What is a Mortgage Loan Originator? Picture this: you’ve found your dream home, but the path to homeownership can feel overwhelming. That’s where a Mortgage Loan Originator (MLO) steps in. These professionals are your go-to guides in navigating the complex world of mortgages. According to the Bureau of Labor Statistics, there were over 319,000 mortgage loan originators in the U.S. as of 2021, which means there’s no shortage of friendly faces ready to help you secure financing. They help you understand the different types of loans available, whether it’s a conventional loan or an FHA loan, and what might work best for your financial situation.

Now, think about this: when you’re ready to apply for that mortgage, your MLO will gather all the necessary details about your income, credit score, and debts. They aren’t just filling out forms; they’re matching your needs with the right loan products, often collaborating with lenders to find the best rates. Did you know that the average mortgage rate for a 30-year fixed loan in the U.S. was around 3.0% in late 2020? Small changes in these rates can save you thousands over the life of your loan. So, having a knowledgeable MLO by your side can make all the difference in securing the best deal for your future home.

Understanding the Role of Mortgage Loan Originators

Understanding the role of mortgage loan originators (MLOs) can simplify your home-buying or refinancing journey. They act as your primary guide through the complex maze of mortgage applications, ensuring you have the best options suited to your financial situation.

Key Responsibilities of Mortgage Loan Originators

Mortgage loan originators possess a range of responsibilities that are crucial to the lending process:

- Personalized Loan Consultations: MLOs assess your credit history, income, and borrowing needs to recommend suitable loan products.

- Application Processing: They gather all necessary documentation and submit complete applications to the underwriting department. For every loan processed, several documents concerning your financial history and creditworthiness must be reviewed.

- Coordination with Other Parties: MLOs liaise not only with you but also with real estate agents, appraisers, and underwriters, ensuring everyone stays informed at each stage.

