How to get equity out of your home without refinancing might sound tricky, but it’s totally doable! Picture this: you’ve built up $50,000 in equity because your home’s value skyrocketed — let’s say from $300,000 to $400,000 in just a few years. Instead of going through the hassle of refinancing, where you’d incur closing costs and could potentially increase your debt, you can tap into that equity through a home equity line of credit (HELOC). This flexible option lets you borrow against your home’s value, giving you access to cash for home improvements or paying off high-interest debt without resetting your mortgage.

You might also consider a cash-out refinance, but that isn’t your only choice. Home equity loans are another alternative where you receive a lump sum based on your equity. Imagine needing cash for a major expense like medical bills or funding your kid’s education — both options can provide the funds you need while keeping your existing mortgage intact. With average home prices rising and many homeowners sitting on significant equity, understanding your choices can empower you to make informed financial moves.

Exploring Home Equity Lines of Credit

Home Equity Lines of Credit (HELOCs) offer a flexible way to access the equity you’ve built in your home without needing to refinance. Unlike traditional loans, HELOCs allow you to borrow against your home equity on an as-needed basis, making them a popular choice for homeowners looking for financial flexibility.

Understanding HELOC Basics

A Home Equity Line of Credit is essentially a revolving credit line secured by your home. Here are some key features you should keep in mind:

- Interest Rates: Interest rates for HELOCs are usually variable, often starting around 4% to 10%, depending on market conditions and your credit profile.

- Draw Period: Typically lasts 5 to 10 years, during which you can borrow and repay as needed, often with interest-only payments.

- Repayment Period: Following the draw period, you may need to pay off the balance over 10 to 20 years.

Key Statistics on HELOC Usage

- Recent surveys indicate that over 60% of homeowners are considering a HELOC as their first option for tapping into home equity.

- In the U.S., the average HELOC limit has reached approximately $150,000, providing substantial access to funds for many families.

- Approximately 80% of HELOC borrowers use these funds for home improvements, making it a sensible option for those looking to increase their property’s value.

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Type of Borrowing | Revolving Credit Line | Lump-Sum Loan |

| Interest Rate Types | Variable | Fixed |

| Draw Period | Yes | No |

| Repayment Flexibility | High | Low |

| Typical Loan Amount | Up to 85% of Equity | 80% of Equity |

Real-World Examples

Consider Sarah, a homeowner who has built $100,000 in home equity. She decides to open a HELOC, which allows her to withdraw funds as needed. Over the next few years, she uses $30,000 to renovate her kitchen, transforming her home and increasing its market value substantially. Sarah now has the flexibility to either repay the borrowed amount or draw more funds if opportunities arise.

Similarly, John applied for a HELOC after realizing that his home’s value had appreciated significantly. By opting for a $50,000 line of credit, he financed a landscape overhaul and a new roof, which not only enhanced his home’s aesthetic appeal but also its overall marketability.

Practical Implications for You

When considering a HELOC, think about these practical aspects:

- Emergency Fund: A HELOC can serve as a safety net for unexpected expenses, offering peace of mind and financial flexibility.

- Improvement Projects: If you are planning major home renovations, using a HELOC allows you to manage cash flow without the immediate burden of large, upfront costs.

- Debt Consolidation: You can use your HELOC to pay off high-interest debts, improving your financial health if managed wisely.

Actionable Advice on HELOCs

- Shop Around: Interest rates and terms can vary widely among lenders. Take the time to compare several offers to find the best deal tailored to your needs.

- Understand Your Limits: Know how much equity you have in your home and how much you can borrow without overstretching your finances.

- Plan Payments Strategically: Consider how you will repay any amounts drawn during the draw period to avoid potential financial strain once the repayment phase begins.

The Role of Cash-Out Appraisals

Cash-out appraisals play a crucial role in helping homeowners tap into their equity without triggering a full refinancing of their mortgage. This process provides a pathway to assess your home’s current market value, which can unlock significant funds for various expenses or investments. Understanding how cash-out appraisals work can empower you to make informed financial decisions.

What is a Cash-Out Appraisal?

A cash-out appraisal is a formal evaluation to determine your home’s market value, typically arranged when you want to access a portion of your equity. The appraiser examines various factors including property condition, recent sales of comparable homes, and market trends. Here are some key characteristics:

- Objective: Establishes the current value of your property.

