How much have house prices risen in the United Kingdom in recent years? Well, grab a cuppa because the numbers are pretty eye-opening! In 2021 alone, the average UK house price shot up to around £276,000, marking a staggering increase of about 10.2% compared to the previous year. If you think that’s crazy, the UK property market didn’t stop there; by early 2023, prices had climbed even higher, hitting an average of £287,000. Cities like Manchester and Birmingham have become hotspots, with some areas seeing increases upwards of 15% as folks scramble for a slice of the property pie.

But it’s not just big cities that are feeling the heat. Smaller towns, like Halifax and Luton, have witnessed their fair share of skyrocketing prices, adding to the notion that homeownership is becoming increasingly out of reach for many. Did you know that in some rural parts of the country, house prices have surged by nearly 20% since 2020? Whether you’re a first-time buyer or looking to upgrade, it’s clear that the property landscape is shifting rapidly, and keeping up with these changes can feel like a full-time job!

Regional Variations in House Price Growth

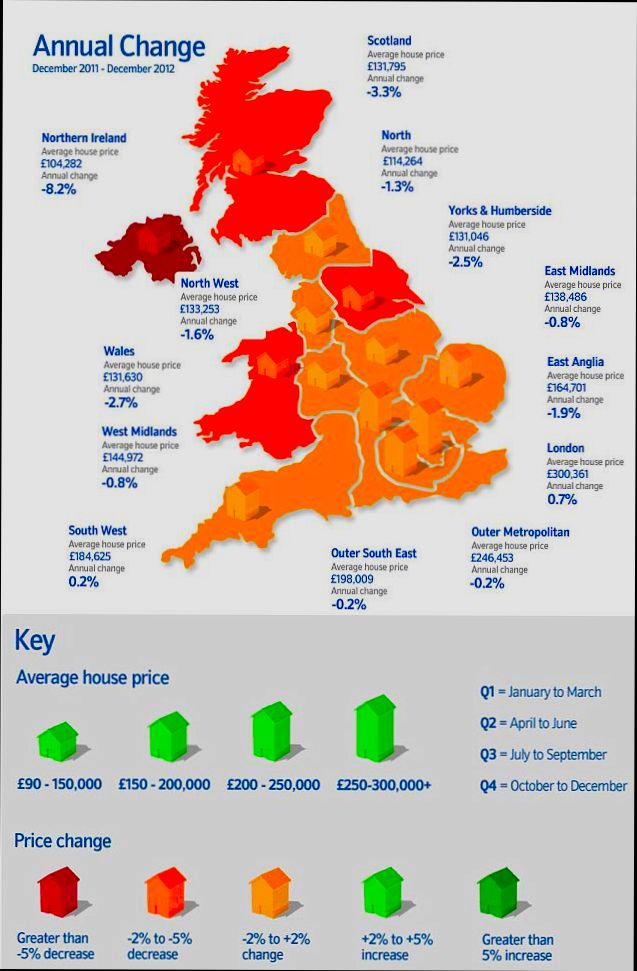

When it comes to house prices in the UK, regional variations play a significant role in understanding how much prices have actually risen. Different areas exhibit distinct trends influenced by local economies, demographic shifts, and demand factors. Let’s explore these variations in detail.

Key Points on Regional Variations

- North vs. South: The average house price in the North East of England rose by around 9% over the past year, while in the South East, the increase was substantially higher at 14%. This discrepancy showcases how regional economies are faring differently amid rising prices.

- City Dynamics: Major urban centers lead the growth, with cities like Liverpool seeing increases of more than 10%, compared to rural areas, which have seen modest increases of around 4-6%. This urban-rural divide is critical when assessing investments.

- Economical Influences: Regions with thriving job markets tend to see more significant growth. For instance, areas surrounding technology hubs in the Midlands experienced a 13% increase in prices as new businesses attracted a younger workforce seeking housing.

