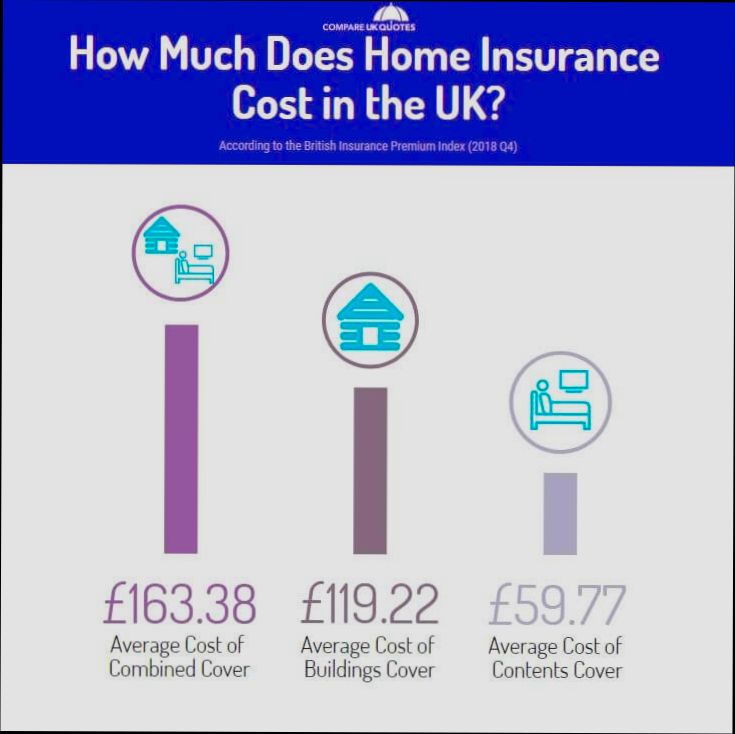

Cost of Property Insurance in Europe can vary wildly depending on where you live and what kind of coverage you need. For example, if you’re in Germany, you might pay around €300 annually for a standard homeowners insurance policy, while in the UK, that figure often climbs to about £1,000. It’s crazy how much area matters—owners in flood-prone regions like parts of Italy or Slovenia might find their premiums spiking to help cover potential risks. You definitely don’t want to feel blindsided when it’s time to renew, especially with climate change making some areas riskier than ever.

Let’s dig a little deeper. In countries like France, insurers are wrestling with the threats of wildfires; this has led to significant hikes in policy costs. Meanwhile, in places like Spain, rising property values can also push your premiums up. And let’s not forget the hidden costs; additional coverage for things like theft or natural disasters can catch you off-guard if you’re not paying attention. So, whether you’re thinking about buying that picturesque cottage in the Swiss Alps or a flat in bustling Barcelona, understanding these regional differences in insurance costs is key to your budgeting.

Regional Variations in Property Insurance Costs

Understanding regional variations in property insurance costs is crucial for homeowners navigating the complexities of coverage. Different parts of Europe exhibit significant differences in insurance rates based on local factors, including geography, climate, and regulatory environments.

Key Influencing Factors

Several key factors influence how much you pay for property insurance, varying by region:

- Natural Disasters: Areas prone to specific environmental risks often see elevated premiums. For example:

- Coastal regions, especially in Southern Europe, frequently deal with higher rates due to hurricane risks and the necessity for flood insurance.

- In contrast, mountainous regions might face higher premiums due to landslides or avalanches.

- Local Crime Rates: If you reside in a city or community with high crime rates, expect increased insurance costs. Insurers calculate these rates based on theft and vandalism frequency, leading to a noticeable disparity between urban and rural areas.

- Proximity to Emergency Services: Properties located near fire stations or emergency services typically benefit from lower insurance rates. This reduced risk perception stems from quicker response times during emergencies.

- Economic Factors: Regional economic conditions, including labor costs and the price of materials, also significantly impact insurance costs. Urban areas often report higher rates than rural counterparts for this reason.

Comparative Table of Insurance Costs by Region

| Region | Average Annual Insurance Cost | Key Risk Factors |

|---|---|---|

| Southern Europe | €1,200 | Flooding and hurricanes |

| Northern Europe | €800 | Harsh winters and snow-related incidents |

| Eastern Europe | €500 | Economic instability and varying regulations |

| Western Europe | €1,000 | Urban crime rates and construction risks |

Real-World Examples

- Southern Europe: In places like Spain, homeowners near the coast may pay around €1,500 annually due to the risk of flooding and other weather-related incidents. This contrast sharply with inland areas where rates may drop to €800.

