How Much Do Manufactured Homes Cost? Well, you’re looking at a price range that can really surprise you. On average, a new manufactured home can cost anywhere from $100,000 to $200,000, depending on size and features. For instance, a single-wide home might run you around $50,000 to $75,000, while a more spacious double-wide ranges from $75,000 to $150,000. And if you fancy something a little fancier with custom designs, you’re definitely looking at higher numbers—some upscale models can even push past $200,000.

But don’t let those numbers scare you off; it’s all about the value you’re getting. Typically, these homes offer a faster route to homeownership at a fraction of the cost of traditional houses. For example, while the average price of a conventional home in the U.S. hovers around $400,000, a manufactured home provides a viable alternative, especially in areas where real estate prices are skyrocketing. Plus, with lower maintenance costs and energy-efficient options, many people find that manufactured homes can offer significant savings in the long run.

Average Price Range of Manufactured Homes

When considering manufactured homes, understanding the average price range can help you make a smart investment. These homes often represent a more budget-friendly option compared to traditional site-built homes. Let’s dive into the pricing specifics for various manufactured home types.

Pricing Breakdown by Home Type

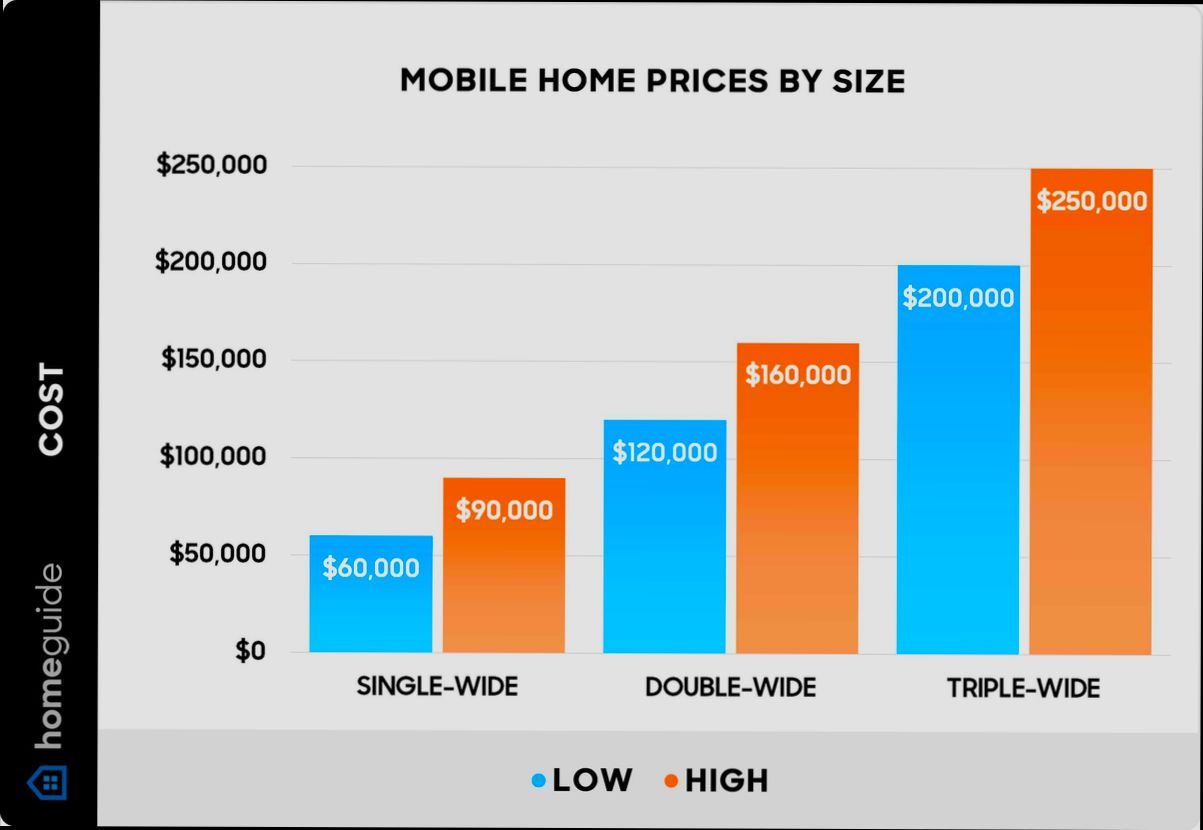

Manufactured homes come in different sizes, and each type has its own average price range. Here’s how they stack up:

