What are Property Inheritance Laws in France? If you find yourself with a beloved family home or any property in France, it’s crucial to know how the law governs what happens to it after you’re gone. Unlike some other countries, France has a unique way of handling inheritance, heavily influenced by its Napoleonic Code. This means that children have a protected share—commonly known as “forced heirship.” For instance, if you have two kids and you own a home worth €300,000, your estate must be divided in such a way that they each receive at least €100,000, regardless of what you might have wished in your will.

Now, let’s spice things up with the fact that spouse rights in France can also surprise you. While they aren’t automatically entitled to inherit everything, they do have a strong claim, especially if you’re married. If you pass without a will, your spouse could inherit your property and an equal share in any joint possession, but only after any children have gotten their legally mandated shares. It can get pretty complicated, especially if you’ve blended families or own properties in different locations. So, whether you’re drafting a will or simply pondering what happens next, understanding the ins and outs of these laws can really shape what you plan for your loved ones.

Understanding French Inheritance Principles

When it comes to navigating French inheritance laws, understanding the principles governing inheritance is essential. In France, it’s not just about who gets what; the law has a specific order and distribution of assets depending on the presence of heirs. Let’s dive into the essential aspects of these principles.

Key Principles of Inheritance

- Forced Heirship: In France, if the deceased has children, they cannot be disinherited. The law guarantees that children inherit a significant portion of the estate, specifically three-quarters (3/4) of it, while the surviving spouse receives one-quarter (1/4). This ensures the protection of direct descendants.

- Distribution Among Heirs: The remaining inheritance is divided among heirs based on their relationship to the deceased. For instance, if a person has siblings, they could inherit collectively from the estate. More specifically:

- If the deceased has no children but has siblings, they will inherit half of the estate.

- If only one parent survives, they inherit a quarter of the estate alongside the siblings who receive the other half.

- No Children: In cases where the deceased had no children but is survived by parents, each parent will receive a half share of the inheritance. If both parents have passed, the estate transfers to siblings or other relatives.

Comparative Taxation of Shares

Here’s a quick look at how inheritance tax may affect the shares of heirs, depending on their relationship to the deceased:

| Relationship | Taxation Rate |

|---|---|

| Between parents and until the 4th degree | 55% |

| Between parents and beyond the 4th degree | 60% |

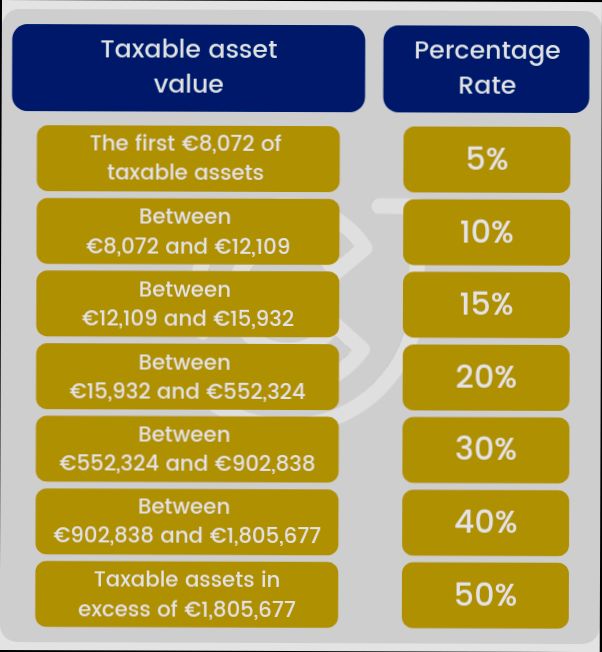

| Net taxable share up to €8,072 | 5% |

| Net taxable share between €8,072 and €12,109 | 10% |

| Net taxable share between €15,932 and €552,324 | 20% |

Real-World Examples

Consider a scenario where a parent passes away, leaving behind an estate valued at €200,000 and three children. Under French inheritance principles:

- The children collectively inherit €150,000, with each receiving €50,000 due to equal shares (3/4 of the estate).

- The surviving spouse would retain the remaining €50,000 (1/4 of the estate).

In another case, if the deceased had no children but only siblings, the estate would be split into halves, with each surviving sibling receiving a share of the inheritance. If there were two siblings and both parents were deceased, each sibling would inherit three-eighths (3/8) of the estate.