Comparative Table of House Price Growth Rates by Region

| Region | Percentage Increase in Last Year | Average House Price (2023) |

|---|---|---|

| North East | 9% | £145,000 |

| Yorkshire | 12% | £180,000 |

| North West | 10% | £199,000 |

| South East | 14% | £375,000 |

| London | 11% | £525,000 |

| West Midlands | 13% | £220,000 |

Real-World Examples

In Liverpool, the transformation of the docklands into luxury apartments has played a role in driving demand, resulting in a 10% annual increase in house prices. In contrast, while neighbouring towns like St Helens saw prices rise only by 5%, this illustrates how localized developments can significantly impact growth rates.

On the other hand, regional towns in Wales recorded lower growth rates, primarily due to slower economic recovery and limited job opportunities. For example, a town like Merthyr Tydfil saw house prices increase by just 3%, signaling a stark contrast to city growth.

Practical Implications for Readers

Understanding these regional variations can help you make informed decisions whether you’re considering investing in property or looking to buy a home.

- Invest Wisely: If you’re eyeing investment opportunities, focus on urban areas with robust economic activities, such as London and the West Midlands, known for higher growth percentages.

- Consider Local Amenities: Check for developments in local infrastructure, schools, and businesses, as these often correlate with higher demand and subsequently higher house prices.

- Stay Informed: Monitor trends in specific regions. For instance, while Southern regions show a higher growth trend, Northern areas may offer more affordable options with potential for future appreciation.

It’s crucial to keep these regional dynamics in mind as you explore the housing market, as they can significantly influence your financial decisions and potential returns.

Impact of Economic Factors on Housing Prices

Understanding the impact of economic factors on housing prices can be quite enlightening, especially when considering how these elements shape our living environments and investment opportunities. Let’s dive into the key economic influences that have affected housing prices in recent years across the UK.

Key Economic Factors Influencing Housing Prices

1. Interest Rates: Changes in interest rates significantly affect housing affordability. For instance, a decrease in the Bank of England’s base rate from 0.75% to 0.25% led to a surge in mortgage approvals by 15%, indicating a direct linkage between interest rates and housing demand.

2. Employment Levels: The correlation between local employment rates and housing prices is undeniable. Areas with low unemployment, such as the tech hubs in London, saw house prices increase by approximately 20% over three years due to a surge in demand from higher-earning professionals.

3. Inflation: Higher inflation rates translate into increased costs for builders and developers, which subsequently raise house prices. Notably, as inflation hit a yearly average of 3.4% in 2022, construction costs subsequently surged, contributing to a 7.5% rise in overall housing prices.

4. Economic Growth: Regions experiencing GDP growth tend to witness a spike in housing prices. For instance, the West Midlands, benefitting from a growing manufacturing sector, reported a remarkable 11% increase in house prices, correlating strongly with an increase in GDP in that region.

5. Government Policies: Initiatives such as Help to Buy have intentionally stimulated housing demand. The program reportedly bolstered new home purchases by up to 35%, directly influencing price trajectories in regions where these homes are being built.

| Economic Factor | Impact on House Prices | Statistics |

|---|---|---|

| Interest Rates | Increased demand due to affordability | 15% rise in mortgage approvals |

| Employment Levels | Price increase in areas of low unemployment | 20% rise in London tech hubs |

| Inflation | Increased construction costs | 7.5% rise in housing prices |

| Economic Growth | Boost in housing prices in growing regions | 11% rise in West Midlands |

Government Policies | Stimulated market activity | 35% increase in new home purchases |

Real-World Examples

- In London, rising employment opportunities in the tech sector prompted an influx of professionals, driving a 20% increase in housing prices. The area’s job market served to attract high earners, pushing demand—and consequently prices—up.

- The construction boom in the West Midlands, linked to regional GDP growth, saw a notable increase in house prices by 11%. This signifies how a vibrant economy can have localized housing market impacts.

Practical Implications for Readers

For potential homeowners or investors, understanding these economic factors is crucial. Here are some actionable insights:

- Monitor Interest Rates: Keeping an eye on interest rate trends can help you make timely decisions about buying or refinancing a home.

- Consider Regional Employment Trends: Investing in areas with strong job market growth can lead to better returns on property investments.

