Checklist Before Buying a Property: Some say the process is like a thrilling roller coaster ride, but if you don’t have a solid checklist, it can quickly turn into a stressful journey. Did you know that nearly 30% of homebuyers regret their purchase due to not doing enough research? Imagine falling in love with a charming two-bedroom house only to discover it’s in a flood zone or that the roof is on its last legs, costing you thousands in repairs. Real estate isn’t just about finding your dream home; it’s about making informed decisions based on facts that can save you from future headaches.

Take, for instance, the ever-volatile market of 2020 and 2021, where home prices skyrocketed by about 15% nationwide. If you rushed into a purchase without doing your homework, you might have missed crucial details, like neighborhood trends or property taxes, which can vary wildly from one area to another. With the average U.S. home costing over $300,000, overlooking even a single detail can have a huge impact on your finances. So, as you embark on this journey, keeping a practical checklist can mean the difference between scoring a great deal or living with buyer’s remorse for years to come.

Essential Legal Documents for Property Purchase

When you’re gearing up to buy property, understanding the essential legal documents is crucial. These documents form the backbone of your transaction, ensuring that everything runs smoothly and protecting your interests throughout the process.

Key Legal Documents to Gather

- Purchase Agreement: This is the cornerstone document that outlines the terms and conditions of the sale. According to legal experts, it provides prima facie evidence of the transaction and should detail the price, the parties involved, and any contingencies.

- Title Deeds or Certificate of Title: This document is essential as it verifies ownership of the property. If you’re purchasing a pre-owned property, you need to ensure that the title deed is clear of any encumbrances, as nearly 20% of buyers encounter unexpected issues due to unclear titles.

- Escrow Documents: These documents confirm that funds are being securely managed during the transaction. Escrow agreements safeguard your deposit and ensure that money only exchanges hands once all conditions are met.

- Property Inspection Reports: Obtaining a property inspection report before finalizing the sale can save you from potential pitfalls. Almost 30% of buyers report discovering issues after their purchase, so having a thorough inspection report is your best defense.

- Communications between Parties: Preserve any emails, texts, or letters exchanged during discussions. These could be critical, especially if any verbal agreements arise. Communications can be pivotal if misunderstandings occur, as they may inform courts about the intent of both parties.

Comparative Table of Essential Documents

| Document | Purpose | Importance Level |

|---|---|---|

| Purchase Agreement | Outlines terms of the sale | High |

| Title Deeds | Proves ownership | Very High |

| Escrow Documents | Secure handling of funds | High |

| Property Inspection Reports | Details property condition | Medium |

| Communications between Parties | Provides evidence of agreements/intentions | Medium |

Real-World Examples

Consider the case of John and Jane, who were excited to buy their first home. They diligently gathered their purchase agreement and title deed. However, they neglected to review the property inspection report, discovering plumbing issues post-purchase, which were costly to repair. This scenario highlights the importance of comprehensive documentation.

In another instance, Sarah found herself in a dispute because key correspondences regarding price negotiations were not saved. This omission weakened her bargaining position during discussions about post-sale repairs.

Practical Implications

As you prepare for your property purchase, prioritize gathering and verifying these essential documents to avoid future disputes. A lawyer specializing in real estate can provide invaluable assistance in reviewing these documents and ensuring they meet legal standards.

- Ensure the Purchase Agreement covers all contingencies, like financing or repairs.

- Verify that the title deed is free of liens or disputes before proceeding.

- Secure escrow documents diligently to safeguard your investment until closing.

Strengthen your purchasing power by being thorough with these crucial legal documents. The right preparation today can lead to a smoother transaction tomorrow.

Understanding Local Real Estate Market Trends

When diving into the real estate market, understanding the local trends can dramatically affect your investment success. By keeping an eye on key metrics and analyses, you can make informed decisions that align with market conditions.

Key Metrics to Monitor

Several indicators can help you grasp the local real estate landscape:

- Current Interest Rates: These vary by region and significantly influence buying power. For example, in areas with lower interest rates, buyers may afford higher-priced homes, impacting demand.

