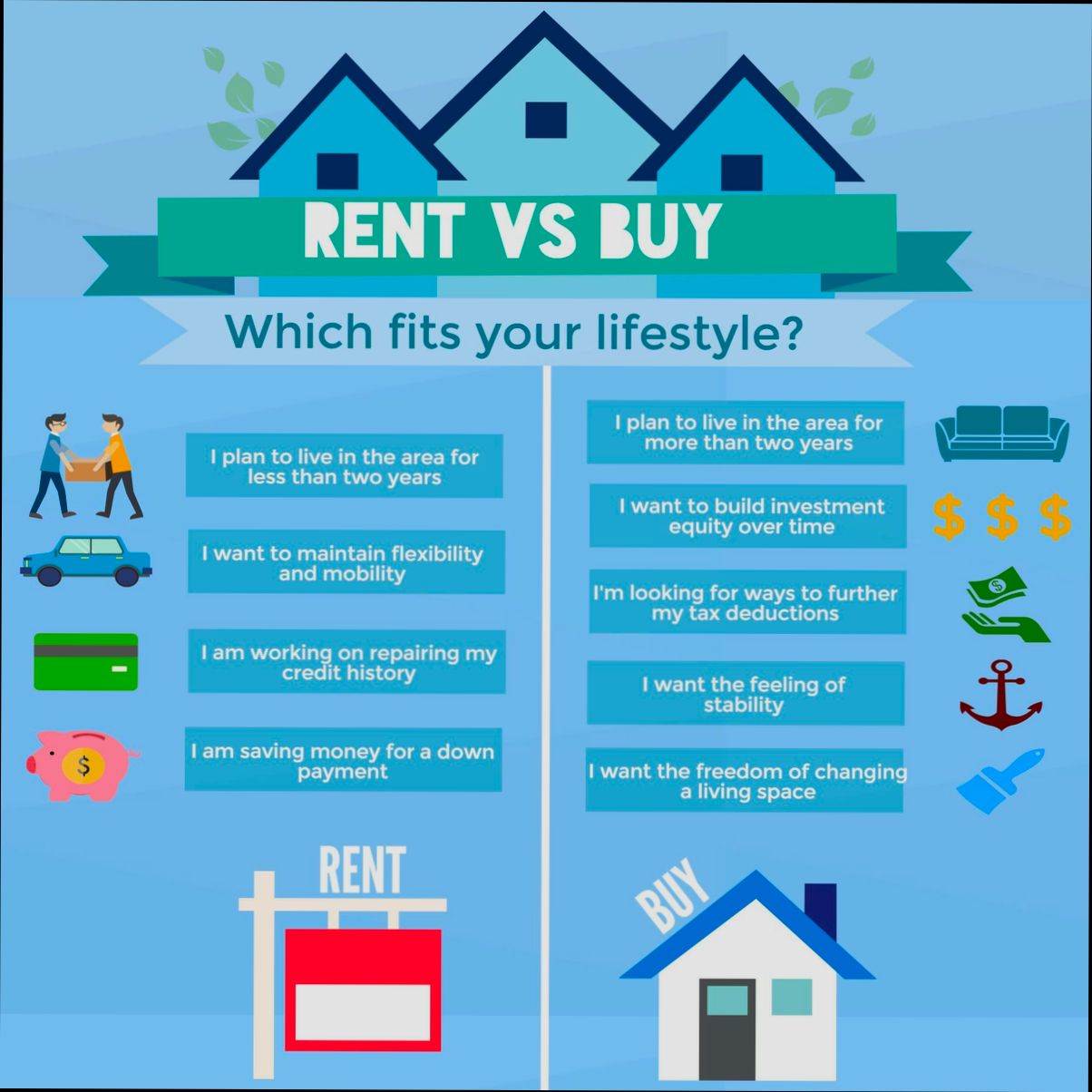

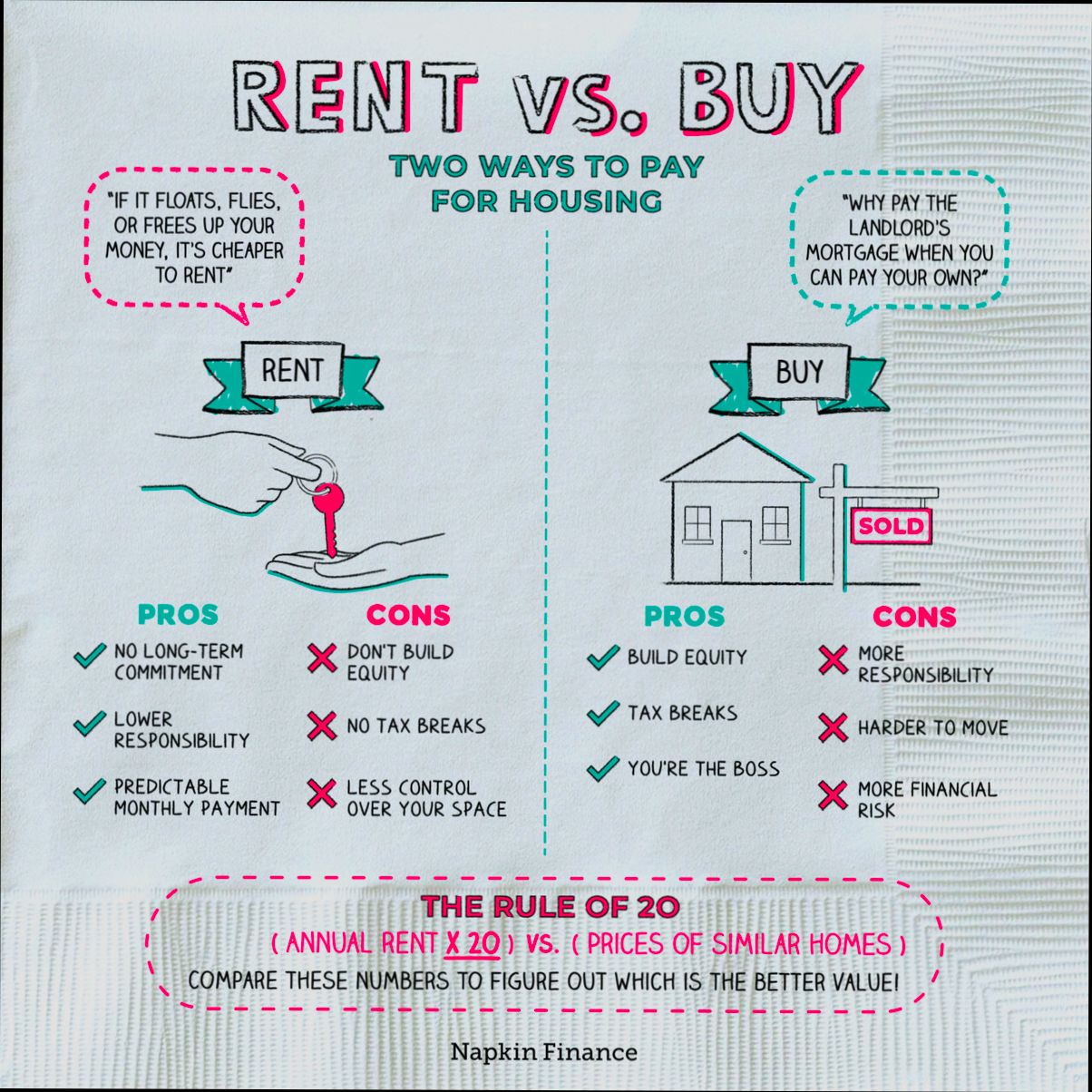

Renting vs Buying: What is Better? It’s a question that’s on the minds of many, especially first-time homebuyers or those looking to switch up their living situation. Let’s break it down with some real-world numbers. Did you know that the average rent in the U.S. hit around $1,200 per month in 2023? That’s a hefty sum to shell out each month. On the flip side, the median home price has soared to about $400,000, with mortgage rates hovering around 7%. For many, that initial down payment can feel daunting; but owning means you’re investing in something that could appreciate over time.