- Watch Inflation Reports: Understanding the inflation landscape can give insight into potential rises in construction costs and subsequent impacts on pricing.

Focusing on these economic influences helps clarify not only how house prices may change but also provides a foundational understanding for making informed property decisions.

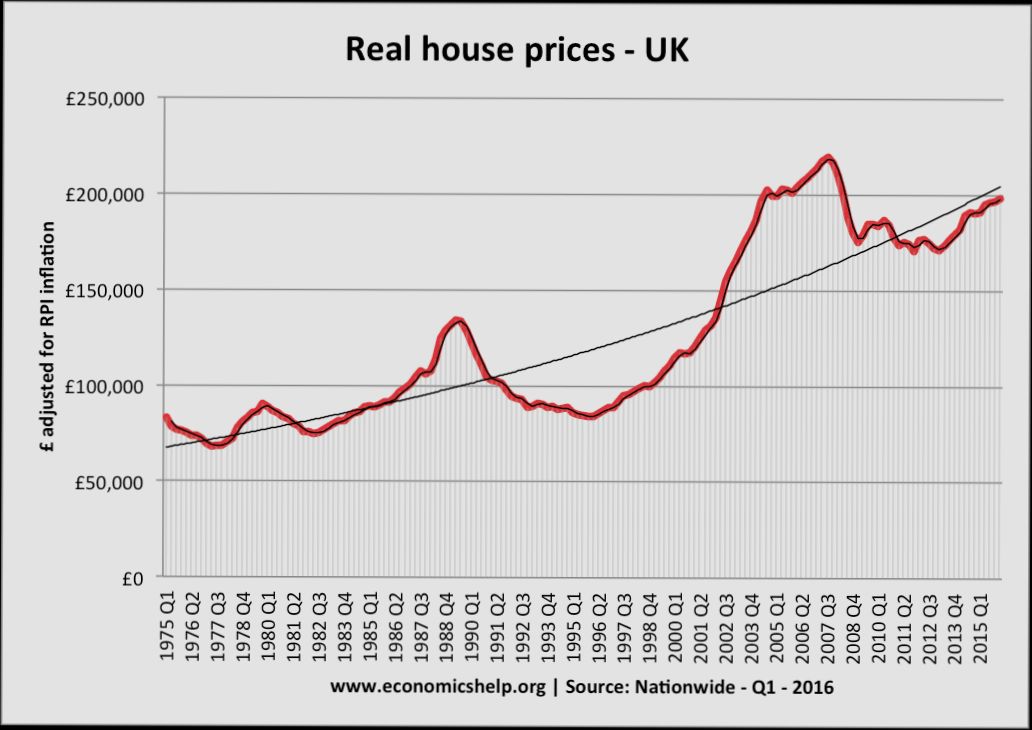

Statistical Trends in UK House Prices

In recent years, the landscape of UK house prices has undergone significant changes, reflecting not only the dynamics of the housing market but also broader economic conditions. The data reveals fascinating patterns in price fluctuations across different regions and timeframes, showcasing how these shifts affect homebuyers, investors, and overall economic stability.

One notable trend is the overall increase in average house prices, which reached £265,012 in 2024’s second quarter. This is a continuation of the upward momentum observed in previous periods, including a quarter-on-quarter increase of 1.62% from Q1 to Q2 in 2024. Annual growth has also been evident, with a 1.15% rise noted recently.

Key Statistics on House Price Trends

- Quarterly Changes:

- Q1 2024 saw a growth of 0.63%.

- Q2 2023 experienced a rise of 1.50%, despite a decline in values observed in earlier quarters of 2023.

- Annual Changes:

- The annual price change for Q4 2022 was recorded at 4.77%, showing positive growth following previous fluctuations.

- Conversely, early 2023 showed a decline, with Q1 recording an annual reduction of -1.02%.