- Required Documents: You may need to provide recent improvements, permits, and previous appraisals.

- Professional Assessment: Conducted by a licensed appraiser who adheres to industry standards.

Importance of Cash-Out Appraisals

Understanding the importance of cash-out appraisals can dramatically influence your borrowing strategy. Here are several critical points:

1. Equity Access: Accurate appraisals ensure you receive an appropriate amount of equity; otherwise, you might undervalue your home.

2. Loan Approval: Lenders often require appraisals to approve lines of credit or other borrowing options.

3. Valuation Trends: Regular appraisals help homeowners track value appreciation, assisting in future financial planning.

| Feature | Cash-Out Appraisals | Home Equity Line of Credit (HELOC) |

|---|---|---|

| Purpose | Value assessment | Access revolving credit |

| Frequency | As needed | Can be continuous |

| Cost | Varies by location | Typically lower upfront costs |

| Impact on Loan Amount | Direct connection | Indirect, based on your equity |

Real-World Examples

Consider these scenarios related to cash-out appraisals:

- Case Study 1: Maria, a homeowner in California, sought to remodel her kitchen and needed $40,000. After a cash-out appraisal revealed a home value increase of 15%, she was able to access her equity without refinancing, maximizing her funds for renovations.

- Case Study 2: John and Sara wanted to invest in a rental property. Their appraisal showed that their home appreciated significantly due to recent renovations. This allowed them to leverage equity and secure additional financing for their investment goals.

Practical Implications

When considering a cash-out appraisal, think about the following practical aspects:

- Plan Ahead: Schedule your appraisal strategically to align with market trends that could enhance your home’s value.

- Invest Wisely: Use the funds obtained through a cash-out appraisal for high-return investments or necessary expenses to maximize the equity you release.

- Stay Informed: Keep abreast of local real estate trends to anticipate potential equity changes in your home.

It is critical to note that cash-out appraisals can provide direct access to funds based on current market conditions, while also allowing you to maintain your existing mortgage terms.

Understanding Home Equity Loan Benefits

When you think about accessing the value in your home, understanding the benefits of a home equity loan can empower you to make informed financial decisions. A home equity loan enables you to leverage your property’s equity without needing to refinance your existing mortgage, providing you with a one-time lump sum that can be used for various needs.

Key Advantages of Home Equity Loans

1. Predictable Payments: Home equity loans typically come with fixed interest rates, meaning your monthly payments remain consistent throughout the loan term. This predictability can facilitate budgeting and financial planning.

2. Tax Benefits: In many cases, the interest you pay on a home equity loan is tax-deductible, provided you use the funds to purchase, build, or substantially improve your home. This can lead to considerable savings at tax time.

3. Quick Access to Funds: Home equity loans usually have a simplified approval process compared to other types of financing. Once approved, you receive a lump sum, which can be funded quickly, allowing you to address urgent financial needs.

4. Lower Interest Rates Compared to Unsecured Loans: Because a home equity loan is secured by your property, it often carries lower interest rates than unsecured financing options like personal loans or credit cards. This means you can save on interest costs over the life of the loan.

5. No Need to Refinance: By choosing a home equity loan instead of refinancing your mortgage, you maintain your existing mortgage terms and interest rate, which can be beneficial if your current mortgage rate is lower than current market rates.

Comparative Table of Home Equity Loan Benefits

| Benefit | Description | Potential Impact |

|---|---|---|

| Fixed Monthly Payments | Consistent payments simplify financial planning | Easier budgeting |

| Tax-Deductible Interest | May reduce overall tax liability if funds are used for home improvements | Saves money on taxes |

| Quick Funding | Fast approval and funding process | Immediate access to cash |

| Lower Interest Rates | Generally lower than unsecured loans | Saves on interest cost |

| Keeps Existing Mortgage Terms | Maintains current mortgage rate and payments | Avoids disadvantageous refinancing |

Real-World Examples

- Example 1: Sarah needed $40,000 for home renovations. She opted for a home equity loan with a fixed rate of 5%. The predictability of her payments allowed her to comfortably manage her monthly budget, and because she used the money to improve her home, she was also eligible to deduct the interest on her taxes.

- Example 2: John was facing unexpected medical expenses totaling $25,000. He took out a home equity loan secured against his property and appreciated the lower interest rate of 4.5% compared to the credit card interest of over 18%. This decision significantly reduced his financial strain.

