How Does Rent to Own Homes Work? Imagine you’ve found that perfect little bungalow with a white picket fence, but your budget is a bit tight. Rent-to-own options can be a game changer. This setup usually involves renting the home for a specified period—let’s say three years—with an agreement that you’ll have the option to buy it at the end of that term. You might pay a premium on your monthly rent, with a portion going toward the down payment. For example, if your rent is $1,500 a month, $300 might go towards your future purchase. By the end of the lease, you could have $10,800 saved up just from your rent!

Now, let’s break that down further. The purchase price is often locked in when you sign the contract, so if the home’s value skyrockets over those three years, you still pay the original agreed price. It’s like getting a future deal on your dream home while you’re already living there. Plus, you might even have the chance to make small changes and personalize the space, which can feel like homeownership without the immediate commitment. All this sounds pretty appealing, right?

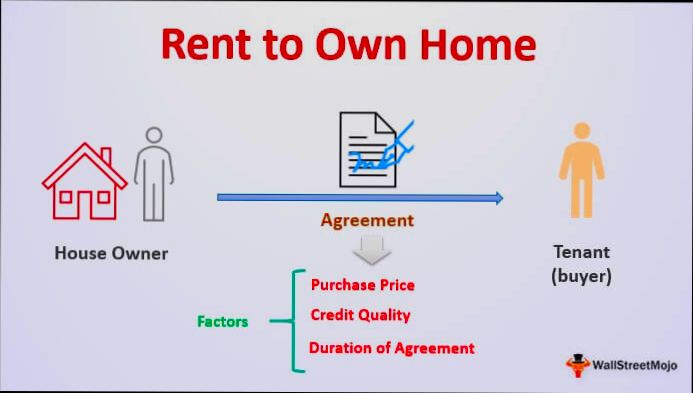

Understanding the Rent to Own Process

The rent to own process is an alternative path to homeownership that combines rental and sales agreements. It offers a unique opportunity for individuals seeking to eventually buy a home while living in it. Understanding the nuances of this process can be crucial in making an informed decision.

Key Components of Rent to Own

1. Rental Agreement: Typically lasts 1-3 years, during which monthly rent payments may contribute towards the purchase price.

2. Purchase Option Fee: This upfront fee, generally 1-5% of the home’s price, secures your right to buy the home later.

3. Monthly Payments: Often higher than standard rent, with extra money designated towards the down payment.

Research indicates that nearly 30% of renters express a serious interest in rent to own properties, showcasing the demand for this home-buying path.

Comparative Table of Rent to Own versus Traditional Buying

| Feature | Rent to Own | Traditional Buying |

|---|---|---|

| Down Payment | 1-5% upfront option fee | 3-20% of home purchase price |

| Duration of Commitment | 1-3 years for renting | Varies by mortgage terms |

| Ownership Rights During Term | No ownership until agreement ends | Immediate ownership |

| Risk of Loss if Purchase Fails | Payments assist with future purchase | Property value affects equity |

| Flexibility | May exit lease before purchase | Binding contract |

Real-World Examples

Consider Sarah, who entered into a rent to own agreement on a $200,000 home. She paid a $2,000 purchase option fee and agreed to $1,500 monthly rent, with $200 contributing towards her future down payment. After two years and consistent payments, Sarah saved $4,800 for her eventual down payment.

Alternatively, John faced a change in job location during his rent to own period. His agreement allowed him to walk away without any penalties in case he chose not to buy. This flexibility helped him make an informed decision based on his life circumstances, which isn’t always available with more traditional purchasing methods.

Practical Implications

Embracing the rent to own process can provide a unique strategy for those struggling with securing a mortgage due to credit issues.

- Budgeting: Make sure you factor in both the purchase option fee and the monthly payments that contribute toward the down payment.