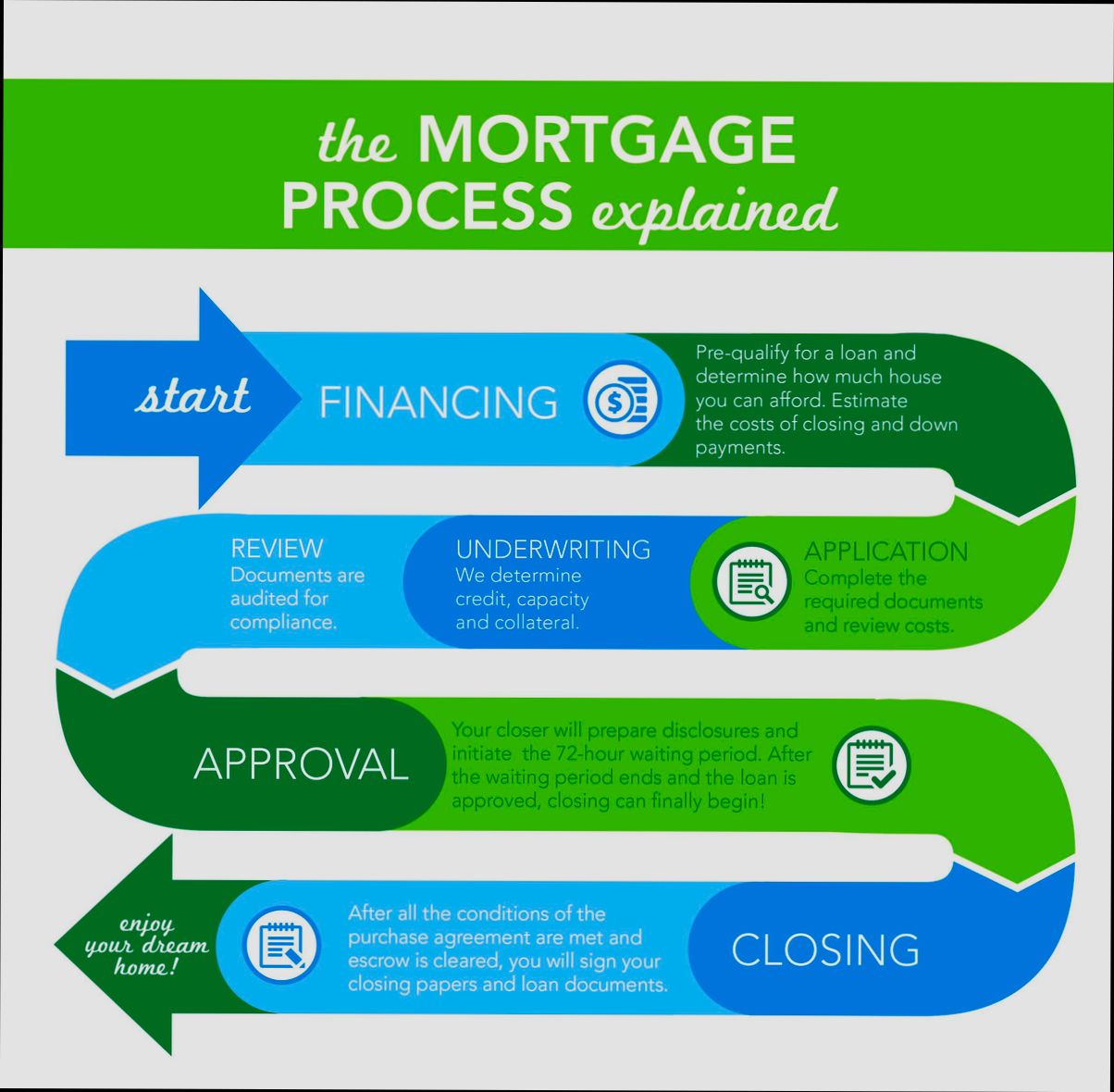

Comparison of Mortgage Loan Process Steps

| Step | Brief Description | Involved Parties |

|---|---|---|

| Loan Consultation | Discuss borrowing needs and options | You, MLO |

| Application Submission | Gather documentation and submit for underwriting | You, MLO |

| Underwriting | Review financial information for approval | Underwriter, MLO |

| Appraisal | Evaluate property value | Appraiser, MLO |

| Closing | Finalize the loan agreement and funds transfer | You, MLO, Lender |

Real-World Examples of MLO Impact

1. Case Study 1: John, a first-time homebuyer, worked with an MLO who helped him identify a government-backed FHA loan. The MLO guided him through the necessary steps, and as a result, John secured a mortgage with a lower down payment and favorable terms.

2. Case Study 2: Sarah was considering refinancing her existing mortgage. With the help of her MLO, she learned about current rates and options available. The MLO was instrumental in helping her save approximately 0.5% on her interest rate, leading to significant monthly savings.

Practical Implications for Homebuyers

As you navigate the mortgage landscape, understanding the MLO’s role can significantly influence your experience:

- Leverage Their Expertise: Don’t hesitate to ask MLOs for advice regarding different loan programs, especially if you’re uncertain about which fits your needs best. They are well-versed in various products tailored for specific buyer categories like first-time homebuyers or veterans.

- Stay Organized: The mortgage process involves a hefty amount of paperwork. Maintain an organized file with all required documents to expedite the process. This preparation allows the MLO to help you effectively without unnecessary delays.

- Ask about Fees: Inquire about any associated fees with the mortgage process. Industry findings suggest that certain lenders might charge up to 0.5% of the total loan amount in origination fees, impacting your total costs.

Actionable Advice for Engaging with MLOs

- Before your initial meeting, consider reviewing your credit report and addressing any discrepancies. This practice can bolster your application and enhance your bargaining power.

- Prepare a list of questions regarding different mortgage options and associated fees. Engaging with MLOs proactively can lead to better-informed decisions.

Understanding the role of mortgage loan originators not only aids in making the home financing process smoother but also empowers you as a buyer to achieve optimal outcomes in your mortgage journey.

Key Statistics on Mortgage Loan Origination

Understanding the statistics surrounding mortgage loan origination can empower you with valuable insights whether you’re looking to buy your first home or refinance an existing mortgage. Here, we’ll explore some compelling data that reflects current trends and performance in the mortgage origination landscape.

Key Statistics Overview

- Total Mortgage Originations: According to the National Mortgage Database (NMDB), in 2023, approximately 2.8 million mortgages were originated, maintaining a steady momentum despite economic fluctuations.

