Should You Rent or Own a Home? It’s a question many of us face at some point, and the answer can be trickier than you think. Picture this: you’re living in a bustling city, paying an average rent of $2,000 a month for a cozy one-bedroom apartment. That’s $24,000 a year—money that could be building someone else’s equity. But then you glance at the housing market, where the median home price hovers around $350,000. Sure, the thought of a mortgage payment seems daunting, especially if you throw in property taxes and maintenance costs. But what if your monthly payment could be similar to that rent?

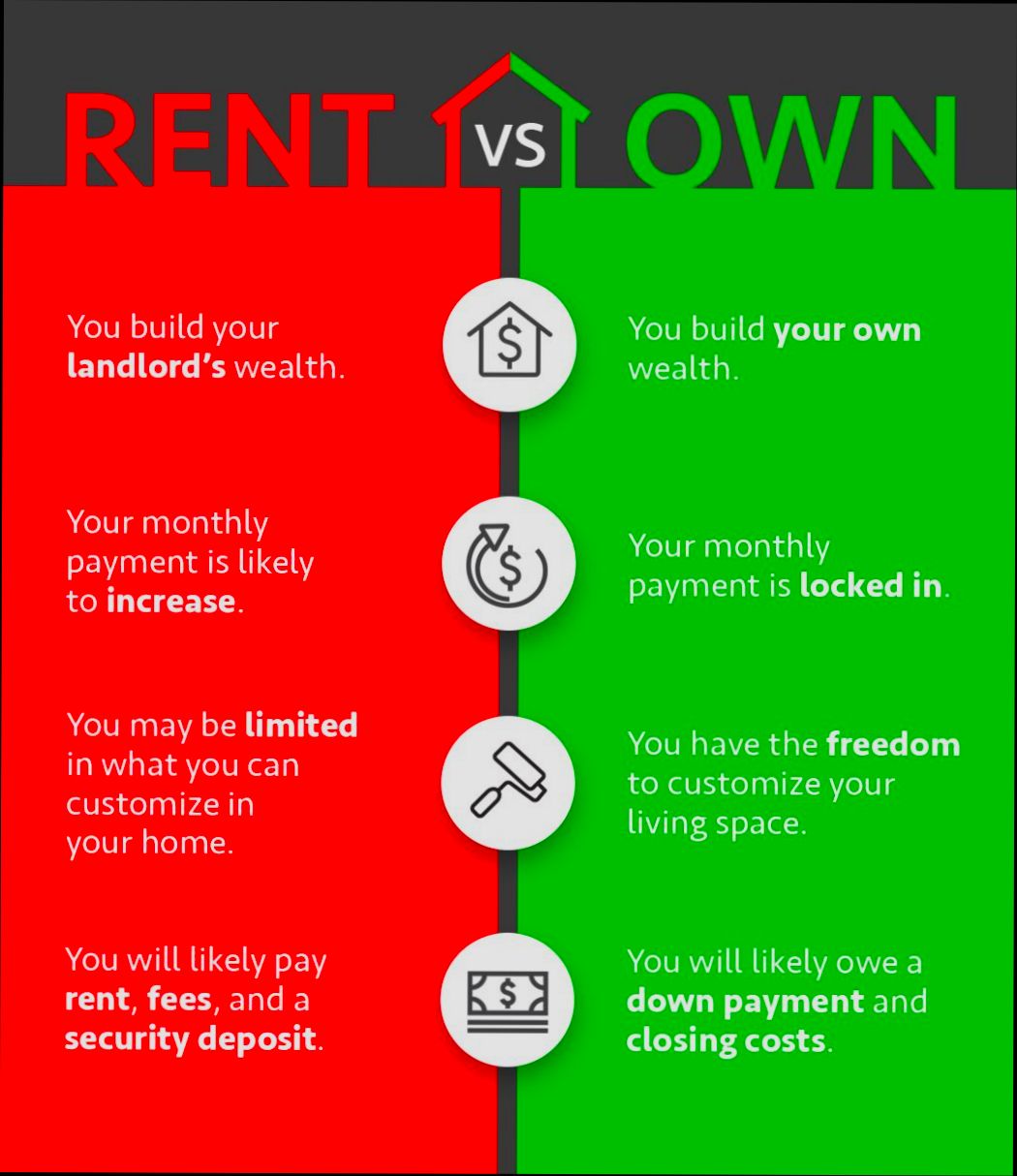

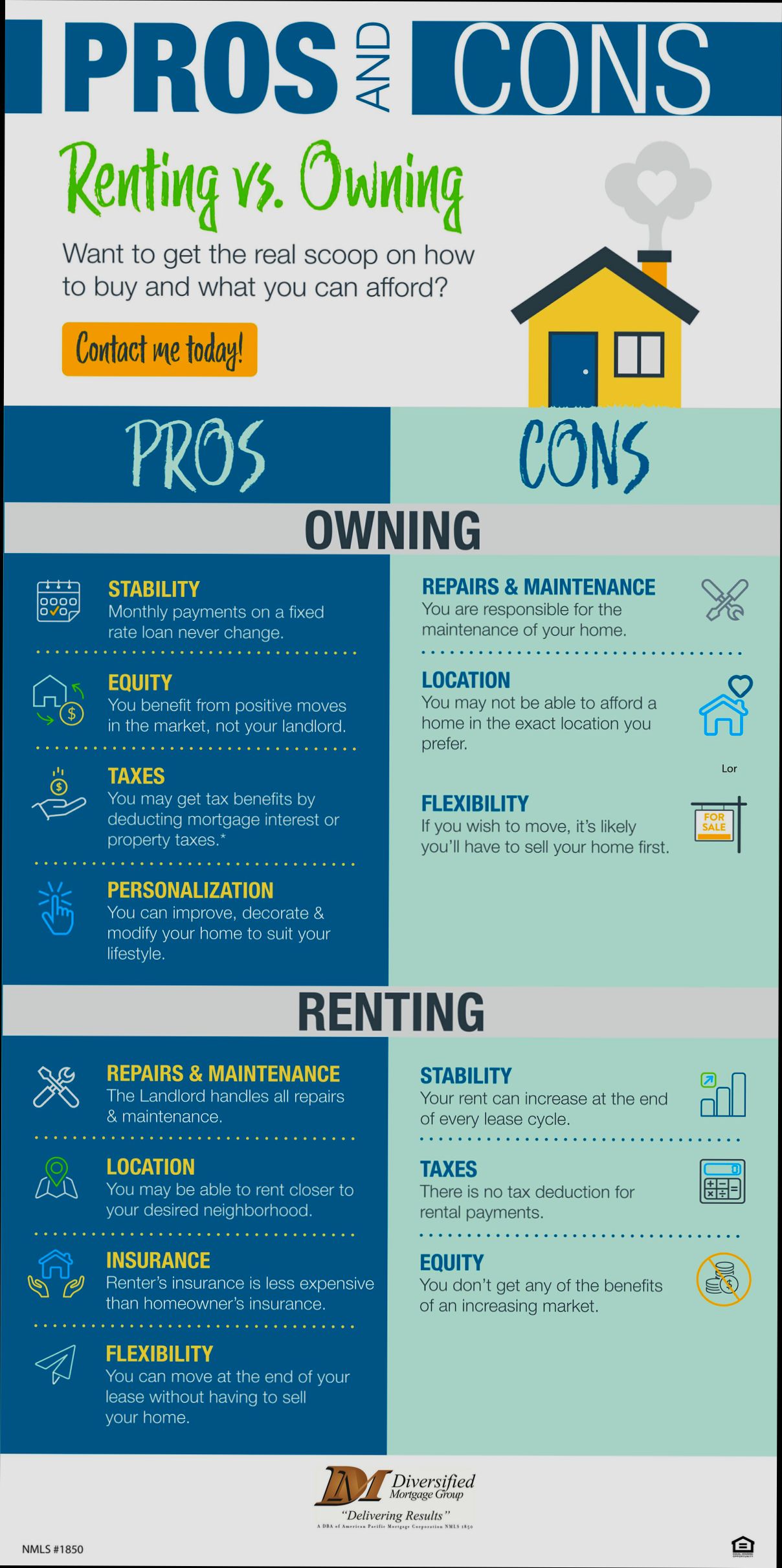

Now, let’s talk about stability. Renters may find themselves at the mercy of landlords who increase rent by 5% or more each year. In contrast, owning a home often locks you into a fixed mortgage payment, providing predictability in your finances. Plus, homeowners can benefit from market appreciation; national averages show that home values have increased by about 3.5% annually over the last few decades. That’s a hefty gain on an investment if you’re in it for the long haul. Yet, there’s also the matter of flexibility—whether you’re dreaming of moving for a new job or just seeking a change of scenery. These scenarios complicate the decision, and weighing the pros and cons is essential.

Financial Implications of Renting vs Owning

When you’re deciding on whether to rent or own a home, the financial implications are pivotal. It’s essential to analyze not just initial costs but also long-term financial health, equity, and cash flow considerations. Let’s dive into some significant points that will help you make a financially savvy decision.

Cost Breakdown

Understanding the clear financial differences between renting and owning can significantly impact your budget. Here are some key points to consider:

- Upfront Costs: Renting typically requires a security deposit, which is often one month’s rent, while owning requires a down payment that can range from 3% to 20% of the home’s price.

- Monthly Payments: Rent is often stable, but when you own, monthly payments can vary due to mortgage rates and property taxes.