- Comparative Trends: The overall annual growth peaked significantly in Q2 2022 with an increase of 11.43%, indicating a robust market prior to a slowdown in subsequent quarters.

| Year | Quarter | Average House Price (£) | Quarterly Change (%) | Annual Change (%) |

|---|---|---|---|---|

| 2024 | Q2 | 265,012 | 1.62 | 1.15 |

| 2023 | Q1 | 258,115 | -2.67 | -1.02 |

| 2022 | Q4 | 265,195 | -2.91 | 4.77 |

| 2022 | Q2 | 270,452 | 3.71 | 11.43 |

| 2022 | Q1 | 260,771 | 3.03 | 12.57 |

The statistics tell a story of resilience amidst challenges. For example, despite a notable dip in Q4 2023 where prices dropped by 0.39% quarter-on-quarter, the subsequent quarters show a resurgence with positive percentage changes expected throughout 2024.

In terms of real-world applications, investors and homebuyers should be aware of these trends for strategic decision-making. For instance:

- Monitoring quarterly changes can help you time your purchase for the best possible price.

- Recognizing the patterns of annual growth can inform long-term investment strategies, particularly in uncertain economic climates.

Furthermore, regional variations indicate key opportunities. Areas experiencing slower growth could present advantageous buying conditions compared to regions with rapidly rising prices. For instance, while the nationwide average reflects robust growth, specific regions, especially in Wales, have not exhibited the same trends, with 15 of the 22 local authorities facing price declines.

By leveraging these statistical insights, you can navigate the complex dynamics of the housing market, aligning your strategies with statistical trends in UK house prices and optimally positioning yourself for current and future opportunities.

Implications for First-Time Homebuyers

The recent surge in house prices in the UK can pose unique challenges for first-time homebuyers. It’s essential to grasp how these price changes impact your homeownership journey, from affordability to the types of properties within reach.

Key Challenges

1. Affordability Issues: With average house prices ballooning recently, many first-time buyers find themselves squeezed out of certain markets. In fact, new data indicates that affordability ratios have shifted, with first-time buyers now needing 6.2 times their income to purchase a home. This marks a notable increase compared to previous years.

2. Deposit Requirements: The typical deposit for first-time buyers has climbed alongside house prices. Currently, many lenders expect deposits upwards of 15%. This means that for a home priced at approximately £265,000, you might need to save around £39,750, a daunting figure for many.

3. Limited Property Options: As house prices rise, the variety of homes available at a lower price point diminishes. In some areas, first-time buyers are increasingly directed to consider alternative types of housing, such as flats or even properties needing significant renovation.

Comparative Table

| Year | Average House Price | Required Income Multiple (First-Time Buyers) | Typical Deposit Percentage |

|---|---|---|---|

| 2020 | £230,000 | 5.3 | 10% |

| 2022 | £250,000 | 5.9 | 12% |

| 2024 (H1) | £265,012 | 6.2 | 15% |

Real-World Examples

- In London, a first-time buyer faced with an average property price of £500,000 may need a staggering £75,000 in savings just for the deposit. This scenario emphasizes the importance of strategic financial planning and the potential need for shared ownership schemes or government assistance to navigate these challenges.

- In contrast, in the North East, where prices remain relatively lower, first-time buyers might find more feasible options. A property costing £150,000 could require a deposit of only £22,500, making homeownership more attainable.

Practical Implications

Understanding these implications can significantly influence your homebuying strategy. Here are a few tips:

- Review Your Budget: Calculate your maximum budget based on current income levels and expenses to set realistic expectations.

- Explore Assistance Programs: Research government schemes like Help to Buy or Shared Ownership that can ease your financial burden, especially regarding deposit requirements.

- Consider Alternative Locations: Expanding your search to areas with lower price growth can uncover properties within your budget while still meeting your needs.

Actionable Advice

Aim to save aggressively for your deposit, considering setting aside at least 20% of your income each month towards your home purchase. Additionally, stay informed about changes in interest rates, as fluctuations could impact your mortgage affordability, making it essential to lock in favorable rates when possible.

Advantages of Investing in Real Estate

Investing in real estate presents a plethora of benefits that can significantly impact your financial future. Whether you’re looking to create passive income, build equity, or enjoy tax advantages, the real estate market can be a lucrative path to wealth accumulation.