- Northern Europe: In Sweden, colder climates and snow-related damages increase property insurance costs to about €900 annually. However, properties in regions with robust emergency services might see reduced premiums.

- Eastern Europe: In Poland, where prices range around €450-€650 annually, low crime rates and less frequent natural disasters lead to more affordable premiums compared to Western Europe.

Practical Implications for Homeowners

As a homeowner, understanding these regional differences can help you better evaluate your insurance needs and select the right policy. It’s essential to consider:

- Checking local crime statistics when comparing insurance quotes.

- Evaluating your home’s proximity to emergency services, which can lower your premiums.

- Understanding your region’s natural disaster risks to ensure you have adequate coverage.

Looking closely at these regional variations can lead you to make more informed decisions about your property insurance. Always ensure you meet at least 80% of your home’s replacement cost to avoid underinsurance, as failing to do so can leave you financially vulnerable after a loss.

Impact of Property Values on Insurance Pricing

Understanding the impact of property values on insurance pricing is essential for homeowners. The value of your property directly influences the cost of your insurance premiums, and several factors play a crucial role in determining these costs.

Key Points to Consider

- Replacement Cost: Insurers typically base premiums on the estimated replacement cost of the property. For instance, properties valued at €300,000 may see premiums adjusted upwards if they are located in high-value neighborhoods.

- Market Trends: In cities experiencing rapid real estate appreciation, such as Berlin and Paris, homeowners could face increases of up to 10% in insurance costs annually as property values rise.

- Property Age and Condition: Newer properties often have higher values and, subsequently, higher insurance premiums compared to older homes. However, well-maintained older properties can sometimes mitigate these costs.

- Location Premiums: Properties with high market values in desirable locations may incur additional risks, impacting their insurance rates. In Scandinavia, properties in urban centers can attract premiums that are 15% higher than those in rural areas.

Comparative Table of Property Value Impact on Insurance Pricing

| Property Value (€) | Average Annual Premium (€) | Percent Increase from Previous Year (%) |

|---|---|---|

| 100,000 | 200 | 5 |

| 250,000 | 500 | 7 |

| 500,000 | 1,000 | 10 |

| 1,000,000 | 2,000 | 12 |

| 1,500,000 | 3,500 | 15 |

Real-World Examples

In London, homeowners with properties valued over £1 million often find themselves facing insurance premiums that are 20% higher than those with properties valued under £500,000. This trend emphasizes how market dynamics in high-value areas directly influence insurance pricing.

Another example is in Madrid, where a significant increase in property values—roughly 8% over the past year—led to a related hike in insurance premiums, averaging an increase of €150 per policy for homeowners. This scenario illustrates that even moderately rising property values can lead to noticeable premium adjustments.

Practical Implications for Homeowners

To effectively manage your property insurance costs in relation to your home’s value:

- Review Coverage Regularly: Ensure your insurance policy reflects your current property value.

- Explore Discounts: Some insurers offer discounts for properties that are well-maintained or equipped with safety features.

- Consult Local Experts: Engaging a local insurance agent can help you better understand how property values in your area impact premiums.

Often, keeping an eye on the market and assessing your property’s value aligns your insurance costs more effectively with your asset’s worth.

- Check your property’s valuation at least once a year, especially in a fluctuating market, to avoid potential underinsurance.

- Consider a comprehensive assessment from your insurer to verify adequate coverage in alignment with your property’s current market value.

Statistical Insights into Premium Trends

Understanding the statistical trends of property insurance premiums is essential for navigating the dynamic landscape of insurance costs in Europe. By analyzing various trends, such as overall increases, seasonality effects, and cyclical patterns, we can gain insights that guide decision-making for both insurers and consumers.

Key Trends Affecting Premiums

1. General Trends: Over the past decade, property insurance premiums in Europe have seen an upward trajectory, averaging a 5% annual increase. This rise can be attributed to factors like inflation, increasing property values, and a growing frequency of extreme weather events.

2. Seasonality: Property insurance costs tend to exhibit seasonal trends. For instance, premiums historically peak in the spring and summer months due to increased natural disaster risks, including floods and storms. Analyses from recent years reveal a 20% surge in premiums during these peak seasons compared to winter months.