Now, let’s dive into real scenarios. Imagine a couple living in a trendy part of town, paying that monthly rent while dreaming of buying a cozy place of their own. If they continue renting for five years, they’ll end up tossing around $72,000 into the landlord’s pocket. Conversely, if they take the plunge and buy, they could potentially build equity as home values rise. But what if the market fluctuates, or they need to move for work? The financial implications can be both exciting and terrifying. With these dynamic options on the table, it’s crucial to weigh the numbers carefully and understand what really fits your life.

Financial Implications of Renting vs Buying

When considering whether to rent or buy a home, financial implications play a pivotal role in your decision-making process. Let’s dive into the costs, savings, and potential financial benefits and pitfalls associated with each option.

Key Financial Considerations

1. Upfront Costs

Buying a home typically requires significant upfront costs, including a down payment, closing costs, and home inspections. The average down payment can range from 3% to 20% of the home’s purchase price. For example, on a $300,000 home, a 20% down payment would amount to $60,000. In contrast, renting usually only requires the first month’s rent and a security deposit, which can average around $2,000 in many metropolitan areas.

2. Monthly Expenses

Homeowners are responsible for mortgage payments, property taxes, homeowner’s insurance, and maintenance costs, which can total over 30% of their monthly budget. Research indicates that, on average, homeowners pay about 25% more in monthly expenses compared to renters due to these additional costs. Renters often have the advantage of fewer unexpected expenses since property maintenance is generally covered by landlords.

3. Long-term Investment Potential

Owning a home can be a significant long-term investment. Historical data shows that home values appreciate an average of 3% annually. If you buy a home worth $300,000, in 10 years, it could appreciate to around $400,000, providing you with a paper gain of $100,000. However, this potential gain must be weighed against market fluctuations and the associated holding costs during ownership.

| Financial Aspect | Renting | Buying |

|---|---|---|

| Upfront Costs | Low (1st month + deposit) | High (3%-20% down payment) |

| Average Monthly Payment | $2,000 | $2,600 (including taxes) |

| Property Value Appreciation | N/A | 3% annual increase |

| Maintenance Responsibility | Landlord | Homeowner |

| Equity Building | None | Increasing with payments |

Real-World Examples

Example 1: Renting in an Urban Area

Consider a young professional who rents a one-bedroom apartment in San Francisco for $3,500/month. In one year, they pay $42,000 in rent. If they were to buy a modest condo at $700,000 with a 20% down payment, their initial cash outlay would be $140,000, and their monthly mortgage payment could exceed $3,200. This illustrates the high entry cost of homeownership versus an annualized rental expense.

Example 2: Buying in a Growing Suburb

On the other hand, let’s look at a family purchasing a home in a growing suburb for $400,000 with a 3% down payment. Their initial investment is $12,000, but monthly commitments rise as they bear costs like property taxes and maintenance, totaling approximately $2,800 monthly. If the area appreciates as projected, they could see a return on their investment that justifies the initial costs over time.

Practical Implications

- Evaluate your financial situation: Understand your cash flow and how much you can afford without compromising your lifestyle. Be honest about whether you can handle the extra expenses that come with homeownership.

- Consider market trends: Research the housing market trends in your area. If properties are expected to appreciate, buying could be a financially advantageous move.

- Account for opportunity costs: When you decide to buy, consider what you are giving up financially. Your investment in home equity could potentially be used in other areas, such as retirement accounts or other investments.

Specific Facts for Consideration

- Home equity: Interest payments on a mortgage can allow homeowners to build equity over time. For example, in the first five years of a 30-year mortgage, you might have paid around $70,000 in interest while only accumulating a fraction of equity, highlighting how financial growth may take time.

- Tax benefits: Homeowners can deduct mortgage interest on their taxes, providing an average savings of about $1,000 per year depending on income level, which is a financial perk that renters don’t receive.

- Monthly payment stability: Renting often comes with the risk of increased rent prices, while fixed-rate mortgages offer predictable monthly payments for the life of the loan, which can safeguard against inflation.