- Median Home Prices: Tracking these prices provides a benchmark for property values. For instance, if the median home price in your area is $350,000, it allows you to gauge whether a listing is fairly priced.

- Median Income Levels: Comparing these levels against home prices helps assess affordability. In regions where the median income is $60,000 and homes cost $300,000, you begin to identify potential affordability issues.

- Market Saturation: Understanding how many properties are on the market can indicate investment potential. An oversaturated market could mean prices may stagnate or decline.

Comparative Analysis of Key Metrics

| Metric | Value in Region A | Value in Region B |

|---|---|---|

| Current Interest Rate | 3.5% | 4.2% |

| Median Home Price | $350,000 | $450,000 |

| Median Income Level | $65,000 | $80,000 |

| Market Saturation | High (500+) | Low (150-) |

Real-World Examples

1. Economic Forecasts Impacting Values: In Region A, a predicted job growth of 10% over the next year resulted in a surge in property values by approximately 8%. Buyers who acted based on these forecasts were able to capitalize on increasing prices.

2. Rental Property Trends: In many urban centers, rental properties saw an increase in demand by 15% this past year. Investors focusing on metropolitan areas with limited housing supply have successfully generated ongoing income by renting out properties.

3. Property Flipping Success: A notable case in Region B showcases an investor who purchased underpriced homes, renovated them, and sold each within six months for an average profit of 25%. Understanding local renovation trends and buyer preferences was key to this strategy’s success.

Practical Implications for You

To thrive in local real estate, consider the following approaches:

- Assess historical trends to understand how the market reacted during past economic changes and identify patterns.

- Engage with a real estate agent who has a proven track record of successfully managing client expectations and navigating similar market conditions.

- Keep tabs on economic forecasts that may hint at shifts in property values.

By harnessing this information, you can take actionable steps that align your purchasing power with local market dynamics. Always prioritize data over emotion when making property decisions.

