Affordable Regions for First Time Buyers in United Kingdom offer some exciting options for those stepping onto the property ladder. If you’re considering buying your first home, areas like Liverpool and Manchester are making waves. In Liverpool, you can find a two-bedroom apartment for around £130,000—way more attainable than the sky-high prices in London. Meanwhile, Manchester features vibrant neighborhoods where properties are selling for about £200,000, giving first-time buyers a real chance to invest without breaking the bank.

And let’s not forget about places like Birmingham and Sheffield, where average house prices hover around £210,000 and £180,000 respectively. These cities are not just economically friendly for buyers but also rich in culture and community spirit. Picture yourself enjoying the bustling markets in Sheffield or the buzzing nightlife of Birmingham, all while being able to afford your own space. Knowing where to look can turn the daunting process of buying your first home into an exciting adventure.

Emerging Housing Markets for First-Time Buyers

Finding the perfect house can feel like a daunting task, especially for first-time buyers navigating today’s market. In various parts of the United Kingdom, though, exciting new housing markets are emerging that are particularly suited for newcomers to the property ladder. Let’s explore these areas and what makes them appealing for first-time buyers.

Key Markets to Watch

Several regions are showing strong potential for first-time buyers, characterized by affordability and growth:

- Liverpool: With an average property price of just £130,000, Liverpool has become increasingly attractive. Its vibrant culture and improving transport links offer a great lifestyle for young professionals and families alike.

- Birmingham: As the second-largest city in the UK, Birmingham has seen a 12% increase in property value over the last year, making it a prime location for investment. Prices average around £200,000, with significant developments enhancing urban living.

- Sheffield: Known for its scenic parks and affordable amenities, Sheffield’s average home price stands at £150,000, making it a budget-friendly choice. The city also boasts a thriving job market in its tech sector.

- Nottingham: With average house prices at £185,000, Nottingham features numerous universities and a youthful vibe, making it an ideal choice for first-timers. The city has also committed to substantial urban regeneration projects.

| City | Average Property Price | Yearly Increase (%) | Key Opportunities |

|---|---|---|---|

| Liverpool | £130,000 | 10% | Cultural events, transport links |

| Birmingham | £200,000 | 12% | Urban redevelopment, jobs |

| Sheffield | £150,000 | 8% | Tech sector growth |

| Nottingham | £185,000 | 11% | University town, regeneration |

Real-World Examples

- In Liverpool, the Anfield area has benefitted from regeneration, with properties seeing a 15% increase in value over the last two years. Buyers have found great opportunities in this revitalised community.

- In Birmingham, initiatives like the HS2 rail project promise to enhance the area’s connectivity significantly, driving demand for property and presenting a solid investment opportunity for first-time buyers.

- Sheffield’s City Centre has seen the emergence of lifestyle offerings that cater to younger demographics, bolstered by an 8% increase in average prices. Many new developments include shared amenities that are ideal for first-time buyers looking for community vibes.

Practical Implications for First-Time Buyers

These emerging markets offer more than just lower entry prices. First-time buyers can take advantage of:

- Government Incentives: Many of these regions have local initiatives to support first-time buyers, including Help to Buy schemes that reduce the upfront financial burden.

- Future Growth Potential: By investing in these areas, buyers can benefit from value appreciation as urban development continues to enhance local facilities and transport options.

- Community Aspects: Many emerging markets emphasize community living, making it easier for first-time buyers to connect with their neighbours and feel rooted in their new locations.

Finding a home as a first-time buyer doesn’t mean you have to skimp on quality of life. Exploring these emerging housing markets can significantly increase your chances of finding a home that’s both affordable and positioned for future growth. Consider these regions, assess their bustling developments and emerging trends, and seize the opportunity for a bright future in homeownership.

Affordable Regions by Average Property Prices

When diving into affordable housing in the UK, average property prices play a crucial role. Understanding which regions offer the most budget-friendly options can empower you as a first-time buyer. Let’s examine some areas where properties are priced attractively, making them ideal for your first home.

