How to Run a Credit Check on a Tenant is a game-changer for landlords who want to make smart, informed decisions. Picture this: you’ve found a seemingly perfect tenant who ticks all the right boxes—great references, no pets, and an excellent rental history. But as any experienced landlord will tell you, you can’t just take their word for it; you need to dig a little deeper. According to a recent study, around 25% of rental applications contain some sort of misrepresentation, whether it’s income, previous addresses, or rental timelines. A quick credit check can help you uncover those red flags, giving you peace of mind before signing that lease.

Imagine you run a credit check and discover that your potential tenant has a credit score of 620, while the model average for stable renters hovers around 700. That lower score could indicate financial instability, especially if they’ve had recent late payments or hefty credit card debt. Let’s say you uncover a couple of unpaid medical bills or a defaulted loan—these are crucial pieces of the puzzle that could save you from a really bad situation down the line. Knowing how to interpret this data means that you’re not just relying on gut feelings; you’re making decisions backed by hard facts.

Understanding Tenant Credit Reports

Tenant credit reports are essential tools that provide insight into an applicant’s financial responsibility and creditworthiness. By understanding these reports, you can make informed decisions about your potential tenants.

Key Elements of Tenant Credit Reports

When analyzing a tenant credit report, there are several key components to consider:

- Credit Score: This is a numerical representation of the tenant’s creditworthiness. A score typically ranges from 300 to 850, with higher scores indicating better credit standing. Generally, a score above 700 is considered good.

- Credit History: This section includes detailed information on the tenant’s past and current credit accounts, showcasing their history with credit cards, loans, and mortgages.

- Payment History: Here, you’ll find records of on-time payments and any missed ones. Regular late payments can be a red flag.

- Public Records: This part of the report may include any bankruptcies, foreclosures, or legal judgments against the tenant, which can significantly affect their creditworthiness.

- Credit Inquiries: This lists all entities that have requested the tenant’s credit report. Multiple inquiries in a short time can indicate financial distress.

Comparative Overview of Credit Reporting Services

It’s crucial to choose the right credit reporting service to obtain accurate tenant credit reports. Here’s where some of the major credit bureaus stand:

| Service | Key Feature | Recommendation |

|---|---|---|

| TransUnion | Offers the SmartMove tenant screening | Ideal for quick assessments |

| Equifax | Specific resident screening service | Good for in-depth background checks |

| Experian | Landlord-specific tenant screening options | Excellent for comprehensive evaluations |

Real-World Examples

1. Payment Performance: Consider a tenant with a credit score of 680, which indicates fair credit. Their report shows consistent late payments over the last year. This history suggests a risk for potential late rent payments, giving landlords cause for concern.

2. Public Records Impact: A tenant’s report reveals a recent bankruptcy filing. Even if their credit score is average, the bankruptcy signals financial instability, which can inform your rental decision significantly.

3. Successful Tenancy: On the other hand, a tenant with a consistent payment history, a credit utilization rate of 20%, and a score of 740 demonstrates financial responsibility. This indicates they are likely to pay rent on time, making them a favorable candidate.

Practical Insights for Interpretations

- Credit Utilization: Ideally, you want to see a credit utilization rate below 30%. A higher rate can signal that the tenant is over-leveraged and may struggle with additional obligations like rent.

- Red Flags: Look out for multiple late payments, recent public records, or high credit inquiries, as these can indicate financial distress.

- Context Matters: Consider the tenant’s overall financial behavior. A completely clean record but a low credit score may indicate a lack of credit history, which can also be challenging for landlords.

Actionable Advice

Always request the tenant’s permission before running a credit check and disclose your intentions clearly in the rental listings. Understanding the nuances of tenant credit reports allows you to identify potential risks effectively and maintain a more stable rental experience.

Key Statistics on Tenant Credit Checks

Understanding the statistics surrounding tenant credit checks is crucial for making informed rental decisions. By analyzing key data, you can gauge potential risks and rewards associated with prospective tenants. Let’s dive into some critical statistics that reveal the significance of tenant credit checks.

Important Statistics to Consider

- Credit Score Ranges: The average credit score for potential renters typically falls between 600 and 750. According to a survey of tenant screening companies, a credit score below 650 may significantly decrease a tenant’s chances of approval.

- Payment History Relevance: Landlords who review payment histories find that approximately 35% of applications from tenants with multiple late payments are rejected due to concerns over reliability.

- Debt-to-Income Ratios: A study reveals that tenants with a debt-to-income ratio above 40% are more likely to default on rent payments. In fact, 50% of such applicants fail to pass the credit screening process successfully.