Practical Implications

Understanding the advantages of home equity loans means you can better assess your options for accessing funds. If you find yourself needing cash for home improvements, debt consolidation, or major purchases, a home equity loan could be a wise choice, allowing flexibility and affordability without altering your mortgage.

- Actionable Tip: Before applying for a home equity loan, compare offers from different lenders to find competitive interest rates and favorable terms. Don’t hesitate to negotiate the fees and terms to get the best deal possible.

- Remember: If you’re considering a home equity loan, ensure that the loan amount aligns with your financial goals and that you have a clear plan for repayment. This approach will help you maximize the benefits of tapping into your home’s equity.

Real-World Strategies to Access Equity

Accessing equity in your home without refinancing can seem daunting, but several practical strategies can help you tap into this resource. By understanding the available options, you can make more informed financial decisions and utilize your home’s value effectively.

Key Strategies to Access Equity

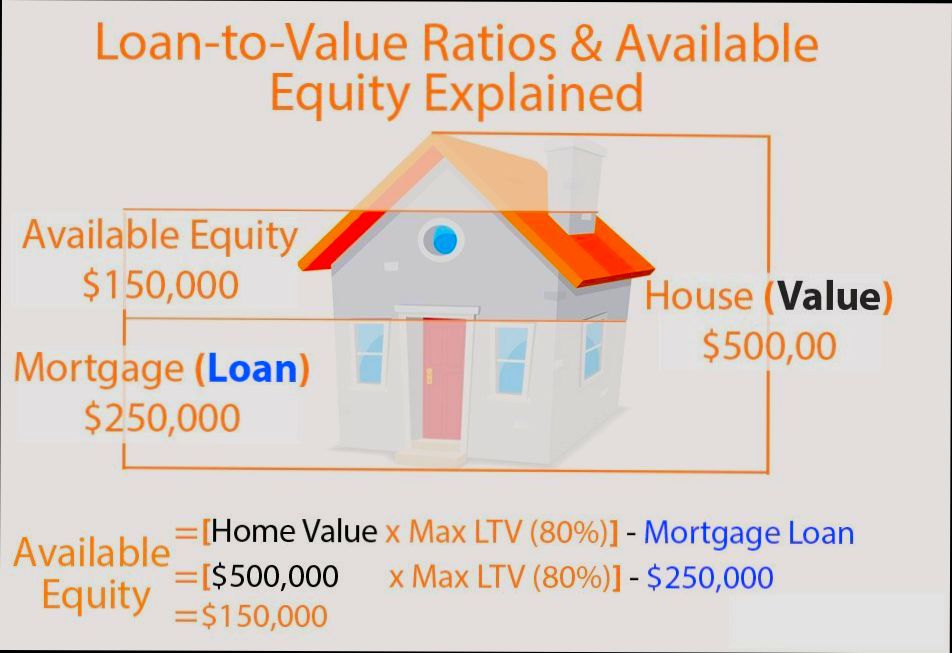

1. Home Equity Loans: These loans allow you to borrow against the equity you’ve built. Typically, you can borrow up to 85% of your home’s appraised value, minus the balance you owe on your mortgage.

2. Home Equity Lines of Credit (HELOC): This option offers revolving credit based on your home’s equity. Notably, most lenders cap this at 80-85% of your home’s appraised value, allowing for flexible withdrawal as needed.

3. Selling Partial Equity: Websites like Unison and Hometap allow you to sell a portion of your home’s equity in exchange for upfront cash. This method doesn’t involve monthly repayments and allows you to keep ownership of your home.

4. Shared Appreciation Mortgages (SAM): With a SAM, a lender gives you below-market mortgage rates in exchange for a percentage of your home’s appreciation when you sell. This can provide immediate cash without increasing your monthly payments.

Here’s a comparative overview of these strategies:

| Strategy | Borrowing Limit | Repayment Terms | Ownership Impact |

|---|---|---|---|

| Home Equity Loan | Up to 85% of home’s value | Fixed monthly payments | Full ownership retained |

| HELOC | Up to 80-85% of home’s value | Flexible monthly withdrawals | Full ownership retained |

| Selling Partial Equity | Varies based on agreement | No monthly repayments | Partial ownership retained |

| Shared Appreciation Mortgage | Below-market rate, contingent on value | Based on appreciation at sale | Full ownership retained |

Real-World Examples

- Hometap Case Study: A family struggling with debt used Hometap to sell 10% of their home’s equity for $40,000. They used the funds to pay off high-interest credit cards, effectively improving their financial situation without monthly repayments.

