What is Personal Property Tax? It’s that bill you might see sneaking into your mailbox that catches you off guard, especially if you’re not prepared for it. Think of it as a tax on your tangible assets, like the cars you drive, the machinery in your business, or even the jewelry you wear. In places like Texas and California, personal property taxes can make up a significant chunk of local revenue, often funding essential services like schools and infrastructure. For instance, if you own a small business with equipment valued at $50,000, you could be looking at a tax bill that ranges anywhere from a few hundred to several thousand dollars each year, depending on local rates.

You might wonder why some items are tax-exempt, while others aren’t. Well, it usually boils down to state laws and definitions. For example, most states don’t tax personal belongings like clothing or household goods, but when it comes to that shiny new car parked in your driveway, you can bet the taxman is interested. According to the National Conference of State Legislatures, nearly 90% of states impose some form of personal property tax, creating a hefty financial consideration for businesses and individuals alike. This tax can have real implications on your bottom line, shaping decisions from purchasing new equipment to investing in property.

Defining Personal Property Tax Essentials

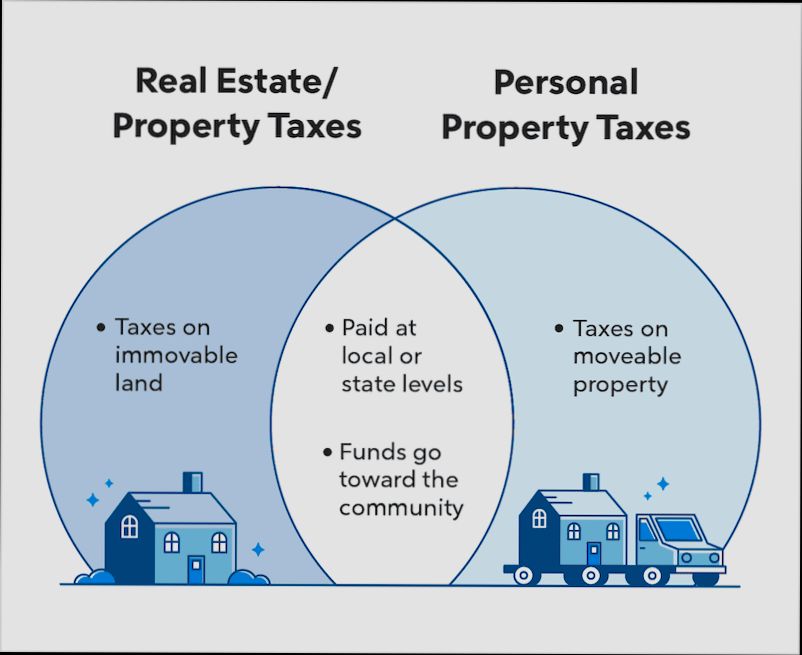

Understanding personal property tax essentials is crucial for managing your finances effectively. Personal property taxes apply to movable assets rather than fixed properties like land and buildings. Let’s dive into the key elements of personal property tax so you can navigate this complex area with confidence.

Key Points to Consider

1. Tax Rates and Valuation: Personal property tax rates can vary significantly based on your jurisdiction. For example, in Virginia, the vehicle tax rate is set at $4.57 per $100 of assessed value. This means that you’ll need to calculate the assessed value of your personal items to determine your total tax liability.

2. Types of Taxable Assets: Understanding what assets are taxable is essential. Common taxable items include:

- Motor vehicles (cars, trucks)

- Boats and watercraft

- Machinery (industrial and agricultural)

- Mobile homes

- Business equipment (computers, printers)

- Livestock (cattle, horses, etc.)

3. Penalties for Noncompliance: Failing to file personal property taxes or underreporting can lead to penalties. These penalties can range from 5% to 25% of the unpaid tax, emphasizing the importance of accurate and timely reporting.

4. Exemptions and Deductions: Certain jurisdictions offer exemptions based on specific criteria, such as business size or type of asset. It’s important to research available exemptions to potentially reduce your tax burden.

Comparative Tax Rate Table

| Asset Type | Jurisdiction Example | Tax Rate |

|---|---|---|

| Motor Vehicles | Virginia | $4.57 per $100 |

| Boats and Watercraft | Florida | 1.25% of assessed value |

| Business Equipment | California | Varies by county |

| Livestock | Texas | $0.00 for some types |

Real-World Examples

Take the case of a $1.6 billion refinery base-oil project that successfully attained a 10-year exemption, estimated to reduce property tax liabilities significantly. Such strategies show how understanding personal property tax regulations can benefit large investments.

