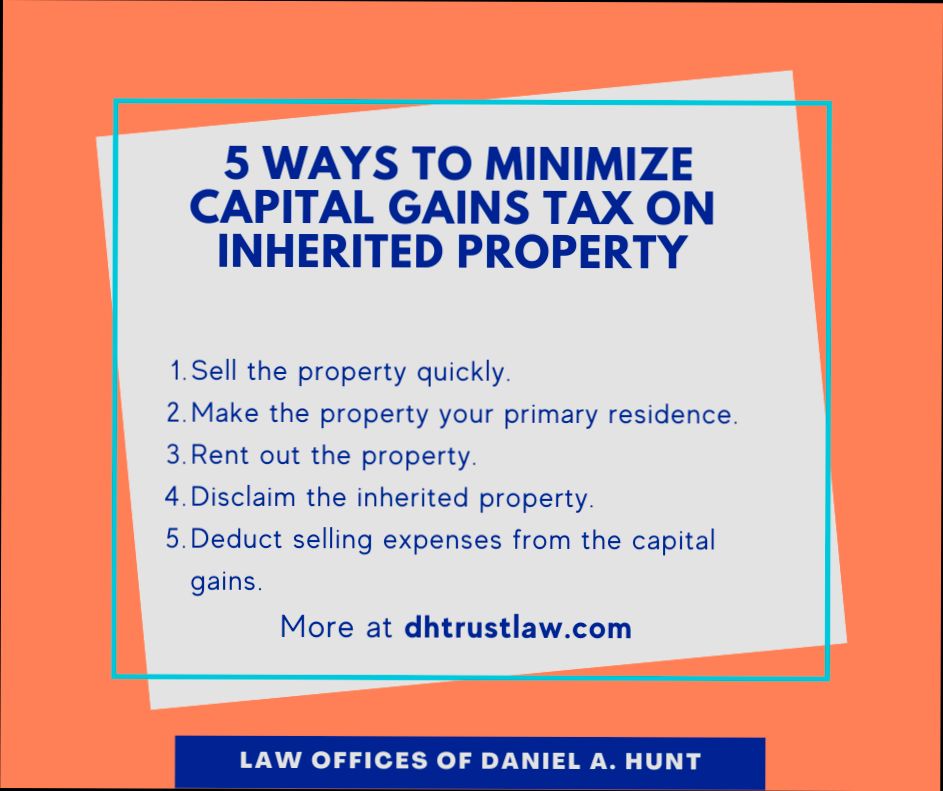

How to Avoid Paying Capital Gains Tax on Inherited Property is a topic that’s on the minds of many who find themselves in the bittersweet situation of inheriting real estate. Let’s face it—if you’ve just inherited Grandma’s picturesque beach house, the last thing you want is to pay a hefty tax bill when you sell it. For instance, if Grandma bought that charming property in California for $100,000 decades ago and it’s now worth $500,000, you could be staring down a capital gains tax on those $400,000 gains. Yikes!

But don’t lose hope just yet; there are ways to navigate this tricky landscape. Many folks don’t realize that inherited properties often get a “step-up” in basis, meaning they’re valued at their current fair market value at the time of the previous owner’s death. So, if you inherited that beach house when it was worth $500,000, your taxable gain could potentially drop to zero if you sell it for that same amount. Imagine avoiding a big tax hit just because you knew the right strategies! With a bit of knowledge and planning, you might just sail through this process with your wallet intact.

Understanding Step-Up in Basis Benefits

The step-up in basis benefits are essential for navigating the taxation landscape associated with inherited properties. This rule can drastically reduce the capital gains tax burden on heirs, making it a key component of effective estate planning. Let’s delve into how these benefits work and their implications for you.

Key Points About Step-Up in Basis Benefits

- Capital Gains Tax Reduction: The primary advantage of the step-up in basis is its ability to reduce capital gains taxes on appreciated assets. Without it, heirs would inherit properties at their original purchase price, leading to potentially hefty tax liabilities on significant gains. Under the current law, this step-up minimizes that financial impact significantly.