| Home type | Average width | Average square footage | Average delivered cost* |

|---|---|---|---|

| Single-wide | 14 – 18 feet | 500 – 1,500 | $60,000 – $90,000 |

| Double-wide | 20 – 36 feet | 1,500 – 2,500 | $120,000 – $160,000 |

| Triple-wide | 28 – 54 feet | 2,000 – 3,600 | $200,000 – $250,000+ |

Factors Influencing Average Cost

Numerous factors can impact the overall pricing of manufactured homes. Here are some average costs you should consider:

- Double-wide unit: $116,000 – $150,000

- Full-service delivery: $4,000 – $10,000

- Site preparation: $7,000 – $47,000

- Utilities installation: $2,500 – $12,500

- Permits and fees: $7,500 – $28,500

These additional expenses play a significant role in the overall cost, so keep them in mind while budgeting for your new home.

Real-World Example

For instance, if you’re looking to buy a double-wide manufactured home, you might find it priced around $148,100 on average. When you factor in delivery and additional installation costs, the total could rise to between $143,000 and $268,000. This variation depends on the home’s location and any necessary site preparation.

Another example involves a triple-wide home. If its base price is around $200,000 and you consider the extra costs for utilities and site setup, you might end up spending significantly more. Being aware of these overall costs is essential for effective financial planning.

Practical Insights

To make the most of your budget:

- Research local prices: They can vary widely depending on region and demand.

- Consider used homes: They can range from $10,000 to $100,000, offering a more affordable option.

- Budget for hidden costs: Be prepared for additional expenses like land rent, permits, and installation.

When planning your purchase, keep these price ranges front and center as you navigate the world of manufactured homes. Understanding the costs directly related to each home type empowers you to make informed decisions tailored to your financial situation.

Factors Influencing the Cost of Homes

When it comes to understanding the cost of homes, several factors play a critical role in determining their price point. From the number of bedrooms and bathrooms to the overall size of the home, these elements drastically influence the market value. Let’s dive into the primary factors that affect home pricing, backed by recent research data.

Key Factors Affecting Home Prices

1. Number of Bedrooms and Bathrooms: The composition of a home, particularly the count of bedrooms and bathrooms, is a major determinant of its price. Research indicates that these two aspects account for approximately 36.2% of the variability in home prices. Homes with more bedrooms and bathrooms are generally considered more desirable and command higher prices.

2. Home Size: The square footage of a home also significantly impacts its market value. The average size of manufactured homes surveyed is approximately 931.62 square feet, with prices increasing along with size. Typically, larger homes provide better value due to their additional living space and potential for customization.

3. Location: Location remains an indispensable factor in home pricing. In the recent study, for instance, a significant number of homes were identified in the Northern region (34.2%), which may correlate with slightly higher prices due to location desirability. Homes in urban areas or near amenities often have a higher price tag compared to those in rural locations.

4. Market Variability: Market conditions, including economic factors such as interest rates and employment levels, also play a critical role. A vibrant local economy tends to increase demand for homes, thereby elevating their price. Conversely, areas with declining economies may see a reduction in home values.

5. Number of Floors: The number of floors in a home can also influence its appeal and cost. Homes with multiple floors often appeal to larger families and can command higher prices compared to single-floor layouts.