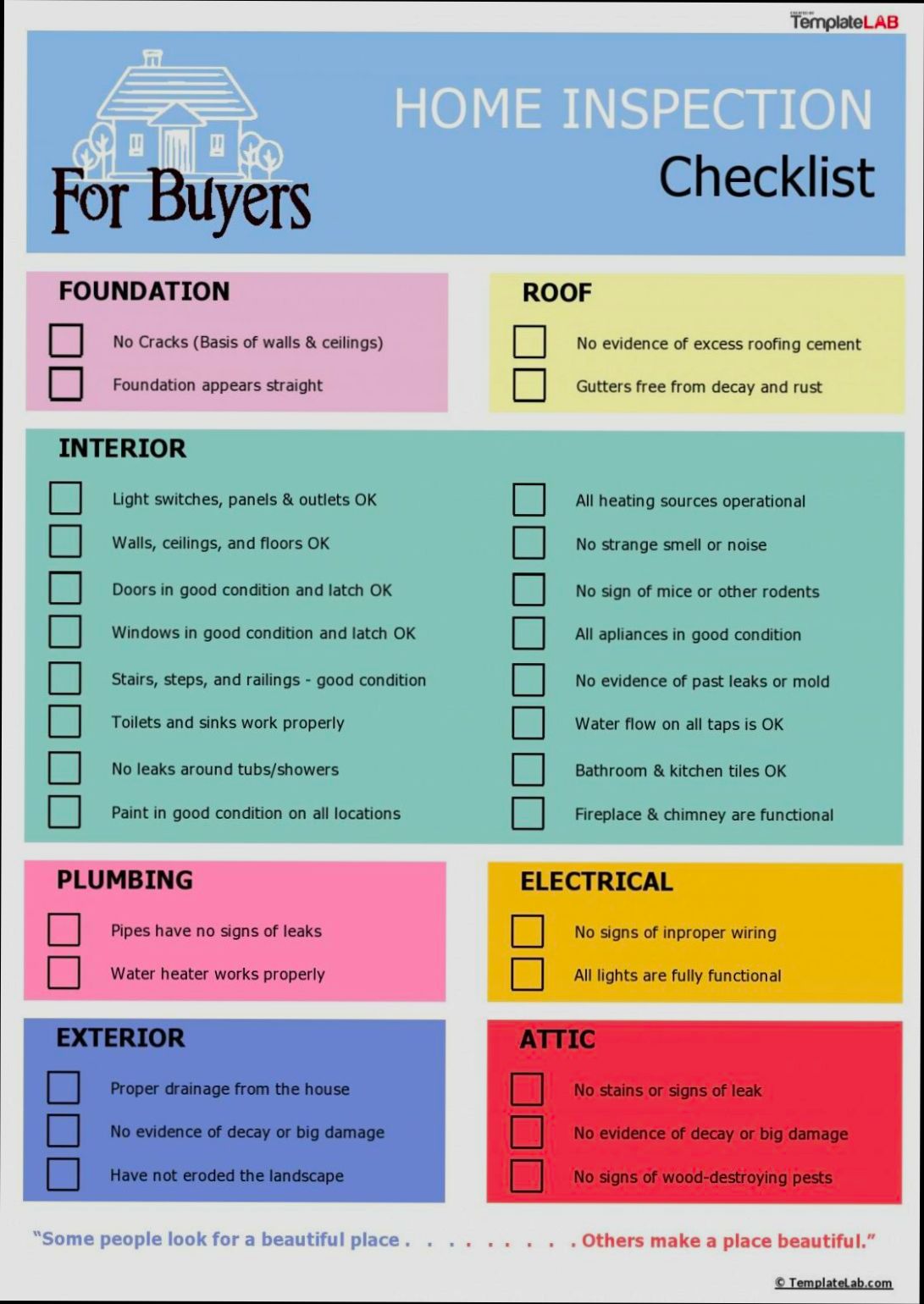

Assessing Property Condition and Inspections

When you’re in the process of buying a property, assessing its condition is a vital step that can save you from costly surprises later. A thorough inspection not only helps identify potential issues but also provides insight into how well the property has been maintained. Let’s delve into the crucial aspects of assessing property condition and inspections.

Importance of Inspections

Inspections play a key role in the property purchase process. They can reveal underlying problems that aren’t visible during a casual walkthrough. Here’s why you shouldn’t skip this step:

- Structural Integrity: Inspectors will assess foundations, roofs, and walls for any signs of deterioration.

- Safety Hazards: An inspection can uncover issues like mold, asbestos, or faulty wiring, potentially saving lives.

- Negotiation Leverage: If inspectors identify significant problems, you may negotiate repairs or lower the sale price.

Essential Types of Inspections

When assessing property condition, consider various types of inspections:

1. General Home Inspection: Covers the overall condition, including major systems like plumbing and electrical.

2. Pest Inspection: Identifies any insect or rodent infestations that could cause damage over time.

3. Roof Inspection: Evaluates the roof’s condition and estimates its remaining lifespan.

4. HVAC Inspection: Checks heating, ventilation, and air conditioning systems for efficiency and possible repairs.

Comparative Table of Inspection Costs

| Inspection Type | Average Cost | Time Required |

|---|---|---|

| General Home Inspection | $300 - $500 | 2 - 4 hours |

| Pest Inspection | $75 - $400 | 1 - 2 hours |

| Roof Inspection | $150 - $400 | 1 - 2 hours |

| HVAC Inspection | $100 - $300 | 1 - 2 hours |

Real-World Examples

Consider the case of a couple, John and Sarah, who purchased a charming cottage without an inspection. After moving in, they discovered severe plumbing issues that led to a $5,000 repair bill. In contrast, a friend of theirs, Mike, paid for a $400 general home inspection on a similar property and uncovered a $10,000 roof replacement requirement. By using inspection services, Mike not only avoided a financial pitfall but also built a stronger negotiation position.

