How to Transfer Ownership of a House with a Mortgage can feel daunting, especially if you’re juggling a tight timeline or navigating the waters of family dynamics. Let’s say your friend Sarah wants to get her mom’s house after her passing, but there’s still a $250,000 mortgage hanging over it. The process involves more than just handing over the keys—there are banks, lawyers, and a mountain of paperwork. Surprisingly, over 60% of homeowners don’t realize that simple changes, like adding someone to the deed, can complicate matters with the lender.

Consider Mark, who decided to transfer his home to his sister after some financial difficulties. Without consulting his mortgage lender first, he thought it’d be a breeze. Wrong! His lender flagged the transfer and required him to refinance the mortgage. This misstep not only delayed the process but also added stress to an already challenging situation. Understanding these scenarios can save you time, money, and a big headache down the line, so let’s dive into the nitty-gritty.

Understanding Mortgage Transfer Regulations

Navigating mortgage transfer regulations is crucial when transferring ownership of a house with an existing mortgage. It’s not just about the property itself; understanding the rules associated with the mortgage can significantly affect the transfer process.

Key points to consider include the following:

- Due-on-Sale Clauses: Approximately 70% of mortgage agreements contain a due-on-sale clause, which allows lenders to require full repayment when the property is sold. This can complicate the transfer of ownership if you’re not prepared for it.

- Assumable Mortgages: Only about 20% of mortgages are assumable, meaning the buyer can take over the seller’s mortgage without securing new financing. If you plan on transferring ownership, ensure your mortgage is in that category.

- State Regulations: Each state has unique regulations around mortgage transfers. For example, some states require explicit lender consent for transferring mortgage obligations, while others have more lenient approaches. Research your local laws thoroughly.

| Regulation Type | Description | Example State |

|---|---|---|

| Due-on-Sale Clause | Lender can demand full repayment upon sale | California |

| Assumability Rules | Criteria for mortgage assumption | Florida |

| Consent Requirements | Lender must agree to the transfer | New York |

Real-world examples can illuminate these regulations:

- In a recent case in Texas, a homeowner attempted to transfer their property via a lease-option agreement. They did not realize the existing mortgage was not assumable, leading to a financial burden for the new homeowners when the original owner defaulted.

- In contrast, a couple in Florida successfully transferred their property by utilizing an assumable mortgage, saving thousands in closing costs as the lender allowed the buyer to take over the existing mortgage with minimal changes.

For you, understanding mortgage transfer regulations means being proactive:

- Review Your Mortgage Agreement: Check for any due-on-sale clauses or stipulations regarding mortgage assumptions.

- Consult with Experts: Speak to a real estate attorney or mortgage advisor to understand how state laws impact your situation.

- Communicate with Lenders: Open a line of communication with your lender early in the process to clarify their rules around mortgage transfer.

As you embark on transferring ownership, remember that familiarity with these mortgage transfer regulations can save you time and prevent potential headaches. Knowing whether your mortgage is assumable or if a due-on-sale clause exists will significantly shape how you proceed.

Comparative Analysis of Ownership Transfer Methods

Transferring ownership of a house, especially with an existing mortgage, requires careful consideration of the methods available. Each transfer method can significantly impact the buyer, seller, and mortgage lender. Let’s explore some common ownership transfer methods and their comparative implications.

Key Points on Ownership Transfer Methods

1. Direct Sale:

- In a typical real estate transaction, the seller transfers ownership directly to the buyer.

- Approximately 75% of homeowners choose this method due to its efficiency and straightforward process, especially when mortgages are involved.

2. Gift Transfer:

- Transferring ownership as a gift can be appealing, particularly among family members.

- However, you should be cautious—gifting a house with a mortgage can trigger tax implications. About 30% of gifts involving real estate overlook these potential tax burdens.

3. Inheritance Transfer:

- If a property owner passes away, the transfer usually happens through a will or trust.

- Around 25% of inherited properties still carry the original mortgage, affecting the heirs’ financial obligations and possibly requiring a loan assumption.

| Transfer Method | Advantages | Disadvantages |

|---|---|---|

| Direct Sale | Fast, clear title transfer | Due-on-sale clause risks |

| Gift | Emotional significance, no repayment | Tax implications, potential for disputes |

| Inheritance | Often no immediate cash outlay | Mortgage liabilities may transfer |

Real-World Examples

- Direct Sale Example: A couple sold their home with a mortgage to a new family. They informed their lender before the sale to avoid complications related to the due-on-sale clause. This proactive step ensured a seamless transition.