Comparative Table of Home Features and Average Prices

| Feature | Mean Value | Median Value | Std. Deviation |

|---|---|---|---|

| Number of Bedrooms | 1.82 | 2 | 0.47 |

| Number of Bathrooms | 1.66 | 2 | 0.47 |

| Size (in square feet) | 931.62 | 914 | 201.22 |

| Number of Floors | 2.37 | 2 | 0.97 |

Real-World Examples

In our study examining the price influences on manufactured homes, homes with two bedrooms and two bathrooms showed a strong correlation with higher prices, reflecting the critical value placed on these characteristics. A home with three bedrooms and two bathrooms typically attracted an average increase in price due to the increased desirability for larger families, highlighting how space directly translates to value.

Practical Implications for You

When considering a home purchase, it’s essential to evaluate these factors - the more you know about what drives home prices, the better informed your decisions will be. For instance, if you’re searching for a larger family home, focusing on properties with more bedrooms and bathrooms can yield better resale value in the long run.

Taking into account that the number of bedrooms and bathrooms accounts for roughly 36.2% of price variability, prioritize these features in your home search to maximize your investment. Additionally, keep an eye on local market trends, as becoming aware of fluctuating economic conditions can guide your timing in buying or selling a home.

Comparative Analysis of Financing Options

When it comes to buying a manufactured home, selecting the right financing option is crucial. Different financing routes can significantly impact your costs, down payments, and monthly payments. Let’s break down the popular financing options available for manufactured homes, so you can make an informed choice.

Types of Financing Options

1. Chattel Loans

- Designed for manufactured homes classified as personal property.

- Generally have shorter terms (typically 5-20 years).

- Interest rates may range from 4% to 10%, depending on credit score and loan amount.

- Down payments can vary, but you might expect around 10% of the purchase price.

2. Conventional Mortgages

- Suitable for homes considered real property.

- Typically longer terms (15-30 years) and lower interest rates (around 3-5%).

- Down payments can start as low as 3%, but 20% is standard to avoid private mortgage insurance (PMI).

3. FHA Loans

- Insured by the Federal Housing Administration, aimed at first-time homebuyers.

- Allow as little as 3.5% down payment.

- Interest rates range from 3.25% to 5.5%.

- Can finance manufactured homes as long as they meet specific criteria.

4. VA Loans

- Exclusively for veterans and active-duty service members.

- No down payment is required.

- Competitive interest rates (often lower than conventional loans).

- Guarantee can cover up to 25% of the home price.

Comparative Table of Financing Options

| Financing Option | Interest Rates | Down Payment | Loan Terms | Eligibility Criteria |

|---|---|---|---|---|

| Chattel Loans | 4% - 10% | 10% | 5-20 years | Personal property classification |

| Conventional Mortgages | 3% - 5% | 3% - 20% | 15-30 years | Real property classification |

| FHA Loans | 3.25% - 5.5% | 3.5% | 15-30 years | Must meet FHA requirements |

| VA Loans | Varies | 0% | 15-30 years | Military service verification |

Real-World Examples

- A client in Texas opted for a chattel loan for a $80,000 single-wide manufactured home. With a 10% down payment, their out-of-pocket cost was $8,000, and they faced an interest rate of 7%, resulting in manageable monthly payments over 15 years.

- Conversely, a veteran in Florida used a VA loan to purchase a $150,000 double-wide. With no down payment and a strong credit score, they secured a 3.5% interest rate, significantly reducing their monthly financial obligation compared to other options.

Practical Implications for Readers

Understanding these financing options can drastically influence your budget and capability to secure a manufactured home. Consider your financial situation carefully:

- If you’re a first-time buyer with limited savings, FHA loans might be appealing.

- For those with military experience, exploring VA loans could yield substantial savings.

- Always calculate the total cost of financing over the loan’s lifespan, not just the monthly payment.

Specific Facts or Actionable Advice

- Before deciding on a financing option, review your credit score; this figure crucially affects interest rates and loan terms.

