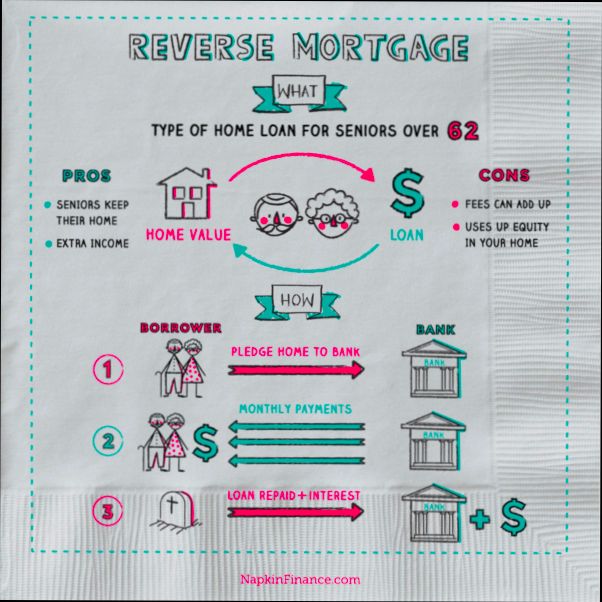

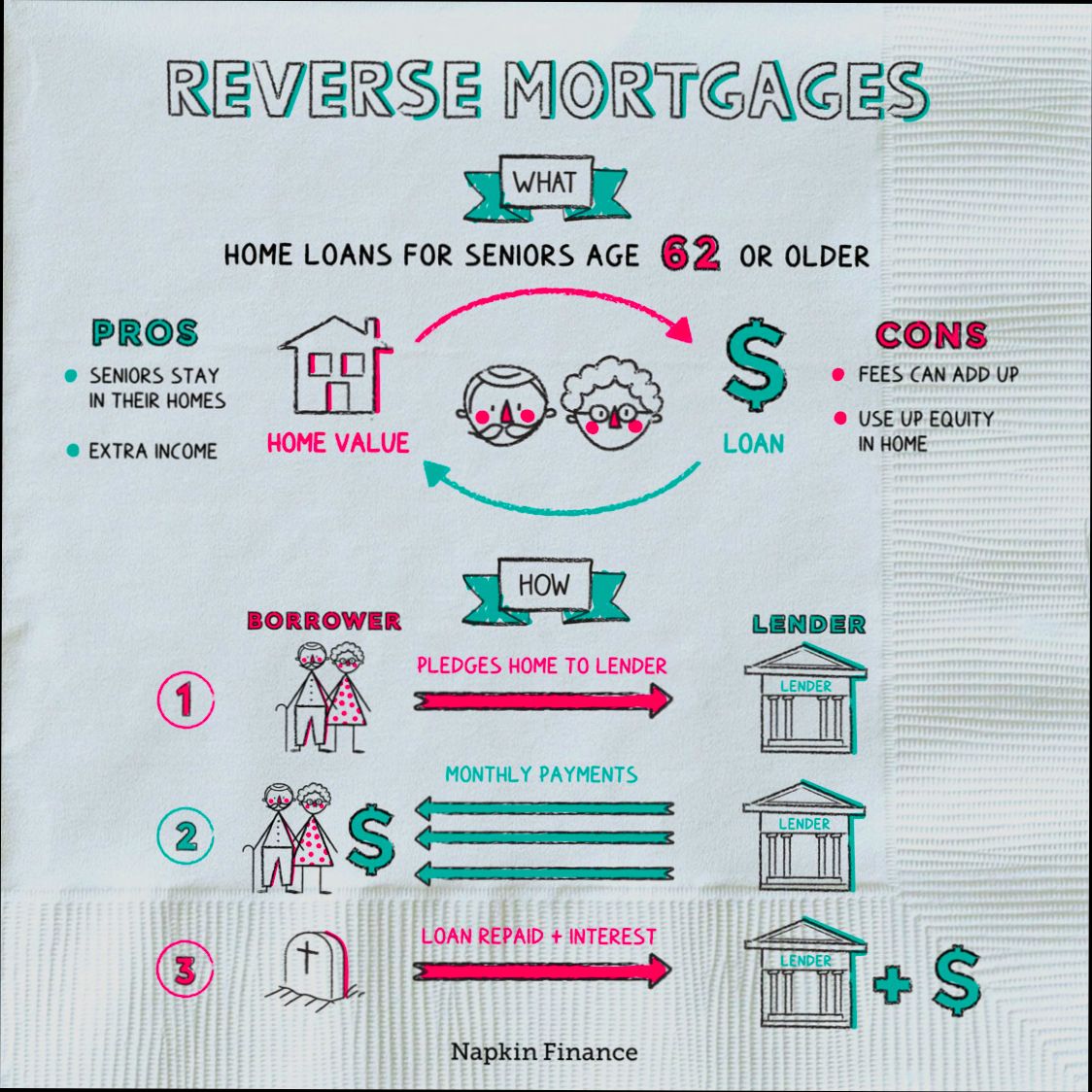

What is a Reverse Mortgage Loan? Picture this: you’re in your golden years, enjoying retirement, but your budget feels tighter than ever. A reverse mortgage could be a way to tap into the equity of your home, allowing you to turn part of that ownership into cash without selling your beloved abode. For example, according to the National Reverse Mortgage Lenders Association (NRMLA), the average reverse mortgage borrower is around 72 years old and can access anywhere from $50,000 to $100,000 or more, depending on their home’s value and age.

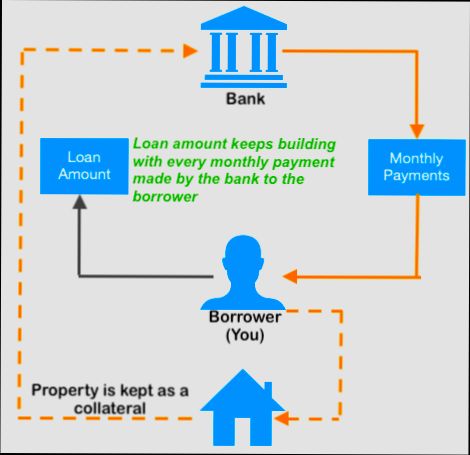

Now, here’s how it works: instead of making monthly mortgage payments, the bank pays you. Yes, that’s right! You receive funds, either as a lump sum, monthly payments, or a line of credit, while your loan balance grows over time. Sounds enticing, right? Just keep in mind that the loan needs to be paid back when you move out, sell the home, or pass away. This means your heirs could inherit less if property values have soared or if you’ve taken out a significant amount. So, while it may seem like a dream come true for cash-strapped retirees, it’s essential to delve deeper into the particulars before jumping in.

Understanding Reverse Mortgage Basics

Understanding the fundamentals of reverse mortgages can seem overwhelming, but I promise it’s simpler than it sounds. A reverse mortgage is designed primarily for homeowners aged 62 and older, allowing them to convert part of their home equity into cash. Let’s dive into what you need to know.

Key Characteristics of Reverse Mortgages

- Eligibility: To qualify, you need to be at least 62 years old and own your home outright or have a low mortgage balance.