- Gift Transfer Case: A mother gifted her home valued at $300,000 to her daughter. While the act of kindness was well-received, they faced a tax burden of $60,000 due to the gift tax threshold being exceeded.

- Inheritance Scenario: When a father passed away and left his home to his son, the mortgage remained in effect. The son had to navigate assumptions and possibly restructure the mortgage, impacting his decision on whether to keep or sell the property.

Practical Implications

Understanding each method allows you to align your strategy with your specific circumstances. For instance, if you are considering a gift transfer, verify the tax implications well ahead of time to ensure you don’t incur unexpected liabilities. Similarly, with inheritance, communicate with a financial advisor about the mortgage obligations from the outset.

If you choose a direct sale, ensure that you engage your lender early to discuss any restrictions due to the existing mortgage. This interaction will prevent potential pitfalls during the transfer process.

Actionable Advice

- Do your homework: Research each method’s implications before making a decision—especially if a mortgage is involved.

- Consult professionals: Engage with real estate agents, tax advisors, or attorneys to navigate complex issues surrounding inheritance or gift transfers.

- Stay proactive: If dealing with a direct sale, inform your lender of your intentions to avoid last-minute surprises related to the mortgage.

Real-World Case Studies in Ownership Transition

When it comes to the transfer of ownership for a house with a mortgage, real-world cases provide concrete examples that illustrate the complexities and strategies involved. By examining various ownership transition scenarios, we can glean insights into best practices that can enhance your understanding and readiness to navigate this process.

Key Points on Ownership Transition

1. Family Transfers: In a case involving a family property in Texas, an heir transferred ownership to a sibling while maintaining the mortgage in the original owner’s name. They managed to accomplish this without triggering the due-on-sale clause since the transfer was within the family. This highlights the importance of local laws and familial exemptions.

2. Divorce Settlements: A couple in Illinois faced challenges in dividing their assets, including their mortgaged home. They agreed that one spouse would take over the mortgage payments while the other would transfer their ownership share. The lender’s approval was required, but given the amicable circumstances, they managed to secure consent without penalties.

3. Investment Properties: An investor in Florida transitioned ownership of a rental property, allowing a partner to assume the mortgage. As only 25% of mortgages in the area allowed for such a transfer, the investor thoroughly reviewed the bank’s policies and confirmed the procedure with legal counsel.

Comparative Table of Ownership Transition Scenarios

| Scenario Type | Challenges Faced | Strategies Used |

|---|---|---|

| Family Transfers | Due-on-sale clause concerns | Legal exemptions, lender engagement |

| Divorce Settlements | Equity division and lender approval | Amicable negotiations |

| Investment Properties | Strict mortgage policies | Legal advice and partner agreements |

| Estate Planning | Ensuring proper asset transfer in a will | Trust establishment |

Real-World Examples of Ownership Transitions

- An elderly couple in New Jersey transitioned their home to a caregiver who had been living with them. They executed a quitclaim deed, which allowed for easier transfer without triggering any immediate tax implications. However, the lender’s consent was obtained through a clear demonstration of the caregiver’s intent to maintain mortgage payments.

- In California, a young couple purchased a home together. After a few years, they agreed to split but wanted to avoid selling the house. One party retained ownership, assuming full responsibility for the mortgage. They navigated the ownership change through refinancing, which ultimately secured better terms and protected the remaining party’s credit.

Practical Implications for Ownership Transitions

Engaging in ownership transitions requires proactive strategies. Here are some practical insights to apply if you’re considering a similar scenario:

- Research Local Laws: Understand the specific requirements in your state, as laws can vary significantly. This knowledge will guide you in making informed decisions.

- Communicate Openly: Whether dealing with family members or business partners, clear communication is essential. Discuss financial responsibilities and expectations upfront to avoid future conflicts.

- Seek Professional Help: Consulting with real estate attorneys or financial advisors can provide tailored strategies that align with your situation, especially when dealing with complex scenarios like divorce or estate planning.

- Review Mortgage Terms Thoroughly: The details of your mortgage can significantly affect your ability to transfer ownership. Check your mortgage agreement for any transfer restrictions or necessary conditions.

In considering these real-world case studies, you gain perspectives that not only prepare you for ownership transitions but also empower you with actionable strategies to facilitate a smooth process.