Practical Implications for Readers

Understanding these principles can significantly affect estate planning. If you are a parent in France, be aware that your children are entitled to a substantial portion of your estate, making it critical to consider this when drafting a will or determining how to manage your property during your lifetime.

Additionally, knowing the tax implications based on your relationship to the deceased can help heirs plan financially for the responsibilities that come with inheritance. For example, if you stand to inherit from distant relatives (beyond the 4th degree), the taxation rate could be as high as 60%.

In summary, understanding French inheritance principles is essential for effective estate planning and managing inheritances. Being aware of the forced heirship rules and how assets distribute among heirs can assist you in making informed decisions, ensuring your wishes are respected while navigating the complexities of inheritance law.

Key Statutes Governing Property Succession

Navigating property succession in France involves understanding several key statutes that shape how property is transferred upon death. These laws define not just who inherits, but also how much they inherit, making it crucial for anyone dealing with property in France.

Important Statutes

1. French Civil Code (Code Civil): The foundation of inheritance law in France is grounded in the French Civil Code, particularly articles 720 to 892. This code delineates the rules governing both forced heirship and the distribution of estates.

2. Law of 23 June 2006: This law introduced significant reforms to property succession, particularly focusing on cross-border inheritances within the EU. You might find it helpful, as it simplifies processes when a deceased person has ties in multiple EU member states.

3. Taxation Laws: Law No. 2007-1775 outlines inheritance tax rules, which apply to successors based on the relationship to the deceased. The rates vary significantly; for example, lineal descendants may pay between 5% to 45% depending on the value of the inheritance.

4. Law of 17 July 2001: This law allows individuals to include non-relatives in their wills to some extent, although it still respects the forced heirship principle. This provides a slightly broader scope for estate planning in line with personal wishes.

Comparative Overview of Key Statutes

| Statute | Area of Focus | Key Provision |

|---|---|---|

| French Civil Code | General inheritance regulations | Establishes forced heirship principles |

| Law of 23 June 2006 | Cross-border inheritance | Simplifies procedures for EU-related estates |

| Taxation Laws | Inheritance tax | Tax rates between 5% to 45% depending on the relationship |

| Law of 17 July 2001 | Testamentary freedom | Allows inclusion of non-relatives in wills |

Real-World Examples

- Estate of André Dupuis: After the death of André, who lived in Paris but owned property in Spain, the Law of 23 June 2006 played a crucial role. His heirs were able to navigate both French and Spanish laws due to the streamlined provisions within the EU framework, saving them time and legal fees.

- Inheritance of Sophie Martin: Sophie, an only child, was surprised to find that despite the substantial wealth of her parents, the distribution was clearly governed by the French Civil Code. The forced heirship rules dictated that she would retain a fixed portion of the estate, irrespective of her parents’ wishes otherwise.

Practical Implications

For readers dealing with property succession in France, be aware:

- Familiarize yourself with the French Civil Code to understand your rights and obligations clearly.

- If your situation involves cross-border elements, consider consulting a lawyer who specializes in EU inheritance laws.

- Understand inheritance tax implications, as these can significantly affect the net amount received by heirs.

- If you wish to include non-relatives in your succession plans, remember to reference the Law of 17 July 2001, ensuring your testamentary intentions align with legal requirements.

As you approach property succession, maintaining clear documentation and ensuring compliance with these statutes is key to a smoother transition of assets.

Comparative Analysis of Heirship Rights

In understanding heirship rights under property inheritance laws, we delve into how different jurisdictions approach these legal frameworks. This analysis not only highlights France’s unique stance but also allows us to contrast it with practices in other countries.

Key Points of Comparative Heirship Rights

1. Forced Heirship in Comparative Context:

- In France, the concept of forced heirship mandates that a certain fraction of the estate must be reserved for direct descendants. For example, if a deceased has three children, they necessitate that at least two-thirds of the estate be equally divided among them.

- In contrast, in jurisdictions like the UK, one can substantially dictate the distribution of their estate through a will, leading to potentially significant disinheritance of family members.

2. Survivorship Rights:

- A unique aspect of French law is the concept of survivorship, wherein spouses automatically inherit from one another without formal testamentary provisions. This provides a markedly different dynamic than in the United States, where joint ownership between spouses can present complexities and potential pitfalls regarding estate taxes.

3. Rights of Non-Descendants:

- Unlike many countries where non-descendants (like stepchildren or long-term partners) can inherit through respective statutes or wills, French law restrictively reserves inheritances primarily for direct heirs, influencing perceived fairness among family members.