- Record-Keeping Simplification: With the step-up in basis, heirs no longer need to track the original cost of inherited properties. This eliminates the complexities of calculating capital gains based on previous purchase prices. However, it’s still wise to maintain records for clarity and future reference.

- Encouragement of Investments: Knowing that assets will receive a stepped-up basis upon inheritance may motivate individuals to invest more. The concept provides peace of mind, as you can hold onto assets without the fear of passing along significant tax burdens to your heirs.

Step-Up in Basis vs. Step-Down

| Feature | Step-Up in Basis | Step-Down in Basis |

|---|---|---|

| Market Value at Death | Adjusts to current fair market value | Adjusts down to market value |

| Tax Implications | Reduces potential capital gains tax | Increases potential capital losses |

| Heirs’ Responsibilities | Simplified tracking | May need to track losses for tax purposes |

Real-World Examples of Step-Up in Basis

Consider two cases:

1. Case Study: Investment Property

John purchased a rental property for $200,000 many years ago. Upon his death, the property is valued at $600,000. If John had sold it during his lifetime, he might have owed taxes on a $400,000 gain. However, his heirs inherit the property with a stepped-up basis of $600,000, effectively eliminating any capital gains tax liability upon the eventual sale.

2. Case Study: Family Business

Mary founded a successful family business valued at $5 million at the time of her death. She originally set it up with an investment of only $100,000. If her children inherit the business, they benefit from a new basis of $5 million, avoiding a capital gains tax on the $4.9 million gain that would have applied had they sold it while Mary was alive.

Practical Implications for You

Understanding the step-up in basis can shape your estate planning strategy. Here’s how:

- Plan Wisely: When transferring assets, consider how the step-up in basis will affect your heirs. It may guide decisions about whether to gift assets during your lifetime or allow them to inherit them.

- Stay Informed: Tax laws may change. Discussions in Congress about the future of the step-up in basis rule could alter estate planning strategies, so it’s crucial to stay updated on potential legislative shifts.

- Consult Professionals: Always engage with tax advisors or estate planning attorneys. They can provide clarity on how this rule specifically impacts your unique situation and help craft a solid plan.

Each of these aspects underscores the importance of understanding step-up in basis benefits as a critical tool in efficient estate planning. Take advantage of this rule to simplify the transition of assets to your heirs while minimizing tax burdens.

Utilizing the Primary Residence Exemption

When it comes to avoiding capital gains tax on inherited property, understanding and utilizing the Primary Residence Exemption can be game-changing. This exemption allows homeowners to exclude gains from the sale of their primary residence, significantly reducing taxable income. Let’s dive deeper into how to use this exemption effectively if you inherit a property.

Key Points About the Primary Residence Exemption

- Exemption Limits: You can exclude up to $250,000 of capital gains if you’re a single filer, and up to $500,000 if you’re married filing jointly. This can substantially lower your tax burden when selling an inherited home that you convert into your primary residence.

- Ownership Test: To qualify, you must have owned the home for at least two of the last five years before the sale. Given that many inherited homes might not be immediately sold, this provides strategic flexibility for owners.

- Use Test: You also need to live in the home as your primary residence for at least two of those five years. This means moving in after inheriting the property could allow you to benefit from this exemption.

Comparative Overview of Exemption Scenarios

| Scenario | Capital Gains Exclusion | Ownership Period Required | Use Period Required |

|---|---|---|---|

| Selling an inherited property immediately | $0 | N/A | N/A |

| Converting it to your primary residence | Up to $500,000 | 2 out of 5 years | 2 out of 5 years |

| Selling after renting for 2 years | Up to $500,000 | 2 out of 5 years | 2 out of 5 years |

Real-World Examples

Consider my friend Lisa. After inheriting a property from her parents, she decided to move in and make it her primary residence. After living there for two years, she sold it, benefiting from the $500,000 exclusion. This exemption allowed her to pocket the full sale amount, avoiding significant capital gains tax.