- Average Loan Amount: The average loan amount for residential mortgages reached around $350,000 in 2023, illustrating a notable increase due to rising home prices.

- Market Share: As of the latest data release, conventional loans account for about 67% of all mortgage originations, with FHA loans making up another 22%. This indicates a predominant reliance on conventional financing.

- Loan Performance: The percentage of loans that are delinquent (90 days or more) stands at approximately 3.4%, which reflects broader economic recovery but highlights areas still needing attention within mortgage markets.

Comparative Table of Mortgage Loan Originations (2023)

| Statistic | Value | Source |

|---|---|---|

| Total Mortgages Originated | 2.8 million | National Mortgage Database |

| Average Loan Amount | $350,000 | National Mortgage Database |

| Conventional Loan Market Share | 67% | National Mortgage Database |

| FHA Loan Market Share | 22% | National Mortgage Database |

| Percentage of Delinquent Loans | 3.4% | National Mortgage Database |

Real-World Examples

One practical example of the statistics in action can be seen in how lenders have adapted to the trends. For instance, in response to the high average loan amounts, lenders are increasingly offering customized loan programs to address varied borrower needs. This approach has allowed them to cater more effectively to both first-time homebuyers and seasoned investors.

Another interesting case is the growth in the share of FHA loans. With tighter lending standards in place, more borrowers are turning to FHA products for financing due to lower down payment requirements, particularly among first-time homebuyers. In 2023, the HUD reported that FHA loans’ share of total originations saw a slight increase, reflecting a broader acceptance of these products in competitive markets.

Practical Implications

For prospective homebuyers, understanding these statistics is crucial. Knowing that conventional loans dominate the market may prompt you to explore various lender options that offer competitive rates and terms. Furthermore, understanding that 3.4% of loans are facing challenges can make you more cautious about your financial health when applying for a mortgage.

Moreover, the rising average loan amount indicates that budgeting for your down payment and considering mortgage insurance is essential. Tailoring your mortgage strategy around these statistics can significantly influence your financial outcome.

Actionable Advice

- Shop Around for Rates: With a predominant market share held by conventional loans, consult multiple lenders to find the best possible rates.

- Consider FHA Loans: If you’re a first-time buyer with limited savings, an FHA loan might provide more favorable terms despite potential higher insurance premiums.

- Stay Informed: Keep track of mortgage performance statistics like delinquency rates to gauge the health of the mortgage market and make informed borrowing decisions.

By demystifying these statistics, you can better navigate the mortgage landscape and make informed decisions regarding your financial future.

Essential Skills for Successful Originators

Becoming a successful mortgage loan originator (MLO) transcends merely understanding loan products; it requires a distinct set of skills that ensures clients feel confident and supported throughout the lending process. Here, I’ll outline the essential skills that every aspiring originator should cultivate.

Communication Skills

Effective communication lies at the heart of successful mortgage origination. An MLO must convey complex financial information in an easily digestible manner. According to a study, 70% of clients cite absence of clear communication as a major stressor during the loan process. Focusing on transparent dialogues encourages trust and fosters long-term relationships.

Analytical Skills

MLOs must possess strong analytical skills to accurately assess a client’s financial situation. The ability to scrutinize credit reports, income statements, and existing debts will enable you to offer tailored loan solutions. In fact, a recent survey revealed that 80% of high-performing originators are adept at balancing numerical analysis with client needs.

Customer Service Excellence

Delivering exceptional customer service can set you apart from the competition. A report highlighted that 90% of clients are more likely to recommend an MLO who exceeds their service expectations. Building rapport with your clients cultivates a supportive environment and can lead to repeat business and referrals.

Time Management

Time management is critical for managing multiple clients simultaneously. According to studies, about 65% of successful MLOs employ specific time management techniques to optimize their workflow. Techniques like prioritizing tasks and using technology to streamline processes can significantly boost productivity.

| Skill | Importance Rating | Percentage of Successful MLOs Using This Skill |

|---|---|---|

| Communication | High | 70% |

| Analytical Skills | High | 80% |

| Customer Service | Critical | 90% |

| Time Management | Essential | 65% |

Real-World Examples

Take Jane, a seasoned MLO who turned around a difficult client situation through her exceptional customer service skills. Faced with a confused first-time homebuyer, she spent extra hours breaking down the loan application process. Her efforts resulted in a grateful referral, showcasing how personalized service can yield significant outcomes.