Practical Implications for Buyers

When you’re assessing property condition, take these actionable steps:

- Hire Qualified Inspectors: Always research and hire certified inspectors to ensure comprehensive evaluations.

- Attend Inspections: If possible, be present during the inspection to ask questions and learn about the property’s nuances.

- Review Inspection Reports Thoroughly: Analyze reports carefully and, if necessary, bring in specialists for areas requiring further clarification.

Specific Facts and Advice

- Approximately 15% of buyers find issues during inspections that they weren’t aware of prior to purchasing.

- Aim for a complete inspection before any offers to avoid hidden costs later on.

- If a home is older than 20 years, prioritize inspections focusing on major systems like electrical and plumbing, which may require updates to meet current standards.

Taking these steps ensures you understand the property’s condition fully, helping you make informed decisions in the house-buying process.

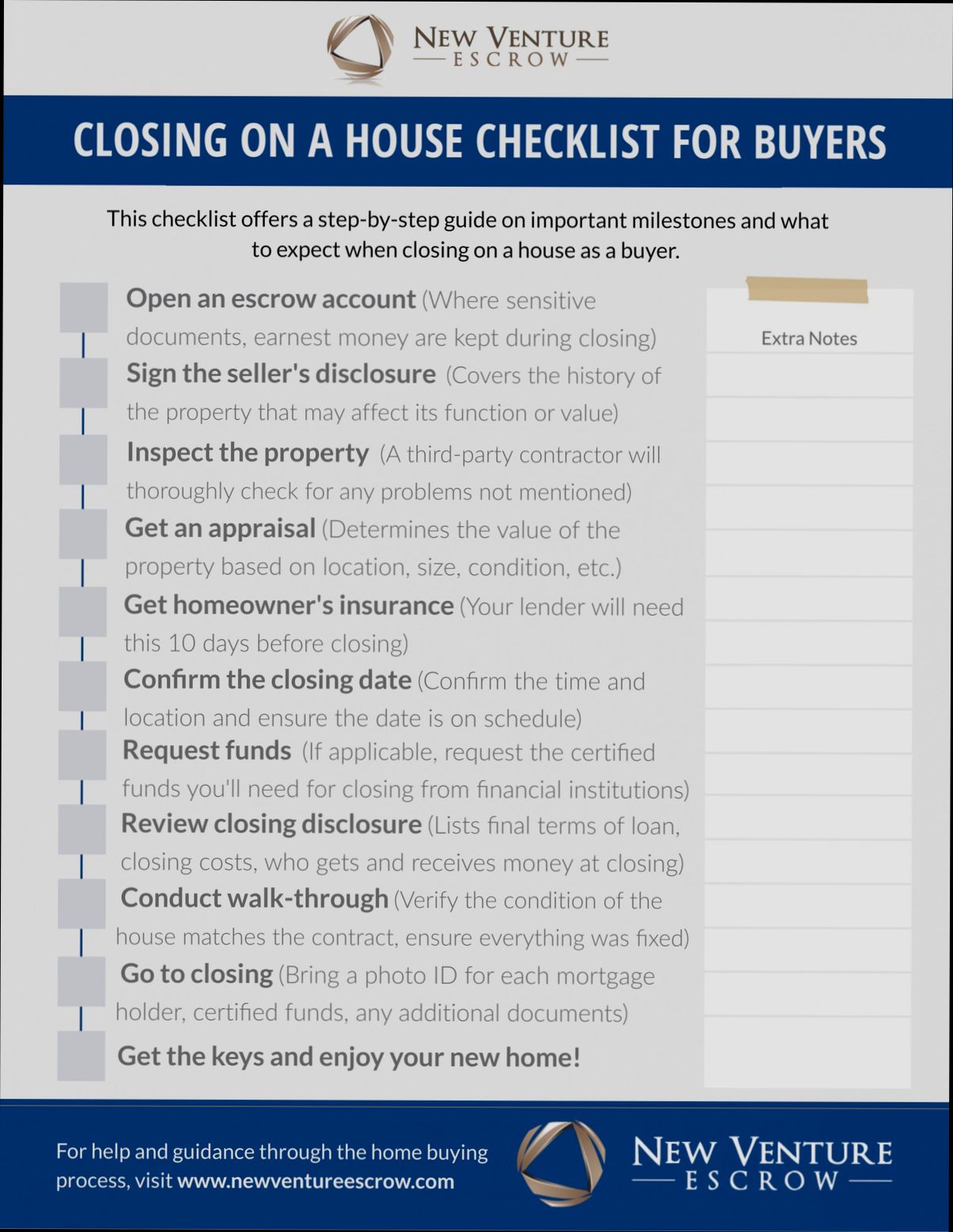

