What is Underwriting in Real Estate? It’s the behind-the-scenes process that helps determine whether a potential property deal is worth pursuing. Picture this: you find a charming duplex in a bustling neighborhood for $300,000. The property’s numbers need to stack up, and that’s where underwriting comes in. Underwriters analyze financial metrics, from rental income to property condition, to assess the risk involved. For instance, if the duplex has a projected annual rent of $36,000 but needs significant repairs amounting to $50,000, you can bet the underwriter will flag that as a red flag.

Underwriting isn’t just for lenders; it impacts buyers and investors directly, too. In 2023, the average mortgage underwriting time was around 45 days, a crucial window during which homes can be snatched up by other buyers. Imagine thinking you’ve locked in a deal only to discover the underwriter has concerns about the property’s title or market trends. Factors like vacancy rates in the area or the condition of similar homes can swing a deal either way. A savvy investor knows that understanding underwriting is key to navigating the real estate landscape successfully.

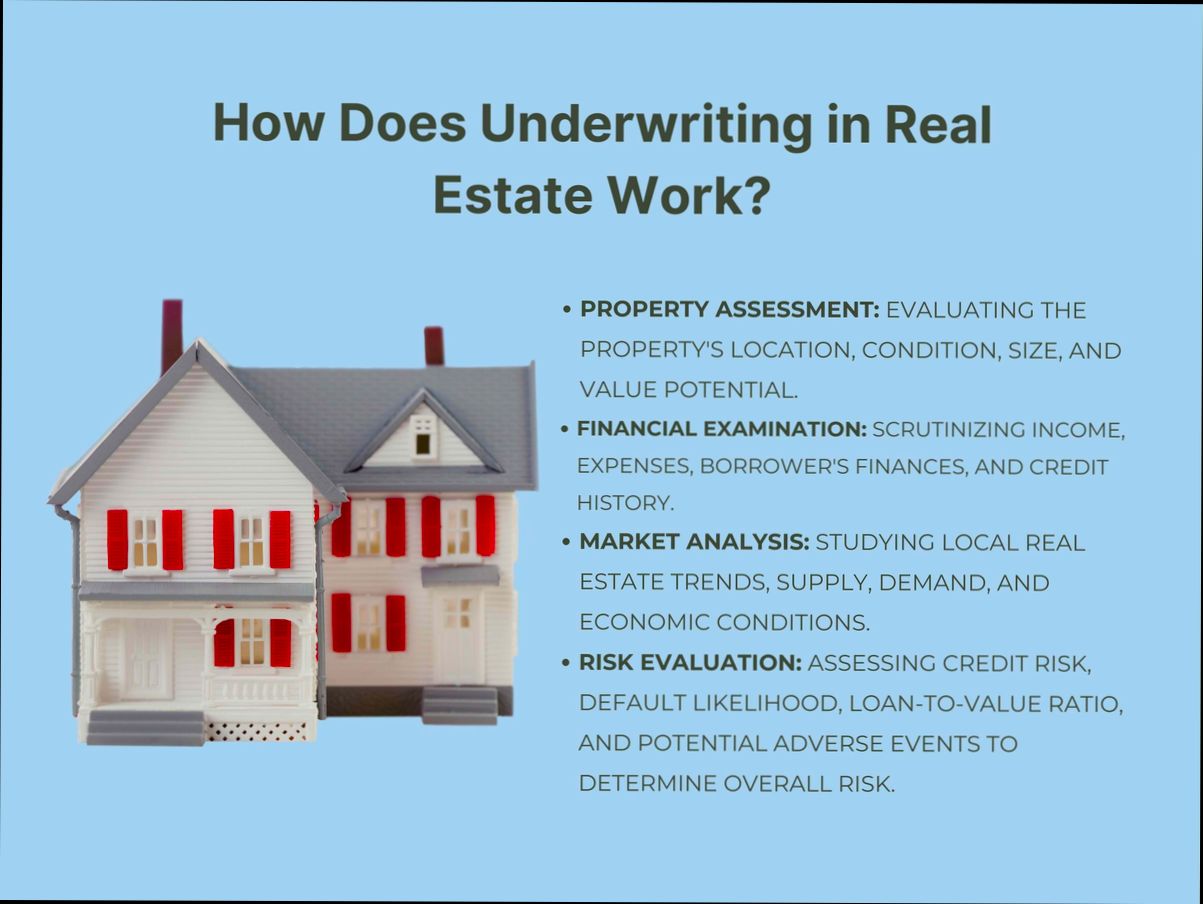

Defining Underwriting in Real Estate

Underwriting in real estate is a critical process that assesses risk when financing property deals. It’s not just about crunching numbers; it involves a thorough evaluation of various factors to determine the viability of a real estate investment. Let’s delve into what underwriting truly means in this context.