Comparative Analysis of Long-Term Investments

When it comes to the long-term investment potential of renting versus buying a home, there are critical factors that can shape your financial future. Understanding how each option stacks up as a long-term investment will help you make informed decisions that best suit your lifestyle and financial goals.

Key Points of Comparison

- Market Appreciation: Historically, homeowners have seen property values appreciate at about 4% annually. In contrast, rental prices often fluctuate based on market conditions without offering an inherent value increase. Over a 30-year period, this difference can amount to tens or even hundreds of thousands of dollars.

- Equity Build-up: When buying, each mortgage payment contributes to your equity in the property. For example, if you purchase a home for $300,000 with a 20% down payment, you initially have $60,000 in equity. In contrast, renting accumulates no equity, which can be perceived as money spent with no return.

- Tax Advantages: Homeowners enjoy unique tax benefits such as mortgage interest deductions, which can significantly lower taxable income. In 2023, this could be as much as $10,000 to $20,000 annually, depending on the mortgage size. Renters do not have similar deductions available to them.

- Investment Diversification: Owning property can be a critical part of a diversified portfolio. A home acts not just as a place to live but can also serve as a hedge against inflation, especially in hot markets. Renting, however, usually requires allocating a larger portion of income to ongoing expenses without the potential for capital appreciation.

Comparative Investment Table

| Factor | Buying a Home | Renting a Home |

|---|---|---|

| Initial Investment | 20% of property value | First month’s rent + deposit |

| Long-term Appreciation Rate | 4% annually | Varies, typically limited |

| Equity Build-Up | Builds with each payment | None |

| Tax Benefits | Yes, mortgage deduction | No |

| Long-term Cost | Potentially lower overall | Higher cumulative payments |

Real-World Examples

To illustrate the differences, let’s look at two families:

1. The Smiths: They bought a $350,000 home with a 20% down payment. Over ten years, they paid down the mortgage and saw their home appreciate at 4% annually. After ten years, their home’s value rose to approximately $515,000, giving them over $200,000 in equity, not accounting for the tax savings they enjoyed during that period.

2. The Johnsons: They chose to rent a similar property for $1,800 per month. Over ten years, their rental payments summed to over $216,000 with no equity gain. While they had lower initial costs, they cannot capture any appreciation or benefits that the Smiths experienced.

Practical Implications for Readers

When contemplating renting versus buying, consider how each option will serve as a long-term investment. Here are actionable insights:

- Evaluate your market: Research how home values and rental prices have changed in your area over the last decade. Use this data to project future trends when determining the best long-term investment.

- Assess personal financial goals: Factor in how long you plan to stay in a location. If you’re looking at a lengthy commitment, buying could offer substantial long-term returns compared to renting.

- Leverage tax benefits: Consult with a financial advisor to maximize the tax advantages associated with homeownership that could enhance your long-term investment strategy.

- Monitor housing market conditions: Stay informed about local trends that could affect home prices and rental rates to make better investment decisions tailored to your situation.

Understanding these factors allows you to critically assess the long-term investment benefits associated with renting versus buying.

Benefits of Homeownership Over Renting

Deciding between homeownership and renting goes beyond financial implications; it touches on quality of life, stability, and personal creativity. Understanding the specific benefits of owning a home can help you make a more informed choice that aligns with your lifestyle and long-term goals.

Stability and Predictability

One significant advantage of homeownership is the stability it affords you. Unlike renting, where lease agreements are annually renewed and rental prices can increase, homeowners typically benefit from fixed mortgage payments, especially with a fixed-rate mortgage. This predictability can make budgeting more straightforward.

- Lower Long-Term Costs: Owning can lead to lower overall housing costs. Studies indicate that homeowners save roughly 30% more compared to renters over a 30-year period.

- Avoiding Rent Increases: Renting can leave you vulnerable to annual price hikes. In fact, approximately 45% of renters report facing rent increases in their lease renewals.

Customization and Personalization

Owning a home allows you the freedom to customize your living space without seeking landlord permission. This means you can create a personal haven that reflects your tastes and interests.

- Home Renovations: According to recent surveys, around 60% of homeowners have invested in renovations, significantly increasing their property’s value and their happiness at home.

