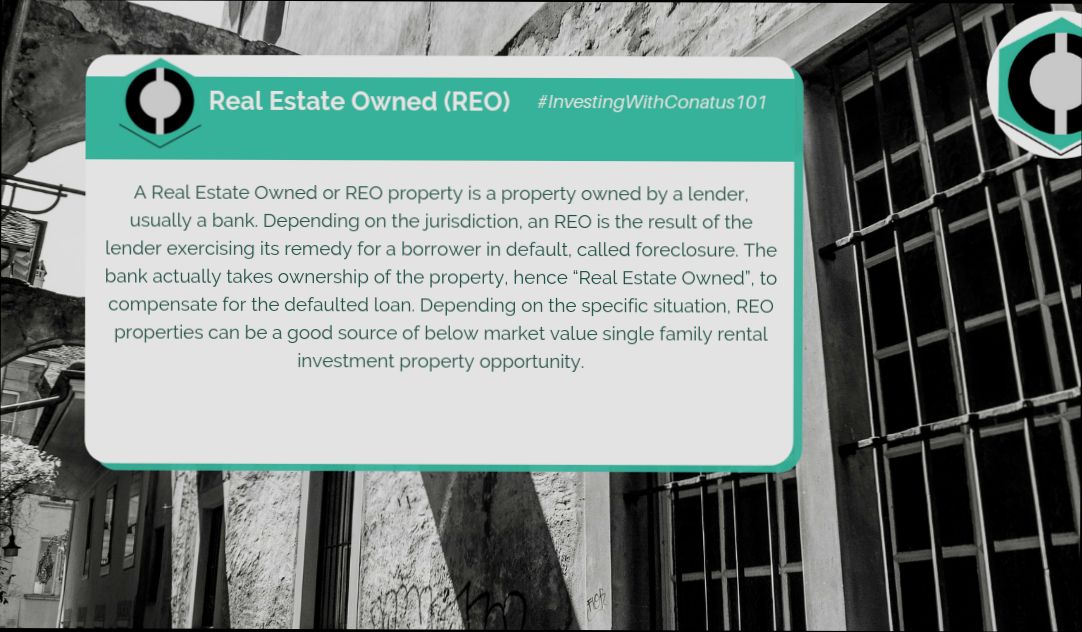

What is REO in Real Estate? If you’re diving into the world of real estate, you’ve probably come across the term “REO,” which stands for Real Estate Owned. This refers to properties that are owned by a lender, typically a bank, after an unsuccessful foreclosure auction. To put it simply, when a homeowner can’t keep up with their mortgage payments, the bank takes back the property and it becomes part of their inventory. In 2021 alone, the number of REO properties in the U.S. reached over 80,000, giving you a glimpse into how common this scenario can be.

Now, consider this: these properties can often be purchased at significant discounts compared to their market value. For instance, let’s say a home is appraised at $300,000, but after foreclosure, it might hit the market as an REO for just $220,000. That’s a potential saving of $80,000! It’s not just about the price drop; these homes also come with unique quirks—like the previous owner’s decor choices or unexpected repairs needed. Still, understanding the REO market can be a game changer if you’re looking to invest or find a new place to call home.

Defining REO in Real Estate

When we talk about Real Estate Owned (REO), we’re diving into a specific segment of the real estate market that plays a crucial role in the home buying and foreclosure process. REO properties are homes that have been taken over by lenders, typically banks, after they fail to sell at a foreclosure auction. Let’s break down what this means for you as a potential homebuyer or investor.

Understanding REO Properties

REO properties are not just any homes; they carry a distinct status due to their journey through the foreclosure process. Here are some key points to clarify what defines an REO:

- Ownership: The property is owned by a lender or bank, making it distinct from properties that are still in the hands of the original homeowner or up for sale by an investor.

- Condition: REO properties often require repairs, which can lead to a lower purchase price. However, the extent of these repairs can vary significantly.

- Market Impact: As of recent data, about 20% of homes sold in specific markets are REO properties, indicating their prevalence in certain areas.