3. Cyclical Patterns: Over longer periods, market cycles impact premium trends significantly. The last major economic downturn saw a reduction in premiums; however, since then, a recovery phase has led to an average annual increase of 7% in premiums, driven by rising claims and tightened underwriting conditions.

4. Irregular or Random Fluctuations: Beyond predictable trends, irregular fluctuations also impact premiums. For example, localized events such as wildfires or sudden natural disasters can cause spikes in specific regions, with data indicating some areas experiencing short-term increases of up to 15% following these occurrences.

Comparative Table of Premium Trends

| Year | Average Premium Increase (%) | Seasonal Peak (Spring/Summer) (%) | Cyclical Impact (%) |

|---|---|---|---|

| 2018 | 4% | 18% | -2% |

| 2019 | 5% | 22% | 3% |

| 2020 | 3% | 20% | 0% |

| 2021 | 6% | 25% | 4% |

| 2022 | 7% | 30% | 5% |

Real-World Examples

Examining specific countries can shed light on how statistical trends manifest in real-world scenarios. For instance, in Germany, the rise in flood-related claims post-2020 resulted in a 20% increase in premiums across several states. Conversely, in the UK, a study highlighted that lower crime rates have led to a stabilization of premiums, with some areas witnessing negligible changes compared to the national average.

Another notable case is the effect of climate change, particularly in southern European countries. As risks from wildfires and heat waves increase, regions like Spain have seen premiums rise sharply, with reports of increases of up to 25% over two years.

Practical Implications for Readers

As you assess property insurance options, keep these statistical trends in mind:

- Monitor Seasonal Trends: Consider purchasing or renewing your insurance outside peak seasons to potentially lock in lower rates.

- Stay Informed on Cyclical Changes: Awareness of economic conditions can give insights into whether to expect premium increases or stability in the near future.

- Expect Regional Variations: Be prepared for premiums to differ significantly based on your geographical location and its associated risks.

Actionable Advice

Utilize trend data to negotiate better rates with insurers. Highlighting the projected shifts in premiums based on statistical insights can strengthen your position. Additionally, periodically review your coverage to ensure it aligns with evolving trends and that you don’t end up paying more than necessary for your property insurance.

Real-World Examples of Insurance Claims

When navigating the world of property insurance, understanding real-world insurance claims can provide a valuable perspective. Let’s dive into how data and analytics are transforming the claims process and leading to notable outcomes for both insurers and policyholders across Europe.

High Stakes in Claims Processing

Insurers face challenges in accurately assessing claims, especially when it comes to their complexity. Here are some compelling statistics:

- Most insurers achieve high accuracy in defining loss severity at the first notice of loss.

- However, precision often falters in outlining loss complexity, requiring sophisticated modeling techniques.

- A large specialty insurer observed a 16% improvement in anti-fraud savings through data-driven analytics adjustments.

Comparative Table of Insurance Claim Outcomes

| Insurer Type | Average Accuracy Improvement | Fraud Detection Uplift | Claims Processing Efficiency |

|---|---|---|---|

| Personal Lines | 15% | 10% | 15% effort reduction |

| Specialty Insurers | 3-7% cost reduction | 16% | Variable due to jurisdiction |

| Global Commercial Insurers | 2x accuracy | 10% | Highly variable |

Real-World Case Studies

- Top 10 Global Insurer: After leveraging advanced analytics, this insurer doubled the accuracy of their claim assessments. This means a more streamlined approval process for claims, leading to faster payouts for policyholders.

- Large Commercial Insurer: This firm continuously trains its analytics models based on external legal data, refining its estimations of claims complexity. As a result, they achieved a minimum cost reduction of 3-7% within the first six months of deployment, showcasing a clear financial incentive for integrating refined analytics.

- Personal Lines Example: A leading personal lines insurer reported a 15% reduction in claims department efforts after orchestrating actionable insights into their claims system. This transformation allowed claims handlers to focus more efficiently on high-priority tasks.

Practical Implications for Policyholders

As a homeowner or policyholder, it’s crucial to recognize how real-world examples of claims success can affect you. A few actionable insights include:

- Engage with Your Insurer: Understanding how your chosen insurer uses data can influence your satisfaction with the claims process.