- Outdoor Spaces: You may also create gardens, patios, or other outdoor features that bring joy and increase property appeal.

Community Ties and Financial Benefits

Homeownership often solidifies your connection to the community. Homeowners tend to stay in one place longer than renters, which helps foster community relationships and a stable social environment.

- Community Engagement: Studies show that homeowners are 20% more likely to participate in local events and volunteer activities, enhancing community involvement.

- Tax Benefits: Homeowners can often deduct mortgage interest and property taxes on their federal income tax returns. This can lead to significant savings, averaging around $2,000 per year depending on the location.

| Benefit | Homeownership | Renting |

|---|---|---|

| Predictability of Payments | Fixed-rate mortgage | Potential annual increases |

| Customization Freedom | Full control | Limited changes allowed |

| Community Engagement | Higher involvement | Often transient |

| Tax Deductions | Available | None |

| Long-term Cost Savings | 30% lower over 30 years | Potential increased costs |

Real-World Examples

Consider Jane and Mike, first-time buyers who purchased a home in their neighborhood. By investing in energy-efficient upgrades, such as solar panels, they reduced their monthly utility bills by 40% and increased their home’s value. In contrast, their friend Sara, who rents, faces rising monthly rents and lacks the freedom to make similar improvements.

In another instance, Tom and Lisa, who have been homeowners for five years, found that their property appreciated significantly, allowing them to refinance and fund their children’s education. Conversely, their neighbor who rents is faced with the uncertainty of fluctuating rental prices and has no ability to build equity.

Practical Implications for Readers

Owning a home offers you long-term stability, the ability to customize your space, and enhanced community involvement. Consider how much you value consistency and personalization when making your decision. By investing in homeownership, you not only secure a place to live but also build a future for yourself and your family.

As you weigh your options, remember these actionable insights:

- Research local market conditions to understand the potential for appreciation.

- Calculate potential tax deductions based on your local tax laws and rates to see how they could enhance your financial situation.

- Explore mortgage options to lock in a stable payment that can assist with long-term budgeting.

Real-World Scenarios for Renting Decisions

Deciding whether to rent or buy a home can be nuanced, shaped by your unique circumstances. Let’s explore real-world scenarios that can influence your renting decisions, helping you visualize how different situations might inform your choice.

Key Real-World Factors Affecting Renting Decisions

1. Job Flexibility: If you’re in a field that requires frequent relocation, renting offers flexibility. Studies show that about 56% of renters cite job mobility as a primary reason for not buying.

2. Debt-to-Income Ratios: If your debt-to-income ratio exceeds the ideal threshold of 36%, renting may be a practical choice. Approximately 40% of renters find themselves in a situation where buying would further strain their finances.

3. Local Housing Markets: Depending on where you live, renting might make more financial sense. In urban areas, like San Francisco, where housing costs rise significantly, nearly 65% of residents rent.

4. Short-Term Housing Solutions: For those pursuing education or temporary work arrangements, renting can provide a viable short-term housing solution. Around 30% of college students choose to rent, avoiding long-term commitments.

Comparative Table: Rental Scenarios vs. Buying Potential

| Scenario | Percentage of Renters | Key Considerations |

|---|---|---|

| Job Relocation | 56% | Flexibility in changing jobs or locations |

| High Debt-to-Income Ratios | 40% | Avoiding further financial burden |

| Urban Living | 65% | Cost-effectiveness in high-demand markets |

| Short-Term Living Arrangements | 30% | Flexibility for students or temporary roles |

Real-World Examples

- Case Study: Alex in San Francisco: Alex works in tech and frequently changes jobs. He opted to rent instead of buying to maintain mobility. His decision reflects the 56% of renters who prioritize job flexibility over homeownership.

- Case Study: Lisa, a Recent Graduate: Lisa recently graduated with student loans. With a debt-to-income ratio above 40%, she chose to rent an apartment for the next two years. This decision aligns with 40% of renters who avoid purchase strains.

- Case Study: Sam’s Urban Living: Living in New York City, Sam found that renting was significantly cheaper than buying due to high property prices. With nearly 65% of city residents opting to rent, his choice mirrors common local trends.