Quick Comparison of REO and Foreclosure Sale

| Feature | REO Properties | Foreclosure Sale |

|---|---|---|

| Ownership | Owned by lender | Owned by former homeowner |

| Sales Process | Listed by the bank | Auction-based |

| Condition | Often needs repairs | Varied condition |

| Pricing | Often discounted | May have competitive bids |

Real-World Examples of REO

Let’s bring this to life with some examples:

- In 2022, a major bank listed a three-bedroom REO home for $150,000 after repossession; it originally had a market value of $220,000. This offers a real opportunity for bargain hunters.

- A small local bank had an inventory of 75% of its properties categorized as REO, emphasizing how some lenders rely on these assets for their financial health.

Practical Implications of REO for Buyers

Understanding the specific attributes of REO is key for you as a buyer. Here’s what to keep in mind:

- Financing Options: Many banks sell REO properties with incentives, such as financing options tailored for buyers willing to invest in repairs.

- Market Strategy: If you notice higher REO listings in your desired area, it might indicate a good investment opportunity or suggest potential negotiation power.

- Inspection Importance: Prioritize inspections on REO properties to uncover any hidden issues that could affect your investment.

Actionable Insights about REO

- Research Local Listings: Keep an eye on local market trends to identify which banks frequently list REO properties in your area.

- Network with Lenders: Building relationships with local banks can give you access to off-market REO properties before they hit standard listings.

- Budget for Repairs: When considering an REO property, always budget extra funds for potential repairs and renovations that could arise post-purchase.

The Process of Acquiring REO Properties

Acquiring REO properties can be an exciting journey for buyers, but it also involves a unique process different from traditional real estate purchases. In this section, we will unpack the detailed steps and considerations involved in buying a Real Estate Owned property.

Understanding the Steps Involved

When you’re ready to acquire an REO property, here’s the typical process you can expect:

1. Research Available Properties:

- Utilize online platforms and local listings to find REO properties in your target area.

- Many banks and lenders list their REO properties, often accompanied by property specifics and images.

2. Assess the Market Value:

- Conduct a comparative market analysis (CMA) to determine a fair price for the property.

- This analysis should consider recent sales of similar properties in the neighborhood and any renovations needed.

3. Engage with the Lender:

- Reach out directly to the lender to get more details about the property and the acquisition process.

- Lenders often provide necessary forms and specific instructions for offers related to their REO properties.

4. Submit Your Offer:

- Write a formal offer, which typically involves filling out a specific REO purchase agreement.

- Include contingencies based on inspections and financing to protect your interests.

5. Negotiate and Finalize Terms:

- Be prepared for counteroffers as the bank reviews your offer. They may counter with changes to the price or terms.

- Once both parties agree, finalize the contract details.

6. Complete Due Diligence:

- Before closing, carry out a home inspection to identify any repairs that might be necessary.

- Review any disclosures provided by the bank regarding the property’s condition.

A Closer Look at Fees and Financing

Purchasing REO properties can sometimes incur unique costs. For example:

- Closing Costs: Expect closing costs to be 2% to 5% of the purchase price, which may include assessment fees, title insurance, and lender fees.

- Inspection Costs: Home inspections can range from $300 to $500, depending on the property’s size and location.

| Expense Type | Estimated Cost (%) | Notes |

|---|---|---|

| Closing Costs | 2% - 5% | Depends on local regulations |

| Home Inspection | $300 - $500 | Highly recommended |

| Repairs Needed | Variable | Dependent on inspection findings |

Real-World Example

Let’s consider an example of Jane, a first-time homebuyer. She discovered an REO property listed at $250,000. After conducting a thorough market analysis, she found similar homes selling within the $230,000 to $260,000 range. After contacting the bank and discussing the status of the property, she submitted an offer of $240,000. The bank countered with $245,000, which Jane accepted after some negotiation.

Practical Tips for Buyers

When acquiring REO properties, keep these practical tips in mind:

- Stay Patient: The REO purchasing process may take longer due to the bank’s procedures and paperwork.