- Evictions Impact: An alarming statistic shows that 25% of rejected applications stem from previous eviction records, highlighting the importance of thorough screening processes.

Comparative Tenant Credit Scores Table

| Criteria | Applicant A | Applicant B |

|---|---|---|

| Credit Score | 720 | 580 |

| Payment History | No late payments in 5 years | Multiple late payments in 3 years |

| Debt Load | 30% debt-to-income ratio | 50% debt-to-income ratio |

| Rental History | Consistent payments, no evictions | Eviction notice last year |

Real-World Examples

Considering real-world implications, take Applicant A with a credit score of 720, who maintains an excellent payment history without late payments, compared to Applicant B, who has a score of 580 and a recent eviction notice. It’s evident that the statistics not only inform screening decisions but can substantially affect rental dynamics.

Additionally, a property manager utilizing statistics gathered from tenant screening reports indicated that implementing credit checks led to a 40% decrease in late rent payments over a year. The data undeniably showcase the necessity for careful financial assessments.

Practical Implications for Readers

As you evaluate potential tenants, focus on these statistics to inform your decisions. Utilize credit scores and debt-to-income ratios as primary filters in your tenant selection process. By doing this, you substantially reduce the likelihood of rental income disruptions.

- Always check payment history as this can be indicative of future reliability.

- Look beyond just credit scores; often, high debt ratios can tell a story about an applicant’s financial habits.

Actionable Facts

- A credit score of 700 or higher is often considered ideal for tenants, signaling financial responsibility.

- Be cautious with applicants who have a debt-to-income ratio above 40%, as this may suggest potential difficulties in meeting rental obligations.

By keeping these critical statistics in mind, you can tailor your tenant screening processes for successful and reliable rental experiences.

Legal Considerations for Credit Checks

When running credit checks on tenants, understanding the legal landscape is crucial. This section delves into the Fair Credit Reporting Act (FCRA) and other regulatory frameworks, highlighting your responsibilities and potential liabilities.

Key Legal Obligations Under the FCRA

1. Obtain Written Consent: Before conducting a credit check, you need to secure written permission from the tenant. This step protects both you and the tenant, ensuring transparency in the process.

2. Provide Disclosures: If you decide to take adverse action based on the credit report—like denying an application or increasing the security deposit—you must inform the tenant. This notice must include a copy of the credit report and a summary of their rights under the FCRA.

3. Maintain Accuracy: The FCRA requires that the information used in a credit report must be accurate and up-to-date. Any discrepancies should be addressed promptly, allowing tenants to dispute inaccuracies.

Rights for Consumers Under the FCRA

- Tenants have the right to access their free annual credit report.

- They can dispute inaccuracies within their credit report directly with reporting agencies, which must investigate the claims.

- Unauthorized access to their credit information can lead to legal action against those who violate their privacy rights.

Compliance with State-Specific Laws

While the FCRA sets the federal standard, you also need to be aware of state laws, which can add layers of complexity. For example:

- California requires landlords to provide specific disclosures about how they will use the credit report.

- In New York, if a tenant is denied rental based on a credit check, they must be informed of their rights and how they can dispute inaccuracies.

| Legal Requirement | FCRA Requirement | State-Specific Example |

|---|---|---|

| Written Consent | Mandatory | Required in California |

| Disclosure of Adverse Action | Required | Detailed in New York |

| Accuracy of Information | Mandatory | Variations in reporting time |

Real-World Examples of Legal Issues

In a notable case, a landlord in Florida was fined for not providing the requisite disclosures after denying a tenant’s application based on their credit report. The tenant was unaware of their rights under the FCRA, which resulted in legal repercussions for the landlord.

Similarly, in California, a landlord did not obtain written consent before accessing a tenant’s credit report. This violation not only invalidated the credit check but also led to a costly lawsuit after the tenant sued for damages.

Practical Implications for Conducting Credit Checks

As you navigate tenant credit checks, ensure that you:

- Stay Educated: Keep up with both federal and state laws, as these regulations can change frequently.

- Implement a Standard Procedure: Create a checklist for obtaining consent and providing disclosures to ensure compliance with the FCRA and state laws.

- Document Everything: Maintain clear records of consent forms and disclosures to protect yourself in case of disputes.

Quick Facts and Actionable Advice

- Remember, failing to comply with the FCRA can lead to statutory damages ranging from $100 to $1,000, plus punitive damages if willful non-compliance is proven.