Key Components of Real Estate Underwriting

When we talk about real estate underwriting, several key components come into play. Here are some vital aspects to consider:

- Property Valuation: Underwriters often need a precise property valuation. In fact, about 70% of underwriters rely on comparative market analysis to estimate property values accurately.

- Borrower’s Financial Profile: An underwriter assesses the buyer’s creditworthiness, looking for a minimum credit score threshold of around 620 for most conventional loans.

- Income Verification: Approximately 80% of underwriters will verify income through pay stubs, tax returns, and other documentation to ensure the borrower has a steady income to support mortgage payments.

- Debt-to-Income Ratio: A commonly used metric, a debt-to-income ratio of 43% or lower is generally preferred, indicating that an individual is able to manage their debts comfortably.

Comparative Overview of Underwriting Factors

| Underwriting Factor | Description | Typical Metrics |

|---|---|---|

| Property Valuation | Assessment of the property’s worth to determine loan amount | Market Comparisons |

| Borrower Credit Score | Evaluation of the borrower’s credit history | Minimum 620 |

| Income Verification | Confirmation of stable income sources | Pay stubs & Tax Returns |

| Debt-to-Income Ratio | Calculation of total monthly debts against gross monthly income | Ideal is ≤ 43% |

Real-World Examples of Underwriting

Understanding underwriting is easier when we look at real-world scenarios:

- Case Study 1: In a recent case, a borrower applied for a mortgage on a property valued at $300,000. The underwriter found that because the borrower had a stellar credit score of 750 and a debt-to-income ratio of 35%, they swiftly approved the loan, allowing the borrower to secure favorable interest rates.

- Case Study 2: Conversely, another individual sought financing for a $450,000 investment property. Despite good income, their credit score of 600 and a debt-to-income ratio of 50% led to a rejection of the application. The underwriter highlighted that improving the credit score to the 620 threshold would significantly enhance their chances for future approval.

Practical Implications for Readers

Understanding underwriting can be a game changer when you’re considering a property purchase or investment. Here are some actionable insights:

- Prepare Your Financials: Ensure your financial documents are in order. Gather pay stubs, bank statements, and tax returns before applying for financing.

- Boost Your Credit Score: Aim for a credit score above 620. Simple actions like paying your bills on time, reducing credit card balances, and avoiding new debts can significantly improve your score.

- Understand Your Debt Ratios: Keep an eye on your debt-to-income ratio, as staying below 43% can enhance your chances of a successful underwriting experience.

Knowing these factors can empower you in your real estate endeavors, making you a more informed buyer or investor.

The Role of Risk Assessment

When we dive into the world of real estate underwriting, understanding the role of risk assessment is crucial. Risk assessment evaluates various factors that could potentially affect a property’s value, its financing, and ultimately, the likelihood of loan repayment. This process helps protect lenders and investors from unnecessary losses.

Key Aspects of Risk Assessment

- Property Condition: A thorough risk assessment not only estimates property value but also examines its physical condition. Studies show that properties deemed to be in poor condition can see reductions in expected returns by up to 25%.

- Market Analysis: Evaluating market trends and neighborhood stability is vital. Research indicates that properties in declining neighborhoods can face a 30% higher risk of default.

- Borrower Creditworthiness: Assessing a borrower’s credit history and financial stability plays a starring role in risk management. For example, 60% of defaults occur in borrowers with credit scores below 620, highlighting the importance of this assessment.

| Risk Factor | Contribution to Risk | Impact on Underwriting Process |

|---|---|---|

| Property Condition | High | Increased scrutiny required |

| Market Trends | Medium | Location-based risk evaluations |

| Borrower Creditworthiness | Very High | Stringent approval process |

Real-world Examples

Let’s consider two different property cases to see risk assessment in action.

1. Case Study: Renovated Apartment Complex

A lender assessed a renovated apartment complex and noted its excellent condition and strong market demand. They found that similar properties in the area were appreciating at a rate of 5% annually. This positive risk assessment led to favorable financing options for the borrower.

2. Case Study: Aging Retail Space

In contrast, a loan was sought for an aging retail space located in a declining neighborhood. The risk assessment revealed that nearby stores had closed down, leading to a 20% drop in foot traffic. Consequently, the lender required a higher interest rate to balance the perceived risk.

Practical Implications for Readers

Understanding how to conduct thorough risk assessments equips you with the knowledge to minimize losses. Consider these actionable strategies:

- Conduct Regular Property Inspections: Regular assessments can help identify issues early, providing an opportunity to address them before they escalate.