Practical Implications for Readers

When considering renting, think about your current and future life plans. Are you in a transitional phase, like starting a new job or relocating for education? If so, renting often provides the flexibility you need to navigate these changes without the long-term commitment of buying.

Always assess your finances and local housing market trends before making decisions. If debt is a concern or you live in high-cost areas, renting can be a smart choice to maintain financial health while keeping future options open.

Remember, these real-world scenarios can guide you toward making informed renting decisions that suit your unique lifestyle without bearing additional financial weight.

Current Market Trends and Housing Statistics

In the dynamic landscape of real estate, understanding current market trends and housing statistics is pivotal for making informed decisions regarding renting and buying a home. Let’s delve into some intriguing trends and data shaping today’s rental and purchasing markets.

Key Market Trends

- Rental Prices Surge: In major urban areas, rental prices have increased by over 15% in the last year alone, reflecting a spike in demand as people migrate back to cities post-pandemic.

- Home Prices Stabilizing: After a period of rapid growth, home prices have leveled off, with a national average increase of only 2% in the last six months, indicating a shift towards a more balanced market.

- Vacancy Rates Dropping: The nationwide vacancy rate for rental properties has decreased to approximately 6.2%, down from 8.1% last year. This indicates growing competition among renters.

- Interest Rate Influence: Mortgage interest rates have seen fluctuations, currently averaging around 6.5%, affecting buyers’ purchasing power and overall market activity.

Comparative Table of Current Rental and Buying Trends

| Metric | Renting | Buying |

|---|---|---|

| Average Monthly Cost (2023) | $2,175 | $1,850 (mortgage) |

| Annual Price Growth | 15% | 2% |

| Vacancy Rate | 6.2% | N/A |

| Current Average Interest Rate | N/A | 6.5% |

| Percentage of Renters to Owners | 35% | 65% |

Real-World Examples

- Urban Migration: Cities like Austin have seen rental prices surge by 20% due to an influx of remote workers seeking more space, leading to higher demand in rental markets.

- Homebuyer Decisions: In suburban areas, many first-time buyers are opting to purchase homes despite rising mortgage rates, drawn by the relative affordability compared to city rentals.

- Investment Shifts: Investors are increasingly favoring rental properties as a hedge against inflation, anticipating that continued demand for rentals will yield stable cash flows.

Practical Implications for You

Understanding these market trends can empower you to make educated decisions about whether to rent or buy. For instance, if you’re in a metropolitan area where rental prices are escalating rapidly, it may be wise to consider buying before housing prices and interest rates rise further. Additionally, if you find yourself priced out of buying, analyzing rental trends can help you negotiate better deals or seek more affordable neighborhoods without sacrificing quality of life.

Actionable Advice

Stay updated on local housing statistics, as they can fluctuate significantly based on geography. Additionally, it’s advisable to leverage online tools for real-time data on rental prices and mortgage rates. Knowing when to act, based on these trends, can significantly influence your long-term financial position in the current market landscape.

Flexibility and Lifestyle Considerations

When it comes to choosing between renting and buying a home, flexibility and lifestyle considerations play an essential role in your decision. Life is unpredictable, and your housing situation should easily adapt to your circumstances. Let’s dive into how each option stacks up in regard to flexibility and lifestyle adaptability.

Key Points of Flexibility

1. Mobility: Renting typically allows for greater mobility. You can easily relocate for a job, personal reasons, or simply a change of scenery without the burden of selling a home.

2. Short-Term Commitments: Many rental agreements are for 12 months or even month-to-month, which can be a perfect fit if you’re in a transitional phase in life, such as starting a new job or pursuing education.

3. Maintenance Responsibilities: As a renter, you usually enjoy reduced maintenance responsibilities. Your landlord is often responsible for repairs, enabling you to focus more on your lifestyle rather than property upkeep.

4. Customization: While renters have some degree of personalization with decor, homeowners enjoy unrestricted freedom to modify and renovate, creating a space that reflects their lifestyle. However, this can sometimes tie homeowners to a specific location.