Additionally, in regions where large quantities of oil and gas are stored, over 80 million barrels have been assessed for taxation. This demonstrates the scale on which personal property taxes impact various industries, particularly in resource-rich areas.

Practical Implications

For individuals and businesses, understanding personal property tax essentials means keeping detailed, accurate records of all taxable assets. This includes purchase receipts and values for depreciation. Accurate filing is not just a recommendation; it is necessary to avoid the financial pitfalls of noncompliance.

Actionable Advice

- Regularly consult local tax authorities to stay informed about applicable rates and regulations.

- Maintain thorough documentation of all personal property to support tax filings.

- Consider hiring tax professionals for complex assets to maximize potential savings and ensure compliance.

- Monitor deadlines closely to avoid incurring penalties, which can significantly increase your tax liabilities.

Understanding these essentials will empower you to manage your personal property tax obligations effectively.

Statistical Overview of Personal Property Tax

Understanding the statistical overview of personal property tax allows us to grasp its importance in local economies and to businesses. It provides insight into how widespread personal property tax is, which assets are commonly taxed, and the potential savings opportunities available to taxpayers.

Key Statistics

- In the United States, 37 out of 50 states, including the District of Columbia, levy taxes on business personal property. This signifies a strong reliance on personal property tax for funding local public services.

- Business inventory is included in the taxing process in 13 of those 37 states, indicating regional differences in the treatment of taxable assets.

- A notable example is the downstream chemical plant that secured abatements worth $160 million across two capital investment projects, ultimately reducing its tax liabilities by an estimated $3.2 million annually.

Comparative Table of Taxable Assets by Type and State Prevalence

| Asset Type | Taxed in States | Percentage of States Taxing |

|---|---|---|

| Business Equipment | 37 | 74% |

| Motor Vehicles | 50 | 100% |

| Machinery | 37 | 74% |

| Boats and Watercraft | Varies | Less Common |

| Aircraft | 37 | 74% |

| Mobile Homes | 37 | 74% |

Real-World Examples

Consider the downstream chemical plant, which illustrates how effectively businesses can manage personal property tax liabilities through strategic investments and negotiations. Securing abatements illustrates a proactive approach that can lead to significant annual savings.

Another example can be derived from the business owner filing returns illustrating that proactive engagement can also benefit them. By staying on top of deadlines and hiring experts to assess their property’s value, businesses are in a better position to appeal unjust valuations and reduce their tax burden.

Practical Implications for Readers

It’s crucial to be aware of specific deadlines for filing personal property tax returns to avoid penalties and interest charges. Actively managing your documentation and filing timely can save you from financial setbacks.

Engage with tax professionals who specialize in personal property assessments; they can help you navigate the complexities of the tax system and identify further opportunities for exemptions or reductions specific to your business property.

Actionable Advice

- Businesses should familiarize themselves with the thresholds for personal property tax exemptions that may apply to their specific assets.

- You can actively seek out local laws regarding the assessment of personal property tax to understand your obligations.

- Review potential exemptions and ensure you engage an expert to monitor changes in assessment values and filing requirements regularly.

By understanding these statistics and actionable insights, you can maximize your savings and compliance in relation to personal property tax.

Real-World Examples of Personal Property Tax

Understanding real-world examples of personal property tax helps to clarify how these taxes function in our daily lives. Personal property tax applies to various movable assets you or your business may own, affecting both individuals and companies alike. Let’s explore some specific instances and implications.

Key Types of Taxable Assets

Personal property tax encompasses a range of assets, including but not limited to:

- Motor Vehicles: Cars, trucks, and motorcycles are frequently taxed based on their registered value.

- Boats and Watercraft: From small fishing vessels to luxurious yachts, these are assessed for tax based on their current market value.

- Business Equipment: Items such as computers and office furniture contribute to tax obligations for business owners.