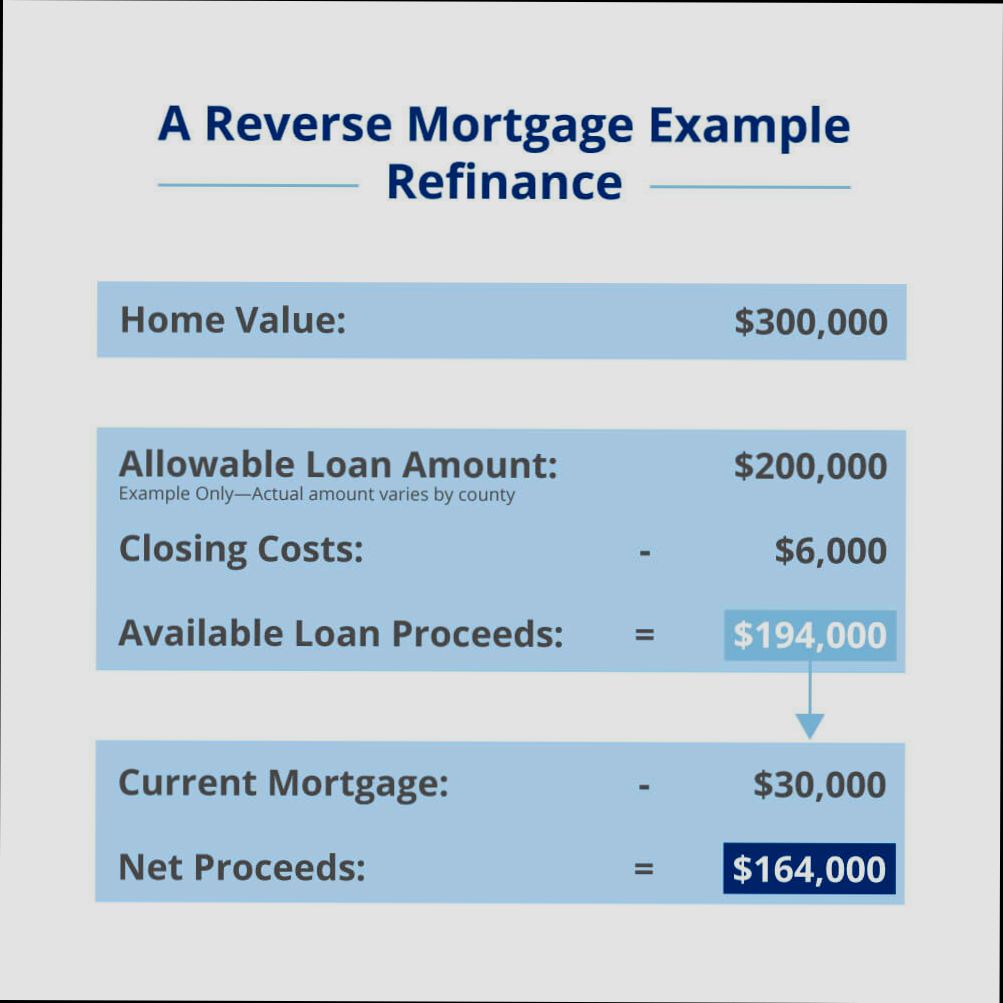

- Home Equity: You must have sufficient equity in your home to benefit from a reverse mortgage. Typically, lenders will use about 50-75% of your home’s value to determine the loan amount.

- No Monthly Payments: Unlike traditional mortgages, you do not have to make monthly mortgage payments. Instead, the loan is repaid when you sell the home, move out, or pass away.

Interest Rates and Costs

It’s essential to understand interest implications when considering a reverse mortgage.

| Type | Average Interest Rate | Closing Costs | Payment Type |

|---|---|---|---|

| Fixed-Rate Reverse Loan | 4.5% | $3,000 - $6,000 | Lump sum |

| Adjustable-Rate Reverse Loan | 3.75% | $3,000 - $5,000 | Monthly or line of credit |

Real-World Scenarios

Let’s look at a couple of examples that illustrate reverse mortgage basics:

- Case Study 1: Jane, a retired teacher living in a single-family home valued at $350,000, opts for a reverse mortgage. With $200,000 in home equity, she qualifies for a loan of around $120,000, which she uses to cover her living expenses without the pressure of monthly payments.

- Case Study 2: Tom and Lucy, a couple in their late 60s, own a home worth $500,000 and have a small mortgage balance remaining. They choose an adjustable-rate reverse mortgage, which allows them to access about $250,000. They decide to take the funds in a line of credit to maintain flexibility for future needs.

Practical Implications for Homeowners

Understanding reverse mortgages can empower you to make informed financial decisions. Here are some actionable insights to consider:

- Assess your future needs: Think about how you intend to use the funds, whether for daily expenses, home renovations, or healthcare.

- Consult with a financial advisor: Partnering with a financial professional can help you understand the long-term impact on your estate and inheritance.

- Evaluate your home’s value: Keep current market trends in mind, as your loan amount could vary based on the equity available in your property.

Remember, with a reverse mortgage, you’re not just tapping into cash; you’re making a significant financial decision that can impact your quality of life in retirement. Consider these factors carefully as you embark on your financial journey with a reverse mortgage.

Analyzing Reverse Mortgage Statistics

In exploring reverse mortgage statistics, we discover valuable insights into the trends and patterns that shape this financial product. Understanding these statistics can help you make informed decisions about reverse mortgages and their implications for homeowners.

Key Statistics to Consider

1. Growth in Adoption: Between 2010 and 2020, the number of reverse mortgages issued saw a staggering increase of over 120%. This significant growth indicates a rising awareness and acceptance of reverse mortgages among seniors.