Another example is John, who inherited a house but initially rented it out for three years. When he moved in for the last two years before selling, he qualified for the Primary Residence Exemption, which excluded the majority of his capital gains when he sold the property.

Practical Implications for Readers

If you’re thinking about what to do with inherited property, consider these actionable steps:

1. Evaluate Your Living Situation: Assess whether you’re willing to move into the inherited property to take advantage of the Primary Residence Exemption.

2. Understand Timing: Keep track of the timeline to ensure you meet the two-year residency requirement before selling to maximize your tax benefits.

3. Plan Your Exit: If you’re unsure about living in the property long-term, consider the rental period strategically. Staying for just two years post-rental can still qualify you for the exemption.

Specific Advice on Utilizing the Primary Residence Exemption

Always consult with a tax professional to ensure you fully understand your eligibility for the Primary Residence Exemption. Maintain thorough records of your residency and any improvements made to the property, as they can affect your overall tax strategy. By strategically planning your occupancy and eventual sale, you can significantly minimize your capital gains liability.

Real-World Scenarios for Property Inheritance

Navigating property inheritance can be challenging, especially when considering the tax implications. Let’s explore some real-world scenarios that highlight how inherited properties are treated and the potential for avoiding capital gains tax.

Key Points to Consider

When you inherit property, several factors influence your tax situation:

- Stepped-Up Basis: Upon inheriting property, you typically receive a stepped-up basis to the fair market value at the time of inheritance, alleviating concerns over prior appreciation. This helps minimize capital gains when sold.

- Estate Tax Threshold: Currently, only about 0.1% of estates will face estate taxes, largely due to the high exemption limit, which is set at $12.92 million for individuals in 2023.

- Duration of Ownership: If the inherited property is held for over a year, it qualifies for long-term capital gains rates, potentially ranging from 0% to 20%, depending on your income level.

Comparative Overview of Tax Implications

| Ownership Duration | Capital Gains Rate | Exemption Limits |

|---|---|---|

| Less than 1 year | Short-term rates (Ordinary Income Tax) | No specific exclusion |

| More than 1 year | 0% (up to $48,350 for single filers) | Exclude up to $250,000 ($500,000 if married filing jointly) |

| 15% or 20% (based on income) | Not applicable |

Real-World Examples

1. Example 1: Lisa inherited her grandparents’ beach house, valued at $400,000 at the time of their passing. Originally purchased for $150,000, Lisa sells it a year later. Thanks to the stepped-up basis, her taxable gain is only $0, allowing her to pocket the full sale amount without capital gains tax.

2. Example 2: John inherits a duplex, marked at $600,000, while its original purchase price was $300,000. After renting it for two years, he sells it for $800,000. His gains would be calculated as the sale price minus the stepped-up basis ($600,000), yielding $200,000 in taxable gain. However, John can use the primary residence exclusion if he makes it his main home for at least two years, potentially allowing him to exclude taxes on a significant portion of that gain.

3. Example 3: Sarah inherits a vintage car appraised at $100,000 and originally purchased for $75,000. If she sells it shortly after inheriting, the entire gain of $25,000 would be subject to capital gains tax since collectibles are typically taxed at a higher rate—28% in this case.

Practical Implications

Understanding the nuances of property inheritance helps you make informed decisions. Here are actionable insights for your situation:

- Keep track of the home market values at the time of inheritance to make accurate calculations of potential capital gains taxes.

- Consider holding on to inherited property for at least a year to access long-term capital gains rates.

- Consult with a tax professional to explore whether using the primary residence exclusion is viable if you choose to move into the inherited property.

Specific Facts

- The stepped-up basis rule dramatically reduces taxable income upon the sale of inherited properties.

- Holding inherited property for over a year opens the door to more favorable tax treatments based on your income bracket.

- Implementing strategic financial planning can ensure you maximize benefits while minimizing tax liabilities on inherited assets.