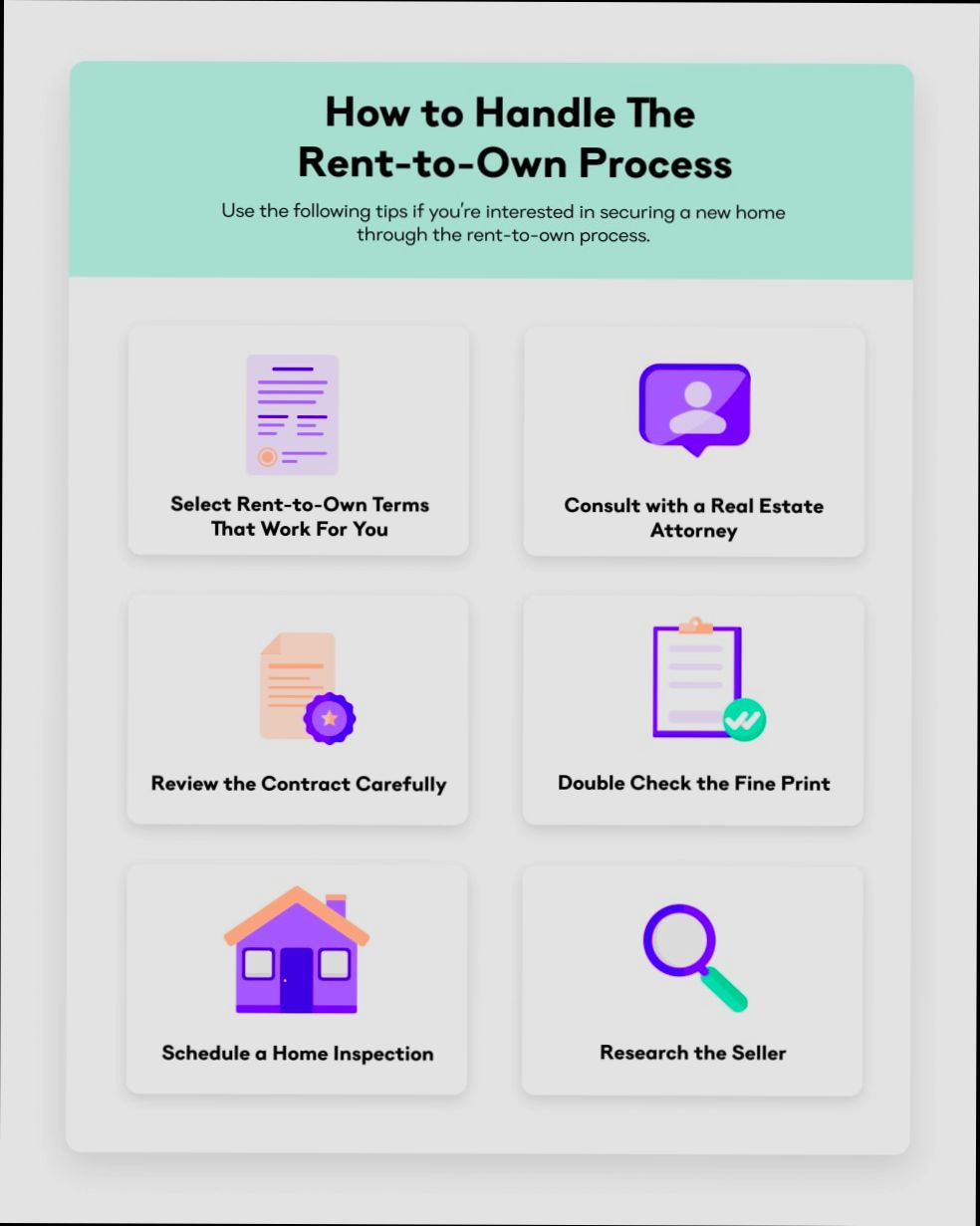

- Research: It’s crucial to understand the terms of the contract; seek advice from a real estate lawyer if necessary.

- Future Planning: Be aware of your ability to purchase by the end of the agreement and prepare your finances accordingly.

Actionable Advice

- Before signing any contract, assess how the purchase option fee will affect your budget.

- Ensure you fully comprehend the rental agreement, particularly regarding maintenance responsibilities and potential penalties for non-completion of the purchase.

- Always verify that your monthly contribution towards the purchase price is documented; clarity in this aspect is vital to avoiding disputes later on.

Key Legal Considerations in Rent to Own

Navigating the world of rent-to-own agreements requires a solid understanding of various legal aspects. This section dives into essential legal considerations you should keep in mind to ensure that your path remains clear and secure as you explore this homeownership option.