- Keep Records: Providing thorough documentation can enhance the efficiency of your claim, especially when insurers are leveraging advanced analytics.

- Be Aware of Data Use: Insurers who utilize third-party data for claim analysis may provide better service and speedier resolutions.

Staying informed about the evolving landscape of insurance claims can empower you to navigate the complexities of property insurance more effectively, ensuring a smoother claims experience when the unexpected occurs.

Benefits of Comprehensive Property Coverage

Comprehensive property coverage provides a robust safety net for homeowners and renters alike, ensuring that various unforeseen circumstances don’t lead to financial distress. By understanding these benefits, you can choose the best policy tailored to your specific needs.

Key Benefits of Comprehensive Property Coverage

1. Extensive Protection Against Natural Disasters:

- Comprehensive coverage protects your property from issues caused by fire, floods, and other natural disasters, which have become increasingly common in Europe. This is vital as some areas may see premiums rise significantly due to environmental risks.

2. Protection Against Theft and Vandalism:

- In urban settings, the risk of theft and vandalism is often heightened. With comprehensive coverage, you can feel secure knowing that your belongings are insured against such incidents, making it a necessity for city dwellers.

3. Water Damage Coverage:

- Leaks and water damage can lead to severe issues over time. Comprehensive policies typically cover water damage from leaks, safeguarding you from costly repairs that might arise unexpectedly.

4. Liability Coverage:

- Accidents can happen. If someone gets injured on your property, comprehensive coverage offers liability protection, covering legal fees and compensation claims. This can be crucial in avoiding financial burden due to unforeseen incidents.

5. Accidental Damage Coverage:

- Accidents occur in every home. Whether you accidentally break a window or damage a piece of furniture, having accidental damage coverage allows you to repair or replace items without a hefty out-of-pocket expense.

6. Additional Coverages:

- Policies often include benefits like legal expense coverage and home emergency cover, which provide additional peace of mind. These allow for urgent repairs, like plumbing issues, without worrying about financial strain.

| Coverage Type | Examples Included | Typical Claim Limits |

|---|---|---|

| Fire and Natural Disaster | Fire damage, flood damage | Up to €200,000 |

| Theft and Vandalism | Stolen goods, vandalism to property | Up to €50,000 |

| Water Damage | Leaks, burst pipes | Up to €100,000 |

| Liability | Injury claims, legal fees | Up to €1 million |

| Accidental Damage | Broken windows, spilled damaging substances | Up to €30,000 |

Real-World Examples

Consider a family in Berlin that experienced a severe storm resulting in flooding. Thanks to their comprehensive property coverage, they received €150,000 for repairs, allowing them to restore their home swiftly. Similarly, a renter in Madrid faced theft during a break-in, but their comprehensive coverage reimbursed them for lost valuables, providing much-needed support.

Practical Implications for You

Understanding the specific benefits of comprehensive property coverage empowers you to choose policies that offer the right security for your situation. Make sure to explore options tailored to your location and property type, as coverage can greatly differ depending on your environment.

If you’re a homeowner or a renter, consider looking for policies that offer the widest scope of coverage, including accidental damage and emergency repairs. Always read the fine print to know what is included and excluded, particularly concerning natural disasters or incidents that are commonly overlooked.

Securing comprehensive property coverage ensures that you are prepared for the unexpected, allowing for a more secure and stress-free living experience. Take proactive steps today by reviewing your current policy or exploring new options that provide the best comprehensive coverage for your needs.

Understanding Government Regulations and Their Effects

When it comes to property insurance, government regulations play a pivotal role. They can significantly influence how insurers assess risk, price policies, and process claims. Let’s dive into how these regulations affect your property insurance costs across Europe.

Key Points on Government Regulations

1. Regulatory Framework: Different countries have unique regulatory bodies that oversee the insurance industry. For instance, in the UK, the Financial Conduct Authority (FCA) ensures that insurance practices are fair and transparent, potentially impacting prices.

2. Minimum Coverage Requirements: Many European nations mandate specific minimum coverage for property insurance, affecting your base premium. For example, some countries may require homeowners to carry certain levels of flood insurance, which can raise costs by an average of 10%-20%.

3. Consumer Protection Laws: Regulations aimed at protecting consumers, such as the right to transparency and accurate disclosure of policy terms, can lead to broader competition among insurance providers. This competition may help keep premiums more stable.