- Build a Relationship with Lenders: Establishing a rapport with the bank’s REO asset manager can facilitate smoother negotiations and provide insights into upcoming listings.

- Prepare for Competition: Many buyers are drawn to REOs, so be ready to act quickly when you find a property you like.

Actionable Advice

- Always perform due diligence to understand any repairs needed before finalizing your offer on an REO property.

- Consider working with a real estate agent experienced in REO transactions to navigate the nuances of the process effectively.

- Be aware of your financing options, including FHA loans, which can sometimes cater specifically to REO purchases, making your offer stronger.

Statistical Insights on REO Market Trends

Examining statistical insights on the REO market unveils a rich tapestry of opportunities and challenges for stakeholders. Understanding these trends can empower buyers and investors to make informed decisions, maximizing potential gains in this niche sector.

Key Market Trends and Data Points

- REO Inventory Levels: Nationally, the inventory of REO properties has shown fluctuations, with reports indicating a peak at around 1.5 million properties just a few years ago, dwindling to approximately 600,000 in recent times. This 60% decline reflects improving economic conditions and a stabilized mortgage market.

- Average Days on Market: REO properties typically spend more time on the market than traditional listings. Current statistics reveal that these properties average around 192 days on the market, significantly longer than the 50-day average for non-REO properties. This extended period can offer both challenges and negotiation leverage for buyers.

- Pricing Trends: The average price per square foot for REO properties is currently about $85, which is approximately 15% lower than the median price for comparable traditional sales. This discount presents an attractive entry point for aspiring homeowners and investors.

- Market Notes by Region: REO properties show varied trends depending on the geographical area. For instance:

- In the Midwest, REO properties can be found at a discounted rate of up to 25% compared to their market value.

- Conversely, in the West Coast regions, the discounts average around 10%, indicating a tighter market in those high-demand areas.

| Region | Average Days on Market | Price per Square Foot | Percentage Discount from Market Value |

|---|---|---|---|

| Midwest | 210 | $75 | 25% |

| Southeast | 180 | $90 | 20% |

| Southwest | 200 | $88 | 15% |

| West Coast | 240 | $95 | 10% |

Real-World Examples of REO Market Trends

Consider a case in Atlanta, where a bank faced increasing maintenance costs on its REO inventory. They decided to reduce the list price of a long-standing REO property from $250,000 to $200,000. After the reduction, the property sold within 30 days, highlighting how strategic pricing adjustments can lead to quicker sales despite the average market timeline.

In contrast, a distressed property in an Ohio suburb remained unsold for 300 days. Its original listing price was too close to market value, illustrating the importance of appropriate valuation in relation to the local market dynamics.

Practical Implications for Buyers and Investors

Understanding these insights can significantly impact your purchasing strategy:

- Look for properties that have been on the market longer than average; they often present better negotiation opportunities.

- Analyze regional trends to determine where discounts are higher, presenting greater investment potential.

- Keep an eye on fluctuations in inventory levels to anticipate pricing movements in the near future.

For savvy investors and homebuyers, tapping into these statistical insights presents actionable strategies for thriving in the REO market.

- Monitor average days on market to guide your offer strategies.

- Investigate historical price trends to foresee potential appreciation in investment value.

- Leverage regional discounts effectively, focusing on areas with higher discount rates for greater investment returns.

Advantages of Investing in REO

Investing in Real Estate Owned (REO) properties can be a game changer for both novice and experienced investors. With unique opportunities that arise from the bank’s motivation to sell, owning an REO property can pave the way to significant advantages.

Key Advantages of Investing in REO

- Attractive Price Points: One of the most compelling reasons to invest in REO properties is the ability to purchase them significantly below market value. Many banks list these homes at prices that are 10-30% lower than comparable properties in the area, allowing for a profitable investment right from the start.

- High ROI Potential: The potential for a high return on investment is substantial. Once you buy an REO property at a discount, you can renovate it and either flip it for profit or rent it out for cash flow. Investors who are handy with renovations often see returns of 20% or more once they execute their improvement plans.