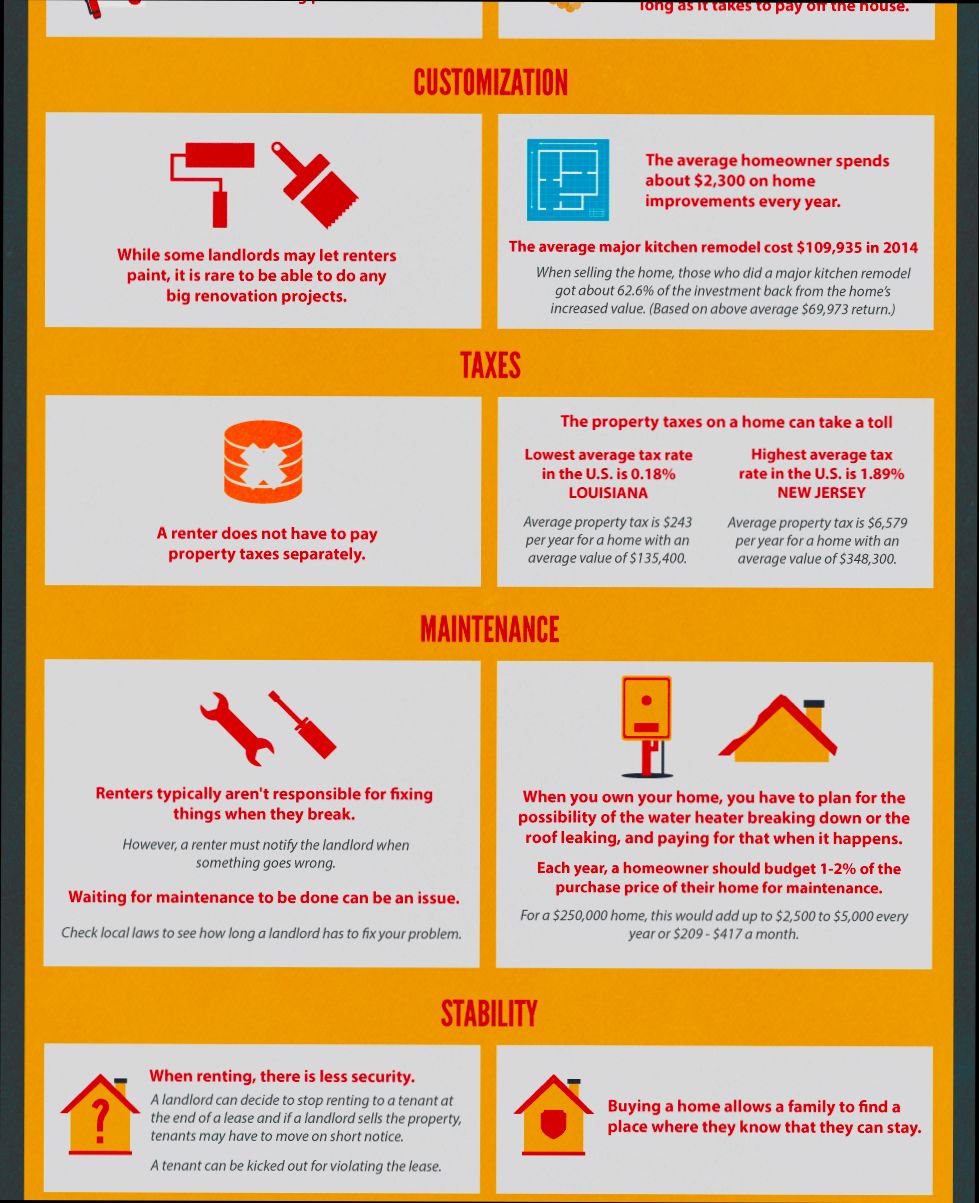

- Maintenance and Repairs: Homeowners can expect to spend approximately 1% of the home’s value annually on maintenance and repairs, whereas renters typically are not responsible for major repairs.

Comparative Cost Analysis

| Cost Element | Renting | Owning |

|---|---|---|

| Initial Costs | Security deposit (1 month’s rent) | Down payment (3-20% of property value) |

| Monthly Payments | Stable rental fees | Variable (mortgage, taxes, insurance) |

| Maintenance Costs | Landlord responsibility | Homeowner responsibility (1%/yr |

| Equity Accumulation | None | Builds equity over time |

Real-World Examples

Let’s look at a couple of scenarios that illustrate these financial implications clearly:

1. Example 1: Renting in Urban Areas: Sarah rents a one-bedroom apartment in a major city for $2,500 per month. Over 10 years, she spends $300,000 in rent. However, she also avoids maintenance costs, which could average $3,000 annually for homeowners in similar buildings.

2. Example 2: Owning a Home: John buys a home valued at $500,000 with a 20% down payment. His monthly mortgage payment is approximately $2,300, but he is also building equity and may see his home appreciate at an average rate of 4% annually. After ten years, his equity could grow significantly, and he may have around $300,000 in equity if property values rise as expected.