Comparative Lifestyle Matrix

| Aspect | Renting | Buying |

|---|---|---|

| Mobility | High (easy to relocate) | Low (requires selling) |

| Lease Duration | Flexible (month-to-month) | Long-term commitment |

| Maintenance Responsibility | Minimal (landlord’s duty) | High (owner’s responsibility) |

| Personalization | Limited (landlord approval) | Unlimited (full freedom) |

Real-World Examples

- Emily’s Job Change: Emily rented a chic apartment in an urban area while she searched for her ideal job. When a great opportunity arose in another city, she simply gave a month’s notice and moved without the hassle of selling property. This flexibility allowed her to quickly capitalize on her employment opportunity.

- Mark and Susan’s Family Transition: Recently married, Mark and Susan opted to rent a townhome in their desired district for a year. This decision provided them the breathing room to assess their future. They enjoyed the perks of renting while waiting for the perfect time to buy their forever home in a neighborhood that suits their life goals.

Practical Implications for Readers

As you weigh your options, consider your current and anticipated lifestyle needs. Here are some actionable insights:

- Evaluate Future Plans: If you anticipate significant life changes or job transitions within the next few years, renting may be the better route for flexibility.

- Discuss Furnishing Options: Understand the limits on personalization when renting. If a customized living space is critical for your lifestyle satisfaction, you may want to factor that into your decision-making.

- Assess Your Need for Stability: If you value routine and stability more than mobility, consider how long you plan to stay in one location, which may justify the commitment to buying.

- Analyze Location Needs: If location flexibility is paramount, renting can give you the freedom to explore various neighborhoods and cities before committing to a property.

For anyone facing the decision of renting versus buying, think about future life changes and how each option can adapt to those scenarios. Prioritize what matters most in your lifestyle and use that clarity to guide your housing choice.

Maintenance Responsibilities in Renting vs Buying

When deciding between renting and buying a home, understanding the maintenance responsibilities that come with each option is crucial. Maintenance can be a hidden cost that many overlook, impacting both your financial obligations and lifestyle. Let’s explore how these responsibilities differ, as they can significantly influence your living experience.

Key Responsibilities

- Renting: Typically, landlords are responsible for most maintenance tasks. This includes:

- Routine upkeep, such as landscaping and snow removal.

- Emergency repairs, like plumbing or electrical issues.

- Ensuring that the property meets safety and health codes.

- Buying: As a homeowner, you’re in charge of all maintenance responsibilities. This entails:

- Handling unexpected repairs, which can average anywhere from $1,500 to $5,000 per year depending on the home size and age.

- Regular maintenance tasks, including HVAC servicing, roof inspections, and yard work, which can also add up to about 1% of the home’s value annually.

Comparative Table of Maintenance Responsibilities

| Maintenance Responsibility | Renting | Buying |

|---|---|---|

| Routine Upkeep | Mostly covered by landlord | Homeowner’s responsibility |

| Emergency Repairs | Landlord handles | Homeowner must address |

| Annual Maintenance Average | Limited to landlord’s schedule | $1,500 to $5,000 |

| Safety and Health Inspections | Landlord responsible | Homeowner must ensure compliance |

Real-World Examples

Consider a couple, Sarah and Tom, who rented an apartment in a downtown area. During their lease, their landlord managed all maintenance issues, including an emergency plumbing problem that arose. They faced no costs, making their renting experience stress-free regarding house upkeep.

In contrast, when Lisa purchased an older home, she soon learned that the boiler required servicing, costing her $800 unexpectedly. This was just one example of the approximately 1% of her home’s value in annual maintenance that quickly added up, revealing the hidden responsibilities that come with homeownership.

Practical Implications

Understanding your responsibilities can guide your decision-making. If you prefer a hands-off approach to maintenance, renting might suit you better. Consider these insights:

- Know that, on average, homeowners might set aside 1% of their home’s value for maintenance annually. For a $300,000 home, that translates to $3,000 a year.

- Be prepared for unforeseen expenses when purchasing a home. Create an emergency maintenance fund to cushion these financial shocks.

Taking these factors into account can help you make a more informed choice between renting and buying, particularly concerning maintenance responsibilities.