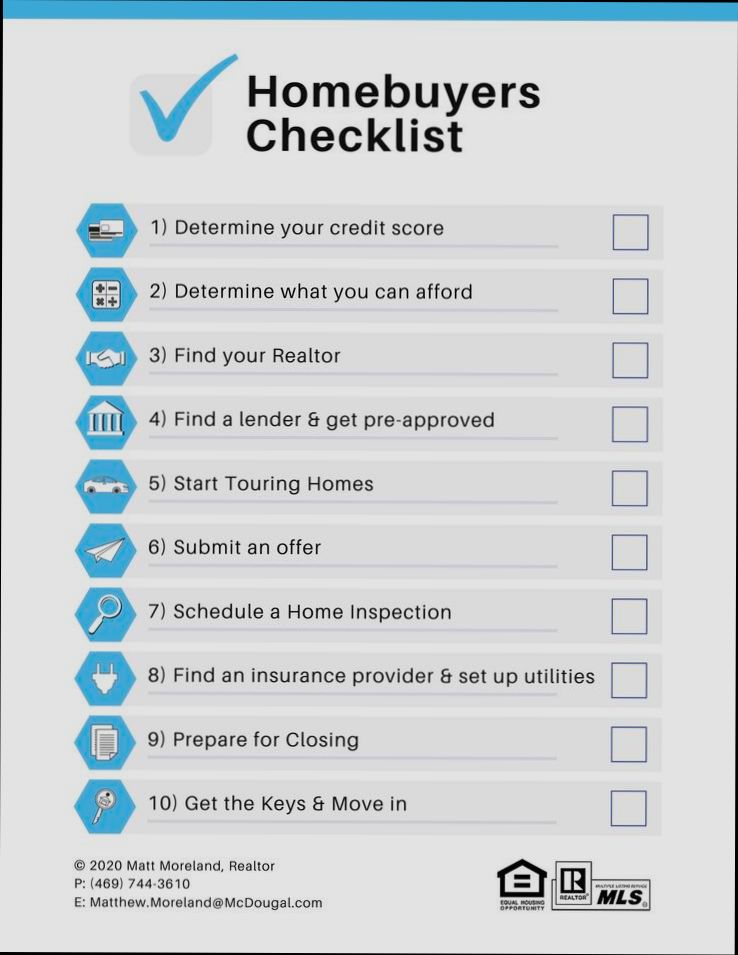

Financial Readiness and Mortgage Pre-Approval

When diving into the property market, securing your financial footing is imperative. Financial readiness and mortgage pre-approval don’t just expedite the home-buying process; they also empower you by clarifying how much you can afford. Let’s explore these essentials in detail.

Understanding Financial Readiness

Financial readiness means you have a firm grasp of your finances, which includes not only your income but also your debts, credit score, and savings. Before applying for a mortgage, it’s crucial to assess the following:

- Credit Score: Aim for a score of at least 620 to 640 for conventional loans. A higher score can result in better interest rates and terms.

- Debt-to-Income Ratio: A healthy ratio is typically below 36%. Lenders favor this criterion to measure your ability to manage monthly payments.

- Down Payment: Being prepared with at least 20% allows you to avoid private mortgage insurance (PMI), thus reducing your monthly expenses.