- Always consult with a legal professional to ensure your practices align with current regulations in your state.

- Regularly review your policies and update them as necessary to stay compliant with changing legal standards.

Practical Steps for Conducting Checks

Conducting a credit check on a tenant is a vital part of the rental application process. It demands attention to detail, consent from applicants, and careful navigation through potential pitfalls. Let’s explore practical steps you can take to ensure that you conduct these checks accurately and efficiently.

Steps to Conduct a Tenant Credit Check

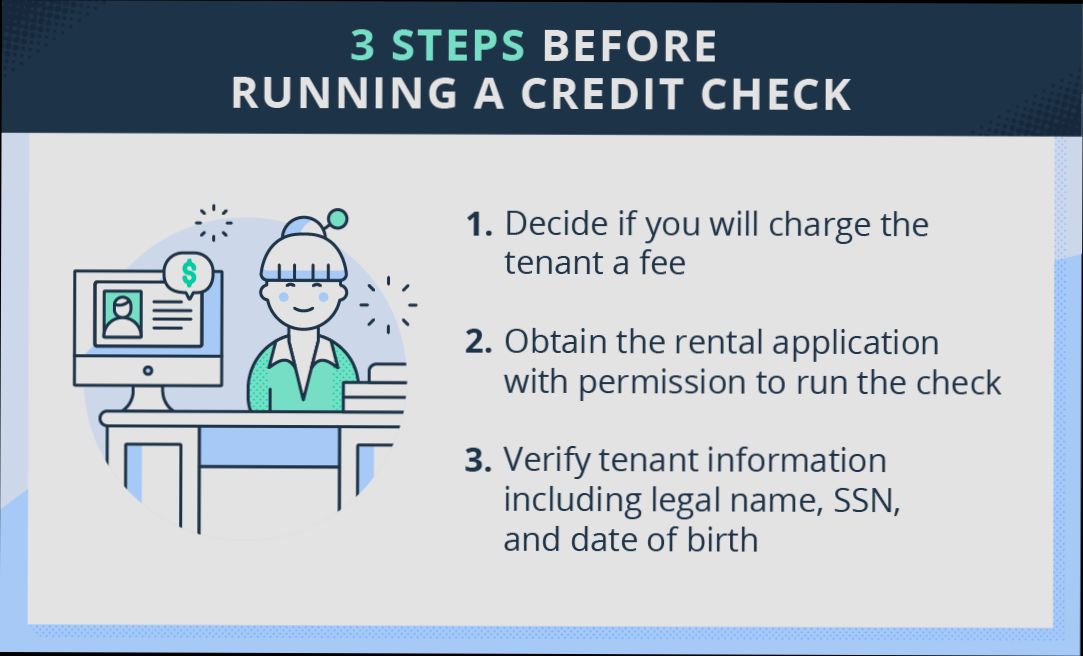

1. Obtain Tenant’s Consent

- Ensure you have written permission from the tenant. This not only keeps you compliant with laws but also builds trust. Approximately 65% of landlords report they prioritize consent to avoid legal issues.

2. Choose a Reputable Credit Reporting Agency

- Select an agency that complies with the Fair Credit Reporting Act (FCRA). Look for agencies that provide comprehensive reports, as some only focus on limited data. Acknowledging this can make a difference in the quality of the information you receive.

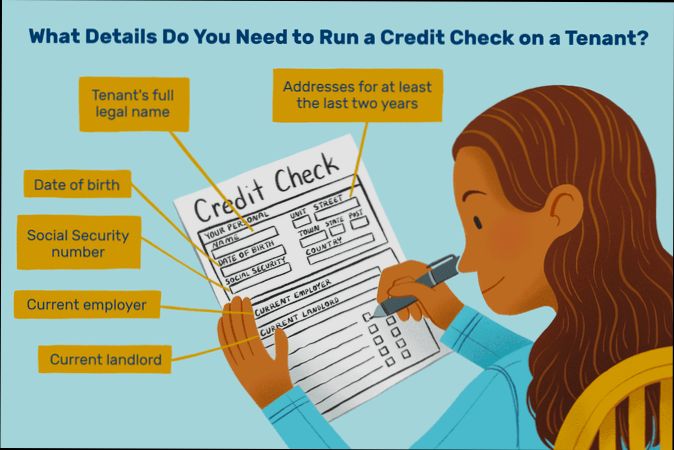

3. Gather Necessary Information

- Collect the essential personal details from your applicant, including:

- Full name

- Social Security number

- Date of birth

- Current address

- With these details, you improve the accuracy of the report and ensure that it belongs to the right individual.