- Always compare offers from multiple lenders—small differences in interest rates can lead to significant savings over time.

- Be prepared for additional costs, such as inspection fees and appraisals, which can vary based on the financing option chosen.

Statistical Trends in Manufactured Housing Prices

When diving into the world of manufactured housing prices, it’s essential to understand the statistical trends that emerge from recent data. These trends not only reveal how prices fluctuate over time but also guide prospective buyers in making informed decisions.

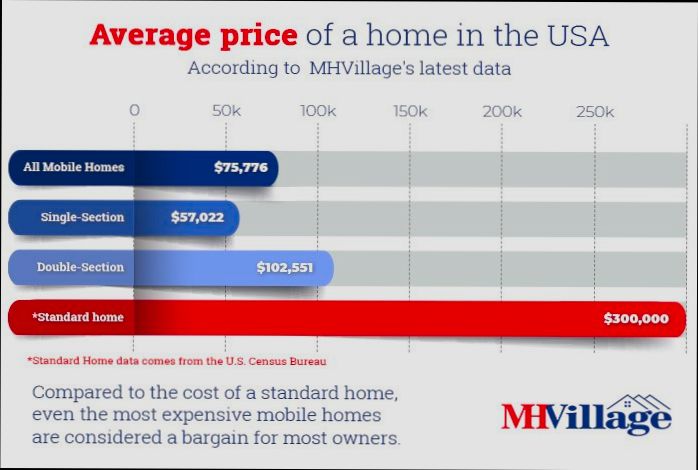

One striking statistic is that the average cost of a new manufactured home in 2023 hovers around $113,951.97. If we break it down further, multi-section homes tend to command higher prices, averaging $193,103, while single-section homes are more budget-friendly, averaging $106,629. Furthermore, existing manufactured homes fall into a more affordable range, with an average sale price of $69,781. These figures illustrate the varied landscape of manufactured home pricing.

Key Statistical Insights

- The average price per square foot for manufactured homes is approximately $130.53.

- Multi-section homes are priced higher at about $140.07 per square foot, while single-section homes are more accessible at an average of $110.17 per square foot.

- A significant 57 percent of new manufactured homes are placed in communities, underscoring the demand for affordable housing arrangements.

Cost Breakdown Table

| Home Type | Average Cost | Average Square Footage | Price per Square Foot |

|---|---|---|---|

| Single-Section | $106,629 | 500 – 1,500 | $110.17 |

| Multi-Section | $193,103 | 1,500 – 2,500 | $140.07 |

| Existing Homes | $69,781 | Varies | Varies |

Real-World Examples

Let’s look at the manufactured housing communities in the United States. There are roughly 43,000 manufactured home communities, with approximately 4.3 million manufactured home sites. Communities vary in size, with about 29 percent containing between 25 to 99 homesites. This diversity in community size reflects differing market dynamics, which can influence the pricing strategies of homes placed within them.

For instance, larger communities tend to enjoy economies of scale, potentially offering homes at slightly lower prices due to shared infrastructure costs. Conversely, smaller communities might inflate prices, reflecting limited supply and greater demand.

Practical Implications for Buyers

Understanding these statistical trends can help you navigate the manufactured housing market more effectively. For example:

- If you’re aiming for value, consider opting for a single-section home, which tends to be more affordable both in terms of upfront cost and cost per square foot.

- If you’re placing your home in a community, be aware that community size can influence pricing. Larger communities may offer cost advantages due to their scale.

- Keep an eye on the overall trends in manufactured home prices in your region, as these can fluctuate based on market conditions, availability, and demand.

Actionable Advice

Stay informed about the average costs and market condition trends in your area. Engage with local manufactured home retailers or builders who can provide recent data tailored to your specific interests. By leveraging current statistics and market insights, you position yourself as a savvy buyer in the manufactured housing landscape.