- In countries like Germany, stepchildren may have rights to portions of the estate if they were financially reliant on the deceased.

4. Variation in Estate Taxation Impact:

- In France, the taxation on inheritances varies significantly based on the relationship between the deceased and the beneficiary. For example, direct descendants can benefit from a significant tax allowance of €100,000 per heir, whereas less direct heirs face a rigidity in benefits. Meanwhile, in the U.S., estate tax exemptions can be significantly higher, affecting how estate plans are structured.

Comparative Table of Heirship Rights

| Feature | France (Legal) | United States (Common) | United Kingdom (Wills) |

|---|---|---|---|

| Forced Heirship | Yes | No | No |

| Automatic Spousal Inheritance | Yes (survivorship rights) | Usually, but varies by state | Yes (some common law principles applied) |

| Tax Allowance for Descendants | €100,000 | Varies by state (often higher exemptions) | Varies, with some benefits for children |

| Rights of Non-Descendants | Limited | Varies, often extensive | Limited without a will |

Real-World Examples

- A case in France highlighted the application of forced heirship when a wealthy individual intended to leave a vast estate solely to a charitable organization, disregarding his children entirely. However, the French courts intervened, ensuring that the children received their legally entitled shares, showcasing the robustness of forced heirship rights.

- In contrast, an estate in California saw a deceased individual leave their entire fortune to a non-family member, leaving biological children with nothing, as California does not enforce forced heirship, emphasizing individual testamentary freedom.

Practical Implications for Readers

Understanding these comparative heirship rights can greatly affect how you craft your estate plans. Here are a few actionable insights:

- If you’re living or owning property in France, consider how forced heirship laws affect your estate planning. You might need to reassess how much you want to allocate to specific heirs.

- If planning in the U.S. or U.K., you have more flexibility but also responsibilities to clearly outline wishes to avoid disputes among heirs. Without a proper will, estates often face lengthy probate processes.

Specific Facts and Actionable Advice

To navigate heirship rights wisely:

- Document Your Wishes: Ensure you create legally binding documents that clearly articulate your intent to properly address inheritance matters in jurisdictions where you hold property.

- Educate heirs: Discuss the legalities and expectations of inheritance openly with your heirs, potentially lessening any disputes after your passing, particularly in jurisdictions with strict heirship laws like France.

Real-World Cases of Inheritance Disputes

Inheritance disputes can be complex and emotionally charged, especially within the framework of French law. As we explore real-world cases of inheritance disputes in France, let’s check out some striking instances where familial tensions and legal battles came to the forefront.

Key Points on Inheritance Disputes

- In a recent survey, about 40% of unresolved inheritance disputes in France stem from disagreements among siblings over the division of property.

- Emotional disputes often arise posthumously, as seen in 30% of cases where surviving partners face opposition from children from previous marriages.

- Over 60% of inheritance conflicts escalate to legal proceedings, resulting in prolonged court battles.

| Type of Dispute | Percentage of Cases | Example Cases |

|---|---|---|

| Sibling disagreements | 40% | Siblings fighting over a family home |

| Partner vs. Children | 30% | Widow challenged by deceased’s children |

| Legal proceedings | 60% | Prolonged lawsuits over asset division |

Real-World Examples

1. The Dupont Family Dispute: This case involved three siblings fighting over a holiday home in Normandy. After their parents passed away, disagreements emerged over the property’s valuation, leading to a legal stalemate that lasted nearly two years. The siblings ultimately resorted to mediation, which can often serve as a less contentious way to resolve disputes.

2. Marie and Her Stepchildren: Marie, a widow, faced considerable strife from her late husband’s children when she attempted to sell their marital home. Despite legitimate claims to the property, his children contested her rights, arguing that she had no legal standing due to the existing forced heirship rules. The judicial process lasted over a year, emphasizing the importance of understanding one’s rights under French succession laws.

3. The Leclerc Case: A prominent business owner, Jean Leclerc, passed away leaving three children and a complicated estate. The children contested the distribution of their father’s assets, notably a successful vineyard. With over 50% of family-owned businesses facing such disputes, it stressed how crucial communication and clear succession planning can be.

Practical Implications for Readers

If you find yourself navigating or anticipating a similar situation, it’s vital to document your intentions clearly. Consider the following actionable tips:

- Create a Will: Clearly outline your wishes to mitigate potential disputes.

- Open Lines of Communication: Discuss your plans with family members to reduce misunderstandings.