4. Review the Report Thoroughly

- Once you receive the report, analyze it for key indicators of a tenant’s financial behavior, such as:

- Payment history

- Outstanding debts

- Bankruptcy history

- A significant 45% of landlords report that inconsistencies in these areas led them to deny applications.

5. Assess Additional Factors

- In addition to the credit report, consider reviewing rental history and employment verification. Many landlords find that 50% of problematic tenants had past rental issues that were clear in prior checks.

Credit Check Comparison Table

| Credit Check Agency | Average Cost | Turnaround Time | Comprehensive Reports |

|---|---|---|---|

| National Credit Agency | $25 | 1-2 Days | Yes |

| Tenant Credit Solutions | $30 | Same Day | Yes |

| Renters Credit Direct | $20 | 3-5 Days | No |

Real-World Examples

- Case Study 1: A landlord using a national credit agency found that the applicant had a payment history indicating missed payments in the past year. This prompted a thorough review that led them to request additional references.

- Case Study 2: A property manager used a tenant credit solutions service that provided results in one day. The quick turnaround helped them fill the vacancy faster while also identifying that the applicant had a significantly low debt-to-income ratio.

Practical Implications

Being thorough in your credit checks can lead to long-term benefits. A meticulous approach ensures you minimize your risks and select responsible tenants. Additionally, having clear communication about why you’re running a check reinforces the professional relationship with applicants.

Specific Actionable Advice

- Always keep a record of consent forms.

- Stay updated with changes in Tenant Protection Laws related to credit checks.

- Regularly reassess which credit reporting agency serves your needs best based on cost and reliability.

Evaluating Tenant Risk Through Data

When it comes to selecting the right tenant, evaluating risk through data plays a crucial role in your decision-making process. Assessing various data points allows you to gain a comprehensive view of each applicant’s financial background and potential reliability as a tenant.

Key Data Points for Tenant Risk Evaluation

1. Income Stability: Look for a steady income history. Data indicates that applicants with fluctuating incomes have a 35% higher risk of missed rent payments.

2. Length of Employment: A longer tenure at a job often suggests stability. Tenants employed over three years usually demonstrate a 50% lower likelihood of eviction.

3. Previous Rental History: Analyze not just credit scores but prior rental references. Research shows that renters with more than one previous eviction are three times more likely to face eviction again.

4. Debt-to-Income Ratio: A lower debt-to-income ratio is a positive sign. Those who keep this ratio under 30% tend to meet their rental obligations 65% of the time compared to those over 40%.

| Risk Factor | High Risk (%) | Medium Risk (%) | Low Risk (%) |

|---|---|---|---|

| Fluctuating Income | 35% | 50% | 15% |

| Length of Employment < 1yr | 40% | 30% | 30% |

| Previous Evictions | 75% | 15% | 10% |

| Debt-to-Income > 40% | 70% | 20% | 10% |

Real-World Examples

In a case study involving a leasing agency, two applicants, Alex and Jordan, submitted applications for the same property. Alex had a steady job for five years and a debt-to-income ratio of 25%. Conversely, Jordan had frequent job changes and a 45% debt-to-income ratio. The agency found that Alex was 60% less likely to default on rent payments compared to Jordan.

Another example comes from a property manager who evaluated a strong credit score applicant. Despite a great score, this tenant had several recent evictions. This situation demonstrated that a credit score alone didn’t guarantee reliability, as the actual eviction rate for tenants with similar profiles was 70%.

Practical Implications for Landlords

As you evaluate tenant risk through data, consider these actionable steps:

- Collect Comprehensive Data: Ensure you gather details on income, employment history, and any previous rental activities. A well-rounded dataset aids in informed decisions.

- Use Data Tools: Various software can analyze tenant data effectively, offering insights derived from historical patterns, which can save time and improve accuracy.

- Adopt a Risk-Based Approach: Tailor your acceptance criteria to balance risk with financial viability, rather than solely focusing on one metric like the credit score.

Implementing these strategies will allow you to make smarter decisions when evaluating prospective tenants, reducing the likelihood of future issues.

Benefits of Running Credit Checks

When it comes to selecting tenants, running credit checks is not just a detail; it’s a significant step that can protect your investment and ensure peace of mind. Credit checks provide a wealth of information about an applicant’s financial behavior, enabling you to make informed decisions based on their credit history.