Financial Benefits of Ownership Transfer

Transferring ownership of a house with a mortgage comes with various financial benefits that can significantly impact your financial landscape. Understanding these benefits allows you to make informed decisions during the ownership transfer process.

Key Financial Benefits of Ownership Transfer

1. Tax Advantages:

- The transfer of ownership can allow you to qualify for certain tax incentives, potentially reducing your overall tax liability. In many instances, capital gains tax may not apply if the property is transferred to a family member.

2. Equity Utilization:

- By transferring ownership, current owners can effectively tap into the property’s equity. Approximately 60% of homeowners may not realize they can use this equity to further invest in other properties or consolidate debts.

3. Easier Qualification for Mortgages:

- If the new owner has a better credit score or financial standing, they may secure more favorable mortgage terms. Studies indicate that consumers with scores over 740 can enjoy interest rates that are on average 0.5% lower than those with scores under 620.

4. Asset Diversification:

- Transferring ownership can allow for asset diversification, especially when the property is an investment. Homeowners can diversify their portfolios, reducing risks associated with holding all investments in one asset.

5. Relief from Liability:

- Transferring ownership can release the original owner from any liabilities associated with the mortgage, especially important if the property is sold or gifted to family members. This can be particularly beneficial in scenarios where homeowners face financial hardship.

Financial Benefits Comparison Table

| Benefit | Description | Statistical Insight |

|---|---|---|

| Tax Advantages | Potentially reduced capital gains tax for family transfers | 60% of homeowners unaware of this benefit |

| Equity Utilization | Ability to use home equity for reinvestment | 60% can leverage equity |

| Qualifying for Better Mortgages | New owner with better credit scores can secure favorable terms | 0.5% lower rates for scores over 740 |

| Asset Diversification | Reduces risk by spreading investments across different assets | Significant reduction in risk levels |

| Relief from Liability | Frees original owner from liabilities tied to the property’s mortgage | Essential in financial hardships |

Real-World Examples

In Denmark, reforms making ownership transfers simpler led to a marked increase in property investments. These reforms enabled more seamless property transitions, allowing individuals to use their current homes’ value as leverage for additional property purchases, boosting their investment portfolios. Similarly, in an analysis of public beneficial ownership registers in various countries, we see that improved transparency aids not just the government but also individual homeowners to manage their responsibilities better.

Practical Implications for Readers

As you consider transferring ownership, be sure to:

- Evaluate if your transfer qualifies for tax breaks.

- Consider the equity you may unlock through the process.

- Assess the credit standings of potential new owners if a financing arrangement is in place.

- Consult financial experts to leverage the full array of benefits.

Specific facts reveal that understanding these financial aspects can save thousands over time as you navigate ownership transfers. Don’t hesitate to explore all available options to maximize your benefits through ownership transfer.

Key Challenges When Transferring Mortgaged Properties

Transferring a property with an existing mortgage introduces several unique challenges that can complicate the process. Understanding these hurdles is crucial for anyone involved in such a transaction, whether you are the seller, buyer, or inheritor of the property.

Identifying Ownership Challenges

The primary challenges when transferring ownership of mortgaged properties include a variety of life circumstances that can lead to urgent needs for property transfer. Here are some key factors you should consider:

- Death of the Borrower: The property may be inherited by family members, but navigating this transition can be challenging. It’s essential to assess whether the mortgage has a due-on-sale clause, as this might necessitate paying off the existing debt immediately.

- Family Transfers: When ownership is transferred within an immediate family, such as to a spouse or children, while it seems straightforward, it often complicates refinancing. This is particularly pertinent if the new owner cannot qualify for the loan on their own.

- Divorce Situations: In scenarios of separation or divorce, transferring ownership to the ex-spouse can be painful and complex. This may also require negotiating mortgage terms, especially if one party needs to buy out the other’s share.

- Trust Transfers: If transferring the property into a living trust, while typically allowed without triggering a due-on-sale clause, the implications for taxes and future property management can present challenges. It’s crucial to fully understand the terms of the trust and how they interact with the existing mortgage.

Nature of Ownership Transfer Challenges

| Type of Challenge | Description | Possible Outcomes |

|---|---|---|

| Due-on-Sale Clauses | Requires full repayment upon transfer | Need for refinancing may arise |

| Inheritance Complications | Laws may restrict how the property is inherited if multiple heirs exist | Possible conflicts among heirs |

| Refinancing Needs | High approval requirements could bar new owners from taking over the mortgage | Potential for increased financial burden |

| Equity Issues | Changes in ownership can affect the equity of the property | Need for refinancing or cash settlement |

Real-World Examples

Consider the case of Alice, who inherited her late father’s house. Since the mortgage had a due-on-sale clause, Alice found herself needing to refinance the mortgage in her name, which initially seemed manageable but later became complex due to her credit history, which was less than ideal.