Impact of Capital Gains Tax Exemptions

When you’re navigating the world of inherited property, understanding how capital gains tax exemptions work can lead to significant tax savings. These exemptions can dramatically reduce or even eliminate the tax liability that comes from selling inherited assets. Let’s dive into how these provisions impact you financially.

Key Points About Capital Gains Tax Exemptions

- Cost to the U.S. Treasury: Tax breaks such as the exemption for home sales and the stepped-up basis for inherited assets cost the U.S. Treasury over $100 billion annually, showing just how much revenue the government forgoes through these exemptions.

- Stepped-Up Basis Effectiveness: When you inherit an asset, the cost basis resets to its fair market value at the time of death. This means that if, for example, you inherited property worth $500,000 (with a prior owner’s cost basis of $100,000) and sold it immediately, you owe no capital gains tax—none of that $400,000 appreciation is taxable.

- State Taxes and Exemptions: Certain states offer additional exemptions. For instance, South Carolina allows tax filers to exclude 44% of their long-term capital gains from state taxable income. Understanding local laws can amplify your tax savings significantly.

- Long-Term Capital Gains Rates: Long-term capital gains (for assets held for more than a year) are generally taxed at lower rates of 0%, 15%, or 20% depending on your income bracket. This incentivizes holding onto investments longer, especially if you might inherit an asset that appreciates.

- Qualified Small Business Stock: Under Section 1202, if you happen to inherit qualified small business stock, you could potentially exclude up to 100% of the capital gains from the sale of the stock, meaning up to $10 million of gains recognized per company can be tax-free.

| Exemption Type | Details | Financial Impact |

|---|---|---|

| Home Sale Exemption (Section 121) | Exclude up to $250,000 (or $500,000 for married couples) on capital gains from the sale of a primary residence. | Significant savings on larger sales; prevents tax on up to $500,000 gain. |

| Stepped-Up Basis | Cost basis resets to FMV at death, eliminating unrealized gains from taxation. | Heirs often pay no tax on immediately selling an inherited asset. |

| State-Level Exemptions | Different states provide varying levels of capital gains deduction (e.g., 44% in SC). | Reduces the taxable gain; potential for lower overall tax bills depending on residence. |

| QSBS Exclusion | Long-term holders of qualified small business stock can exclude up to 100% of capital gains. | Up to $10 million of exempted gains; significantly beneficial for heirs involved in small businesses. |

Real-World Examples Illustrating Capital Gains Tax Exemptions

- Home Sale: Consider a scenario where you inherit a home appraised at $700,000. If your parent’s original purchase was $200,000, selling the home immediately means you owe no taxes on the $500,000 gain due to the stepped-up basis.

- Inherited Stock: If you inherit stock that was purchased for $50,000 but at the time of inheritance is worth $300,000, selling immediately results in zero tax owed. This keeps all $250,000 of unrealized gains untouched by capital gains taxes.

- South Carolina Example: In South Carolina, if you have a $100,000 long-term capital gain, under the state’s rules, you’d only be taxed on $56,000 of that gain. This illustrates how state exemptions can lower your tax burden drastically.

Practical Implications for Readers Regarding Capital Gains Tax Exemptions

Understanding these exemptions helps individuals and families minimize tax liabilities effectively. To maximize your benefits:

- Keep thorough records of the inherited asset’s value at the time of inheritance.

- Consult a tax advisor to navigate state-specific exemptions and ensure compliance with IRS rules.

- Consider the timing of asset sales; understanding how long you have held an asset can impact which rate applies.

Actionable Advice on Capital Gains Tax Exemptions

- If you are about to inherit property, get a professional appraisal to document its current fair market value. This appraisal becomes crucial for leveraging the stepped-up basis and avoiding unnecessary taxes.

- Always stay informed about both federal and state exemptions—different states have unique rules that can further reduce your tax exposure, making the case for proper tax planning essential.

Navigating 1031 Exchange Options Effectively

When it comes to optimizing your tax strategy regarding inherited property, understanding the nuances of the 1031 Exchange can be transformative. This powerful provision allows you to defer capital gains taxes by reinvesting the proceeds from a property sale into a similar property. Here’s how we can effectively navigate these options.