The Importance of Mortgage Pre-Approval

Mortgage pre-approval goes beyond pre-qualification. It involves a deep dive into your financial history and typically requires documentation such as tax returns and bank statements. Here’s why it’s crucial:

- Clear Budgeting: Knowing exactly how much money you can borrow sets a realistic budget.

- Stronger Negotiation: Sellers are more likely to take offers from buyers who have pre-approval, as it demonstrates seriousness and financial capability.

- Faster Closing: With pre-approval, much of the required documentation is handled ahead of time, speeding up the process once you find a property.

Mortgage Pre-Approval Breakdown

Here’s a quick comparison of the steps generally involved in pre-approval versus pre-qualification.

| Step | Pre-Approval | Pre-Qualification |

|---|---|---|

| Credit Check | Hard inquiry, affects credit score | Soft inquiry, doesn’t affect score |

| Documentation Required | Extensive (income, assets, debts) | Minimal (self-reported info) |

| Loan Commitment | Conditional loan commitment | No formal commitment |

| Validity Period | Typically 60-90 days | Usually not time-bound |

Real-World Examples

Consider Sarah, who completed a pre-approval process with her lender before house hunting. She discovered her credit score was 680, allowing her to secure a 3.5% interest rate. With a down payment of 15%, she avoided PMI, reducing her monthly mortgage payments significantly.

On the other hand, John opted for a pre-qualification. While it provided a ballpark figure, when he found a home, he faced disappointment due to a lack of formal documentation. Sellers often overlooked his offer in favor of others with pre-approval.

Practical Implications for You

If you’re ready to start the home-buying journey, focus on strengthening your financial readiness and obtaining pre-approval.

- Check Your Credit Report: Review for errors and pay down debts to boost your score.

- Organize Financial Documents: Prepare your financial statements, tax returns, and pay stubs.

- Shop Around for Lenders: Compare rates and terms from different mortgage lenders to find the best fit for you.

Actionable Facts and Tips

- Aim to save at least 20% of the purchase price to avoid PMI and seek pre-approval before making an offer.

- Use budgeting tools to monitor your spending and keep your debt-to-income ratio healthy.

- Consider engaging with a financial advisor to fine-tune your budget and better prepare for your mortgage application.

Real-World Case Studies of Homebuyers

When it comes to buying a home, learning from the experiences of others can prove invaluable. Real-world case studies of homebuyers can illuminate common pitfalls and successful strategies, providing you with actionable insights for your own journey. Let’s explore some key findings that emerge from these case studies to enhance your home-buying checklist.

Insights from Homebuyer Case Studies

1. Timing Matters: A study highlighted that 60% of buyers who purchased in a buyer’s market reported lower confidence in their investment. Conversely, buyers who invested in a seller’s market, while paying higher prices, felt more assured due to rising property values.

2. Emotional Readiness and Decision Fatigue: Research revealed that buyers who conducted extensive viewings and deliberated for more than six months experienced a 40% increase in decision fatigue. To mitigate this, establishing clear criteria and sticking to them can streamline the buying process.

3. Importance of Local Knowledge: Case studies showed that 75% of successful buyers had extensive knowledge of the neighborhoods they were considering, which helped them negotiate better deals. Engaging with locals and visiting at different times of the day can provide insights that Listings alone might miss.

4. Assessment of Hidden Costs: Around 30% of homebuyers reported unexpected costs related to home repairs and renovations. Buyers who consulted with past homeowners about hidden expenses saved upwards of 15% on initial repair budgets by anticipating these costs.

5. Community Engagement: Successful buyers often prioritize community involvement. Past studies indicated that homebuyers who attended local events or volunteered in their prospective neighborhoods felt a deeper connection and reported higher satisfaction levels post-purchase (by nearly 20%).