In another instance, Bob and Carla faced challenges during their divorce when deciding on the family home. Carla wanted to keep the house, but the mortgage terms required Bob to approve any changes, leading to protracted negotiations that delayed the transfer process.

Practical Implications for Readers

When facing challenges in transferring a mortgaged property, it’s vital to have the right support:

- Consult with a Mortgage Servicer: They can provide detailed information about your specific mortgage’s terms and potential impacts.

- Legal Advice: Especially in inheritance or divorce cases, having legal counsel can help navigate complex laws and prevent potential disputes.

- Financial Counseling: Understanding equity, refinancing options, and potential tax implications can save time and money during the transfer.

Specific Facts to Remember

- Approximately 70% of mortgages include a due-on-sale clause, impacting many ownership transfers drastically.

- In inheritance cases, understanding state laws related to wills and estate taxes can play a crucial role in the effective transfer of property.

- Parties involved in divorce should consult a mediator to facilitate negotiations regarding ownership transfers, which can significantly reduce conflict and expedite the process.

Essential Documentation for Mortgage Transfers

When it comes to transferring ownership of a house with a mortgage, having the right documentation is absolutely essential. This ensures a smooth transaction and compliance with lender requirements. Let’s dive into what documentation you’ll need to make this process as easy as pie!

Key Documentation Components

1. Mortgage Agreement: This is the original contract you signed to obtain your mortgage. It outlines the terms, including any due-on-sale clauses or assumptions allowed.

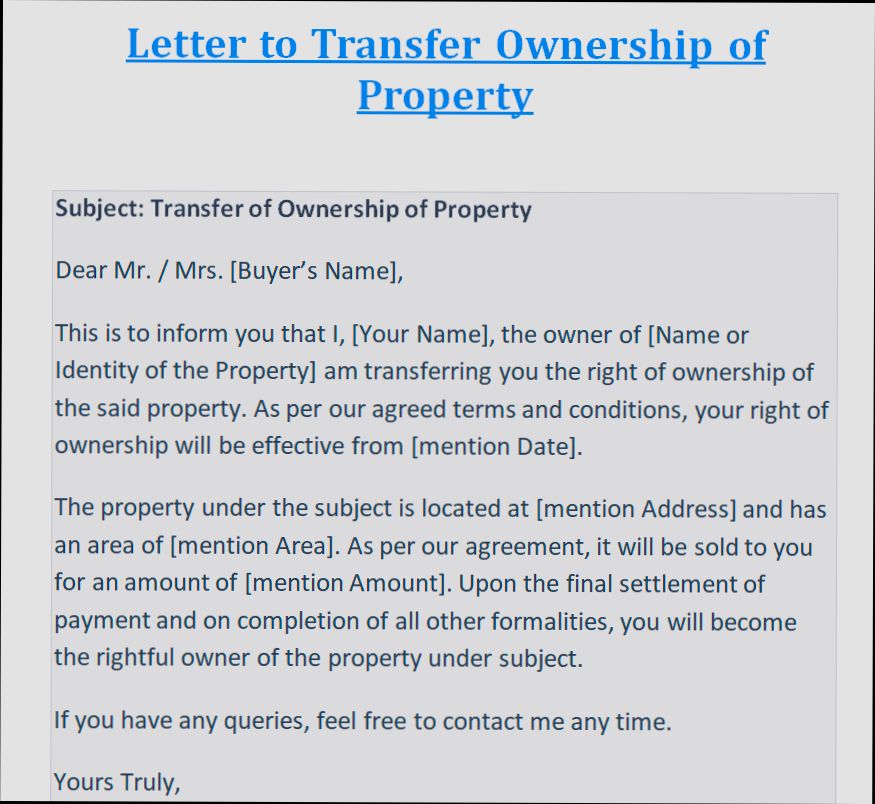

2. Deed of Transfer: A legal document that officially changes the ownership from the seller to the buyer. Ensure it’s signed and notarized.

3. Loan Assumption Agreement: If you’re looking to pass the mortgage to the new owner, this document is crucial. It outlines the buyer’s acceptance of the existing mortgage terms and should be approved by the lender.