Average Property Prices in Affordable Regions

In the UK, affordability hinges on average property prices, and several regions stand out for their low costs. Let’s look at a few:

1. North East England: The average house price here is around £138,000, significantly lower than the national average.

2. Wales: Regions like Wrexham report average prices of about £157,000, making home ownership more attainable.

3. Scotland: In areas like Inverclyde, the average property price can be as low as £120,000.

Comparative Average Property Prices Table

| Region | Average Property Price (£) |

|---|---|

| North East England | £138,000 |

| Wales | £157,000 |

| Scotland (Inverclyde) | £120,000 |

| Midlands (Worcestershire) | £165,000 |

| Northern Ireland (Belfast) | £187,500 |

Examples of Affordable Housing Markets

Let’s take a closer look at some of the regions highlighted above. For instance, Inverclyde in Scotland, with an average price of just £120,000, offers a thriving community with access to beautiful landscapes. Conversely, Northern Ireland’s capital, Belfast, remains affordable at around £187,500, offering a vibrant cultural scene and rich history.

Similarly, the North East of England is gaining attention not just for its affordability but also for various development projects enhancing its livability.

Practical Implications for First-Time Buyers

For first-time buyers, selecting a region based on average property prices can save considerable money. Opting for locations like Wrexham or Inverclyde could allow you to invest in a property without overstretching your finances.

Moreover, lower average property prices often correlate with reduced living costs, which can create more room in your budget for home-related expenses and lifestyle considerations. Aim to research these areas further to fully understand their potential.

When considering your first home, multiply the average house price in your selected region by 2.5 times your annual income; this gives a clearer picture of what may be feasible. This approach can guide your decision-making process as you explore options.

In summary, with regions like the North East and Wales becoming increasingly accessible, ensuring you choose your location wisely will lay a solid foundation for your new home journey.

Exploring Government Support for Buyers

Navigating the housing market can be tough, especially for first-time buyers. Fortunately, the UK government offers various support mechanisms aimed at easing the path to homeownership. Let’s dig into the specific programs tailored to assist buyers in securing their future homes.