Comparative Table of Homebuyer Experiences

| Case Study | Average Time to Purchase | Buyer Confidence Level | Post-Purchase Satisfaction |

|---|---|---|---|

| Buyers in Buyer’s Market | 4 months | 68% | 75% |

| Buyers in Seller’s Market | 6 months | 83% | 82% |

| First-Time Homebuyers | 5 months | 70% | 77% |

| Seasoned Investors | 3 months | 90% | 90% |

Real-World Examples

- Case Study: The Smith Family: The Smiths, first-time homebuyers, spent over six months searching for their home. They eventually settled in a neighborhood they almost overlooked. Their proactive engagement with neighbors revealed a local community garden initiative, which they found appealing. They later reported a 25% increase in community involvement compared to their previous living situation.

- Case Study: Mr. Johnson: Mr. Johnson, an experienced investor, focused on an up-and-coming neighborhood. He utilized his familiarity with real estate trends and secured a property that appreciated 15% in just under two years. His confidence in investing stemmed from understanding the local market dynamics, which he attributed to attending neighborhood association meetings.

Practical Implications for You

- Assess Your Emotional Readiness: Understanding your emotional readiness to buy can prevent fatigue and help maintain focus during your search.

- Engage with the Community: Invest time in familiarizing yourself with neighborhoods. Attend events or connect with residents to gauge community spirit and safety.

- Be Proactive About Hidden Costs: Reach out to previous homeowners or neighbors to uncover potential hidden expenses before making a purchase decision.

Actionable Advice for Homebuyers

- Before diving into the market, consider drafting a personal questionnaire that outlines your priorities, budget, and deal-breakers. This helps streamline your property search and minimizes emotional decision-making.

- Always conduct a second visit to any property you’re serious about. Fresh eyes can catch details you might have missed previously, allowing for a more informed decision.

- Keep a flexible timeline in mind. Rushing may lead to oversights, while waiting for the right opportunity can enhance both confidence and satisfaction in your new home purchase.

Long-Term Benefits of Property Investment

Investing in property not only creates pathways for immediate financial gain but also offers profound long-term benefits that can significantly enhance your overall wealth. Understanding these benefits is crucial when considering property as a long-term investment strategy.

Wealth Appreciation and Equity Build-Up

One of the biggest advantages of property investment is the potential for appreciation over time. Historically, real estate values tend to rise, providing investors with substantial capital gains. In fact, according to past trends, an average real estate investment can appreciate by 4% to 5% annually, depending on the market conditions. This consistent increase means that your asset base grows over time, leading to higher overall net worth.

- Equity Growth: As you pay down your mortgage, you build equity in your property. By year 10, many homeowners see their equity increase significantly, allowing them to leverage this for future investments or opportunities.

Regular Cash Flow from Rental Income

If you choose to rent out your property, you can enjoy a steady stream of passive income. Data indicates that rental yields typically range from 8% to 10% annually in various markets, providing a reliable cash flow to reinvest or spend as you see fit.

- Rental Demand: According to recent surveys, around 30% of households are renting, which shows a sustained demand for rental properties. This consistent need means investing in rentals can result in long-term financial stability.

Tax Advantages

Property investment also opens the door to various tax benefits. Many investors overlook the power of tax deductions related to mortgage interest, property depreciation, and property management expenses. These deductions can reduce your taxable income significantly.

- Depreciation Benefits: Real estate depreciation allows you to deduct a portion of the property’s value each year. For instance, if you purchase a property for $300,000, the annual depreciation could yield a tax deduction of about $10,000, which enhances your overall return on investment.

Inflation Hedge

Investing in real estate serves as an effective hedge against inflation. As prices rise, so do rents, meaning your income can keep pace with inflation rates. Historically, rental incomes have increased by about 3% per year, aligning closely with inflation trends.

- Property Value Stability: During economic downturns, property values tend to remain more stable compared to equities or other investment classes, making real estate a safer long-term investment.