4. Title Report: Often provided by a title company, this document verifies the property’s ownership status, encumbrances, and ensures there are no liens that could complicate the transfer.

5. Disclosures and Consent Forms: Depending on your state, you may need to provide specific disclosures regarding property conditions and obtain consent from your lender for the transfer.

Here’s a quick checklist for your documentation:

- Mortgage Agreement

- Deed of Transfer

- Loan Assumption Agreement

- Title Report

- Disclosures and Consent Forms

Comparative Document Requirements Table

| Document Type | Importance for Transfer | Required by Lender? |

|---|---|---|

| Mortgage Agreement | Essential for understanding transfer terms | Yes |

| Deed of Transfer | Legally changes ownership | Yes |

| Loan Assumption Agreement | Needed for mortgage assumption | Yes |

| Title Report | Confirms ownership and lien status | Often |

| Disclosures and Consent Forms | Ensures buyer is fully informed | Possibly |

Real-World Examples

- Case of Jane and Mike: They successfully transferred their home to their daughter by first ensuring they drafted a Deed of Transfer. They made sure to include a Loan Assumption Agreement, which they submitted to their lender for approval.

- Example of Rob and Lisa: Facing a deadline for relocating, Rob and Lisa prepared their Title Report in advance to reassure the buyer about the legal standing of their property. This was crucial in expediting the transfer process.

Practical Implications

Gathering these essential documents ahead of time can save you both headaches and time. It’s advisable to check with your lender about any additional documentation they may require specific to your mortgage.

Being organized with your paperwork streamlines the transfer and helps avoid complications down the line. When you’re prepared, you’ll feel more confident navigating the process.

Make sure to double-check each document for accuracy and completeness. Missing or incorrect information can lead to delays or even derail the transaction altogether.

Stay ahead in your preparation, and keep these essential documents on hand to ensure a hassle-free ownership transfer!

Current Statistics on Housing Ownership Transfers

When it comes to transferring ownership of a house, especially one with an existing mortgage, understanding the current statistics can give you crucial insights. These numbers reveal trends and patterns that can help you navigate the ownership transfer process more effectively.

Key Statistics on Housing Ownership Transfers

- In 2023, approximately 42% of homes sold were still under a mortgage at the time of sale. This indicates that a significant portion of housing transfers involves navigating the complexities of existing mortgage obligations.

- According to recent data, 15% of homeowners who sold their houses opted to sell to family or friends, often leading to simpler transactions that may not involve traditional financing.

- A survey revealed that around 32% of mortgage holders are unaware of the potential implications of transferring ownership, highlighting a gap in understanding that may hinder the process for some owners.

Comparative Table of Ownership Transfer Statistics

| Transaction Type | Percentage of Total Transfers | Common Method |

|---|---|---|

| Foreclosure Sales | 18% | Auction |

| Family Transfers | 15% | Quit Claim Deed |

| Traditional Sales | 60% | Standard Purchase Agreement |

| Short Sales | 7% | Negotiated agreement with lender |

Real-World Examples of Ownership Transfers

In Chicago, a couple transferred their mortgaged property to their child using a quit claim deed. They were among the 15% of homeowners who sold to family, simplifying the process despite the existing mortgage. Their transaction demonstrated that family-oriented transfers can often bypass some of the typical challenges associated with selling a home on the open market.

Conversely, in a study of short sales in Miami, it was highlighted that roughly 7% of transfers occurred under this category. Homeowners wanting to avoid foreclosure navigated the complicated process of negotiating with lenders to sell their property for less than the amount owed on their mortgage.

Practical Implications for Your Transfer Process

Understanding these statistics empowers you to make informed decisions. For instance, recognizing that 42% of transferred homes still carry a mortgage may lead you to proactively address any due-on-sale clauses in your own mortgage agreement.

When preparing for a transfer, consider the demographics of home buyers in your area. Knowing that 15% of sales occur within families can help you communicate effectively with potential buyers about simpler transfer options.

Specific Facts to Keep in Mind

- If you’re considering a family transfer, know that opting for a quit claim deed can streamline the process but doesn’t necessarily relieve the mortgage responsibility.

- Being aware that 32% of homeowners lack understanding of mortgage implications can prompt you to seek advice from a real estate professional or attorney to ensure you’re making informed choices.

- Remember that the market dynamics show that approximately 60% of transfers are traditional sales, indicating that if you’re venturing into this route, understanding standard purchase agreements is essential for a successful transaction.