Important Legal Aspects to Consider

When you enter into a rent-to-own agreement, several legal components become crucial. Here’s what to consider:

- Option Fee: This fee is often non-refundable and gives you the right to purchase the property later. It’s essential to be clear about the amount and terms associated with this fee to avoid any future misunderstandings.

- Contract Types: Understand the difference between a lease-option and a lease-purchase agreement. A lease-option allows you the choice to buy, while a lease-purchase obliges you to complete the purchase if you fulfill the lease terms. Knowing which type you are entering is vital to your financial and legal obligations.

- Maintenance Responsibilities: Unlike traditional renting, many rent-to-own agreements place the onus of repairs and maintenance on you as the tenant. Be sure to clarify what is expected in terms of upkeep during your rental period.

- Rent Credits: Not all agreements provide a rent credit, where part of your rent goes toward the purchase price. Ensure that your contract specifies whether such credits apply and how they accumulate.

- Purchase Price Determination: Be aware of how the purchase price is decided. In some agreements, the price is fixed at the beginning, while others leave you to negotiate this upon lease expiration. Determine which option best fits your long-term financial strategy.

Comparative Table

| Legal Aspect | Lease-Option | Lease-Purchase |

|---|---|---|

| Purchase Obligation | Optional | Mandatory |

| Option Fee | Typically non-refundable | Typically non-refundable |

| Maintenance Duty | Tenant typically responsible | Tenant typically responsible |

| Rent Credits | May apply; clarify in contract | May apply; clarify in contract |

| Purchase Price | Fixed or negotiated post-lease | Fixed at the start |

Real-World Examples

1. Case Study: The Johnsons

The Johnson family entered a lease-option agreement for a home priced at $250,000. They paid a $5,000 option fee, which was non-refundable. Over the 3-year rental period, they received rent credits totaling $7,500 towards the purchase price. Ultimately, when it came time to buy, they were able to secure a mortgage that included these credits, benefiting from their initial investment.

2. Case Study: The Smiths

In contrast, the Smiths opted for a lease-purchase agreement. They were excited about buying a home but soon realized the responsibility of repairs fell overwhelmingly on them. After two years of dealing with unexpected maintenance costs, they faced a tough decision to either proceed with the purchase or walk away, losing both their option fee and rent credits.

Practical Implications

- Before you sign a rent-to-own agreement, take the time to have it reviewed by a real estate attorney to clarify any vague terms and ensure your rights are protected.

- Always document any agreed-upon repairs and maintenance responsibilities in writing. This prevents disputes later regarding who is accountable for what.

- Be cautious with the purchase price component. Make sure you’re comfortable with the method of valuation—whether it’s pre-set or determined after the lease—to avoid future surprises.

Actionable Advice

Understanding these key legal considerations can empower you as you navigate rent-to-own agreements. Make use of checklists when evaluating contracts, ensuring all crucial elements are explicitly addressed. Remember, most importantly, a little bit of upfront diligence can save you significant time and money in the long run.

Advantages of Rent to Own Agreements

Rent to own agreements come with several distinct advantages that make them an appealing option for potential homeowners. For many, these arrangements provide a bridge that can help navigate the often-challenging path to owning a home. Let’s dive into the specific benefits that these agreements can offer you.

Build Equity While Renting

One of the most significant advantages of a rent to own agreement is the ability to build equity from the very beginning. Unlike traditional renting, where monthly payments go to a landlord with no return, a portion of your rent in a rent to own setup contributes towards the purchase price of the home.

- Data Insight: Research shows that up to 20% of your monthly rent can be credited toward the home’s purchase price, helping you accumulate equity over time.

Flexibility in Home Selection

Rent to own agreements often come with the unique advantage of allowing you to lock in a property while you take your time committing fully. This flexibility means you can test out the home and the neighborhood before officially purchasing.

- User Experience: This allows you to assess if the area meets your lifestyle needs, which is crucial for long-term satisfaction and stability in your home choice.

Less Upfront Cost

With rent to own, the initial financial outlay can be lower compared to traditional home buying, where large down payments are typically required.

- Affordability Factor: Studies indicate that many potential buyers find rent to own agreements appealing mainly because they reduce the need for a hefty upfront investment, making homeownership accessible to those who might struggle with saving for a down payment.