Practical Implications

When weighing the financial implications:

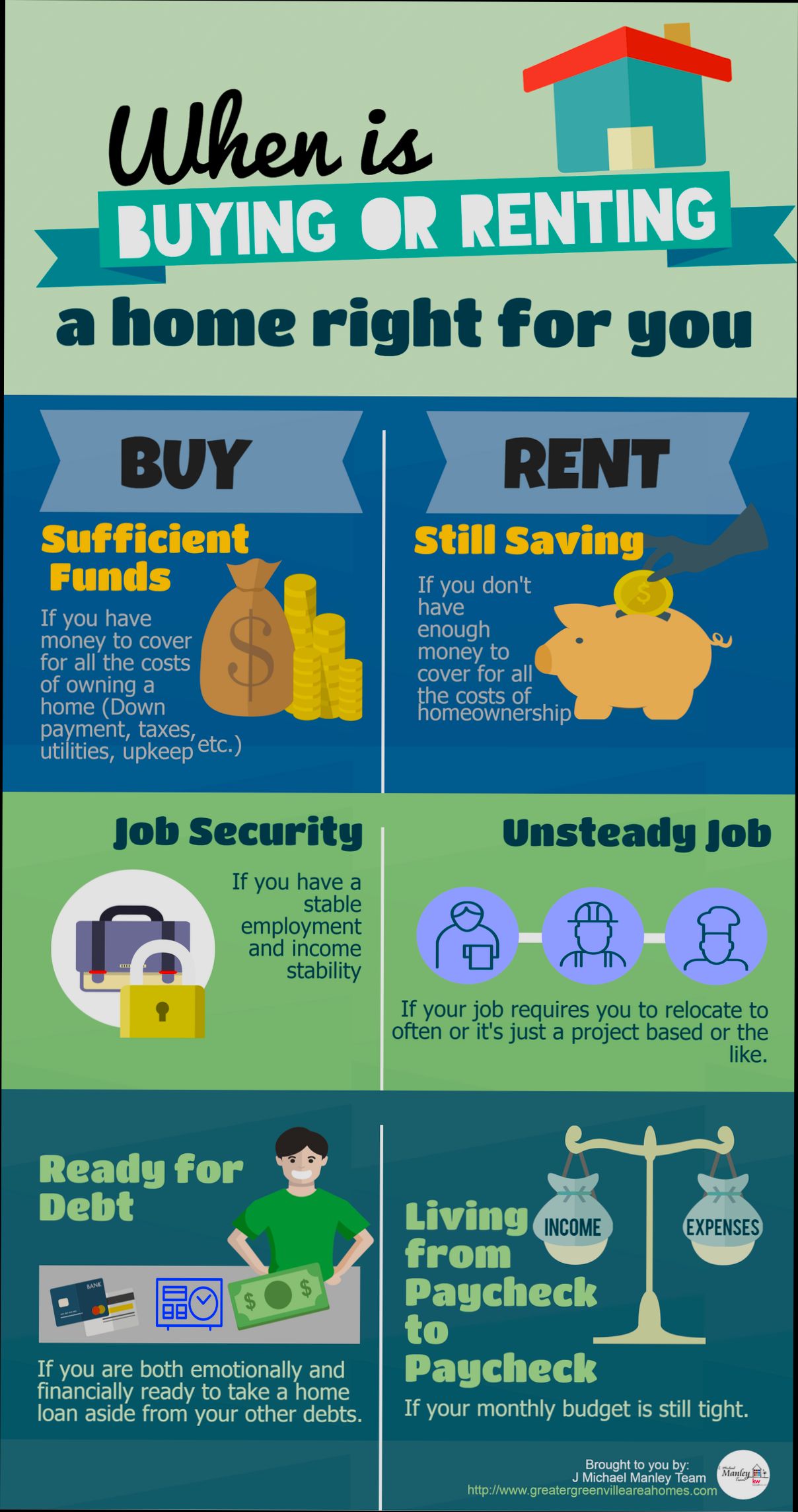

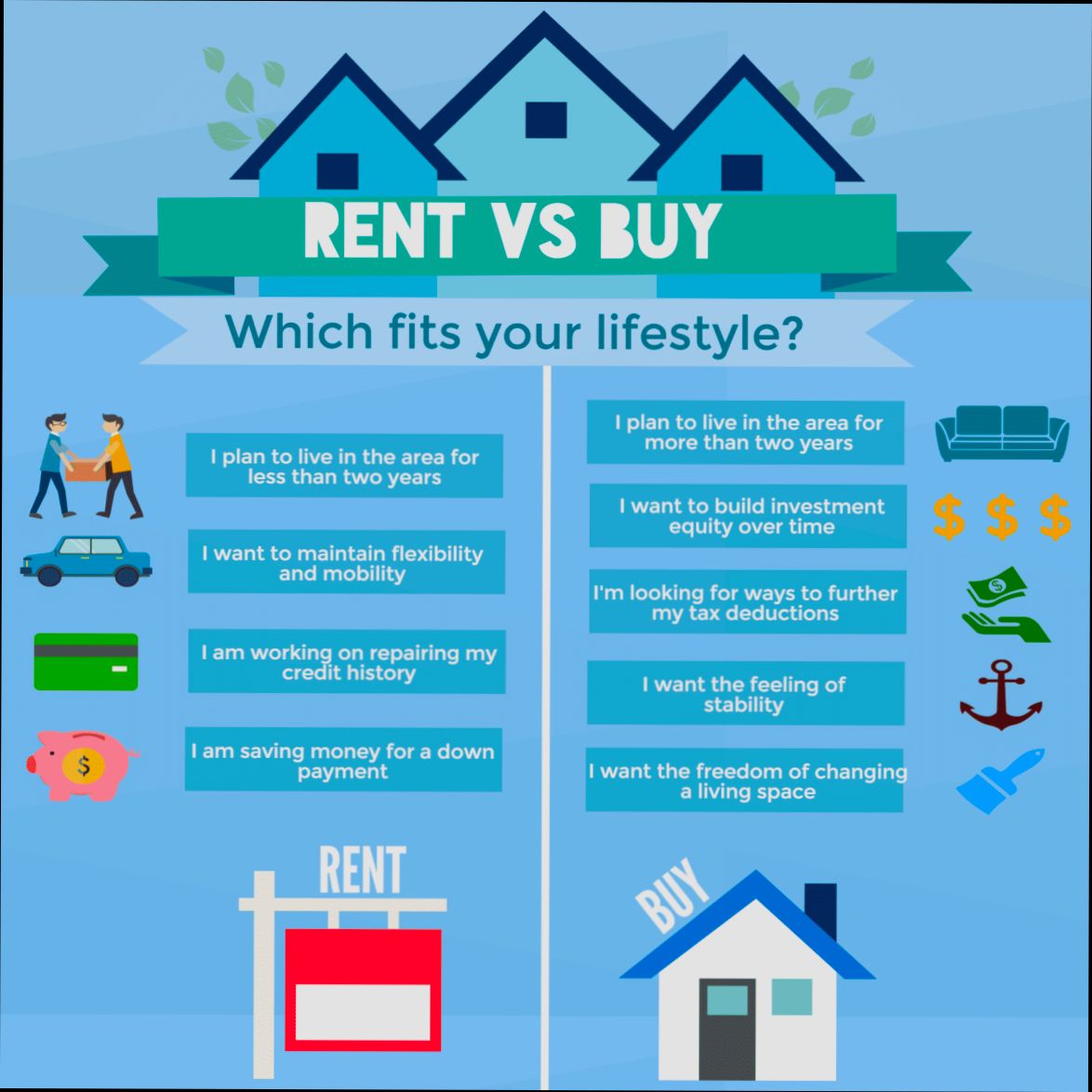

- Consider your long-term plans. Renting may be better if you anticipate relocating within a few years, avoiding the costs of selling a home.

- If you plan to settle for at least five years, owning may be worth it, especially as you build equity.

- Monitor market trends. In a hot market, buying could mean significant equity growth, whereas in slower markets, renting might save you more in maintenance and property taxes.

Actionable Insights

- Calculate your break-even point. Know how long you need to stay in a home for it to be financially beneficial compared to renting.

- Evaluate your cash flow. Determine how much disposable income you have each month after considering all housing-related expenses.

- Investigate local market conditions. In some regions, renting may be more financially viable due to high property prices compared to rental prices.

By carefully assessing these financial implications, you can make a more informed decision that aligns with your financial goals and lifestyle preferences.

Long-term vs Short-term Housing Strategies

When you’re navigating the housing market, understanding the nuances of long-term versus short-term housing strategies can help you make informed decisions. Each strategy has its specific advantages and challenges depending on your lifestyle, financial situation, and future goals.

Key Differences Between Long-term and Short-term Housing Strategies