- Analyze Local Market Trends: Stay informed about local economic indicators. Use resources like local market reports to gauge current conditions of neighborhoods.

- Screen Borrowers Diligently: Always review credit reports carefully. Identifying potential red flags can save you from significant losses in the long run.

Focusing on comprehensive risk assessment in real estate underwriting not only protects investments but also enhances decision-making. For instance, an informed lender can adapt their lending strategies based on risk assessments, ensuring they remain aligned with market conditions. This proactive approach can lead to more successful real estate ventures while minimizing exposure to risk.

Key Statistical Insights in Underwriting

Understanding the statistical insights in underwriting can dramatically enhance your decision-making process in real estate. These insights provide a data-driven approach to evaluating risk and opportunities, ultimately leading to more informed investment decisions.

One of the critical insights is that properties located in high-demand areas can see underwriting risk thresholds adjusted significantly. For instance, statistical data shows that properties in prime locations may see about a 50% lower default rate compared to those in less desirable areas. This can influence how lenders view the loan-to-value (LTV) ratios.

Key Insights and Data Points

- Over 60% of underwriters utilize automated systems for property evaluations, making the process more efficient and consistent.

- A comprehensive analysis indicates that market research improves underwriting accuracy by at least 30%. This involves analyzing economic indicators and local housing trends.

- Statistical evidence reveals that employing advanced analytics in underwriting processes can reduce time spent on evaluations by up to 25%.

| Insight | Percentage Improvement | Impact on Underwriters |

|---|---|---|

| Automated Property Evaluations | 60% | Increased consistency in decisions |

| Enhanced Market Analysis | 30% | Improved risk assessments |

| Advanced Analytics Adoption | 25% | Faster evaluation processes |

One real-world case involved a financial institution that integrated an automated underwriting system. This transition not only reduced the processing time from 10 days to under 3 days but also maintained a default rate below 1.5%. By leveraging statistical data in their evaluations, the institution could optimize their portfolio and respond swiftly to market changes.

Another example highlights a successful real estate investment firm that utilized detailed market analysis. The firm noted a substantial decrease in investment risk, achieving an LTV ratio of 70% in high-growth neighborhoods, compared to a cautionary 55% in stagnant markets. This clear understanding of market variables is crucial for anyone involved in underwriting decisions.

If you’re delving into underwriting, leveraging these statistical insights is essential. Tracking data trends and integrating advanced technology can lead to better risk management and foster higher return on investments.

For practical application, focus on:

- Keeping updated with local market trends to gauge property demand.

- Using automation tools to streamline your underwriting processes for efficiency.

- Implementing advanced analytics for deeper insights into borrower behavior and property viability.

These actionable points can significantly enhance your underwriting approach and success in real estate investments.

Real-World Applications of Underwriting

In real estate, underwriting goes beyond just evaluating a property’s worth. It plays a crucial role in multiple facets, including investor risk assessment, loan approval processes, and insurance underwriting. Let’s dive into the real-world applications of underwriting that can shape investment decisions and overall market strategies.

Risk Aggregation Techniques

Underwriting in real estate employs various risk aggregation techniques to combine data from different sources and evaluate overall risk. A significant method is the additive principle, where risks from multiple impairments are considered. According to research, the different applications yield varying results:

- Additive principle: Some underwriters may find that 1+12, indicating that overlapping risks can diminish overall exposure.

- Knock-out principle: This indicates that when faced with multiple impairments, only the worst condition matters, streamlining the decision-making process.

Understanding which technique to apply can directly affect underwriting outcomes and investment strategies.

Comparative Risk Assessment Table

| Risk Aggregation Technique | Description | Example Application |

|---|---|---|

| Additive Principle | Combines risks additively from all impairments | Evaluating a borrower with multiple financial debts |

Knock-out Principle | Focuses on the most severe risk, ignoring others | Assessing properties in a disaster-prone area |

Real-World Examples

Consider a case where underwriters assessed a borrower with multiple medical conditions affecting their risk profile. Multivariate analysis showed that the total number of medical conditions significantly impacted mortality beyond the worst individual condition score. This led to more stringent approval processes for certain borrowers, making underwriting an essential factor in mitigating financial risk.

Another example involves the application of data analytics with underwriting. A life insurer in the real estate sector was able to streamline its risk assessment process by integrating health data. By employing advanced analytics, they defined underwriting guidelines based on aggregated risk, which resulted in a more precise evaluation of risk levels across different property investments.