Cost-Saving Advantages of Manufactured Homes

When it comes to homeownership, cost is often a crucial factor. Manufactured homes present a compelling option for those looking to save significantly not just on the purchase price, but also on long-term costs associated with homeownership. Let’s dive into the specific cost-saving advantages that these homes offer.

Affordability and Construction Savings

One of the standout features of manufactured homes is their affordability. On average, manufactured homes cost 10 to 35 percent less per square foot than their site-built counterparts. By streamlining production in a factory setting, manufacturers can cut down on labor and materials costs. This affordability makes manufactured homes accessible to a broader range of buyers looking to invest smartly.

- Savings per square foot: Typically 10-35% lower than site-built homes.

Quick Move-In Times

You can also save on living costs thanks to faster construction times. Manufactured homes are usually about 90 percent complete when they arrive at your property. This efficiency means you can move into your new home sooner, reducing the transitional costs associated with prolonged living situations such as temporary rentals or extended hotel stays.

- Example: A traditional site-built home could take several months or even over a year to complete, whereas a manufactured home can be ready to occupy within weeks.

Energy Efficiency Benefits

Manufactured homes are designed to be energy-efficient, which often leads to low utility bills. Research from the U.S. Department of Energy indicates that these homes can be up to 55 percent more energy-efficient than standard homes, translating into significant savings on monthly energy expenses. This is particularly beneficial for families and individuals looking to maintain household budgets.

- Expected energy savings: 55% more efficient compared to traditional homes.

Reduced Maintenance Costs

With robust manufacturing standards set by the U.S. Department of Housing and Urban Development (HUD), manufactured homes tend to have lower maintenance costs over time. Many of these homes utilize durable materials and modern technology that withstand wear and tear, further reducing the need for expensive upkeep.

Cost Comparison of Standard Foundations

Foundations are a critical aspect of manufactured home installation, and choosing the right one can affect overall costs. Here’s a quick breakdown of foundation costs:

| Foundation Type | Cost Range |

|---|---|

| Pier and Beam | $8,200 - $22,000 |

| Slab | $5,000 - $40,000 |

| Basement | $13,000 - $30,000 |

| Pit/Crawl Space | Approximately $13,000 |

Real-World Examples

Let’s consider a family that opted for a double-wide manufactured home. With an initial cost of around $120,000 and a quick move-in time, they immediately reduced their housing expenses compared to the typical rent market in their area. Additionally, their monthly energy bills were cut by nearly half due to the home’s energy-efficient features, leading to substantial savings over time.

Practical Implications for Home Buyers

When considering the purchase of a manufactured home, it’s essential to calculate the total cost of ownership. This includes initial purchasing costs and the long-term savings on energy and maintenance. Research conducted indicates that over time, the reduced cost of construction, faster move-in times, and energy savings make manufactured homes a savvy financial choice for many.

Investing in a manufactured home can result in substantial cost advantages, making homeownership more achievable while enjoying the benefits of modern living. With the potential to save significantly on initial investment and ongoing expenses, manufactured homes are an excellent alternative for budget-conscious buyers looking to own a quality home.

Real-World Examples of Home Purchases

When considering buying a manufactured home, real-world examples can provide valuable insights into the purchasing experience and outcomes. This section will explore specific purchases that demonstrate the unique benefits and challenges of owning a manufactured home.

Case Studies of Home Purchases

1. Single-Wide for Young Professionals

A couple in their late 20s purchased a single-wide manufactured home for $65,000 in a suburban community. They appreciated the flexibility and mobility this home offered, allowing them to relocate when job opportunities arose. Living in a community that offered amenities like a swimming pool and playgrounds provided them with an enriched lifestyle.

2. Double-Wide for Growing Families

A family of four invested in a double-wide manufactured home for $135,000. They opted for this size due to the increased square footage (about 1,800 sqft), allowing room for children and pets. With a lower cost of living in a manufactured home community, they could keep childcare expenses manageable while enjoying communal amenities, contributing to a stronger neighborhood feeling.