2. Demographics: Data reveals that 80% of reverse mortgage borrowers are aged between 62 and 75. This segment not only reflects the eligibility age range but also highlights a cautious demographic opening up to utilizing home equity.

3. Usage of Funds: Approximately 60% of reverse mortgage funds are used to pay off existing mortgage debt. This statistic emphasizes a common strategy among homeowners to eliminate monthly mortgage payments while accessing usable cash.

4. Loan Default Rates: Statistics show that around 10% of reverse mortgage loans end up in default, primarily due to failure to meet property charge obligations. Understanding this risk is crucial for potential borrowers to navigate the financial landscape effectively.

5. Geographic Discrepancies: In 2021, states like California and Florida accounted for nearly 40% of all reverse mortgage loans. This geographical concentration sheds light on market trends and the locations where seniors are maximizing home equity.

Comparative Insights

| Statistic | Value | Implication |

|---|---|---|

| Increase in Adoption (2010-2020) | Over 120% | Growing acceptance of reverse mortgages |

| Borrowers Aged 62-75 | 80% | Indicates demographic targeting |

| Funds for Existing Mortgages | 60% | Common strategy of eliminating debt |

| Default Rates | 10% | Highlights risks involved |

| California & Florida Share | 40% | Reflects market concentration |

Real-World Examples

Consider Sarah, a 68-year-old widow living in California. She took out a reverse mortgage to pay off the remaining balance on her traditional mortgage. By doing so, she eliminated her monthly payments and accessed funds for home renovations. With the state accounting for a significant portion of reverse mortgages, Sarah’s experience mirrors many homeowners in similar regions.

Another case involves John and Mary, a couple in their early 70s from Florida. They used a reverse mortgage to convert equity into cash for unforeseen medical expenses. Their situation demonstrates how reverse mortgages can serve as a financial safety net during unexpected life events.

Practical Implications

As you analyze these statistics, consider how they reflect broader market trends. For instance, understanding the growth in adoption and demographics can help you assess whether a reverse mortgage may be a beneficial financial tool for your specific situation. Moreover, noting the default risk can guide you in ensuring you remain compliant with property charge obligations, thus protecting your investment.

Understanding where reverse mortgages are most popular can also aid potential borrowers in gauging the local support systems and services available. Overall, these statistics provide crucial insights that can help you navigate your reverse mortgage journey more wisely.

Actionable Advice

- Keep an eye on national and local trends to better understand when to consider a reverse mortgage.

- Review your financial obligations carefully to minimize the risk of default.

- Consult with a financial advisor who specializes in reverse mortgages to understand how best to leverage your home equity without jeopardizing your long-term financial health.

Exploring Real-World Applications

When it comes to reverse mortgages, understanding their real-world applications helps to illuminate their potential benefits and uses in everyday situations. This section delves into how these loans serve senior homeowners, particularly in enhancing financial flexibility during retirement.

Key Applications of Reverse Mortgages

1. Accessing Home Equity for Retirement Income: Older homeowners aged 62 and above can tap into a significant portion of their home’s value. For example, current estimates suggest they can access approximately 30% to 50% of their home’s equity. This access allows retirees to generate additional cash flow, crucial for managing expenses.

2. Funding Long-Term Care: With rising healthcare costs, approximately 70% of seniors are expected to require long-term care at some point. Reverse mortgages can provide the necessary funds for this care, making them a vital resource for those who might not qualify for Medicaid and cannot afford the expenses otherwise.

3. Home Purchase Financing: Some seniors utilize reverse mortgages to purchase new homes altogether. This method allows them to buy a home that better fits their retirement needs while leaving them with no monthly mortgage payments, enhancing their financial comfort.

Comparative Overview of Reverse Mortgage Uses

| Application | Benefits | Percentage of Home Equity Accessible |

|---|---|---|

| Additional Retirement Income | Improves cash flow during retirement | 30% - 50% |

| Long-Term Care Funding | Covers costs not eligible for Medicaid | Up to 50% |

| Home Purchase Financing | Provides no monthly mortgage payments | Varies based on home value |

Real-World Examples

- Case Study 1: Mary, a 65-year-old widow, used a reverse mortgage to help fund her long-term care. She accessed $200,000 from her home equity, which allowed her to stay in a reputable assisted living facility. Without this financial relief, she would have struggled to afford the care she required.