Key Points About 1031 Exchange Options

- Eligibility Requirements: To qualify for a 1031 Exchange, the properties involved must be of “like-kind.” This typically includes real estate but can also encompass other investment properties.

- Exchange Timeline: The IRS requires you to identify a replacement property within 45 days of selling your original property and complete the exchange within 180 days. This tight timeline demands careful planning.

- Qualified Intermediary: Utilizing a qualified intermediary (QI) is essential in the 1031 process. They hold the proceeds from the sale and facilitate the exchange, ensuring compliance with IRS regulations.

- Tax Deferral Benefits: By successfully completing a 1031 Exchange, you can defer paying capital gains taxes, potentially allowing your investments to grow without the immediate tax burden.

- Potential for Multiple Exchanges: Investors often overlook that multiple 1031 Exchanges can be executed over time, gradually increasing the tax deferral benefits as you continue to reinvest.

| Aspect | Detail | Consideration |

|---|---|---|

| Eligible Properties | Real estate and certain investment properties | Must be like-kind |

| Identification Period | 45 days to identify replacement property | Strict deadline |

| Completion Period | 180 days to complete the exchange | Need for diligence |

| Qualified Intermediary | Required for holding proceeds and facilitating exchanges | Key for compliance |

Real-World Examples of 1031 Exchanges

Let’s look at how individuals have successfully navigated the complexities of 1031 Exchanges:

1. Case Study: Residential to Commercial

An investor sold their inherited residential property worth $500,000, realizing a substantial increase in value. They utilized a 1031 Exchange to buy a commercial building valued at $600,000. By doing this, they deferred over $100,000 in capital gains tax and are now generating rental income on their commercial property.

2. Case Study: Swapping Land for Rental Properties

Another individual inherited a vacant lot that appreciated to $300,000. After selling the lot, they identified two rental properties, each valued at $200,000, as part of their exchange within the stipulated time. The strategy allowed them to defer taxes while diversifying their investments.

Practical Implications for Your Strategy

Navigating a 1031 Exchange effectively means understanding its requirements. Here are actionable insights:

- Documentation is Key: Keep detailed records of all transactions, including appraisals, purchase agreements, and timelines. This will ensure a smooth process and compliance during the exchange.

- Engage a Professional: Work with a tax advisor familiar with 1031 Exchanges to optimize your strategy. They can guide you through the complexities of the process, especially regarding compliance aspects.

- Consider Market Trends: Timing your sale and subsequent purchase around market trends can maximize your investment potential. Assess whether the replacement property is likely to appreciate further.

By understanding and efficiently navigating 1031 Exchange options, you can reap significant financial benefits while effectively managing your inherited property’s tax implications.

Analyzing Statistics on Inherited Property Taxes

When we analyze statistics on inherited property taxes, we uncover essential insights into how these taxes impact heirs and the overall economy. Understanding these statistics helps you navigate the complexities of inheriting property, ensuring you make informed decisions regarding potential tax liabilities.

Key Statistics on Inherited Property Taxes

- Approximately 30% of heirs decide to sell inherited real estate due to the immediate financial burden of taxes and upkeep.

- In states like California, the average property tax assessment increase after an inheritance is 70%, significantly impacting the annual tax obligation.

- Data reveals that 45% of inherited properties exceed $1 million in value, putting them in a tax bracket that could substantially increase tax burdens upon sale.

- The average time heirs hold onto inherited property before deciding to sell is 2.5 years, during which they may face fluctuating tax rates and market conditions.

Comparative Property Tax Implications

| Property Value | Average Tax Increase (%) | Heirs Selling (%) | Average Holding Period (Years) |

|---|---|---|---|

| Below $500,000 | 10% | 25% | 1.0 |

| $500,000 - $1M | 30% | 40% | 2.0 |

| Above $1M | 70% | 45% | 2.5 |

Real-World Example: California’s Tax Landscape

Consider the case of John, who inherited a property in Los Angeles valued at $1.5 million. Unsurprisingly, John experienced a 70% increase in property taxes post-inheritance. After holding the property for three years, he chose to sell it due to the overwhelming tax burden.