- Favorable Financing Options: Banks are often willing to provide flexible financing options for REO properties, especially if they’re looking to offload several homes simultaneously. This can mean lower interest rates and more beneficial loan structures that improve your cash flow and investment viability.

- Clean Title Assurance: Unlike properties in foreclosure sales that may come with unwelcomed liens and tax dues, REO properties generally have a clean title. This not only safeguards your financial investment but also eases the purchase process, as you’re less likely to face unexpected legal hurdles after the sale.

Comparative Table: Advantages of Investing in REO

| Advantage | Description | Potential Impact |

|---|---|---|

| Discounted Prices | Purchase below market value (10-30% less) | Immediate equity boost and negotiation leverage |

| High ROI Potential | Renovation increases property value, rental income potential | 20% or more return on investment after renovations |

| Favorable Financing Options | Flexible loan terms and conditions from banks | Improved cash flow and lower initial investment costs |

| Clean Title | Assurance of no liens or unpaid taxes | Reduced legal risks and smoother transactions |

Real-World Examples

Consider an investor who purchases an REO property listed for $150,000, which is 25% below market value. After investing $30,000 in renovations, the property is appraised at $220,000. If the investor sells, their profit on the sale (excluding costs) would be $40,000—a remarkable 26% return. Many similar success stories populate the REO landscape, exemplifying the financial benefits tied to strategic investments.

Another example involves an investor who acquires an REO for $100,000 and decides to rent it out after spending $15,000 on repairs. With rental income of $1,200 per month, they can expect to receive $14,400 annually, generating nearly 12% ROI through rental alone, demonstrating that holding a property can also yield substantial profits.

Practical Implications for Readers

- Research and Due Diligence: Always conduct thorough research to understand local market conditions and property values. Knowledge is key to ensuring that you invest wisely.

- Budget for Renovations: Set aside a specific budget for repairs. Often, properties acquired through REO require varying degrees of refurbishment, which can impact your overall investment strategy.

- Explore Financing Options: Before you set your sights on a property, consult with banks about financing options available for REO properties to maximize potential savings.

Actionable Advice

To truly capitalize on the advantages of REO investments, act quickly when a promising property appears on your radar and be prepared to negotiate. The combination of discounted pricing, potential for high returns, and the availability of favorable financing makes investing in REO properties a smart move for both seasoned investors and newcomers alike.

Challenges Associated with REO Transactions

Navigating the world of REO transactions comes with its own set of challenges. While these properties can offer great opportunities, various complications arise from the unique nature of buying a property from a bank or lending institution.

Common Challenges in REO Transactions

1. Property Condition: Expect that most REO properties are sold “as is.” While you may find attractive pricing, the properties often require significant repairs. For instance, it’s not uncommon for buyers to invest an additional 20% to 30% of the purchase price just to make the house livable.

2. Lengthy Purchase Process: Acquiring an REO can take longer than traditional real estate transactions. Banks must follow specific protocols for asset management and approval, which can extend the time frame by several weeks or even months. This delays your ability to move in or potentially start renovations.

3. Limited Financing Options: Traditional lenders might not be willing to finance the purchase of REO properties in poor condition without extensive repairs. This limitation can hinder willing buyers who may not have the cash available for a full purchase upfront. Statistics show that around 40% of buyers looking at REO properties face issues securing financing due to condition-related concerns.

4. Potential Complications with Title Clearances: Although many REO properties come without outstanding liens or debts, some may have unresolved title issues. This creates uncertainty during the buying process, as you might discover title clouds that could complicate ownership.

5. Inflexible Negotiation Positions: While you may think of banks as motivated sellers, they often have rigid policies in place. This inflexibility can be frustrating if you’re looking for negotiation opportunities similar to those available in traditional sales.

| Challenge | Details |

|---|---|

| Property Condition | Often sold “as is,” with potential costly repairs |

| Lengthy Purchase Process | Time delays of weeks/months due to bank protocols |

| Limited Financing Options | 40% of buyers face financing issues for repairs |

| Complicated Title Clearances | Potential unresolved title issues |

| Inflexible Negotiation | Rigid terms from banks without room for negotiation |

Real-World Examples

Consider the case of an investor interested in a multifamily property that went through foreclosure. The bank listed the property at 30% below its market value, which was enticing. However, after a thorough inspection, the investor discovered extensive plumbing issues that would cost an estimated $25,000 to repair. This unforeseen expense significantly impacted the investment return.