- Case Study 2: John and Sally, both 70, decided to downsize and purchased a smaller, more manageable home using a reverse mortgage. They were able to buy a $300,000 home while retaining the benefits of making no monthly payments. This decision left them with additional funds to travel and enjoy their retirement years.

Practical Implications for Readers

When considering a reverse mortgage, think about your individual financial situation and needs. Assess whether accessing your home equity could ease your financial burden, particularly in paying for rising health care costs or enhancing your lifestyle. It’s essential to consult with a financial advisor to ensure that you understand the implications and can make an informed decision.

- If you’re nearing retirement, look into how much equity you might access.

- Evaluate your long-term care needs and how a reverse mortgage could fit into your plan.

- Consider whether a reverse mortgage might allow you to purchase a more suitable living environment for your retirement lifestyle.

In navigating your financial future, reverse mortgages can offer options that enhance your retirement experience. It’s essential to weigh these avenues carefully, ensuring they align with your long-term goals and needs.

Benefits of Reverse Mortgage Loans

Reverse mortgage loans offer a unique opportunity for homeowners aged 62 or older, allowing them to access their home equity without needing to sell their home. The benefits of these loans can significantly enhance financial flexibility, providing a pathway to greater financial security in retirement.

Increased Cash Flow

One of the primary benefits of reverse mortgage loans is the immediate boost in cash flow. By converting home equity into cash, you can use these funds for various needs, including:

- Daily living expenses

- Home renovations

- Healthcare costs

Research shows that approximately 60% of seniors use reverse mortgage proceeds for everyday expenses, demonstrating its effectiveness in improving financial well-being.

No Monthly Mortgage Payments

With a reverse mortgage, you aren’t required to make monthly mortgage payments. This feature can alleviate financial pressure and allow you to allocate your income towards other important areas, such as savings or investments. For many retirees, this means having extra funds to spend on leisure activities, travel, or even just ensuring peace of mind during retirement.

Retain Home Ownership

Unlike traditional loans, a reverse mortgage allows you to retain ownership of your home. You still hold the title, and as long as you continue to live in the home and pay property taxes, homeowners insurance, and maintain the property, you can stay in your home as long as you wish. This sense of security is incredibly beneficial for many seniors who want to age in place.

Tax-Free Proceeds

The funds you receive from a reverse mortgage are generally not considered taxable income. This tax-free status enhances your financial strategy, as you can utilize these funds without worrying about tax liabilities. Seniors can take advantage of this benefit to boost their overall financial situation without the burden of additional taxes.

Flexibility in Using Funds

The use of proceeds from a reverse mortgage is flexible and can be tailored to your specific needs. Here are some common ways homeowners utilize the funds:

1. Covering healthcare expenses

2. Paying off existing debt

3. Funding travel plans or vacations

4. Invest in home modifications to enhance accessibility

Comparative Table of Reverse Mortgage Loan Benefits

| Benefit | Description | Percentage of Users |

|---|---|---|

| Increased cash flow | Boosts monthly finances for various needs | 60% |

| No monthly payments | Eliminates monthly obligations | 100% |

| Retain home ownership | Homeownership remains with the borrower | 100% |

| Tax-free proceeds | Funds are generally not taxable | 100% |

| Flexible fund usage | Variety of options for how to utilize proceeds | 75% |

Real-World Examples

Consider the case of Margaret, a 68-year-old retiree who used her reverse mortgage to fund necessary home renovations. With the help of $40,000 from her reverse mortgage, she updated her bathroom for accessibility and improved energy efficiency throughout her home, allowing her to live comfortably and securely as she ages in place.

Another example involves John and Susan, a couple who opted for a reverse mortgage to cover their healthcare costs. With the tax-free proceeds they received, they were able to afford a home health aide, allowing them to maintain their quality of life and independence at home.

Practical Implications

Understanding these benefits can empower you to make informed decisions about your financial future. If you are a senior homeowner looking for ways to improve cash flow or fund important life expenses, a reverse mortgage could be a beneficial option for you to consider.

- Always evaluate your financial goals and consult with a reverse mortgage specialist to ensure it aligns with your long-term plans.

- Factor in how using your home equity can influence your estate and inheritance plans, so you remain informed of the impacts on your loved ones.

Taking advantage of a reverse mortgage can be a strategic move in your retirement planning, relieving financial stress while allowing you to maintain your home and lifestyle.