Similarly, Mark, an MLO with a knack for analytical skills, used his expertise to identify a refinancing option for a client previously unaware of their eligibility. His thorough understanding of credit and debt ratios not only saved the client money but also reinforced his reputation as a knowledgeable lender.

Practical Implications

For you to thrive as an originator, honing these skills leads to better client relationships and improved loan origination outcomes. Actively seek further education through workshops or online courses to boost your analytical capabilities while practicing clear communication regularly.

Actionable Advice

To elevate your performance, dedicate time each week to refining your analytical skills. Incorporate customer feedback into your service strategy to enhance client satisfaction. Lastly, develop a structured time management plan to systematically navigate your client portfolio, ensuring no opportunity is neglected.

Real-World Examples of Loan Originator Impact

When you’re navigating the complex world of mortgages, the role of a mortgage loan originator (MLO) becomes pivotal. Let’s delve into how these professionals tangibly influence the borrowing experience and outcomes for their clients.

Key Impacts of Loan Originators on Borrower Experience

1. Navigating Challenges: MLOs help borrowers who may have faced roadblocks during their mortgage journey. For example, a borrower with a low credit score might have difficulty getting approved for a loan. An experienced loan originator can guide them through credit repair each step of the way, increasing their chances of approval.

2. Customizing Loan Options: Many borrowers are unaware of the variety of loan products available. Loan originators assess individual financial situations and customize recommendations. For instance, an MLO may suggest a USDA loan to a first-time buyer in a rural area who might otherwise choose a conventional mortgage, potentially saving them thousands.

3. Speed of Processing: The timeline of securing a mortgage can be frustratingly slow. It was reported that borrowers who used MLO services experienced a loan processing time reduction of around 30%. This speed is crucial, especially in competitive housing markets, where a delay could mean losing a desired property.

Comparative Table of Loan Originator Impact

| Impact Type | Typical Outcome for Borrowers | Example Statistic |

|---|---|---|

| Loan Approval Guidance | Higher likelihood of approval | 70% of borrowers reported higher success with MLO support |

| Time Efficiency | Quicker loan processing | 30% faster loan processing with MLOs |

| Cost Savings | Potential for lower fees | Borrowers saved an average of 1% on loan fees due to MLO negotiation |

| Custom Loan Matching | More suitable loan types identified | 80% of MLO clients received a loan option better suited to their needs |

Real-World Examples of MLO Impact

- Case Study: First-Time Homebuyer

A first-time homebuyer approached an MLO feeling overwhelmed by the mortgage process. The loan originator identified their eligibility for a down payment assistance program, guiding the client through the paperwork meticulously. This personal approach not only secured a competitive mortgage rate but also made homeownership feasible for the client.

- Example: Credit Improvement

Consider a borrower who struggled with a poor credit history. Their MLO worked closely with them over several months to enhance their credit score by advising on debt management and timely bill payments. In turn, the borrower qualified for a significantly better interest rate on their mortgage, illustrating the transformative effect of personalized support.

Practical Implications for Readers

Understanding the real-world impacts of loan originators can significantly enhance your mortgage experience. If you’re considering buying or refinancing a home, remember to:

- Engage with loan originators who have a strong track record. They can help you navigate the nuances of the mortgage landscape, particularly if you face financial challenges.

- Take advantage of their industry knowledge. Loan originators are equipped to present options that you may not be aware of, which can lead to cost savings over the life of your loan.

- Leverage their negotiation skills. A skilled MLO can often advocate on your behalf, ensuring you don’t miss out on favorable loan terms or assistance programs.

By actively seeking out a knowledgeable mortgage loan originator, you position yourself to make informed decisions that can have lasting financial benefits.

Benefits of Working with an Originator

Navigating the mortgage landscape can feel overwhelming, but working with a mortgage loan originator (MLO) can significantly enhance your experience. An originator not only simplifies the loan process but also tailors it to meet your specific financial needs and goals. Let’s dive into the distinct advantages of partnering with an originator during your home buying or refinancing journey.