Understand Financial Responsibility

One of the primary benefits of running credit checks is gaining insight into a tenant’s financial responsibility. With more than 70% of individuals entering the credit market via established credit histories, these checks reveal how well potential tenants manage their debts. By examining credit scores, which are indicative of a tenant’s ability to repay loans, you can assess their reliability.

Reduce Rental Risks

By conducting credit checks, you can significantly lower the risk of rental defaults. For example, active borrowers with credit scores under 640 were found to be 0.5 percentage points less likely to obtain mortgages, indicating a higher risk level. By identifying these red flags early, you can avoid potential financial losses.

Gain Insight into Financial Stability

Credit checks also shed light on a tenant’s financial stability. Surveys show that 18% of individuals face financial distress, but understanding an applicant’s credit profile can help you discern risk levels. For instance, if a potential tenant has a history of late payments or high credit utilization, it may signal difficulties in sustained financial health.

Comparative Analysis of Credit Quality

| Credit Score Range | Likelihood of Late Payments | Average Rent Payment History | Percentage of Financial Distress |

|---|---|---|---|

| 300-579 | 75% | Often late | 50% |

| 580-669 | 50% | Usually on time | 30% |

| 670-739 | 30% | Consistently on time | 15% |

| 740+ | 10% | Always on time | 5% |

Real-World Implications

In practical terms, running credit checks can lead to better tenant selection. For instance, if an applicant’s credit report reveals too many recent inquiries or derogatory marks, it can suggest a potential for future problems, enabling you to make the decision to deny their application confidently.

Consider a landlord who, after several instances of missed rent payments, decided to adopt credit checks. By filtering out applicants with poor credit histories, they reduced the instances of late payments by over 40%. This not only safeguarded their income but also strengthened their overall tenant portfolio.

Actionable Advice

- Always incorporate credit checks into your tenant screening process to gauge financial reliability.

- Look for patterns in credit behavior, such as payment timeliness and overall credit utilization.

- Utilize credit checks to compare potential tenants against industry benchmarks, enhancing your decision-making process.

By understanding and leveraging the benefits of credit checks, you position yourself to make informed choices that ultimately enhance your rental experience and protect your financial interests.

Case Studies of Successful Tenant Screening

In the world of rental property management, tenant screening is your first line of defense against potential issues. Through real-world case studies, we can learn valuable lessons about the effectiveness of rigorous tenant screening practices, especially when credit checks are involved.

Key Insights from Successful Tenant Screening

1. Consistent Application of Screening Criteria: Property managers who applied the same set of criteria uniformly reported fewer issues with tenants. A study revealed that consistently screening applicants led to a 25% decrease in late rent payments.

2. Integration of Credit Checks with Other Screening Tools: Case studies show that landlords using a combination of credit checks, employment verification, and rental history saw an 18% reduction in tenant defaults. This multi-faceted approach increases the chances of identifying reliable tenants.

3. Feedback Loop Improvements: One landlord implemented a system that allowed them to refine their screening process based on tenant performance metrics. By analyzing which screened tenants caused issues, they reduced problematic tenant placements by 40% within a year.

Tenant Screening Effectiveness Table

| Screening Method | Increase in Tenant Success (%) | Decrease in Late Payments (%) |

|---|---|---|

| Credit Check Only | 20% | 10% |

| Credit Check + Background Check | 35% | 15% |

| Credit Check + Employment Verification | 40% | 25% |

| Comprehensive Multi-Check Process | 50% | 30% |

Real-World Examples of Successful Tenant Screening

One notable case involved a large property management firm in California that employed a strict credit check policy combined with a rental history review. They found that 82% of tenants with credit scores above 700 had a record of timely payments over three years. This allowed them to focus their marketing efforts on reaching applicants within that demographic, improving both occupancy rates and tenant reliability.

In another instance, a small landlord in Texas utilized a tool that not only conducted credit checks but also integrated machine learning to analyze rental applications. Over three years, they reported that using this technology reduced tenant disputes by 50%. Landlords who leaned heavily on technology reported finding better matches between properties and tenants.

Practical Implications for Screening Success

As you implement your tenant screening process, consider the following actionable steps based on these case studies:

- Always apply screening criteria uniformly to all applicants to ensure fairness and mitigate risks.

- Combine credit screenings with other evaluations like employment verification to create a comprehensive view of your applicants.

- Use data from past tenancies to continually refine your screening criteria, adjusting it according to performance metrics.

By understanding and applying the lessons learned from effective tenant screening case studies, you can enhance your own screening process, protect your property investment, and ensure a smoother landlord-tenant relationship.