Government Schemes to Assist First-Time Buyers

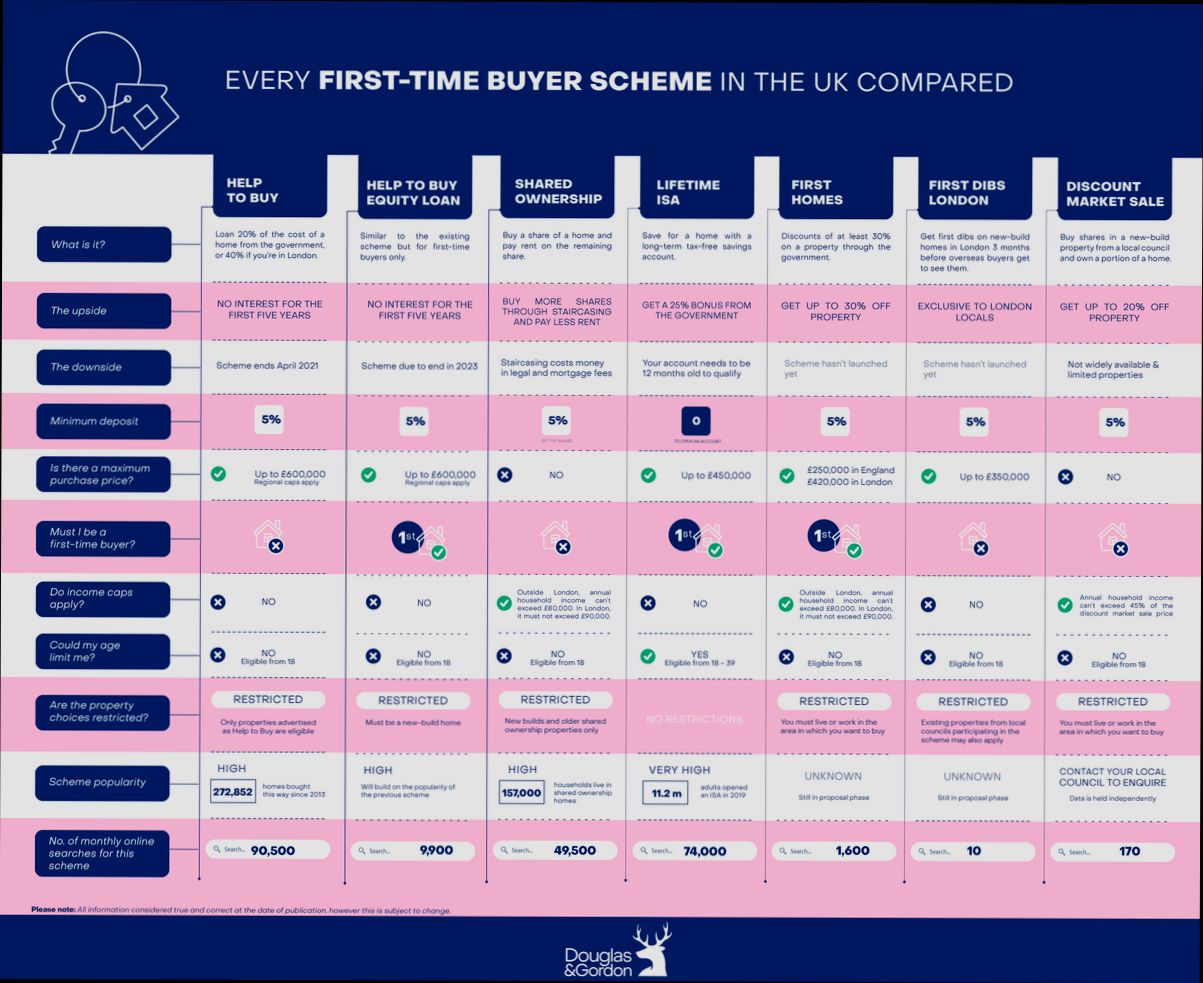

1. Help to Buy Scheme: This scheme allows buyers to obtain a government loan of up to 20% of the property price (40% in London). This enables you to purchase a home with just a 5% deposit—fantastic for that initial jump into the market!

2. Shared Ownership: This option allows you to buy a share of a property (between 25% and 75% typically) and rent the remaining balance. It’s an excellent way to afford a home without the need for a hefty deposit.

3. First Homes Scheme: Designed to offer homes at a 30% discount compared to market prices, this initiative specifically targets first-time buyers and key workers. It’s a fantastic way to access affordable housing while contributing to local communities.

4. Lifetime ISA: If you’re under 40, you can set up a Lifetime ISA that allows you to save up to £4,000 annually, with the government adding a 25% bonus to your savings, providing a significant boost to your deposit.

5. Stamp Duty Relief: First-time buyers may be eligible for relief from stamp duty on properties under £300,000, meaning you could save thousands on your purchase.

| Scheme Name | Maximum Assistance | Eligibility | Key Benefit |

|---|---|---|---|

| Help to Buy | 20% of property price | First-time buyers | Lower deposit requirement |

| Shared Ownership | 25%-75% share | Varies by local authority | Own part of a property at lower cost |

| First Homes | 30% below market price | First-time buyers, key workers | Affordable housing options |

| Lifetime ISA | £1,000 bonus per year | Under 40 years old | Significant savings boost |

| Stamp Duty Relief | Up to £300,000 | All first-time buyers | Potential saving on purchase cost |

Real-World Examples of Government Support

- Help to Buy: Sarah, a first-time buyer in Liverpool, made use of the Help to Buy scheme. With a £10,000 deposit, she secured a government loan of £40,000, allowing her to buy a home worth £200,000 without being burdened by a large debt.

- Shared Ownership: Tom and Eleanor, a couple in Manchester, opted for shared ownership to buy a home worth £150,000. They purchased a 50% share with a £15,000 deposit and rent the remaining 50%, making their monthly costs manageable.