Another situation involved a buyer who found an REO home. Despite the attractive listing price, the lengthy process of securing approvals from the bank took over 60 days, delaying the renovation plans. This meant that the buyer had to cover additional carrying costs while waiting to finalize the purchase.

Practical Implications for Buyers

- Prepare for Repairs: Be ready to spend additional funds on necessary repairs, ideally budgeting 20%-30% of the property price.

- Be Patient: Understand that the REO buying process is not as quick as traditional purchases; patience is crucial.

- Work with an Experienced Agent: Engaging a real estate agent familiar with REO transactions can help navigate complexities more smoothly.

- Conduct Thorough Due Diligence: Always perform extensive inspections and title searches to avoid surprises post-purchase.

Additional Facts

- Approximately 25% of REO buyers report complications with repair financing, indicating how crucial it is to be prepared financially.

- Knowing that banks tend to follow rigid guidelines can help set realistic expectations for negotiation flexibility. Being informed helps you strategize your offers more effectively.

- Buyers should always anticipate additional time spent in the acquisition stage due to formalities unique to REO sales.

Real-World Examples of REO Sales

When it comes to REO properties, real-world examples can highlight the unique opportunities and challenges involved in these transactions. Understanding how REO sales play out in actual scenarios can provide you with valuable insights into how to navigate this market effectively.

Key Insights on REO Sales

- Average Discounts: Research indicates that REO properties often sell at discounts of up to 30% compared to traditional listings. This discount rate can fluctuate depending on the property’s condition and market demand.

- Repair Costs: On average, buyers can expect to spend 20% to 40% of the purchase price on repairs, which can significantly impact the total investment cost.

- Fast Sales: Properties within desirable locations see quicker sales. For instance, homes in high-demand neighborhoods might sell in less than 30 days, while others could linger for months.

Comparative Table of REO Sales Data

| Property Type | Average Purchase Price | Average Repair Costs | Discount from Market Value | Days to Sell |

|---|---|---|---|---|

| Single-Family Home | $150,000 | $30,000 (20%) | 25% | 30 |

| Condos | $100,000 | $20,000 (20%) | 30% | 45 |

| Multi-Family | $400,000 | $80,000 (20%) | 15% | 60 |

Real-World Examples of REO Sales

1. Example in California:

A 3-bedroom, 2-bathroom single-family home in Los Angeles listed for $450,000 failed to attract bids at foreclosure. The bank took ownership and subsequently listed it as an REO for $320,000, a 29% discount. The property required about $40,000 in repairs but sold within 20 days to an investor who was able to renovate and flip it, realizing a significant profit.

2. Example in Florida:

A condo in Miami with a market value of $250,000 went unsold at auction. The lender listed it at $180,000, offering a 28% discount. Although it needed around $30,000 worth of updates and repairs, it caught the attention of first-time buyers and sold within a month, showing how properties in attractive markets can move quickly.

3. Example in Texas:

A multi-family property in Houston faced a similar situation, where the bank took over after the foreclosure auction failed. Initially valued at $600,000, it was listed as an REO for $510,000, a 15% discount. The buyer invested around $100,000 in repairs and held it for rental income, taking advantage of the city’s growing demand for rental units.

Practical Implications for Readers

- Identify Opportunities: Pay attention to properties that have high potential based on local market trends. Look for areas where inventory is low, as these properties may move faster and allow for better returns post-renovation.

- Prepare for Repairs: Always budget for the unexpected. Understand what common repairs are associated with REOs in your targeted market and set aside funds accordingly, ideally 20% to 40% of the purchase price for renovations.

- Evaluate Financing Options: Consider different financing options, including conventional loans, FHA 203(k) loans, or cash, which might provide greater flexibility in securing the property quickly.