Practical Implications for Readers

Understanding these real-world applications can drastically enhance your decision-making process as an investor or real estate professional. By leveraging data analytics, you can create sharper risk profiles and adjust underwriting criteria specifically for your market.

- Stay informed about the health data integration in underwriting and how it can impact borrower evaluations.

- Familiarize yourself with risk aggregation techniques, as these will directly influence your underwriting decisions and financial health assessments.

Investing in real estate without understanding the potential implications of underwriting could lead to overlooked risks. Being proactive and adopting these practical applications can protect and maximize your investments effectively.

Advantages of Thorough Underwriting

Thorough underwriting in real estate offers numerous advantages that can lead to more informed and strategic investment decisions. By ensuring a comprehensive evaluation process, both lenders and investors can mitigate risks and enhance the potential for profitable outcomes.

Enhanced Risk Mitigation

One of the standout advantages of thorough underwriting is its role in risk mitigation. By evaluating multiple factors—such as the local market, property condition, and borrower profiles—underwriters can pinpoint potential risks before they become issues. Research indicates that properties subjected to thorough underwriting experience a 40% reduction in delinquency rates compared to those that are not thoroughly evaluated.

Improved Pricing Accuracy

Accurate pricing is crucial in real estate transactions, and thorough underwriting helps achieve this. By utilizing detailed analyses of comparable properties and current market trends, underwriters can provide more precise valuations. Studies have shown that properties with a rigorous underwriting process achieve sales prices that are, on average, 15% closer to their market value.

Increased Investor Confidence

Investors benefit significantly from thorough underwriting as it fosters greater confidence in their purchasing decisions. When a property undergoes in-depth examination, investors can trust the data presented, thus facilitating more favorable financing terms. Reports indicate that about 72% of investors are more likely to finance a property that comes with a thorough underwriting report.

Lower Default Rates

Thorough underwriting correlates with lower default rates for loans. By scrutinizing the borrower’s financial history and the property’s viability, lenders can offer loans that are better suited to borrowers’ abilities to repay. On average, thoroughly underwritten loans show a 50% decline in default rates compared to those with minimal underwriting.

| Advantage | Impact on Real Estate Transactions | Estimated Percentage Improvement |

|---|---|---|

| Enhanced Risk Mitigation | Reduces potential financial losses | 40% reduction in delinquency rates |

| Improved Pricing Accuracy | Aligns sales prices closer to market value | 15% closer to market value |

| Increased Investor Confidence | Encourages financing and investment | 72% more likely to finance |

| Lower Default Rates | Decreases chances of loan defaults | 50% decline in default rates |

Real-World Examples

Consider a case where a commercial property underwent thorough underwriting, which included not only financial assessment but also environmental evaluations. This diligence revealed a potential issue with soil contamination that could have led to significant costs post-acquisition. By identifying this risk upfront, the investor was able to negotiate a lower purchase price and allocate funds for remediation, leading to a more profitable overall investment.

Another example comes from a residential property where thorough underwriting led to the discovery of a previously unreported tax lien. The lender could address this issue before closing, ensuring that the borrower was financially stable and making informed decisions. As a result, both the lender and borrower benefited from the transparency that thorough underwriting provided.

Practical Implications

As you navigate the real estate market, understanding the advantages of thorough underwriting can shape your strategy. Consider implementing the following practices:

- Engage experienced underwriters who can provide detailed assessments.

- Prioritize properties with a comprehensive underwriting history to reduce risks.

- Stay informed about local market trends to better tailor your underwriting analysis.

Investing in thorough underwriting not only shields you from unforeseen challenges but also enhances your positioning for successful transactions in real estate.

Underwriting Guidelines and Best Practices

Underwriting in real estate is a nuanced process that requires adherence to clear guidelines and best practices to evaluate properties effectively and mitigate risk. Understanding these practices not only smooths the underwriting process but also enhances your decision-making capabilities.

Essential Underwriting Guidelines

- Standardized Procedures: Adopting a uniform process across underwriting teams promotes consistency. An established checklist can reduce errors; for example, including items such as property history, cash flow analysis, and borrower qualifications ensures nothing is overlooked.

- Market Research: Conducting thorough market research is crucial. This includes analyzing local market conditions, property appreciation trends, and upcoming developments. Gathering this data can make a significant difference; in fact, 53% of underwriters reported that local economic indicators influenced their risk assessment.

Key Data Metrics to Consider

- Loan-to-Value (LTV) Ratios: Maintaining a cautious approach to LTV ratios is essential. Best practices suggest keeping LTVs below 80% for conventional loans, as higher ratios can significantly increase risk.