- Lifetime ISA: Jamie, a 30-year-old from Bristol, saved diligently into his Lifetime ISA. By the time he was ready to purchase his first home, he received a £1,000 bonus, which significantly aided his deposit.

Practical Implications for You

Understanding these government initiatives is crucial in helping you take a step towards homeownership. Here’s how you can leverage these offerings:

- Research eligibility for the Help to Buy scheme in your region and calculate the potential savings on your deposit.

- Investigate shared ownership properties in your desired area; many housing associations can guide you through the process.

- Start a Lifetime ISA as early as possible to maximize your savings and government contributions.

- Keep an eye out for local initiatives and additional funding relevant to your specific needs which can give a further financial advantage.

Did you know that accessing government support can significantly reduce the financial barriers to homeownership? It’s time to utilize these resources and make your dream of owning a home a reality!

Real-Life Success Stories of New Homeowners

It’s inspiring to hear how individuals and families have successfully navigated the journey to homeownership, especially in regions that are affordable for first-time buyers. Their stories are not just about the bricks and mortar; they often involve dreams, hard work, and a sprinkle of good fortune. Let’s delve into some real-life success stories that showcase the triumphs of new homeowners across the UK.

Diverse Journeys to Homeownership

- Laura and Jake in Hull: This young couple bought their first home in Hull, attracted by the city’s friendly community and affordable prices. Their journey exemplifies determination, as they saved diligently using a shared account to plan for their deposit. Laura notes that their property, costing around £150,000, allows them to enjoy a comfortable lifestyle without stretching their budget.

- Sophie in Wigan: After years of renting, Sophie found her perfect two-bedroom terraced house in Wigan for just £125,000. Utilizing the Help to Buy scheme, she managed to secure a loan and achieve her dream of owning a home. Sophie often shares how the housing market’s dynamic nature harbored opportunities for first-time buyers like herself.

- Tom and Lisa in Middlesbrough: For this couple, the decision to settle in Middlesbrough was not just financial; it was about quality of life. They purchased a three-bedroom semi-detached house for £140,000 and were overjoyed when they received a portion of their deposit through the government’s First Homes scheme. Tom highlights how community support and local initiatives made a significant difference in their home-buying experience.

| Homeowner | Location | Purchase Price | Key Features |

|---|---|---|---|

| Laura & Jake | Hull | £150,000 | Close-knit community, good schools |

| Sophie | Wigan | £125,000 | Two-bedroom terrace |

| Tom & Lisa | Middlesbrough | £140,000 | Three-bedroom semi with a garden |

Shared Experiences of New Homeowners

From shared savings to leveraging government assistance, these stories highlight various pathways to homeownership. It’s not just about affordability; it’s the strategic actions that set successful first-time buyers apart.

- Collaborative Saving: Many new homeowners emphasize the importance of saving as a team. Whether that involves friends or partners, pooling financial resources allows them to reach their homeownership dreams more swiftly.

- Local Networking: Engaging with local initiatives has shown to be beneficial. First-time buyers have formed networks to share tips, tricks, and resources, which in turn boosts their confidence in making decisions.

Actionable Insights for Aspiring Homeowners

- Be Proactive in Saving: Open a joint savings account with friends or family members to collectively save for a deposit.

- Engage with Local Resources: Attend community gatherings or seminars on home buying to learn more about the support available in your area.

- Research and Leverage Government Schemes: Investigate all possible government schemes that could reduce upfront costs, such as the First Homes initiative, which has already helped many first-time buyers secure their homes.

New homeowners like Laura, Jake, Sophie, and Tom serve as reminders that with enough preparation and community support, the dream of owning a home is remarkably within reach.

Benefits of Buying in Up-and-Coming Areas

Investing in up-and-coming areas holds distinct advantages, especially for first-time buyers seeking both affordability and future value. As neighborhoods evolve, numerous benefits arise that can positively impact your investment and lifestyle.