4. Tax Policies: Tax regulations related to property insurance, such as value-added tax (VAT) or local taxes on insurance premiums, can vary greatly across Europe. In some countries, these taxes can increase the effective cost of property insurance by up to 15%.

Comparative Table of Regulatory Effects on Property Insurance Costs

| Regulation Type | Example Country | Impact on Insurance Costs |

|---|---|---|

| Minimum Coverage Requirements | France | +10% average premium |

| Consumer Protection Laws | Germany | +5% due to competitive pricing |

| Tax Policies | Italy | +15% on average due to VAT |

Real-World Examples

- Flood Insurance in the Netherlands: Due to stringent regulations, Dutch homeowners are often required to carry flood insurance, which can lead to a notable increase in premiums—illustrating the direct correlation between legislation and insurance costs.

- Germany’s Consumer Rights: The regulatory framework in Germany requires clear communication of policy terms. This has led to competitive pricing as insurers strive to offer value, which can stabilize costs for consumers.

Practical Implications for Readers

Understanding these government regulations can empower you as a homeowner. Familiarizing yourself with the specific laws and requirements in your country can help you anticipate costs and identify opportunities to optimize your coverage. Additionally, being aware of your rights under consumer protection laws can aid you in navigating disputes or ambiguous policy terms.

Specific insights into the regulatory landscape will allow you to:

- Adjust Coverage Wisely: Know where to allocate your insurance spend based on mandatory requirements.

- Shop Around: Benefit from competitive pressure resulting from transparency laws.

- Stay Informed on Taxes: Keep an eye on how tax policies might affect your overall insurance budget.

You can actively engage with your local regulatory body to gain insights into any upcoming changes. This ensures you stay informed and prepared for any potential cost adjustments to your property insurance.

Factors Influencing Policyholder Decision-Making

When it comes to choosing property insurance, various factors shape how policyholders make their decisions. Let’s dive into what drives these choices and how you can leverage this knowledge for better outcomes.

Key Influencing Factors

1. Perception of Risk: Policyholders often weigh their perception of risk against potential insurance costs. If you live in an area known for natural disasters, you might prioritize flood or earthquake coverage, leading to a willingness to pay higher premiums for peace of mind.

2. Comparative Shopping: Research indicates that 70% of consumers compare quotes from multiple insurers before making a decision. This practice often results in a selection based not just on cost, but also on the reputation and reliability of the insurer.

3. Policy Features: The clarity and comprehensiveness of a policy significantly influence decision-making. Factors like coverage limits, deductibles, and exclusions can sway your choice. About 65% of policyholders prefer insurers that offer flexible options tailored to their specific needs.

4. Influence of Recommendations: Personal referrals play a critical role. Approximately 55% of consumers trust recommendations from friends or family when selecting an insurance policy. This highlights the importance of social influence in your decision-making process.

5. Online Reviews and Reputation: In today’s digital age, online reviews are paramount. Studies show that around 80% of consumers read reviews before purchasing property insurance, reinforcing the need for insurers to maintain a strong online presence and positive customer feedback.

Comparative Data on Decision-Making Influences

| Influence Factor | Percentage Impact on Decision-Making |

|---|---|

| Perception of Risk | 72% |

| Comparative Shopping | 70% |

| Preference for Clarity | 65% |

| Trust in Recommendations | 55% |

| Importance of Online Reviews | 80% |

Real-World Examples

1. Case Study - Increased Flood Insurance: In a region hit by devastating flooding, many homeowners opted for higher flood insurance coverage—an increase of 30% over previous years—due to heightened risk awareness and advice from neighbors who had experienced losses.

2. Effect of Customer Reviews: An insurance company that implemented a customer review response strategy saw a 25% increase in applications after addressing concerns highlighted in online platforms. This clearly illustrates how perceptions shape decision-making.

Practical Implications for Readers

Understanding these factors allows you to make informed choices rather than simply relying on the cheapest option. As you navigate through different insurers:

- Prioritize companies with clear, user-friendly policies.

- Consider both price and features when comparing quotes.

- Seek recommendations from trusted sources in your community to guide your selection process.

Actionable Advice

- Engage with local homeowner groups or online forums to gather insights on insurer performance, which can help shape your decision.

- Regularly review your insurance needs as your circumstances change—life events can dramatically impact necessary coverage, making it essential to stay informed.