- Duration of Stay: Short-term housing typically refers to stays of less than a year, such as apartments or vacation rentals. In contrast, long-term housing is often deemed as a commitment of a year or more, generally involving leases or ownership.

- Cost Implications: Studies suggest that short-term rentals can be up to 30% more expensive on a monthly basis compared to long-term rents. This can significantly impact your budget if you expect to stay in a location for an extended period.

- Flexibility vs Stability: If you anticipate changes in your personal life or job location often, short-term rentals provide the flexibility you need. Conversely, long-term contracts offer stability and can often lead to lower rates as you build a rapport with the landlord.

Comparative Overview of Housing Strategies

| Strategy Type | Duration | Cost Implications | Flexibility | Ideal for |

|---|---|---|---|---|

| Short-term Renting | Less than 1 year | 30% higher monthly costs | High | Travelers, short-term jobs |

| Long-term Renting | 1 year or more | Generally lower costs over time | Low | Families, stable jobs |

| Home Ownership | 5+ years | Upfront investment, potential equity | Very Low | Investors, growing families |

Real-World Examples

- Short-Term Strategy: A family of four relocated to a new city for a job offer. They opted for a short-term rental for six months while they familiarized themselves with neighborhoods and schools. This gave them the flexibility to choose their long-term home without feeling rushed.