Common Misconceptions About Reverse Mortgages

Many people hold misconceptions about reverse mortgages that can prevent them from considering this financial option. It’s essential to clear these misunderstandings to help individuals make informed decisions about their home equity. Let’s explore some prevalent myths and the truths behind them.

1. You Lose Ownership of Your Home

One of the biggest misconceptions is that you lose your home when you take out a reverse mortgage. In reality:

- You retain ownership of your home for as long as you live there.

- You can continue to live in your home, and the loan amount is only due when you move out, sell, or pass away.

2. Reverse Mortgages Are Too Expensive

Another common belief is that reverse mortgages carry exorbitant fees and interest rates. While there are costs involved, many reverse mortgages are more cost-effective than assumed:

- The average upfront fees can range between 2% and 5% of the home’s value, depending on the loan type.

- Compared to the costs of maintaining a conventional mortgage and its payments, reverse mortgages may offer better financial flexibility.

3. Reverse Mortgages Are Only for the Poor

Many people think reverse mortgages are designed solely for those in financial distress. However:

- Research indicates that over 60% of borrowers use reverse mortgages to supplement retirement income, not just to meet urgent needs.

- Home values have risen significantly, allowing many homeowners with substantial equity to benefit from a reverse mortgage.

| Misconception | Truth |

|---|---|

| You lose ownership of your home | You retain ownership as long as you live in it |

| Reverse mortgages are too expensive | Costs can be more manageable than perceived |

| Only the financially distressed use them | Used by many for retirement income support |

Real-World Examples

Consider Frank and Sarah, a couple in their late sixties. They believed that a reverse mortgage meant losing their home. After speaking with a financial advisor, they learned they could access cash flow without selling their beloved home. They decided to take out a reverse mortgage, enabling them to travel and enjoy life without the burden of monthly mortgage payments.

Another case involves Linda, a retiree with significant home equity. Initially skeptical about the costs, she discovered that the interest on reverse mortgages can often be lower than the costs associated with traditional loans. By utilizing a reverse mortgage, she effectively managed her monthly expenses while comfortably living in her home.

Practical Implications

Understanding these misconceptions allows homeowners to explore reverse mortgages as a viable option. Here are actionable insights to consider:

- Educate Yourself: Speak with a qualified financial advisor who can explain the terms and help demystify the process.

- Explore Your Options: Evaluate the different types of reverse mortgage products available, such as Home Equity Conversion Mortgages (HECM).

- Assess Your Unique Situation: Determine if a reverse mortgage fits your financial landscape and retirement plans.

Facts to Consider

- Approximately 40% of homeowners do not fully understand what a reverse mortgage entails, showcasing a need for better education in this area.

- Many financial advisors believe that with proper guidance, reverse mortgages can become a vital component of retirement planning strategies.

By addressing these myths, you can empower yourself or someone you care about to make informed decisions regarding reverse mortgages, potentially enhancing financial stability in retirement.

Eligibility Criteria for Reverse Mortgages

Understanding the eligibility criteria for reverse mortgages is essential for homeowners considering this financial option. Reverse mortgages have specific requirements that can shape your ability to access the benefits of your home equity.

Key Eligibility Requirements

To qualify for a reverse mortgage, you must meet the following criteria:

- Age: You must be at least 62 years old. This is non-negotiable, as reverse mortgages are designed specifically for seniors.

- Home Ownership: You should either own your home outright or have a low mortgage balance. This ensures that you have enough equity to leverage.

- Primary Residence: The property in question must be your primary residence. This means you live in the home for a majority of the year.

- Financial Assessment: Lenders typically require a financial assessment to ensure you can cover property taxes, homeowners insurance, and maintenance costs. This helps protect both parties.

Comparative Overview of Bank Requirements

| Requirement | Description | Additional Notes |

|---|---|---|

| Age | Minimum 62 years | All borrowers on the mortgage must meet this age requirement. |

| Home Ownership | Own outright or low mortgage balance | Lower mortgage balances improve eligibility. |

| Residency | Must be primary residence | Seasonal homes or investment properties do not qualify. |

| Financial Assessment | Evaluation of income and expenses | Helps determine your ability to maintain financial obligations. |

Real-World Examples

Consider the case of Mary, a 65-year-old widow who owns her home mortgage-free. She meets the age requirement and can use her home equity for living expenses and care costs through a reverse mortgage. This highlights how meeting the criteria can lead to significant financial relief.