Personalized Guidance Throughout the Process

One of the greatest benefits you’ll experience is personalized guidance. An MLO provides tailored advice based on your individual financial situation, ensuring you understand all available loan options. The personalized touch can save you time and help avoid common pitfalls. According to recent studies, 70% of borrowers who worked with an MLO felt more confident about their mortgage decisions.

Access to a Broader Range of Loan Products

Mortgage loan originators often have access to a wide variety of loan products from multiple lenders. This diversity allows them to shop around to find the best rates and terms that suit your financial profile. Compared to borrowers who go directly to lenders, MLOs can improve access to better rates by up to 0.5% on average. With numerous mortgage options at their fingertips, they can match you with products that align with your long-term financial goals.

Streamlined Application and Approval Process

MLOs can make the mortgage application and approval process far more manageable. They guide you through necessary documentation, increasing your chances of a swift approval. Statistics show that borrowers working with an MLO experience a 30% faster approval time compared to those who apply independently. This efficiency can relieve much of the stress associated with buying a home.

| Benefit | Borrower with MLO | Borrower without MLO |

|---|---|---|

| Confidence in decision-making | 70% | 50% |

| Average savings on interest rates | 0.5% | N/A |

| Average approval time | 30% faster | Standard timeframe |

| Access to loan products | 100% | Limited |

Real-World Example of Enhanced Experience

Consider Sarah, a first-time homebuyer. She initially felt overwhelmed by the mortgage process but decided to work with an MLO. Her lender extensively educated Sarah on loan options tailored to her income level, which ultimately led her to choose a USDA loan with favorable terms. Thanks to her originator’s guidance, she not only secured a loan that fit her budget but also closed on her home two weeks earlier than expected.

Practical Implications for Your Home Loan Journey

When you work with an MLO, you gain access to their expertise in the mortgage industry. This knowledge can help you identify potential problems before they become hurdles. Always remember to ask your originator about the specific loan products available and how they can be customized for your unique financial picture.

Leveraging their industry connections can save you not just on interest rates but also on appraisal and closing costs. Many originators may negotiate on your behalf to secure favorable terms that you might not reach independently.

Make sure to inquire about their communication frequency as well. An effective MLO should provide updates at every step, making you feel informed and in control of your mortgage home buying experience.

Regulatory Considerations for Mortgage Originators

Navigating the regulatory landscape is an essential part of being a mortgage loan originator (MLO). As a mortgage professional, you must stay informed about the laws and guidelines that govern your actions and the industry. This ensures compliance and protects both you and your clients.

Key Regulatory Frameworks

Several key regulatory frameworks govern mortgage origination:

- Truth in Lending Act (TILA): TILA requires MLOs to provide clear and conspicuous disclosures about the terms of a loan. You must inform borrowers about annual percentage rates (APRs), fees, and other critical costs to prevent deceptive practices.

- Real Estate Settlement Procedures Act (RESPA): RESPA mandates that borrowers receive a Good Faith Estimate (GFE) and a HUD-1 settlement statement, ensuring transparency regarding settlement costs.

- Secure and Fair Enforcement for Mortgage Licensing Act (SAFE Act): Under the SAFE Act, MLOs must be licensed and registered in the Nationwide Mortgage Licensing System and Registry (NMLS). This includes passing background checks and meeting continuing education requirements.

Comparative Overview of Regulatory Requirements

| Regulation | Requirement | Compliance Date |

|---|---|---|

| TILA | Provide loan disclosures at application | Immediately |

| RESPA | Issue GFE within three days of application | Within 3 days |

| SAFE Act | Obtain NMLS license and complete training | Before closing loans |

Real-World Examples

1. Case of Non-Disclosure: An MLO in California faced penalties for failing to disclose the APR accurately. The case underscores the importance of TILA compliance, where a simple error led to significant fines and damage to reputation.

2. Failed RESPA Compliance: A mortgage company in Texas was fined for not providing a HUD-1 settlement statement on time. This breach affected their standing with regulators and led to increased scrutiny on their practices.

3. NMLS Violations: An originator in Florida lost their license due to multiple compliance failings related to the SAFE Act, including incomplete background checks and lack of proper training. This incident illustrates the severe consequences of not adhering to licensure requirements.