Comparative Analysis of Personal Property Types

| Property Type | Estimated Tax Rate (%) | Common Locations |

|---|---|---|

| Motor Vehicles | 1.25% - 2.5% | Nationwide |

| Boats and Watercraft | 1% - 2% | Coastal States |

| Business Machinery | 1.5% - 3% | Industrial Areas |

| Aircraft | 2% - 3% | Aviation Hubs |

Real-World Applications

1. Motor Vehicles: In Georgia, the personal property tax on vehicles is based on the fair market value, leading to varied tax amounts. For example, if I own a truck worth $20,000, I might end up paying around $500 in personal property tax at an average rate of 2.5%.

2. Business Equipment: A small business in Texas may face a personal property tax bill based on its equipment value. If a company has $50,000 in taxable machinery, and the local tax rate is 2%, that equates to a $1,000 tax liability annually.

3. Boats and Watercraft: In states like California, if you own a boat valued at $30,000, your personal property tax might be around $600 if assessed at an estimated rate of 2%.

4. Aircraft: A private plane worth $100,000 in Florida could incur taxes of $2,000 if the local rate is set at 2%. This shows how significant assets can lead to substantial tax bills.

Practical Implications

- For businesses, keeping detailed records of all taxable items is crucial. This includes purchase dates, depreciated values, and tax correspondence.

- Accurate filing of property values is essential. For instance, neglecting to report an aircraft could lead to significant penalties.

- Business owners should consult local tax professionals to understand regional variations and maximize any allowable deductions.

Actionable Tips

- Track Asset Value Changes: Regularly assess how depreciation affects the value of your assets to report accurately and avoid overtaxation.

- Explore Exemptions: Some jurisdictions offer exemptions or reduced rates for certain types of personal property, especially for small businesses or manufacturing equipment.

- Consider Lease Tax Implications: Leased business equipment can also be subject to property taxes, often overlooked by lessees. Being aware of your obligations here is essential.

Impacts of Personal Property Tax on Businesses

Understanding the impacts of personal property tax (PPT) on businesses is crucial, as it directly influences financial planning and operational strategies. This tax affects what businesses pay on their tangible assets, and managing these responsibilities can enhance or strain your financial resources. Let’s dive deeper into how personal property tax impacts business operations.

Key Points of Impact

1. Increased Operational Costs: As businesses acquire more personal property, their tax liabilities can increase significantly. For instance, if a business adds new equipment or technology, it could face a 5% increase in its annual PPT, directly affecting cash flow.

2. Compliance Risks: Failure to accurately report business personal property can trigger substantial compliance issues. Assessors might impose arbitrary assessments based on outdated data, leading to unexpected tax bills that can impact budgetary allocations.

3. Impact on Expansion Plans: Expansion strategies could be hindered by increased tax liabilities. For instance, businesses planning to upgrade machinery must consider that new assets will add to their personal property tax bills, possibly leading to a 25% increase in their overall tax burden during rapid growth phases.

Comparative Table of Tax Increases by Asset Type

| Asset Type | Average Tax Increase (%) | Compliance Risk Level |

|---|---|---|

| Machinery | 5% | Moderate |

| Office Equipment | 10% | High |

| Vehicles | 15% | Moderate |

| Inventory (varies) | Up to 25% | High |

| Technology Upgrades | 5-15% | Moderate to High |

Real-World Examples

- Case Study 1: A mid-sized manufacturing firm upgraded to state-of-the-art machinery. They initially estimated their personal property tax would rise by approximately 10%. However, upon receiving the first tax bill, they faced a shocking 20% increase due to a lack of accurate reporting on the appraisal of newly acquired assets.

- Case Study 2: A retail business expanded its inventory. The owner underestimated the tax implications, which resulted in a 25% increase in their property tax, significantly impacting their operational budget and forcing a delay in further hiring.

Practical Implications for Business Owners

Being proactive in understanding the implications of personal property tax can lead to better financial health. Here are some actionable insights:

- Regular Asset Assessments: Routinely evaluate your business assets and their depreciated values to ensure accurate tax reporting, which helps avoid overpayments.

- Tax Budget Planning: Integrate potential tax liabilities into your broader financial planning, including cash reserves to manage sudden increases in personal property tax.

- Professional Guidance: If your business operates in multiple jurisdictions, seeking compliance services can save you from critical missteps. Consider partnering with experts who specialize in property tax to navigate complex regulations effectively.

- Leverage Depreciation: Make use of depreciation expense calculation services available in your area to understand how asset values affect your tax liabilities. This insight can significantly impact your annual budget.

By approaching personal property tax with a well-informed strategy, businesses can mitigate risks and make financially sound decisions that foster growth and innovation.