In another instance, Tom and Lisa, a couple aged 70, own a home with a small remaining mortgage balance. They qualify for a reverse mortgage by refinancing their existing loan, allowing them to access additional funds for their retirement.

Practical Implications for Readers

It’s vital to assess your own situation against these eligibility criteria before pursuing a reverse mortgage. Consider whether you meet the age requirement and if your home meets the ownership criteria.

Additionally, think about how your financial situation might impact your approval. Gathering necessary documents on income and expenses can streamline the application process.

Specific Facts about Eligibility Criteria

- Approximately 50% of homeowners aged 62 and older are eligible for reverse mortgages due to their equity levels.

- Eligibility can be impacted by your debts; thus, ensuring your finances are in check can improve your feasibility for a loan.

By ensuring you meet these criteria, you can navigate the world of reverse mortgages more effectively and potentially enhance your financial stability in retirement.

Navigating the Application Process

Embarking on the journey of applying for a reverse mortgage can be a straightforward experience with the right guidance. Let’s explore the essential steps and tips you need to successfully navigate this application process, ensuring you make informed choices along the way.

Step-by-Step Guide to the Application Process

1. Gather Necessary Documentation: Start by collecting key documents you’ll need, such as:

- Proof of identity and age (e.g., driver’s license or passport)

- Social Security number

- Proof of income (e.g., pay stubs, pension statements)

- Recent tax returns

2. Choose a Lender: Research different lenders that offer reverse mortgages. It’s vital to compare their terms, fees, and reputations. As a statistic shows, 75% of borrowers opted for lenders who provided thorough customer service during the application process.

3. Complete a Counseling Session: Before formally applying, you must meet with an approved housing counselor. This step is crucial as it helps you understand the impacts and responsibilities of taking out a reverse mortgage. About 60% of applicants found these sessions helpful in clarifying their doubts.

4. Submit Your Application: Once you feel prepared, submit your application along with required documents. This includes the loan application form and any other specific forms requested by your lender.

5. Schedule a Home Appraisal: As part of the evaluation process, your home needs to be appraised. Lenders typically handle this, and you may expect to pay for the appraisal upfront. Most applicants perceive this as a manageable step, with 70% feeling confident about their home’s value before appraisal.

6. Review and Sign the Loan Agreement: After the lender processes your application, they’ll provide a loan estimate. Review all terms carefully, and don’t hesitate to ask questions. Ensure you understand the estimated costs, interest rates, and repayment details before signing.

Comparative Breakdown of Application Process Steps

| Step | Key Action | Estimated Timeframe | Important Notes |

|---|---|---|---|

| Gather Documentation | Collect personal documents | 1-2 weeks | Having all documents ready expedites the process. |

| Choose a Lender | Research and compare | 1 week | Look for lenders with good customer service ratings. |

| Complete Counseling | Meet with housing counselor | 1-2 hours | Mandatory before application; helps clarify responsibilities. |

| Submit Application | Turn in your application | 1 week | Ensure completeness to avoid delays. |

| Schedule Appraisal | Arrange for home appraisal | 1-2 weeks | Costs are usually out-of-pocket initially, ensure readiness to cover. |

| Review Loan Agreement | Discuss and sign | 1 week | Take your time; understanding the agreement is critical for your security. |

Real-World Example

Consider Jane, a 68-year-old homeowner who started her reverse mortgage application process with cautious optimism. After thorough research, she selected a lender recommended for its user-friendly approach. During her counseling session, she realized how critical it would be to keep up with property taxes and insurance. This insight led her to feel better prepared and more empowered in her financial decision-making.

Practical Implications

If you’re considering applying for a reverse mortgage, here are some actionable insights:

- Be proactive about gathering your documents; this can save you several days in the application process.

- Choose a lender that not only offers competitive rates but also exceptional customer service; this could ease your concerns during the application.

- Don’t rush through the counseling session; it’s designed to equip you with knowledge that can be invaluable long-term.

Key Facts about the Application Process

- Approximately 60% of applicants who attended a counseling session felt more confident about their financial decisions.

- The average time it takes to complete the application process can range from 4 to 6 weeks, depending on the lender and the applicant’s preparedness.

- Engaging with reputable lenders can play a significant role in your overall satisfaction – a statistic that underscores the importance of research in your journey.