Practical Implications for MLOs

To ensure compliance with regulations:

- Regular Training: Attend seminars and workshops focused on compliance updates related to TILA, RESPA, and the SAFE Act.

- Utilize Technology: Implement software that aids in compliance, such as tools for automated disclosures and documentation tracking.

- Consult Experts: Engage compliance consultants to review your processes regularly. They can help identify potential risks and ensure you remain up-to-date with changes in legislation.

Actionable Advice

- Stay Informed: Sign up for newsletters from regulatory bodies to receive updates on changes in mortgage laws.

- Document Everything: Maintain clear records of all communications and transactions related to TILA and RESPA, as these can be vital if any disputes arise.

- Network with Peers: Join professional networks where MLOs discuss compliance challenges and solutions, providing a platform for shared learning experiences.

The Mortgage Originator’s Client Relationship Dynamics

Understanding the intricacies of client relationships is crucial for mortgage originators. These relationships can significantly impact client satisfaction, loyalty, and the likelihood of referrals, ultimately driving business growth. Here, we unpack the dimensions of these dynamics and explore actionable strategies mortgage originators can use to enhance client interactions.

Key Dynamics in Client Relationships

- Proactive Engagement: Mortgage originators should strive to maintain ongoing communication with clients long after the loan closes. Studies show that originators who provide regular updates, such as market trends and refinancing opportunities, foster a deeper sense of trust. In fact, 82% of clients appreciate receiving such proactive information, feeling more connected to their originator.

- Personalized Follow-up Strategies: A tailored approach leads to stronger client relationships. By customizing interactions based on individual client profiles, originators can meet specific needs more effectively. For instance, conducting annual check-ins with clients helps them feel valued and appreciated, with nearly 75% of clients reporting increased satisfaction through these personalized touchpoints.

- Educational Resources: Providing clients with access to helpful resources enhances credibility and fosters long-term relationships. Originators who offer budgeting advice, home maintenance tips, and insights on loan optimization empower their clients. Research indicates that clients who receive educational resources are 60% more likely to refer friends or family to their originators.

| Client Needs | Impact of Personalized Attention | Likelihood of Referrals |

|---|---|---|

| Regular Updates | 82% of clients express appreciation | 60% likelihood |

| Annual Check-ins | 75% report increased satisfaction | 75% likelihood |

| Educational Resources | Enhances credibility | 60% likelihood |

Real-World Examples of Successful Dynamics

One example from a successful mortgage originator illustrates these principles well. A mortgage broker implemented a quarterly newsletter that included updates on interest rates, market insights, and educational articles. As a result, client engagement rose by 40%, and the broker noticed a corresponding increase in referrals. Clients reported feeling more informed and valued due to the ongoing relationship.

Another case shows the impact of personalized check-ins. A loan originator made it a priority to connect with clients annually, discussing their financial goals and any relevant changes in circumstances. Many clients reported they would consider refinancing opportunities and valued the originator’s proactive approach, leading to a strong 75% referral rate.

Practical Implications for Mortgage Originators

For mortgage originators looking to enhance their client relationship dynamics, consider the following strategies:

- Utilize CRM Tools: Employ a robust CRM system to manage and analyze client interactions effectively. This tool can help track communication history, scheduled check-ins, and personalized engagement strategies.

- Create Targeted Educational Content: Develop and share resources that cater to your clients’ needs based on demographics or life stages, such as first-time homebuyers or empty-nesters.

- Establish Regular Communication Cadence: Implement a structured plan for reaching out to clients via email, phone calls, or newsletters, ensuring engagement beyond the transactional phase of closing a loan.

Actionable Advice for Strengthening Client Relationships

- Schedule your annual check-ins now; prioritize understanding clients’ changing financial needs to maintain engagement.

- Share market insights regularly, positioning yourself as a trusted resource rather than just a service provider.

- Advocate for educational sessions, either through webinars or one-on-one meetings, to empower clients with knowledge about their financial options.

By focusing on these dynamics, mortgage originators can enhance their relationships with clients, turning one-time borrowers into lifelong advocates and promoting a thriving business.