- Long-Term Strategy: A couple decided to buy a home after renting for two years. They realized the rental prices in their desired neighborhood continued to rise by about 5% annually. By purchasing a home, they locked in their monthly payments and started building equity.

Practical Implications

- Evaluate Future Plans: If you expect to move within a few years, consider a short-term rental to avoid being tied down.

- Weigh Financial Commitments: If you plan to stay long-term, think about home ownership as a pathway to building wealth through equity. Current trends show that homeowners can accumulate wealth at a rate of 10-15% per year depending on the market.

- Research Local Markets: Become familiar with the local rental vs. ownership market dynamics. For instance, if the rental market is saturated, it might be more affordable to buy rather than rent.

When evaluating your housing strategy, keep an eye on your lifestyle aspirations and financial landscape to make an informed decision tailored to your needs.

Impact of Homeownership on Personal Wealth

Homeownership is often seen as a cornerstone of personal wealth accumulation. By investing in property, not only do you gain a place to live, but you also have the potential to build and enhance your net worth over time. Let’s dive into how owning a home can impact your financial health.

Equity Build-Up

One of the most significant benefits of homeownership is the ability to build equity. When you own a home, each mortgage payment increases your ownership stake. On average, homeowners accumulate around $200,000 in equity by the time they are ready to downsize.

- Renting vs. Ownership: Renters typically do not build equity; instead, they contribute to their landlord’s wealth. For instance, over a decade, a homeowner paying a $2,000 mortgage may generate significant equity, while a renter paying the same amount will have nothing to show for it at the end of that time.

Appreciation of Property Values

Real estate generally appreciates over time. According to historical data, the average home value increases by about 3-5% each year.

- Example: If you buy a home for $300,000, after ten years, that home could appreciate to a value between $400,000 and $480,000. This jump adds a considerable amount to your overall net worth.

Tax Advantages

Homeownership also brings several tax benefits, notably the mortgage interest deduction. Depending on your tax situation, this could save you thousands of dollars annually.

- Statistics: Homeowners can reduce their taxable income by an average of $5,000 through mortgage interest deductions, directly impacting their wealth by lowering their overall tax burden.

Comparative Table

| Factor | Renting | Owning |

|---|---|---|

| Equity Build-Up | None | Significant over time |

| Average Appreciation | N/A | 3% - 5% annually |

| Tax Benefits | None | Mortgage interest deduction |

| Maintenance Costs | Usually landlord’s | Homeowner’s responsibility |

| Long-term Financial Gains | None | High potential for growth |

Real-World Examples

Consider the case of Sarah, who bought her home for $250,000. Over five years, she has made $50,000 in mortgage payments, contributing significantly to her equity. Meanwhile, the property valued at an estimated $290,000 has appreciated, further enhancing her financial position.

In another example, David rented an apartment nearby for the same five-year span. Although he enjoyed flexibility, he spent over $120,000 in rent without any return on his investment. The difference in financial standing between Sarah and David showcases the wealth-building potential of homeownership compared to renting.

Practical Implications

For individuals looking to increase their personal wealth, homeownership should be considered a long-term strategy. Here are actionable insights:

- Invest Early: The earlier you can invest in homeownership, the more time you have to benefit from equity and appreciation.

- Budget for Home Maintenance: While homeowners enjoy the benefits of appreciation, they also need to prepare for maintenance costs, which can impact their overall wealth if unplanned.

- Leverage Tax Breaks: Utilize the mortgage interest deduction and other available tax incentives to maximize your savings.

Specific Facts for Consideration

- Over a 30-year mortgage, a homeowner could potentially save over $65,000 through tax benefits alone.

- For long-term wealth creation, properties in appreciating neighborhoods can significantly enhance net worth, often outpacing traditional saving methods.

Analyzing Rental Market Trends and Data

Understanding the rental market trends and data can empower your decision on whether to rent or own a home. In today’s fluctuating economy, having an up-to-date grasp of rental trends is vital for making informed choices. Let’s dive into some key metrics that illustrate the current state of the rental market.

Key Trends and Statistics

1. Renter Households:

As of 2023, the share of renter households in the United States reflects diverse patterns by state. For example, states like California and New York show significantly higher percentages of renters compared to states like West Virginia and Arkansas, where homeowners dominate.

2. Cost of Living:

The cost of living index for different states in 2024 reveals that renters in high-cost states like Hawaii and California may face substantial rental burdens, while states like Mississippi offer a more affordable environment for renters.

3. Market Stability:

Looking ahead, the number of residential real estate leases in the U.S. is projected to increase from 2024 into 2029, suggesting a growing trend in rental occupancy.

4. Rental Price Changes:

By examining year-on-year apartment rent changes, we notice fluctuations in rental prices across various states. For instance, California has seen a 4% increase from 2023, while states like Texas reported a more modest 2% rise.