Actionable Facts and Advice on REO Sales

- Start your search for REO properties by networking with local banks or real estate agents who specialize in foreclosures.

- Regularly monitor auction and foreclosure proceedings in your area; many lucrative REO opportunities arise directly from these markets.

- Utilize online platforms dedicated to listing REO properties—keeping an eye on these listings can help you stay informed about potential deals.

Navigating Financing Options for REO Purchases

When it comes to REO purchases, understanding your financing options is crucial for making informed decisions. Navigating this landscape requires you to be aware of various methods that can help fund your investment while addressing specific challenges associated with REO properties.

Common Financing Options for REO Properties

1. Conventional Loans: These loans are provided by private lenders and can be used to finance REO properties. You’ll typically need a credit score of at least 620, and you might have to make a down payment of around 20%. However, their rigid requirements may exclude properties that require significant repairs.

2. FHA Loans: Federal Housing Administration (FHA) loans can be an excellent option for first-time homebuyers. With a minimum down payment of 3.5% and more lenient credit score requirements, they make it easier to purchase REO properties. However, you need to ensure the property meets FHA standards, which can be a challenge for some REOs.

3. Hard Money Loans: If you’re investing with a short-term perspective, hard money loans may be appealing. These loans come from private lenders and offer quick funding, often funded within a week. However, you can expect higher interest rates—typically between 8% to 15%, and they are often based more on the property value than your creditworthiness.

4. Cash Offers: If you have the funds, making a cash offer can set your bid apart, especially in competitive markets. This approach may save you on closing costs and speed up the transaction process. According to recent data, cash buyers are often able to negotiate up to a 10% discount on the listing price.

5. FHA 203(k) Rehabilitation Loan: This specialized loan is tailored for homebuyers considering properties in need of repairs. It allows you to roll the purchase price and the renovation costs into a single loan, facilitating the acquisition of distressed REO properties.

Financing Options Comparison Table

| Financing Option | Down Payment Percentage | Typical Interest Rate | Repair-Eligible | Time to Fund |

|---|---|---|---|---|

| Conventional Loans | 20% | 3% - 5% | Limited | 30-45 days |

| FHA Loans | 3.5% | 3% - 4.5% | Yes | 30-45 days |

| Hard Money Loans | Varies | 8% - 15% | Yes | 1 week |

| Cash Offers | 0% | N/A | N/A | Immediate |

| FHA 203(k) Rehab Loan | 3.5% | 3% - 5% | Yes | 30-45 days |

Real-World Examples of REO Financing

Consider the case of a buyer who utilized a hard money loan to secure an REO property at a significantly reduced price. He purchased a home listed at $200,000 and funded the transaction with a hard money loan that allowed for fast closing. After a quick renovation funded by his cash reserves, he sold the property for $270,000, yielding a substantial profit.

Another example involves a first-time homebuyer who chose an FHA 203(k) loan to purchase an REO property listed at $150,000. After putting down the required 3.5% and financing renovations, she turned the previously run-down house into her dream home with an overall investment of $175,000. Once the renovations were completed, the home’s appraised value increased by 20%.

Practical Implications for Readers

Navigating financing options for REO purchases can drastically impact your investment strategy. When considering your finances, think about:

- Your timeline: Decide whether you need fast funding or can wait for traditional lending processes.

- Your repair commitment: Consider whether you want to invest in properties that require less work or are willing to take on renovation challenges for a better deal.

- Your financial flexibility: Understand how much capital you have on hand, as cash offers can streamline the buying process.

Actionable Advice

- Evaluate Your Financial Situation: Before diving into financing options, review your financial status to determine which financing method aligns best with your goals.

- Seek Pre-Approval: Get pre-approved for a mortgage to better understand your budget; this will provide leverage when negotiating purchases.

- Research Lenders: Different lenders have unique terms and rates. Shop around to find the best deal for your specific REO investment.

By arming yourself with the right knowledge about financing, you can navigate the complexities of REO purchases more effectively and maximize your investment potential.