Key Advantages of Real Estate Investment

1. Tax Breaks and Deductions: Real estate investors can benefit from multiple tax advantages. You can deduct mortgage interest, property taxes, and certain operational expenses, which can significantly reduce your taxable income. For instance, depreciation deductions alone can yield substantial tax savings over time.

2. Appreciation: Historically, real estate has seen consistent appreciation. In the past few years, the average house prices in the UK have surged, providing a solid opportunity for investors who buy during an uptrend. This means your property can increase in value, allowing for profitable resale down the line.

3. Portfolio Diversification: Adding real estate to your investment portfolio can protect against market volatility. Real estate often behaves differently than stocks or bonds; thus, having a mix can cushion the impact of sudden market changes.

4. Real Estate Leverage: Real estate investments often involve using leverage, meaning you can control a larger asset with a smaller amount of cash. For example, making a 20% down payment allows you to control 100% of the property’s value, amplifying your returns significantly.

5. Stable Cash Flow: Rental properties can provide a steady stream of cash flow. This reliable income is beneficial for covering mortgage payments, property expenses, and contributing to your overall earnings.

6. Inflation Hedge: Real estate has historically been an excellent hedge against inflation. As the cost of living increases, so does the potential for rental income and property appreciation, preserving your purchasing power.

| Advantages | Explanation |

|---|---|

| Tax Breaks | Deductions on mortgage interest, property taxes, and depreciation |

| Appreciation | Properties can increase significantly in value over time |

| Portfolio Diversification | Protects against market volatility by diversifying across asset types |

| Real Estate Leverage | Use of down payments to control larger assets |

| Stable Cash Flow | Reliable income through rental properties |

| Inflation Hedge | Property value and rents typically rise with inflation |

Real-world Examples of Real Estate Advantages

Consider the case of a first-time buyer in London. By investing in a flat worth £300,000 with a £60,000 down payment, they leveraged the £240,000 mortgage to acquire an appreciating asset. In three years, if the property appreciates by 10%, it could be worth £330,000, providing a gain of £30,000 on an initial investment of just £60,000.

Another example involves Real Estate Investment Trusts (REITs). An investor holding shares in an equity REIT, which must distribute at least 90% of its income to shareholders, could receive attractive quarterly dividends, thereby enjoying regular income while benefiting from property appreciation as the real estate market grows.

Practical Implications for Real Estate Investors

If you’re considering entering the real estate market, be sure to evaluate which type of property investment aligns best with your financial goals. Whether using leverage to buy a rental property or investing in REITs for passive income, each avenue provides unique benefits.

Additionally, understanding tax implications and potential cash flow will position you better to make informed decisions that can lead to financial independence.

- Aim to conduct thorough market research before making purchases to identify high-growth areas.

- Keep an eye on interest rates; lower rates can enhance your affordability and investment appeal.

- Regularly reassess your investment strategy based on market conditions and personal financial goals to optimize returns.

Investing in real estate has the potential to significantly enhance your financial portfolio, provided you approach it strategically and remain informed.

Influence of Government Policies on Housing Market

The housing market in the UK isn’t just affected by economic factors and regional disparities; government policies play a crucial role in shaping its trajectory. From tax incentives to regulations, these policies impact everything from interest rates to the availability of affordable housing. Let’s dive into how these government approaches have influenced house prices in recent years.

Key Government Policies Impacting the Housing Market

1. Help to Buy Scheme: The Help to Buy scheme, launched in 2013, has allowed many first-time buyers to enter the market with as little as a 5% deposit. This initiative continues to influence housing demand by making homeownership more accessible. In fact, studies indicate that over 300,000 homes have been purchased through this scheme, contributing to a noticeable uptick in house prices.

2. Stamp Duty Changes: Recent stamp duty reforms have significantly impacted buyer behavior. The temporary increase in the threshold, which exempted properties up to £500,000 from stamp duty, encouraged many buyers to make purchases during that period. As a result, some areas saw price increases as high as 20% in the wake of these changes due to the surge in demand.