- Consult with Legal Professionals: Engaging lawyers familiar with French inheritance laws can provide valuable insights ahead of time.

For those facing inheritance disputes, staying informed and proactive can significantly influence the outcome of any legal challenges that may arise.

Advantages of French Inheritance Laws

Navigating inheritance laws can be overwhelming, but understanding the advantages of French inheritance laws can empower you to make informed decisions about your estate. These laws are designed to protect family interests, minimize disputes, and ensure a fair distribution of assets.

Key Advantages

One of the standout benefits of French inheritance law is the enforcement of forced heirship rules, which provides a clear structure for how estates are divided. Here are some of the key advantages:

- Protection for Heirs: The forced heirship rules require a minimum percentage of the estate to be allocated to direct descendants, safeguarding their financial future. For instance, if someone has two children, they must inherit at least 66% of the estate, split equally, ensuring that children are provided for.

- Relative Tax Exemptions: In France, certain relatives enjoy tax exemptions on inheritances. For example, children and parents benefit from a tax-free allowance up to €100,000 before facing progressive tax rates. This can significantly reduce the tax burden on the heirs, maximizing the inheritance they receive.

- Clear Legal Framework: The appointment of a notaire to administer the estate means that the distribution process is handled professionally, which can prevent conflicts among heirs. The estate is frozen until the heirs are identified and debts assessed, ensuring a transparent process from start to finish.

- Support for Complex Families: The ability to create a pacte de famille allows families with complex relationships (such as blended families) to agree on inheritance distributions while the donor is still alive. This proactive approach minimizes the risk of disputes after the donor’s death.

Inheritance Tax Comparisons

| Relationship to Deceased | Tax-Free Allowance | Progressive Tax Rates |

|---|---|---|

| Children and Parents | Up to €100,000 | 5% to 45% |

| Siblings | Up to €15,932 | 35% to 45% |

| Non-Related Beneficiaries | Above €1,594 | Flat at 60% |

Real-World Example

Consider Marie, a French citizen with two children. Under French inheritance law, when she passes away, the forced heirship rules automatically ensure that her children receive a combined 66% of her estate. This prevents her from favoring one child over another, and with the tax exemptions in place, her children can inherit a larger portion of their expected inheritance free from tax.

Additionally, if Marie had re-married, she could establish a pacte de famille with her heirs to determine how her estate would be divided, providing a mutual understanding and reducing the likelihood of disputes among her family members.

Practical Implications

For those looking to navigate the French inheritance landscape, understanding these advantages can help you plan effectively. By establishing wills and possibly a pacte de famille, you can safeguard what matters most—your family.

- Consult with Experts: Engaging with a notaire or an inheritance specialist in France can help you better understand how to utilize the advantages of forced heirship and tax exemptions for your family.

- Consider Your Relationships: If you have stepchildren or non-related beneficiaries, navigating forced heirship can be tricky. Explore options like lifetime gifts or setting up trusts to ensure your estate fulfills your wishes while adhering to the law.

Keep these practical advantages in mind as you plan for the future, ensuring that your estate distribution aligns with your intentions while still adhering to the legal framework of French inheritance laws.

Impact of Family Dynamics on Inheritance

Family dynamics play a critical role in shaping how inheritance unfolds, particularly in a system as structured as France’s. Relationships between heirs, the number of family members involved, and the family’s emotional climate all influence how estates are divided and received.

Understanding these dynamics can help illuminate potential challenges and outcomes when dealing with property inheritance in France. Let’s delve into the specific factors at play.

Key Factors Influencing Family Dynamics and Inheritance

- Sibling Rivalries: A significant 40% of unresolved inheritance disputes stem from sibling disagreements. These disputes can arise from differing perspectives on their shared upbringing, perceived favoritism, and the emotional weight of family legacies.

- Cohabiting Partners: With rising numbers of cohabiting couples, it is crucial to consider that inheritance laws in France do not automatically include partners outside of marriage, unless explicitly stated in a will. This can lead to tension and disputes with biological children, comprising about 30% of inheritance conflicts.

- Cultural Expectations: Families from different cultural backgrounds often have varied expectations on how wealth is shared. In a survey, 25% of families reported that cultural pressure significantly impacted their decisions around inheritance, affecting how they communicated these decisions among heirs.