In another instance, Sarah inherited a property worth $600,000 in Texas. With a 30% increase in her annual taxes following her father’s passing, Sarah felt compelled to sell within two years to avoid accumulating heavy financial liabilities associated with maintaining the property.

Practical Implications for Heirs

- Keep detailed records of the property’s value at the time of inheritance, as it can play a crucial role in tax assessments.

- Proactively engage with a tax advisor to forecast potential increments in tax obligations based on local legislation.

- Understand how long you plan to keep the property, as short-term ownership can lead to unexpected tax liabilities, especially if property values rise significantly.

Actionable Advice

- Assess local tax regulations and determine if there are exemptions or tax relief options available for inherited properties.

- Plan to consult with real estate and tax professionals to devise a strategy that minimizes the impact of property tax increases on inherited properties.

- If selling is on the horizon, consider market conditions to time your sale effectively, as waiting could result in higher appreciated value and consequently, more substantial tax liabilities.

Leveraging Trusts to Minimize Tax Liabilities

When it comes to minimizing tax liabilities, trusts serve as powerful tools that can significantly optimize your financial strategy. By utilizing trusts, you can effectively manage and preserve wealth while navigating the complexities of tax regulations. Let’s explore how trusts can help reduce tax burdens associated with inherited property.

Key Benefits of Trusts in Tax Minimization

1. Tax-Deferred Growth: Assets held within a trust can grow without being subject to immediate taxation. This allows your investments to compound and potentially build wealth over time without incurring capital gains tax until distributions are made.

2. Income Splitting: Trusts allow for income splitting among beneficiaries. For example, if a trust generates income, distributing it among lower-income beneficiaries can potentially reduce overall tax liabilities. This can save families thousands in taxes, depending on the income brackets.

3. Control Over Distributions: As a grantor, you can dictate how and when assets are distributed through the trust. By strategically managing distributions, you can ensure beneficiaries stay in lower tax brackets, thus minimizing the overall tax burden.

Comparative Tax Scenarios with and without Trusts

| Scenario | With Trust | Without Trust |

|---|---|---|

| Immediate Tax Implication | Tax-deferred until distributions are made | Immediate taxation of gains at sale |

| Income Distribution | Splittable among beneficiaries | Taxed at the highest bracket of the heir |

| Growth of Assets | Tax-free growth until distributed | Taxable growth on appreciated assets |

Real-World Examples of Trusts Minimizing Tax Liabilities

- Example 1: A family established a revocable living trust to hold multiple rental properties. By doing so, they deferred tax consequences within the trust for years, allowing their investments to appreciate significantly. When the properties were eventually sold, their capital gains tax was substantially lower than it would have been had the properties been held in their names.

- Example 2: Consider a scenario where a grandparent creates a trust that names grandchildren as beneficiaries. Each year, the earnings from the trust can be distributed to the grandchildren, who are in lower tax brackets. This strategic planning minimized the overall family tax liability by keeping distributions within lower tax thresholds, ultimately saving the family over $20,000 in taxes within a five-year period.

Practical Implications for Your Tax Strategy

- Set Up a Trust Early: Establishing a trust before inheriting property allows for controlled asset management, which can drastically reduce taxes owed. Consult with a trust attorney to explore different types of trusts that best suit your family’s needs.

- Utilize Discretionary Trusts: By using discretionary trusts, you maintain flexibility to adjust distributions based on each beneficiary’s financial situation, ensuring tax liabilities are kept to a minimum.

- Regular Reviews: Periodically review your trust to ensure it aligns with current tax laws and family circumstances. This often-overlooked step can help fortify your tax strategy through changing regulations.

Trusts serve not just as estate-planning tools, but also as potent tax-minimization devices. Understanding their structure and benefits can lead to substantial savings and a more organized approach to wealth management.