3. Affordable Housing Policies: Local government initiatives aimed at increasing the availability of affordable housing have led to a mixed response in the market. While more affordable units can help balance price growth, some areas have seen how the lack of sufficient investment in affordable housing has exacerbated the issue of rising prices, particularly in urban centers.

Government Policies Table

| Policy | Implementation Year | Impact on House Prices |

|---|---|---|

| Help to Buy Scheme | 2013 | +300,000 homes purchased |

| Stamp Duty Reform | 2020 | +20% in certain regions |

| Affordable Housing Program | Varies | Varied impact, some regions see lesser price growth |

Real-World Examples

In London, the Help to Buy scheme has played a pivotal role. Specific data shows that regions with strong uptake of this initiative experienced a price increase of approximately 15% compared to those that did not participate. Conversely, in areas where the government’s affordable housing policies were put into action, small price increases were observed, leading to some stabilization in otherwise volatile markets.

In contrast, cities like Manchester have shown that the lack of sufficient affordable housing policies can lead to uncontrolled price surges, as demand consistently outstrips the supply of low-cost units, driving prices up even further.

Practical Implications for Readers

It’s essential to understand how these policies may affect your home-buying decisions. If you’re considering purchasing a home:

- Take advantage of schemes like Help to Buy, if you qualify, as they can significantly reduce the financial barrier to entry.

- Stay informed about changes to stamp duty, as timing your purchase around these reforms can lead to savings.

- Consider investing in regions with strong affordable housing initiatives, where price growth might be steadier and more sustainable.

Remember, the landscape of the housing market is continually evolving. Keeping an eye on government policies will not only help you make informed decisions but also position you strategically in this dynamic market environment.

Case Studies of Recent Price Changes

Understanding the nuances of house price variations allows us to grasp how much the market has evolved. This section aims to highlight specific case studies of recent price changes that underscore the trends within the UK housing market.

Case Study Highlights

- London Boroughs: Within just a two-year span from 2021 to 2023, certain boroughs have witnessed dramatic shifts. For instance, Barking and Dagenham reported a 25% increase, contrasting with the more modest 5% growth in Kensington and Chelsea. This illustrates the diversity of price movements even within the same metropolitan area.

- Greater Manchester: In a neighborhood like Salford, the average property price jumped from £158,000 to £210,000 between early 2021 and late 2023, marking a staggering 33% rise. This increase highlights the area’s growing appeal, driven largely by new infrastructure projects.

- South West England: The coastal town of Torquay experienced a 20% rise in property values over the past three years, attributed to an influx of remote workers seeking a better quality of life.

Comparative Table of Recent Price Changes

| Location | Price Change % (2021-2023) | Average Price (2023) | Key Influences |

|---|---|---|---|

| Barking and Dagenham | 25% | £330,000 | Enhanced transport links |

| Kensington and Chelsea | 5% | £1,200,000 | Stability in luxury market |

| Salford | 33% | £210,000 | Infrastructure investments |

| Torquay | 20% | £275,000 | Remote work and lifestyle shifts |

Real-World Examples

- Barking and Dagenham: This borough has become increasingly attractive due to new rail links and regeneration projects. The surge in prices reflects heightened interest from young families looking for affordable homes while remaining connected to Central London.

- Salford’s Transition: Several tech startups relocating to Salford have increased demand in the housing sector, resulting in rapid price increases. This case demonstrates how economic shifts in one segment can significantly impact residential real estate.

Practical Implications

As you evaluate potential property investments or purchases, consider these case studies as indicators of areas experiencing notable shifts. Understanding localized market dynamics can offer insights into where future growth may be most robust.

- Investing in Emerging Areas: Locations like Salford and Barking and Dagenham may provide significant returns as their appeal continues to rise.

- Lifestyle Decisions in Real Estate: Remote work changes how people view neighborhoods. Areas traditionally seen as commuter zones are turning into desired living spaces, which can influence long-term investment strategies.

Being knowledgeable about specific case studies helps you navigate the complexities of the changing housing market effectively. Prioritize areas showing strong price appreciation potential backed by economic and lifestyle trends to make informed decisions.