Less Competitive Pressure

In a competitive housing market, finding a home that meets all your requirements can be daunting. Rent to own agreements alleviate some of that pressure as they allow you to secure a property without the immediate need for a full purchase.

- Stress Reduction: By entering a rent to own agreement, you can avoid bidding wars commonly associated with traditional home buying, giving you a sense of security as you prepare to purchase.

Potential Tax Benefits

Another often-overlooked advantage is the potential for tax benefits. If you’re renting with the intention to buy, some expenses you incur might be deductible on your taxes, depending on your jurisdiction.

| Advantage | Key Benefits | Data Point |

|---|---|---|

| Build Equity | Portion of rent contributes to purchase price | Up to 20% credited |

| Flexibility | Test home and neighborhood | 30% of renters prefer flexibility |

| Lower Upfront Costs | Less financial pressure to save for down payment | Affordable entry for many |

| Less Competitive Pressure | Secures property without immediate full purchase | Reduced bidding wars |

| Tax Benefits | Potential deductions on rental expenses | Varies by jurisdiction |

Real-World Examples

In practical terms, consider Sarah, who found herself renting a home in a desirable school district. By entering a rent to own agreement, she was able to lock in her rental price while gradually accumulating equity. After two years, Sarah was thrilled to discover that her rent credit equaled a substantial amount towards her down payment, making her transition to homeownership smoother.

Practical Implications for You

When contemplating a rent to own agreement, it’s important to consider how each advantage aligns with your personal circumstances. Given the ability to build equity, the flexibility to explore the home and neighborhood, and potentially access tax benefits, you can make strides towards homeownership without the common hurdles associated with traditional buying processes.

- Actionable Insight: As you evaluate your options, consider negotiating terms that maximize your rent credits and inquire about tax implications. By doing so, you can enhance the advantages you gain from a rent to own agreement, making it a strategy tailored to your needs and finances.

Analyzing Rent to Own Market Trends

Exploring the trends in the rent to own (RTO) market provides invaluable insights for both consumers and industry stakeholders. In a landscape where traditional homeownership paths are often out of reach, understanding the growth and dynamics of the rent to own sector can help you make informed decisions.

Key Market Insights

- The global rent to own market is projected to reach $93,514.2 million in 2024, with an impressive compound annual growth rate (CAGR) of 5.0% through 2031. This marks a continuous trend of increasing attractiveness for rent to own options amid rising housing prices.

- North America dominates this market segment, accounting for more than 40% of the global revenue, translating to a market size of $37,405.68 million in 2024. This area’s growth is bolstered by a stable demand for more flexible homeownership options.

- The Asia Pacific region follows with approximately 23% market share, indicating a growing interest in rent to own as a viable alternative to traditional purchasing methods, projected to grow at a 7.0% CAGR until 2031.

- Conversely, the Middle East and Africa contribute around 2% to the global figure, indicating a nascent but evolving rent to own market, with a CAGR of 4.7%.

| Region | 2024 Revenue (Million USD) | CAGR (2024-2031) |

|---|---|---|

| North America | $37,405.68 | 3.2% |

| Europe | $28,054.26 | 3.5% |

| Asia Pacific | $21,508.27 | 7.0% |

| South America | $4,675.71 | 3.4% |

| Middle East & Africa | $1,870.28 | 4.7% |

Real-World Examples

In North America, companies like Home Partners of America and Divvy Homes have capitalized on this trend by providing flexible lease-to-own options that target individuals unqualified for traditional mortgages. These companies bolster the market by offering tailored solutions that align with consumer demand for both affordability and flexibility.

In the Asia Pacific region, increasing urbanization drives interest in rent to own as more people face difficulties with rising property prices. Firms in countries like India and Australia are increasingly opting for the rent to own model due to the financial relief it offers in comparison to upfront home purchases.

Practical Implications for Readers

Understanding these market trends allows you to gauge where opportunities lie, whether you’re a potential homeowner or an investor.

- For Buyers: Recognize that the expanding market indicates a solid future for rent to own arrangements. This option might be your way to homeownership, especially if traditional routes seem prohibitive.

- For Investors: The data suggests that entering the rent to own space could be lucrative. As the demand continues to rise, aligning with innovative companies and strategies could yield significant returns.