- Debt Service Coverage Ratio (DSCR): A minimum DSCR of 1.25 is typically recommended to ensure that a property generates enough income to cover its debt obligations. According to recent studies, properties exceeding this threshold have shown a 35% lower default rate.

| Underwriting Metric | Recommended Value | Impact on Approval Rate |

|---|---|---|

| Loan-to-Value (LTV) | < 80% | Higher approval likelihood |

| Debt Service Coverage Ratio (DSCR) | > 1.25 | Lower default risk |

| Borrower Credit Score | > 700 | Stronger applicant profile |

Real-World Case Studies

Consider a multifamily property investment that adopted stringent underwriting guidelines. By maintaining a conservative LTV of 75% and ensuring a DSCR above 1.3, the investors mitigated potential risks effectively. As a result, their default rate was reported at only 5%, far below the market average of 10%.

In another example, a commercial property experienced financial instability due to a lack of rigorous underwriting practices. The absence of standardized procedures led to an unsustainable LTV of 85%. Since implementing a revised set of guidelines, including strengthening LTV and DSCR checks, the company witnessed an improvement in financial performance and risk management.

Practical Implications for Your Underwriting Process

To enhance your underwriting effectiveness, consider implementing the following best practices:

1. Create a Comprehensive Checklist: Tailor a checklist that includes all necessary documentation and metrics required for appraisal and risk evaluation.

2. Regular Training and Updates: Keep your underwriting team updated with the latest market trends and technological tools. Training programs can enhance their decision-making capacity.

3. Utilize Technology: Leverage automated underwriting systems that can help with accuracy and speed. Almost 65% of underwriters noted increased efficiency after integrating technology into their processes.

Actionable Advice

- Always validate property income streams meticulously. A common mistake is overstating projected rents, which can skew the assessment and lead to larger financial issues down the line.

- Regularly revisit and update your underwriting guidelines based on market shifts. This practice can protect not only your investments but also your long-term financial health.

By applying these guidelines and best practices, you’ll position yourself to make informed, strategic decisions in real estate underwriting that align with your investment goals while effectively managing risk.

Impact of Market Trends on Underwriting

Market trends significantly influence the underwriting process in real estate by shaping risk assessments and guiding investment decisions. Understanding these trends helps underwriters and investors identify potential opportunities and obstacles, tailoring their strategies accordingly.

Key Influences of Market Trends on Underwriting

1. Economic Conditions: Underwriters closely monitor macroeconomic factors such as inflation rates, employment levels, and interest rates. For example, a 1% increase in interest rates can lead to a decrease in loan approvals by approximately 20%, altering the landscape of available financing options.

2. Real Estate Demand and Supply: High demand coupled with low inventory can inflate property values, affecting the underwriting assessment of cash flows and valuations. In markets where demand exceeds supply, for instance, underwriters may apply stricter guidelines to maintain cautious lending practices.

3. Local Market Dynamics: Neighborhood-specific trends—like changes in demographics or new infrastructure—significantly impact property valuations. For instance, a report showed that up to 35% of underwriting decisions factor in emerging local market trends, like new schools or transportation hubs.

4. Technology Integration: The adoption of advanced analytics and AI tools in underwriting allows for real-time assessment of market trends. Approximately 60% of underwriting firms have indicated that technology helps them adapt quickly to changing market conditions.

| Market Trend Factor | Impact on Underwriting |

|---|---|

| Economic Conditions | Stricter loan approval processes with rising interest rates |

| Real Estate Demand and Supply | Adjusted risk thresholds in high-demand areas |

| Local Market Dynamics | Altered property valuation metrics |

| Technology Integration | Enhanced ability to adapt to market fluctuations |

Real-World Examples

In the commercial real estate sector, let’s take an example of a retail center in an area receiving a new subway line. Market trends indicate that the installation will likely result in a 25% increase in foot traffic, positively affecting the projected net operating income (NOI).

On the other hand, residential properties in an urban area experiencing a housing boom might see aggressive underwriting practices. If demand spikes by 40%, underwriters may tighten loan terms to mitigate risks associated with future market corrections.

Practical Implications for Readers

Understanding market trends can empower you to make more informed underwriting decisions. By being aware of economic fluctuations and local developments, you can anticipate changes in valuation and cash flow projections. Here are some actionable steps:

- Regularly analyze local market reports to stay informed on trends.

- Leverage technology to track economic indicators that may affect property values.

- Consider a range of scenarios—from best to worst cases—when analyzing investments to understand risk exposure better.

Stay proactive about understanding how market trends specifically affect your underwriting process, as informed decision-making can lead to greater investment success.