- Unison Illustration: A homeowner partnered with Unison to access $30,000 as part of a home equity agreement. This allowed them to finance a home renovation that increased their property value significantly, showcasing how leveraging equity can enhance one’s investment.

Practical Implications for Readers

When considering accessing your home equity:

- Assess your current financial needs and decide which option suits you best based on immediate cash flow requirements and long-term goals.

- Research the terms of each alternative thoroughly, as they can vary widely among lenders.

- Engage with a financial advisor or mortgage expert to ensure you fully understand the implications of your chosen strategy.

By leveraging these strategies effectively, you can tap into your home equity without the lengthy process of refinancing, positioning yourself for better financial health. Remember to evaluate each option on how it aligns with your personal financial situation and future objectives.

Analyzing Market Trends for Homeowners

Understanding current market trends is crucial for homeowners looking to access the equity in their homes. By keeping a pulse on the real estate landscape, you can make informed decisions about when and how to leverage your property’s value without refinancing.

Key Market Trends to Monitor

- Home Price Appreciation: According to the National Association of REALTORS® (NAR), recent data shows that home prices have seen an increase of approximately 15% over the past year in certain markets. This appreciation directly reflects the potential equity you can access.

- Supply vs. Demand: The current housing market has experienced a low inventory level, with around 2.5 months of available supply compared to a balanced market’s typical 6 months. This imbalance can drive prices higher, increasing homeowner equity.

- Interest Rates Fluctuation: Despite rising interest rates, which are currently around 6.5% nationally for new mortgages, many homeowners may still find opportunities to access their equity through alternative means.

Comparative Market Data

| Market Factor | Current Trend | Last Year Trend | Projected 6-Month Trend |

|---|---|---|---|

| Home Price Growth | +15% | +8% | +10% |

| Inventory Levels | 2.5 months | 3.5 months | 2.0 months |

| Mortgage Interest Rates | 6.5% | 4.0% | 6.0% |

Real-World Examples

1. Case Study in Austin, TX: A homeowner in Austin saw their property value increase by 20% over the last year due to booming local tech jobs. As a result, they accessed their equity via a home equity loan at a competitive interest rate instead of refinancing.

2. Chicago Neighborhood Insight: Homeowners in specific neighborhoods of Chicago benefitted from rising demand amidst low supply, with some buyers willing to pay up to 10% above asking price. This trend adds value to existing properties, making equity access more viable.

Practical Implications for Homeowners

- Timing is Everything: When monitoring market trends, pay close attention to local events, economic shifts, and seasonal fluctuations that can affect home values.

- Data-Driven Decisions: Utilize housing statistics available from resources like NAR to analyze trends specific to your neighborhood. This can guide you in timing your equity extraction better.

- Consult with Experts: Connecting with real estate professionals can provide personalized market insights, ensuring you understand how macro trends affect your home’s value.

Actionable Insights

- Stay Informed: Regularly check housing statistics, including price trends and inventory levels, from reliable sources like the NAR.

- Evaluate Local Conditions: Understand the nuances of your local market to gauge the right moments to access equity.

- Consider Long-Term Projections: While having a current understanding is important, being aware of longer-term projections can inform your decisions on accessing home equity intelligently.

Using Rent-to-Own Agreements for Equity

Rent-to-own agreements are becoming an increasingly popular way to build equity in your home without the need for immediate financing. These arrangements allow you to rent a property with the option to purchase it later, enabling you to gradually build equity as you make payments toward ownership.

Understanding Rent-to-Own Arrangements

1. Initial Agreement: In a rent-to-own setup, you agree to rent a property for a specified period, often 1 to 3 years, while having the option to buy it at a predetermined price.

2. Rent Payments as Equity: A portion of your monthly rent is typically credited toward the purchase price, thus building up your equity over time. This is an appealing feature for renters who may struggle to save for a down payment.

3. Market Advantages: If home values increase during your rental term, you can secure the property at the initial price agreed upon, potentially locking in significant gains.

Benefits of Rent-to-Own for Equity Building

- Equity Accumulation: On average, up to 20% of your monthly rent can be directed toward the purchase price.