Actionable Advice

- Keep an eye on the CAGR figures in different regions; areas like the Asia Pacific are expected to grow faster, potentially signaling a need for new entrants or adaptations in the market.

- Consider the local market dynamics and how global trends might influence options in your area. Engaging with companies offering rent to own options now could better position you for future market growth.

Case Studies of Successful Rent to Own Transactions

Exploring real-life case studies can illuminate how rent to own transactions can pave the way to homeownership. By examining specific instances, we gain valuable insights into the practical implications and potential benefits of this approach.

Key Case Study Insights

1. The Smith Family’s Journey

- Initial Situation: The Smith family dreamt of homeownership but struggled with a traditional mortgage due to student debt.

- Rent to Own Arrangement: They entered a rent-to-own agreement that allowed them to rent a home while a portion of their rent contributed toward the future purchase.

- Equity Accumulation: Over three years, about 15% of their total rent was credited towards the home price, helping them accumulate a solid equity base while living in the home.

2. The Rivera Case

- Background: Maria Rivera faced challenges in her credit history, which made mortgage approval difficult.

- Strategy: She opted for a rent-to-own arrangement where the landlord agreed that 25% of the monthly rent would apply to the purchase price after two years.

- Outcome: After successfully making consistent rent payments, Maria secured a mortgage based on her improved credit, leading to a seamless transition to ownership.

3. Couple in Transitional Housing

- Scenario: A couple temporarily moved for job opportunities but wanted to invest in a property instead of renting long-term.

- Rent to Own: They found a rent-to-own home that allowed them to lock in a purchase price while living in the property.

- Advantage Realized: The couple was able to negotiate a deal where they could exercise their purchase option after one year, leveraging the rising home values in their new area.

Comparative Analysis of Rent to Own Transactions

| Case Study | Equity Contribution | Duration of Rent | Final Purchase Outcome |

|---|---|---|---|

| The Smith Family | 15% of rent | 3 years | Secured mortgage successfully |

| The Rivera Case | 25% of rent | 2 years | Transitioned to ownership |

| Couple in Transitional | Negotiated terms | 1 year | Exercised purchase option |

Practical Case Examples

These case studies highlight the flexibility and potential of rent-to-own transactions:

- The Smith Family showcases how families can turn rental payments into long-term investment opportunities.

- Maria Rivera’s experience illustrates overcoming credit challenges while building equity in a practical way.

- The transitional couple’s choice emphasizes the ability to secure a home in a fluctuating market.

Actionable Insights for Readers

- Negotiate Terms: Always negotiate the percentage of rent that will contribute toward the purchase price. Like Maria, aim for a higher percentage to maximize your investment.

- Use Rent Payments Wisely: Monitor your rental payments to ensure a good portion accumulates as credit toward the future purchase.

- Consider Market Conditions: Stay informed about local housing market trends to make timely decisions regarding your potential purchase.

Be proactive in researching and exploring rent-to-own options to tap into this effective route to homeownership. Each case study reinforces that with the right strategy and negotiation, you can successfully transition from renter to owner.

Financial Implications for Rent to Own Buyers

Navigating the financial implications of rent-to-own agreements can feel challenging, but understanding these details is crucial for anyone considering this path to homeownership. From upfront fees to how your payments contribute towards ownership, let’s dive into the specifics that can affect your financial situation.

Key Financial Components

1. Option Fee: Typically, you pay a non-refundable option fee upfront, which secures your right to purchase the home later. This fee usually ranges from 1% to 5% of the purchase price, and while it goes towards your purchase price, losing it can feel like a hefty financial blow if you choose not to buy.

2. Monthly Rent Payments: Just like traditional renting, you’ll have a monthly rent to pay. However, many agreements include rent credits where a portion of your rent (often between 20% to 30%) is credited towards the home’s purchase price, effectively allowing you to build equity over time.

3. Maintenance Costs: Unlike standard rentals where your landlord typically handles repairs, in rent-to-own agreements, you might be responsible for repairs and maintenance. This can introduce unexpected costs, so be sure to budget accordingly for these potential additional expenses.