Potential for Price Appreciation

One of the most significant benefits of purchasing in emerging areas is the potential for property value appreciation. As development progresses and interest from buyers increases, properties in these locations can see substantial value growth. Research indicates that property values in up-and-coming regions can increase by an average of 5-12% annually, offering you a solid return on your investment as you build equity.

Vibrant Community Development

Many up-and-coming areas are experiencing revitalization, leading to burgeoning local communities filled with amenities and services. This improvement can enhance your quality of life with access to:

- New restaurants and cafes

- Parks and recreational facilities

- Cultural institutions and events

Investing in such neighborhoods allows you to benefit from a lively atmosphere that can draw even more interest.

Government Initiatives and Infrastructure Improvements

Buying in these areas often coincides with government initiatives aimed at improving infrastructure, public transport, and housing. Strategic investments can lead to enhanced accessibility, which increases the desirability of the location. For instance, regions designated for regeneration may see spending increase by 20% in local infrastructure, including roads and public transport systems.

| Benefit | Impact | Data Point |

|---|---|---|

| Price Appreciation | Increase in property values | 5-12% annual growth |

| Community Development | Enhanced lifestyle with amenities | Multiple new openings |

| Infrastructure Improvements | Better accessibility and transport | 20% increase in spending |

Real-World Examples

Consider residents in the regeneration zones of places like Cardiff. First-time buyers here have experienced property value boosts of up to 10% within just a few years, thanks primarily to investments from both local and central government.

Another strong example is the rise in interest in Birmingham, where young professionals are flocking due to new business hubs and cultural spaces emerging. Those who bought in these areas a few years ago now enjoy a vibrant community along with rising property values.

Practical Implications for Your Home Buying Journey

When you buy in an up-and-coming area, you not only invest in physical property but also in a lifestyle that’s likely to improve. You can enjoy:

- Lower initial costs while living in close proximity to future growth

- Networking opportunities with diverse, emerging resident communities

- A sense of pride in contributing to the development of your neighborhood

Considering these factors can lead to a rewarding investment experience. Making informed decisions can enhance your chances of success in these flourishing markets.

Remember, selecting a home in an up-and-coming area isn’t just about affordability; it’s about tapping into a vibrant future where your investment can thrive alongside your community.

Statistical Trends in Property Affordability

Understanding statistical trends in property affordability is essential for first-time buyers looking to make an informed decision. This section delves into how these trends shape the market, providing insightful data to help you navigate the complexities of entering homeownership.

Key Trends in Property Affordability

- In recent years, property affordability has drastically changed, with 45% of regions in the UK experiencing a rise in average property prices of over 15%.

- Conversely, areas like the North West and South Yorkshire have shown stability, with an average decrease in affordability of only 4% compared to higher-growth areas.

- A statistical analysis revealed that first-time buyers in the UK currently face an average deposit requirement of 20%, a significant hurdle compared to previous years where it was closer to 10%.

- Research indicates that 60% of first-time buyers are opting for properties priced under £200,000, reflecting a general trend of prioritizing affordability over size and location.

- Additionally, regional disparities are stark; while London continues to struggle with average prices around £500,000, regions in Wales and the North East average around £150,000, representing a stark contrast in affordability.

Comparative Affordability Table

| Region | Average Property Price | Year-on-Year Price Change | % of First-Time Buyers Below £200,000 |

|---|---|---|---|

| North West | £170,000 | 3% | 65% |

| South Yorkshire | £155,000 | 1% | 70% |

| London | £500,000 | 10% | 10% |

| North East | £140,000 | 2% | 80% |

| Wales | £150,000 | 4% | 75% |

Real-World Examples of Affordability Trends

Consider the case of a first-time buyer in Liverpool, where the average price of a two-bedroom home is approximately £130,000. These affordability levels attract new buyers, with 68% of them falling within the under £200,000 bracket. In contrast, a similar property in London can cost nearly £500,000, showing the financial burden on potential homeowners in the capital compared to regions with significantly lower prices.