- Flexibility in Financing: Rent-to-own gives you the luxury of time, allowing you to improve your credit score or save additional funds for a down payment.

| Feature | Rent-to-Own | Traditional Purchase |

|---|---|---|

| Monthly Payments | Part goes to equity | Down payment required upfront |

| Purchase Price Determination | Fixed at agreement signing | Market value at purchase time |

| Duration of Agreement | 1-3 years | Immediate purchase |

| Financial Flexibility | Build credit/improve finances | Pressure to secure financing immediately |

Real-World Examples

Consider the case of Jessica, who entered a rent-to-own agreement on a $250,000 home. She agrees to pay $1,500 a month, with $300 allocated toward the home’s purchase price. Over three years, she builds $10,800 in equity, which is essential as she plans for her future financial options.

Another example is Mike, who opted for a rent-to-own deal instead of traditional renting. After two years, he was able to secure a loan for the remaining purchase price, leveraging the equity he had built during this period. He ended up purchasing the home for $240,000 despite the rising market values, making a significant saving while also improving his credit score.

Practical Considerations

- Contract Terms: Always review the contract thoroughly. Understand how much of your rent goes toward the purchase and whether there are any additional administrative fees.

- Market Assessment: Regularly assess home values in your area. If prices continue to rise, moving quickly on the purchase option can yield significant financial benefits.

- Rent-to-Own Timelines: Be clear about the timeframes for both renting and purchasing. Keeping track of these dates can prevent any potential missteps.

Actionable Advice

When considering a rent-to-own agreement, negotiate favorable terms that maximize your equity build-up. Ensure you’re clear on your rights and responsibilities, particularly regarding repairs and maintenance, which can affect the property’s value. By approaching this opportunity strategically, you can effectively leverage rent-to-own agreements as a viable means to build and access equity in your home.

Transforming Renovations into Home Value

When it comes to boosting your home’s equity, strategic renovations can play a pivotal role. By investing wisely in renovations, you can significantly enhance both your living experience and your property’s market value. Let’s dive into how you can transform specific improvements into measurable home value.

Renovation Projects with High Returns

Certain renovations are known to yield impressive returns on investment (ROI), allowing you to increase your home’s worth efficiently. Here are some key projects to consider:

- Kitchen Remodels: Minor kitchen renovations can recoup about 96.1% of their costs, making your kitchen a central hub for boosting value.

- Bathroom Updates: A typical bathroom remodel can return around 60–70% of the investment, especially if you focus on modern fixtures and appealing layouts.

- Flooring Enhancements: Refinishing wood floors stands out with a remarkable ROI of 147%, transforming the aesthetic while significantly increasing value.

- Energy-Efficient Installations: Integrating energy-efficient appliances can not only reduce long-term costs but may also appeal to eco-conscious buyers.

Comparative Table of ROI for Renovation Projects

| Renovation Project | Average ROI (%) |

|---|---|

| Minor kitchen remodel | 96.1% |

| Bathroom remodels | 60–70% |

| Refinishing wood floors | 147% |

| Energy-efficient upgrades | Varies widely |

Real-World Examples

Consider homeowners who opted for a minor kitchen remodel, including modern cabinetry and durable quartz countertops. Not only did they enjoy an updated space for daily cooking, but when it was time to sell, they recouped nearly all of their renovation costs, illustrating a smart investment decision.

Another example includes homeowners choosing to finish their basements. By creating inviting family rooms or guest suites, they expanded their usable space, which is often reflected in higher market values. Properties with more livable square footage can fetch better prices, making this a valuable transformation.

Practical Implications for Homeowners

As you plan your renovations, focus on two main points:

- Invest in Livability: Prioritize updates that enhance daily comfort and functionality, such as dual vanities in bathrooms or walk-in showers that appeal to modern buyers.

- Think Long-Term: Remember that some renovations may take time to pay off, particularly those that involve significant energy efficiency improvements. However, over time, they can lead to lower utility bills and a more attractive property.

Actionable Advice

Instead of embarking on costly renovations without research, start by assessing your home’s existing value and potential market trends. Use this knowledge to direct your renovation budget toward projects that align with buyer preferences and current trends. Simple actions, like improving curb appeal with updated exterior features or landscaping, can also yield quick returns without heavy investment.