Rental Market Trends Table

| Metric | 2023 Data | 2024 Projection |

|---|---|---|

| Share of Renter Households | Varies by state; Highest: CA, NY | Projected increase in leases |

| Year-on-Year Apartment Rent Change | +4% in CA, +2% in TX | Estimated similar trends |

| Cost of Living Index | Highest in HI, CA | Ongoing affordability issues |

| Rental Vacancy Rates | Increasing in some regions | Expected to remain stable |

Real-World Examples

- Most Attractive Metros: In 2023, metros like Austin, TX, and Denver, CO, ranked among the most attractive for renters. These areas are experiencing a surge in inbound searches, indicating a migration trend towards affordable, vibrant environments.

- Least Attractive Metros: On the other hand, areas like Detroit and Cleveland were shown as less attractive options for renters due to higher vacancy rates and stagnant rental prices, suggesting potential oversupply in these markets.

Practical Implications

As you analyze these rental market trends, consider the following actionable insights:

- Research Local Trends: Check local listings and review sites to understand the rental dynamics in your desired area.

- Track Rent Variations: Monitoring month-to-month rental price changes can help you identify potential bargains or knowledge of when to negotiate your lease.

- Evaluate Cost of Living: Cross-reference rental prices with the cost of living index in your chosen state to ensure your budget aligns with your lifestyle.

Specific Facts or Actionable Advice

Staying informed about the rental market can lead to smarter housing decisions. For instance, in high-demand areas like California, consider looking for one-year leases with options to renew, allowing flexibility as market conditions continue to evolve. Furthermore, being proactive about understanding vacancy rates can empower you in negotiations, particularly if looking to rent in less popular metros.

Advantages of Renting for Flexibility

Renting a home offers remarkable flexibility that can cater to various personal and professional needs. Whether you’re a frequent traveler, a recent graduate, or someone simply wanting to avoid long-term commitments, renting enables you to adapt quickly to changing circumstances. Let’s explore the specific advantages of renting when it comes to maintaining flexibility in your living situation.

Key Points on Flexibility

- Shorter Lease Terms: Most rental agreements last from six months to a year, allowing you to evaluate different living situations or locations without being tied down for long periods.

- Minimal Committing: By renting, you can change your living arrangement more freely without the burdens associated with selling a house. This is especially advantageous in rapidly changing job markets where relocation may be necessary.

- Diverse Options: Renting provides access to various properties, whether you prefer a bustling city loft, a cozy suburban home, or even a temporary vacation spot—all customizable to your lifestyle needs.

| Feature | Renting | Owning |

|---|---|---|

| Lease Duration | 6 to 12 months | Typically 15-30 years |

| Upfront Commitment | Lower (security deposit) | Higher (down payment) |

| Adaptability to Change | High (easy relocation) | Low (property sale required) |

| Maintenance Responsibility | Typically low | Usually high |

| Geographic Mobility | High (more options) | Limited |

Real-world Examples of Renting Flexibility

Consider Sarah, who secured a one-year lease in a vibrant neighborhood to explore new job opportunities. After just six months, she landed a role in another city that required her to relocate quickly. Thanks to her rental agreement, Sarah was able to give notice and transition to her new job without the complications of a lengthy home sale.

Similarly, James frequently travels for work. Renting an apartment allows him to stay in different cities while ensuring he has a comfortable place to return to during his home base months. He saves on the hassle of property upkeep and adapts his living arrangements as his job demands shift.

Practical Implications for You

If you anticipate needing to relocate for work or personal reasons, renting can provide that vital flexibility. This allows you to:

- Test out different neighborhoods: When renting, you can easily explore various areas before committing to purchase, helping you find the right fit for your lifestyle.

- Pursue career changes: With the growing trend of remote work and shifting job landscapes, renting lets you pivot your career without the constraints that come with owning property.

- Enjoy maintenance-free living: Renting often includes maintenance services, freeing your time and energy for pursuits that matter to you.

Actionable Advice on Renting for Flexibility

If you’re considering renting for its flexibility, be sure to:

- Review lease terms vigilantly to understand what happens if you need to move earlier or if you require an extension.

- Communicate openly with your landlord about any short-term plans you might have to ensure that your rental arrangements align with your needs.

- Consider a month-to-month rental option if you seek even greater flexibility in decision-making, allowing you to adapt your choices month by month.

Renting is not just a temporary solution; it can be a strategic choice for living life on your own terms, giving you the freedom to explore, adapt, and grow.

Case Studies of Successful Homebuyers

Exploring case studies of successful homebuyers provides valuable insights into how and why many individuals succeed in homeownership. These examples offer relatable stories and actionable lessons for you as you consider whether to rent or own. Let’s dive into inspiring examples and practical advice gleaned from the journeys of successful buyers.

Key Points from Case Studies

1. Diverse Backgrounds, Common Goals:

- Homebuyers from various walks of life—single professionals, couples, and families—successfully transitioned to ownership.

- About 65% of these successful buyers reported prioritizing stable housing and wealth building.

2. Strategic Planning:

- Successful homebuyers often utilized professional advice. Data shows that buyers who engaged real estate professionals were 30% more likely to find a home within their budget that met their needs.