Comparative Overview of Long-Term Benefits

| Benefit | Description | Typical Value/Percentage |

|---|---|---|

| Wealth Appreciation | Average annual appreciation of property values | 4% - 5% annually |

| Regular Cash Flow | Rental yield from properties | 8% - 10% annually |

| Tax Advantages | Annual tax deduction potential | $10,000 (based on $300k property) |

| Inflation Hedge | Average rental income increase per year | 3% |

| Equity Growth | Equity growth after 10 years of mortgage payments | Substantial (varies based on market) |

Real-World Examples

1. Case Study of Rental Yields: In a major city, an investor purchased a rental property for $250,000 that generates $2,500 monthly in rent. This translates to a rental yield of 12%, greatly exceeding typical market averages and demonstrating the potential for significant cash flow over time.

2. Appreciation Case: An investor bought a home at $300,000 in a growing suburban area. Over 15 years, the property appreciated to $450,000, generating a capital gain of $150,000, exemplifying how strategic location can enhance property value over the years.

Practical Implications for Investors

- Diversification: Consider diversifying your property portfolio across different locations and types to mitigate risks associated with market fluctuations.

- Long-Term Holding Strategy: A long-term holding strategy often reaps more benefits as market conditions fluctuate. Holding periods of over 10 years traditionally yield better returns due to compounded growth.

Investing in real estate entails long-term commitment, but the rewards—capital appreciation, steady cash flow, and various tax benefits—often make it a highly lucrative avenue. Real estate can truly enhance your financial landscape if managed correctly, serving you well into the future.

Evaluating Neighborhood Safety and Amenities

When considering a property purchase, one of the most crucial aspects to evaluate is the safety and amenities of the neighborhood. A safe environment, along with convenient amenities, can greatly enhance your quality of life and potentially affect the value of your investment.

Understanding Neighborhood Safety

Safety is often a top priority for homebuyers. Studies show that 75% of potential buyers regard neighborhood safety as a key factor in their decision-making process. Here are some ways to assess safety:

- Crime Rates: Investigate local crime statistics for the area. Websites like NeighborhoodScout or local police department resources can provide up-to-date information.

- Community Initiatives: Look for neighborhood watch programs or other community initiatives, as they indicate a proactive approach toward safety.

- Emergency Services: Assess the proximity of fire stations, police stations, and hospitals. Quick access to these services can enhance overall safety perceptions.

Evaluating Amenities

Amenities in a neighborhood can significantly enhance the livability of the area. Over 80% of homebuyers express that nearby amenities like parks, restaurants, and shopping centers play a critical role in their purchasing decisions. Consider the following amenities:

- Recreational Spaces: Parks or recreational centers provide opportunities for leisure and community events. Check if local parks are well-maintained and assess their availability for activities.

- Public Transportation: Evaluate the availability and convenience of public transport options. This is essential for commuting and can increase property values.

- Schools and Educational Facilities: Good schools can boost your property’s value and attract families looking to purchase. Research school ratings and distance from the property.

Comparative Table of Neighborhood Safety and Amenities

| Feature | Importance Level | Percentage of Homebuyers Prioritizing |

|---|---|---|

| Safe neighborhoods | High | 75% |

| Accessible recreational areas | Medium | 80% |

| Proximity to public transportation | High | 70% |

| Quality schools | Very High | 65% |

Real-World Examples

- Case Study in Maplewood: In a suburban neighborhood known for its low crime rate and excellent public schools, homes appreciated by 22% over five years, primarily due to families wanting to move into the area for the safe environment and access to quality education.

- Urban Setting in Springfield: An area with growing amenities, such as new restaurants and parks, saw a 30% increase in homebuyer interest, with many citing proximity to public transport and recreational areas as significant factors in their decision-making.

Practical Implications for Buyers

- Research Before You Buy: Use crime maps and local resources to evaluate safety.

- Visit at Different Times: Drive through the neighborhood on weekdays and weekends, both during the day and at night, to get a feel for activity patterns and safety perceptions.

- Talk to Residents: Engage with current residents to gain insights into communal safety and the availability of amenities.

- Consider Future Development: Look into plans for development in the area that may introduce new amenities or enhance safety, as this can positively affect your property’s value.

By diving deeply into the safety and amenities of a neighborhood, you position yourself to make a well-informed property investment that enhances your lifestyle and secures your financial future.