Advantages of Personal Property Tax Compliance

When it comes to personal property tax compliance, understanding its advantages can not only simplify your financial responsibilities but also maximize your benefits. Compliance isn’t just about avoiding penalties; it’s about leveraging potential opportunities for savings and stability.

Key Advantages of Compliance

1. Avoiding Penalties and Interest: Non-compliance can lead to hefty penalties, and interest can accumulate quickly. In Virginia, for example, failure to pay the vehicle tax rate of $4.57 per $100 of assessed value can result in additional charges that add up over time.

2. Access to Legal Deductions: Properly reporting your personal property can help you qualify for valuable deductions. Many localities may offer exemptions or reductions for certain types of assets. For example, if you have agricultural machinery, ensuring that it is properly documented may lead to lower tax bills.

3. Maintaining Good Standing with Local Authorities: When you file your personal property taxes correctly and on time, you enhance your credibility with local authorities. This good standing can help in gaining permits or licenses essential for operating a business, as many governmental processes require proof of tax compliance.

4. Simplified Planning for Asset Depreciation: Staying compliant provides you with a clearer picture of your assets’ depreciation. Accurate records can help you make informed decisions regarding asset management and future purchases.

5. Improved Asset Management: Detailed records maintained for compliance allow businesses to track their assets more effectively. You will know not only what you own but also how your assets are performing financially, leading to improved operational decisions.

Comparative Advantages of Compliance

| Advantage | Description | Example |

|---|---|---|

| Avoiding Penalties | Helps prevent late fees and additional charges | Save on late fees from missed deadlines |

| Access to Deductions | Qualify for local exemptions and allowances | Reduced tax burden on eligible business assets |

| Good Standing with Authorities | Maintains credibility necessary for licenses and permits | Ease in obtaining business licenses |

| Clear Depreciation Tracking | Facilitates better financial planning | Forecast asset value for future investments |

| Enhanced Asset Management | Aids in efficient tracking and management of assets | Better decision-making on asset utilization |

Real-World Examples

Imagine owning a fleet of delivery trucks. By maintaining compliance with personal property tax requirements, you won’t only avoid penalties, but you might also find that your local government provides incentive programs to businesses that can demonstrate proper asset documentation.

Another case involves a small business that diligently filed its personal property taxes, which qualified it for state grants aimed at supporting local enterprises that invest in specific equipment, like eco-friendly machinery.

Practical Implications

To maximize these advantages, take actionable steps such as:

- Keep Comprehensive Records: Maintain detailed records of all taxable personal property, including receipts and depreciation schedules. This practice simplifies compliance and ensures you are ready for any tax-related inquiries.

- File Accurately and Timely: Use the correct forms and double-check all calculations before submission. Ensuring accuracy prevents unnecessary audits and eliminations of unexpected penalties.

- Consult with Tax Professionals: If your assets or tax situation is complex, working with a tax professional allows you to navigate local laws effectively and potentially uncover deductions or exemptions you might otherwise miss.

Key Takeaway

Understanding and embracing the advantages of personal property tax compliance is essential for financial stability. It not only helps you avoid unnecessary penalties but also opens opportunities for deductions and improved asset management. Regularly review your assets, stay informed about local tax laws, and don’t hesitate to seek professional advice when needed to ensure you are reaping the full benefits of compliance.

Navigating Personal Property Tax Regulations

Understanding personal property tax regulations is essential for anyone wanting to manage their assets efficiently. These regulations can often seem complex, but breaking them down into manageable parts makes it easier for you to stay compliant and make informed financial decisions.

Key Considerations When Navigating Regulations

1. Filing Requirements: Each state has specific filing requirements for personal property declarations. Some states require annual filings, while others may only require declarations every few years. Staying updated with your state’s timeline helps avoid late fees and penalties.

2. Valuation Methods: Different methods for valuing personal property can impact your tax obligations. Familiarizing yourself with these methods ensures you report your property accurately, whether it’s market value, replacement cost, or income approach.

3. Exemptions and Deductions: Certain personal property may qualify for exemptions or deductions, such as machinery or equipment used for specific business purposes. Researching these allowances could significantly reduce your taxable amount. For instance, many states offer a tax exemption for the first $100,000 of business personal property.

4. Audits: Be prepared for possible audits from tax authorities. Regularly reviewing your property tax filings and maintaining thorough records can help in managing this process effectively. Statistically, 15% of businesses may face an audit every year, underscoring the need for proper documentation.