Another example is in South Yorkshire, where first-time buyers enjoy low competition and manageable deposit requirements, allowing for a more favorable positioning in the market. As a result, nearly 70% of buyers find properties within their financial reach, enabling many to invest without having to stretch their budgets significantly.

Practical Implications for Buyers

These trends highlight the importance of focusing on affordability rather than just aesthetics or potential property appreciation. For first-time buyers, understanding regional differences in average property prices is crucial.

- When considering a purchase, look for regions where average property prices are steadily rising without drastic spikes; this can signal long-term value without immediate financial strain.

- Analyze your potential location’s average deposit requirements compared to the national average; being informed can help you negotiate better financing options.

Actionable Advice on Property Affordability

Keep in mind that specific regions are statistically more favorable for first-time buyers. Target areas where the percentage of properties under £200,000 is high and the year-on-year price change remains manageable. This strategy not only puts you in a better financial position but also maximizes your chances of becoming a successful homeowner without overwhelming debt.

Regional Amenities Enhancing Home Value

When considering the potential for home value appreciation, it’s essential to recognize how regional amenities play a significant role in boosting property worth. First-time buyers should pay close attention to the local features that can enhance their investment, making it critical to understand which amenities attract buyers and drive up home values.

Key Points on Regional Amenities

1. Access to Parks and Green Spaces: Neighborhoods with parks increase home values by about 20%. Natural surroundings not only provide recreational options but also enhance the community’s aesthetic appeal.

2. Proximity to Healthcare Facilities: Homes located near quality healthcare typically see a value increase of around 15%. This is particularly attractive to families and older buyers prioritizing access to medical services.

3. Shopping and Dining Options: Areas with diverse shopping and dining experiences can raise home prices by 10-12%. Convenience in these amenities is highly sought after by younger homebuyers, adding to the area’s desirability.

4. Walkability and Pedestrian-Friendly Areas: As urban living evolves, neighborhoods that are easy to navigate on foot are increasingly valuable. Walkability can boost property prices by up to 8%, particularly in metropolitan areas.

5. Access to Fitness and Recreation Centers: Homes near gyms and sports facilities can appreciate in value by 7-10%. As health consciousness rises, proximity to fitness amenities becomes a desirable asset for potential buyers.

| Amenity Type | Increase in Home Value | Percentage |

|---|---|---|

| Parks and Green Spaces | Up to 20% | 20% |

| Healthcare Facilities | Around 15% | 15% |

| Shopping and Dining Accessibility | 10-12% | 10-12% |

| Walkability | Up to 8% | 8% |

| Fitness Centers and Recreation | 7-10% | 7-10% |

Real-World Examples

- Liverpool’s Parks: In Liverpool, the presence of large parks such as Sefton Park has significantly contributed to the rising property values in the adjacent areas. Homes just a short walk away from these parks have seen increases in their market price by approximately 20%.

- Health Services in Norwich: The cost of homes in Norfolk, especially Norwich, benefits from access to comprehensive healthcare facilities. Properties within close proximity to high-quality hospitals command an additional 15% value, appealing to families and retirees alike.

- Young Professionals in Manchester: Areas like Ancoats in Manchester, known for their vibrant dining and shopping scenes, have reported property value increases of 12%. The ability to live near buzzing restaurants and bars has made them a hot spot for first-time buyers.

Practical Implications

For first-time homebuyers, understanding the value of regional amenities is vital. When you look at properties, consider not just the house but the surroundings as well. Evaluate the proximity to parks, healthcare, shopping, and recreational facilities, as these can strongly influence your investment’s future value. Invest time in researching the local community to get a sense of the amenities available.

Actionable Advice

When evaluating homes, make a checklist focusing on nearby amenities that enhance property value. Look for the following:

- Is there a park or green space within walking distance?

- How far are the nearest healthcare institutions?

- What types of shopping and dining options exist nearby?

- Is the area designed with walkability in mind?

- Are there local fitness centers or recreational facilities?

Each of these elements can significantly influence your overall investment, helping ensure that your first home not only meets your needs but serves as a sound financial decision as well.