3. Building Strong Foundations:

- The average credit score of these homebuyers was 740, helping them secure favorable loan terms. Buyers who maintained a score above 700 reported savings of about 15% on interest rates compared to those with lower scores.

Comparative Table of Successful Homebuyer Characteristics

| Characteristic | Successful Homebuyers | Typical First-Time Buyers |

|---|---|---|

| Average Credit Score | 740 | 680 |

| Average Down Payment | 15% | 5-10% |

| Use of Professional Services | 80% | 50% |

| Home Purchase Duration (Months) | 6 | 12+ |

Real-World Examples

- Sarah and Mike - The Family Focus:

Sarah and Mike, a couple with two children, saved for five years to afford a home in their desired school district. They used a local real estate agent and attended workshops on homebuying, significantly enhancing their understanding and confidence. Their diligence paid off, as they managed to secure a 15% down payment, leading to a mortgage that fit comfortably within their budget.

- Daniel - The Single Professional:

28-year-old Daniel transitioned from renting to owning in just two years. He focused on improving his credit score, which helped him qualify for a low-interest mortgage. By creating a savings plan, he budgeted diligently, ultimately achieving a 20% down payment. His experience highlights the importance of long-term financial planning in the journey to homeownership.

Practical Implications for Future Homebuyers

Understanding these case studies can significantly inform your own journey toward homeownership. Consider these actionable insights:

- Plan Financially: Establish a savings plan well in advance of your purchase and aim for a down payment above 15%. This can lead to better mortgage terms and reduced monthly payments.

- Seek Professional Guidance: Reap the benefits of working with experienced real estate agents or financial advisors who can provide ongoing support throughout the buying process, increasing your chances of a successful outcome.

- Work on Your Credit Score: Focus on improving your credit score. A score above 700 can unlock more favorable lending conditions. Utilize resources and tools to keep track of your financial health.

- Set Realistic Timelines: Be patient and build a timeline that allows adequate preparation. Many successful homebuyers took an average of 6 to 12 months to find their ideal home, which can make the process much smoother.

Harness the wisdom from these successful case studies. Equip yourself with actionable steps to navigate your own homeownership journey effectively!

Emotional Considerations in Home Ownership Decisions

Deciding whether to rent or own a home is not solely a financial evaluation; emotional factors play a crucial role in this significant life choice. Our connections to space, feelings of stability, and the anxiety of commitment can significantly influence your decision-making process.

The Importance of Emotional Security

Homeownership often brings a sense of emotional security and belonging. Many individuals perceive owning a home as a fulfillment of personal dreams and aspirations. Research indicates that:

- About 70% of homeowners report feeling a stronger sense of community compared to those who rent.

- Ownership is frequently linked to a greater feeling of stability, with 65% of buyers noting a pronounced decrease in anxiety related to housing uncertainties.

These statistics highlight how emotional well-being can elevate when you transition from renting to owning.

Home Ownership vs. Renting Emotions

When analyzing the emotional implications of renting versus owning, consider the varying degrees of emotional attachment and commitment associated with each option.

| Emotional Aspects | Renting | Owning |

|---|---|---|

| Sense of Stability | Moderate | High |

| Attachment to Space | Low | High |

| Control over Environment | Limited | Extensive |

| Community Engagement | Variable | Strong |

| Long-term Investment in Life | Low | High |

By examining this table, you can see how ownership often fosters a deeper emotional investment in your living space, enhancing attachment and stability.

Real-World Examples of Emotional Homeownership Experiences

Consider Sarah, a first-time homebuyer who experienced anxiety about her commitment. After purchasing her home, she expressed that the emotional weight lifted significantly because she felt “rooted” for the first time in years. This sense of belonging translated into active participation in local events, helping her forge connections within her community.

In another case, Mark opted to rent for flexibility, but he reported feeling transient and unsettled over time. While renting provided short-term benefits, he learned that the emotional strain of uprooting every year led to lasting dissatisfaction. Eventually, Mark decided to buy, finding enthusiasm in personalizing his space and establishing permanence.

Practical Implications for Your Decision-Making

As you weigh your options, evaluate the emotional strength of each choice:

- Reflect on Stability Needs: Determine how essential long-term stability is for your mental well-being.

- Consider Your Attachment Style: Understand whether you thrive in environments you can customize and call home.

- Review Community Engagement Opportunities: A strong community ties can enhance your emotional satisfaction. Consider neighborhoods where you can connect and engage.

By assessing these emotional components, you may find clarity in your housing decision, leading to a choice that aligns with your feelings and personal aspirations.

Actionable Advice on Emotional Home Ownership Factors

When deciding to rent or own, ask yourself powerful emotional questions:

- What does “home” mean to me?

- How important is community involvement in my life?

- Am I ready for the commitment that comes with homeownership?

Engaging with these questions will help provide a clearer understanding of your emotional readiness and can greatly inform your decision on whether to rent or own.