Comparative Overview of State Regulations

| State | Filing Frequency | Valuation Method | Exemption Threshold |

|---|---|---|---|

| California | Annual | Market Value | $100,000 for business property |

| Texas | Biennial | Acquisition Cost | Machinery exemptions apply |

| New York | Annual | Depreciated Value | Up to $25,000 exemption |

| Florida | Annual | Replacement Cost | Certain agricultural equipment only |

| Virginia | Annual | Fair Market Value | No statewide threshold |

Real-World Examples

- California’s Proposition 13: A key example is California’s Proposition 13, which limits property tax increases to 2% per year, providing a stable tax environment for property owners and business investors alike. Navigating these regulations properly can make a substantial difference in long-term financial planning.

- Texas Machinery Tax Exemptions: In Texas, new manufacturing facilities may qualify for a full exemption from personal property tax for the first two years of operation. Understanding this can lead to significant tax savings while establishing your business presence.

Practical Implications for You

As you navigate personal property tax regulations, pay particular attention to local laws that may differ significantly from state regulations. Tax codes can change, so it’s wise to subscribe to updates from your local tax office or join property tax-related forums.

Begin gathering necessary documentation early in the tax year to prepare for filing deadlines, and consider hiring a tax consultant if the regulations in your area are particularly complex. This proactive approach can save not only time but also potential future expenses.

Seek out resources like state tax websites or chambers of commerce for current changes that may impact your property tax obligations. Staying informed not only helps with compliance but could reveal new opportunities for reducing your personal property tax burden.

Common Misconceptions About Personal Property Tax

Understanding common misconceptions about personal property tax can empower you to navigate this complex financial obligation more effectively. Many people hold misunderstandings that may lead to confusion and even financial penalties. Let’s debunk some of these myths together.

Misconception 1: Personal Property Tax Applies Only to Businesses

One of the most widespread misconceptions is that personal property tax exclusively targets businesses. While it’s true that many commercial assets are taxable, personal property tax also affects individuals.

- Vehicles: Many states tax personal vehicles separately from real estate. Did you know that personal vehicles account for over 30% of all reported personal property tax filings?

Misconception 2: Personal Property Tax is a One-Time Fee

Another common myth is that personal property tax is a one-time payment. In reality, this tax is typically assessed annually.

- Depending on your location, you could face recurring charges that vary based on asset valuations. For example, in some locales, you might see a 12% increase in annual assessments if a vehicle’s market value rises.

Misconception 3: Value of Assets is Always What You Paid

Many believe that the tax value of their personal property is always equivalent to the purchase price. In actuality, tax assessments can differ significantly from what you actually paid.

- Depreciation: Most jurisdictions apply depreciation to calculate taxable value. This means that your asset’s assessed value could be significantly lower, impacting your tax bill. In some cases, cars lose nearly 20% of their value each year, which might lower your personal property tax liability.

| Misconception | Reality | Impact on Tax Liability |

|---|---|---|

| Only businesses pay personal property tax | Individuals also pay for personal assets | Could lead to unexpected taxes |

| It’s a one-time fee | It’s usually assessed annually | Recurring costs over time |

| Asset value equals purchase price | Taxable value often reflects depreciation | Could lower tax obligations |

Real-World Examples

Consider Emily, a homeowner who believed her car wouldn’t be taxed because it was no longer in use. She later found out that it was still on her tax rolls, leading to unexpected fees. Similarly, a small business owner wrongly assumed he only needed to pay personal property tax once his equipment was purchased. When he learned that it was an annual expense, he adjusted his budget accordingly.

Practical Implications

It’s crucial to grasp these misconceptions to avoid surprises when it comes to your financial obligations. By understanding that personal property tax applies to both individuals and businesses, is recurring, and that asset valuations can change, you can better prepare for potential liabilities.

- Stay Informed: Check with local tax authorities to learn how personal property taxes are structured in your area.

- Budget Accordingly: If you’re an individual with taxable assets, factor annual assessments into your budget.

- Watch for Depreciation: Keep an eye on how your assets depreciate over time, as this will directly influence your taxable value.

By clearing up these common misconceptions, you can navigate the complexities of personal property tax with greater confidence and accuracy. Remember, knowledge is power when it comes to managing your financial responsibilities.