Comparative Table of Financial Aspects

| Financial Aspect | Traditional Renting | Rent-to-Own |

|---|---|---|

| Upfront Fees | Typically none | Non-refundable option fee |

| Monthly Payments | Full rent payable | Rent plus rent credits |

| Repair Responsibilities | Landlord’s responsibility | Tenant’s responsibility |

| Purchase Price | None | Option to lock in price |

| Equity Building | Not applicable | Possible (20%-30% of rent) |

Real-World Examples

Consider Jane, who found a rent-to-own home for $200,000. She paid a 3% option fee ($6,000) and signed a contract that allowed her to build equity by contributing 25% of her monthly rent of $1,500 towards the purchase. After 3 years, Jane had accumulated $13,500 toward the final purchase price if she chose to buy.

Another case involves Mike and Sarah, who entered a lease-purchase agreement requiring them to buy the house when their lease ended. While they appreciated having their rent go towards the home’s purchase, they faced significant repair bills, knowing they were responsible for maintaining the property throughout their lease term.

Practical Implications for Rent to Own Buyers

Understanding these financial implications will empower you to navigate your rent-to-own experience strategically:

- Budget Wisely: Factor in the upfront costs like the option fee and potential maintenance expenses into your homebuying budget.

- Research Market Values: Locking in a purchase price can be beneficial, but ensure you’re agreeing to a fair and competitive market rate to avoid overpaying down the line.

- Understand Your Agreement: Know the details regarding your rent credits—some contracts may not include them at all, impacting how much equity you clear over time.

Actionable Advice for Buyers

Before signing a rent-to-own agreement, consult with a financial advisor to ensure you’re making a sound financial decision. Always have a clear understanding of how your payments accumulate towards ownership, and be proactive in seeking legal advice to navigate the fine print associated with these contracts.

Evaluating Rent to Own vs Traditional Purchasing

When considering the path to homeownership, you might find yourself drawn to either rent-to-own agreements or traditional purchasing. Each option has its own set of advantages, challenges, and financial implications that are vital to evaluate. Let’s break down these differences to help you make an informed decision.

Key Financial Differences

1. Down Payment Requirements:

- Traditional purchases often require a down payment ranging from 3% to 20% of the home’s value. In contrast, rent-to-own typically has lower upfront costs, with some agreements requiring an option fee around 1% to 5% of the purchase price, allowing more immediate access to a property without hefty upfront costs.

2. Monthly Payments Application:

- For traditional buyers, monthly mortgage payments go directly toward principal and interest. In rent-to-own arrangements, a portion (which can be up to 30%) of your monthly rent may be applied toward the purchase price, which is not a feature available in standard mortgage agreements.

3. Financial Risk and Equity Building:

- With traditional purchase methods, you start building equity as soon as you make a payment. However, in a rent-to-own scenario, it might take longer to see significant equity build-up if the rent credit is minimal or if the agreement has a lengthy rental period.

Comparative Table

| Factor | Rent to Own | Traditional Purchasing |

|---|---|---|

| Down Payment | 1% - 5% of purchase price | 3% - 20% of purchase price |

| Monthly Payments | Includes rent credit portion | Directly toward loan principal |

| Equity Building | Slower with a rental period | Immediate with mortgage payments |

| Maintenance Responsibilities | Often handled by renter | Typically the homeowner’s responsibility |

| Flexibility | Allows you to walk away | Contractual obligations to continue |

Real-World Examples

In a real-world scenario, consider Maria, who opted for a rent-to-own agreement with an option fee of 3% on a $300,000 home. She benefits from her monthly payments contributing 20% toward the purchase price, accumulating equity while living in the home. On the other hand, Chris chose to buy a home traditionally, paying a 20% down payment and significantly higher monthly mortgage payments but immediately started building equity without restrictions on leaving the property.

Practical Implications for Readers

When evaluating your options, consider your current financial situation and long-term goals. If you have limited savings for a down payment or need time to improve your credit, rent-to-own could be appealing. On the contrary, if you’re ready for the commitment and want to build equity efficiently, traditional purchasing may fit your needs better.

Actionable Advice

- Assess your financial readiness and long-term plans. If flexibility is paramount, rent-to-own may suit you well.

- Calculate potential costs over time for both paths. You could discover that the rent credits in a rent-to-own agreement help bridge gaps in your savings for a future purchase.

- Research local market rates and trends to weigh how traditional purchase prices compare against rental costs in your preferred areas.