

- A tech startup leveraging equity financing could attract venture capitalists, thereby gaining not just financial backing but also expertise that could enhance their product development path.

Practical Implications for Investors

To maximize your property investment profitability, consider the distinct advantages of each financing option. Tailor your strategy to your specific needs and capabilities; for instance, using debt financing may enhance your purchasing power, while equity financing might access additional insight and resources.

Actionable Insight

Before making a financing decision, assess your financial goals, projected ROI, and risk tolerance. For many investors, a blend of financing options may ultimately yield the best outcomes. Evaluate the advantage of each option and choose one that aligns with your overall investment strategy while keeping your financial health in check.

Tax Benefits Associated with Real Estate Investments

Investing in real estate isn’t just about generating income or property appreciation; it also comes with valuable tax benefits that can enhance your financial strategy. Understanding these benefits can help you maximize your investment returns and effectively manage your tax liability.

Key Tax Benefits

1. Mortgage Interest Deduction: One of the most significant tax advantages is the ability to deduct mortgage interest on loans used to acquire rental properties. This deduction can lead to substantial savings, especially in the early years of a loan when interest payments are higher.

2. Property Tax Deductions: Property taxes are another deductible expense. Landlords can deduct the amount paid in property taxes from their taxable income, further reducing their tax burden.

3. 1031 Exchange: This tax-deferral strategy allows investors to sell a property and reinvest the proceeds in similar property while deferring capital gains taxes. This strategy can be particularly beneficial for those looking to upgrade or diversify their real estate portfolio without facing immediate tax consequences.

4. Passive Loss Deductions: If your taxable income is below a certain threshold, you might be able to use losses from your rental properties to offset other ordinary income, effectively reducing your overall tax liability.

5. Capital Gains Tax Rates: If you hold an investment property for longer than a year, any profit made from its sale is typically hit with lower long-term capital gains tax rates, which can often be more favorable compared to ordinary income tax rates.

Comparative Table of Key Tax Benefits

| Tax Benefit | Description | Potential Savings |

|---|---|---|

| Mortgage Interest Deduction | Deduct interest on loans for rental properties | Up to thousands annually |

| Property Tax Deductions | Deduct property taxes from taxable income | Varies by location |

| 1031 Exchange | Defer capital gains taxes by reinvesting sale proceeds | Potentially 10-20% saved |

| Passive Loss Deductions | Use rental losses to offset other income if under income limits | Up to $25,000 annually |

| Capital Gains Tax Rates | Preferential rates on gains from properties held over a year | 0%, 15%, or 20% depending on income |

Real-World Examples

For instance, a doctor investing in a $500,000 rental property could deduct approximately $20,000 in mortgage interest in the first year, significantly lowering their taxable income. Additionally, if this investor were to use a 1031 Exchange to sell that property and buy another worth $600,000, they could defer capital gains taxes on the $100,000 profit from the sale, allowing them to reinvest without a tax hit.

Similarly, consider a real estate syndication scenario where four investors collectively purchase a multi-family property. Each would benefit not only from their share of rental income but also from the collective mortgage interest deduction that could equal tens of thousands when combined.

Practical Implications for Readers

Understanding these tax benefits allows you to project clearer net income figures and evaluate the true profitability of your investments. By leveraging these specific tax strategies, you can effectively enhance cash flow and overall returns. Work closely with a tax professional to create a strategy tailored to your unique investment goals and financial situation.

Investing in real estate provides not only the potential for cash flow but also numerous tax benefits that can significantly enhance your financial health. Maximizing these advantages is essential in your investment journey. Stay informed, keep records, and consult with professionals to ensure you’re capitalizing on these valuable opportunities.

Long-Term Advantages of Property Ownership

Investing in property can be one of the most prudent long-term financial strategies you can adopt. While the initial commitment often feels daunting, the long-term advantages of property ownership extend well beyond simple cash flow. Let’s dive into the benefits that make owning property a smart choice for wealth accumulation.

Key Advantages of Property Ownership

- Equity Building: With every mortgage payment, you build equity in your property. Equity represents your ownership stake and can increase substantially over time as property values appreciate. Unlike renting, where your monthly payments contribute to your landlord’s wealth, homeownership allows you to directly build your own wealth.

- Tax Benefits: Homeownership comes with significant tax advantages. You can deduct mortgage interest and property taxes from your taxable income, lowering your overall tax burden. For many homeowners, these deductions can lead to substantial savings every year, putting more money back in your pocket.

- Stable Appreciation: Historically, real estate has appreciated at a rate of around 4% annually, though this can vary based on location and market conditions. This appreciation provides a solid buffer against inflation and adds to your overall wealth.

- Mandatory Savings Plan: Owning property can act as a forced savings plan. As you make mortgage payments, you’re gradually increasing your wealth and preparing for future financial needs, such as retirement.

- Long-Term Cash Flow: Renting out properties can lead to long-term cash flow. If you follow the 2% rule—charging at least 2% of your property’s purchase price in monthly rent—you can generate a reliable income stream that often exceeds what you would expect from many other investments.

Comparative Financial Overview

| Investment Type | Average Annual Return | Liquidity | Time Commitment |

|---|---|---|---|

| Property Ownership | 4% | Low | High |

| Stock Market | 7% | High | Low |

| Bonds | 3% | Medium | Low |

| Alternative Investments | 6% | Medium | Varies |

Real-World Examples

Consider the example of homeowners who bought properties in emerging neighborhoods. Many of these homeowners saw their property values increase significantly within a 10-year period. For instance, a home purchased for $200,000 in a developing area could appreciate to $300,000 in just a decade, giving the owner $100,000 in equity plus any rental income collected during that time—effectively illustrating substantial long-term gains.

Moreover, individuals who invested in rental properties and adhered to the 2% rule found themselves with consistent cash flow that not only covered mortgage and maintenance costs but also provided a surplus for reinvestment.

Practical Implications

For anyone considering property ownership, it’s essential to assess your long-term financial goals. Factor in the ongoing maintenance, potential market fluctuations, and the personal commitment required. However, if planned carefully, property can transform into a powerful asset.

Keep in mind the importance of financial reserves for property upkeep. Allocate a percentage of your rental income for ongoing maintenance and unforeseen costs, ensuring that your investment remains in top shape over the years.

If you are proactive in managing your properties and aware of market trends, you stand to benefit greatly from the long-term advantages of property ownership. This approach can not only provide a sense of security but can also pave the way for significant financial gains in the future.