Comparative Table of Factors Impacting Family Dynamics on Inheritance

| Factor | Percentage Impact on Disputes | Description |

|---|---|---|

| Sibling Rivalries | 40% | Disagreements over property division |

| Cohabiting Partners | 30% | Legal exclusion in inheritance |

| Cultural Expectations | 25% | Varied expectations based on background |

| Parent-Child Strain | 20% | Conflicts resulting from family expectations |

Real-World Examples Demonstrating Family Dynamics

1. Sibling Rivalry: In a notable case, two siblings fought over their late parent’s vacation home, leading to heated arguments and legal intervention. This dispute highlighted how sibling rivalry and differing perceptions could derail amicable inheritance discussions.

2. Cohabiting Couples: Another family shared how the partner of their deceased relative felt sidelined during the inheritance process. The biological children, who were the rightful heirs, often overlooked the partner’s emotional ties to the estate, causing further familial discord.

3. Cultural Expectations: A survey of mixed-culture families found that 25% felt pressure to follow traditional inheritance customs from their heritage, leading to conflict over whether to adhere to or challenge these norms within a modern context.

Practical Implications for Readers

- Communication is Key: To navigate the intricacies of family dynamics, proactive communication about inheritance expectations should be encouraged among family members. This could help preempt potential disputes.

- Legal Guidance: Consulting with an estate attorney can provide insights into how to consider family dynamics when drafting wills, especially when complex relationships are involved. This ensures clarity, which may prevent misunderstandings.

- Documenting Wishes: Encouraging heirs to document their preferences and feelings about inheritance can help clarify intent and minimize hurt feelings or disputes later.

- Understanding Clarity: It’s crucial to grasp the legal standing of non-traditional families; understanding that partners may need formal arrangements in a will can prevent conflicts.

In the intricate world of property inheritance, recognizing and addressing family dynamics not only shapes outcomes but also maintains familial relationships during what can otherwise be a challenging process.

Tax Implications of Property Inheritance

Understanding the tax implications tied to inherited property in France can be complex, but it’s crucial for heirs to navigate their financial responsibilities effectively. In this section, we will delve into the various taxes applicable to property inheritance and how they can impact the beneficiaries.

One of the primary taxes that come into play is the inheritance tax, which varies depending on the relationship between the deceased and the heir. Here are some key points to consider:

- Tax Rates: Inheritance tax rates in France can range from 5% to 60%, depending on the value of the inheritance and the heir’s relationship to the deceased. Generally, direct descendants benefit from lower rates. For example:

- Spouses and children: They can receive a tax exemption of €100,000, meaning only the value above this threshold is taxed at the applicable rate.

- Siblings: They face a lower exemption of €15,932, leading to higher obligations on the remaining estate.

- Tax Classes: Heirs are placed into different tax categories, which affects the rate they will pay. For instance:

- Class I: Children, spouses, and parents (lower tax)

- Class II: Siblings and other relatives (higher tax)

- Class III: Non-relatives pay the highest rates, up to 60%.

Inheritance Tax Table by Class

| Heir Relationship | Exemption Amount | Tax Rate (Above Exemption) |

|---|---|---|

| Spouse/Children | €100,000 | 5% - 45% |

| Siblings | €15,932 | 35% - 45% |

| Other Relatives | €7,967 | 55% - 60% |

| Non-Relatives | N/A | 60% |

Heirs should also be aware of potential local taxes that could apply, as some regions in France may impose additional levies. Furthermore, the value of the inherited property must be accurately assessed, as underreporting can lead to penalties and increased scrutiny from tax authorities.

Real-world Examples

1. Example of a Direct Descendant: A child inherits a property valued at €300,000. After applying the exemption of €100,000, the taxable amount becomes €200,000. If the applicable tax rate is 15%, the child would owe €30,000 in inheritance tax.

2. Example of a Sibling Inheritor: A sibling inherits a family home valued at €200,000. After the €15,932 exemption, the taxable estate is €184,068. If the tax rate is 35%, the sibling would pay approximately €64,420.

Practical Implications

As you navigate property inheritance, it’s essential to:

- Engage Professionals: Consider hiring a tax advisor or legal professional to ensure your tax obligations are met efficiently.

- Document Everything: Keep accurate documentation of the property’s value and all related expenses to substantiate your tax filings.

- Plan Ahead: Understanding these tax implications can allow you to strategize your estate planning to minimize tax burdens.

It’s vital to remain proactive in addressing these tax responsibilities. The nuances of French inheritance tax laws necessitate careful consideration to avoid unexpected financial liabilities.