3. Retirement in Serene Communities

A retired couple decided to downsize by purchasing a double-wide manufactured home in a 55+ community for $120,000. They were drawn to the low maintenance requirements of manufactured homes and the sense of community living. The amenities available, such as a clubhouse and organized activities, enriched their retirement lifestyle while remaining within their budget.

Comparative Pricing Table

| Home Type | Purchase Price | Average Size (sqft) | Monthly Lot Rent (if applicable) | Community Amenities |

|---|---|---|---|---|

| Single-Wide | $65,000 | 700 | $300 | Pool, BBQ areas |

| Double-Wide | $135,000 | 1,800 | $450 | Clubhouse, events |

| Triple-Wide | $200,000 | 2,400 | N/A | None |

Practical Implications for Readers

By learning from these examples, you can understand that manufactured homes often come with lower ownership costs but vary in initial purchase prices, size, and community factors. When planning your purchase, remember:

- Consider your lifestyle needs. Are you looking for flexibility or community amenities?

- Weigh the benefits of purchasing land versus leasing in a community. While land ownership can offer more privacy and increase potential resale value, leasing might provide quicker access to essential amenities.

- Assess the overall costs—beyond purchase price—such as lot rent and community fees, which can significantly impact your budget.

Make informed decisions based on these real-world experiences and remember the options available to tailor your living situation to your lifestyle preferences.

Budgeting for Land and Installation Costs

When planning to purchase a manufactured home, it’s crucial to understand the expenses associated with land and installation. These costs can significantly impact your overall budget, and being well-informed allows you to make financially sound decisions.

Important Considerations for Land Costs

1. Land Prices Vary: The cost of land can fluctuate dramatically based on location. For instance, residential construction costs in select U.S. cities differ substantially, with major urban areas often commanding higher prices per square foot. In the fourth quarter of 2024, residential construction costs are expected to average $150 per square foot in cities like San Francisco, while lower-cost options might be available in rural areas starting as low as $40 per square foot.

2. Land Preparations: Don’t forget to account for any grading or land preparation costs. Depending on your land’s current state, you might need to invest in clearing and leveling costs, which can range between $1,000 to $4,000.

3. Utilities: Installing utilities such as water, electricity, and sewage can easily add another $5,000 to $10,000 to your total. Be sure to verify if utilities are already accessible on the property to avoid unexpected expenses.

Installation Costs Breakdown

| Cost Component | Estimated Range |

|---|---|

| Home Setup | $2,000 - $5,000 |

| Foundation Construction | $4,000 - $10,000 |

| Utility Connections | $5,000 - $10,000 |

| Permits and Inspections | $500 - $2,000 |

Real-World Examples

Consider the scenario of a couple in Austin, Texas, who purchased a double-wide manufactured home for $120,000. They faced additional costs of $15,000 for land purchase, $6,000 for the foundation, and $10,000 for utility hookups. As a result, their total investment rose to $151,000, highlighting how land and installation costs can elevate the initial budget.

In a different case, a family in a rural part of Florida purchased land for $30,000. They spent a modest $3,000 on site preparation and $2,000 for utility connections. Their total expenditure remained around $135,000, including the cost of a single-wide home at $100,000, showcasing how geographical location can alter overall expenses.

Practical Implications for Readers

- Budget Ahead: Always set aside a contingency fund, ideally 10-20% of your total budget, for unforeseen land or installation expenses.

- Research Local Costs: Investigate specific costs in your targeted area by reaching out to local real estate agents or consulting town hall resources.

- Permitting: Keep in mind that permit costs can vary widely based on local regulations. Always check with your local government for precise figures to avoid costly surprises.

Actionable Advice

I recommend collecting multiple quotes from contractors for installation services and checking local listings for land prices in your desired area. Additionally, using online tools and resources can offer you insights into the average land and installation costs specific to your budget requirements. Always cross-reference these figures with multiple sources to ensure comprehensive understanding and accuracy.