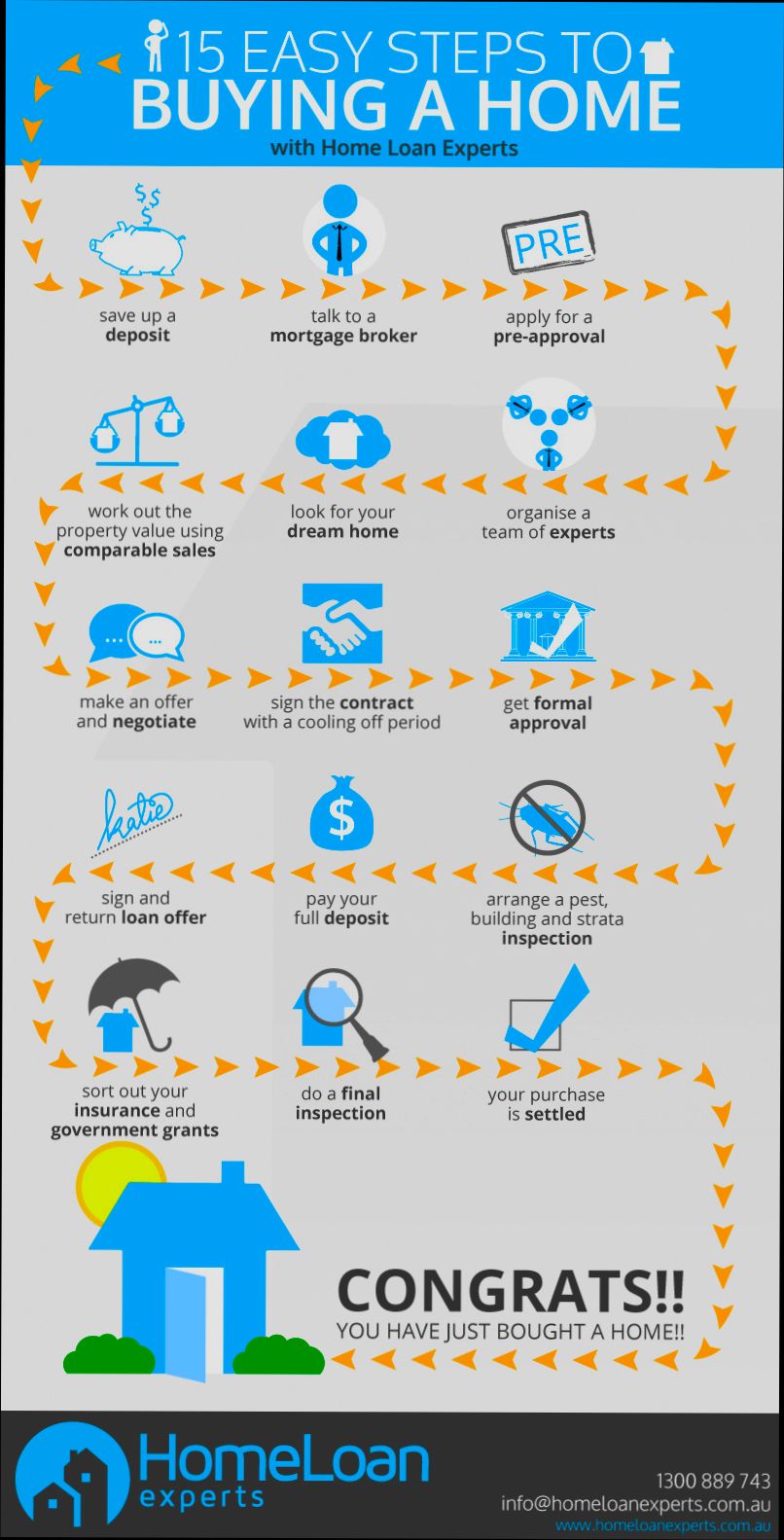

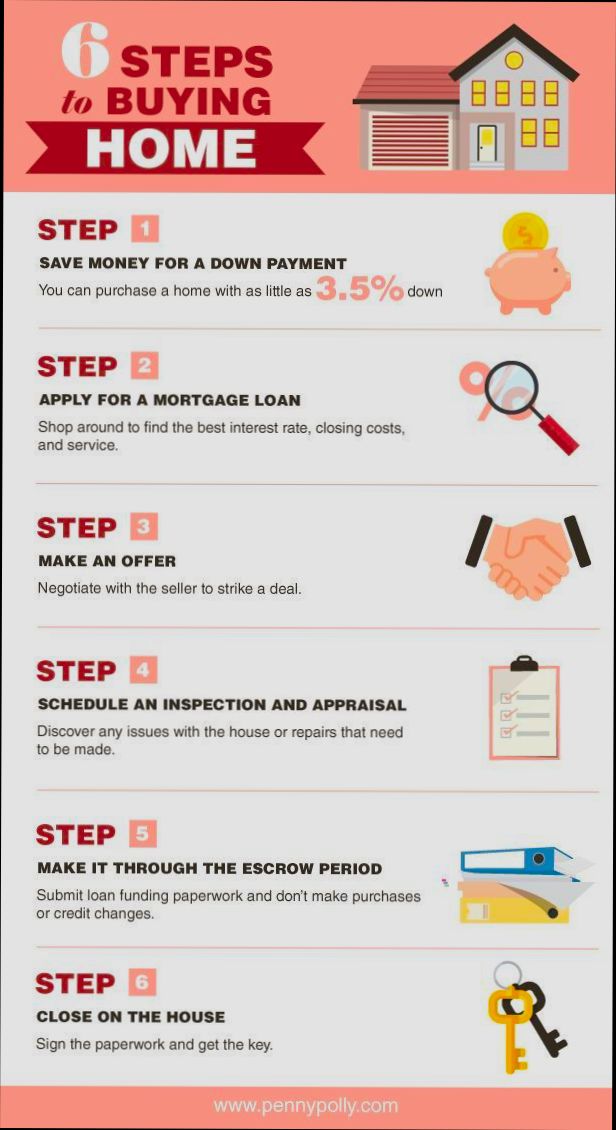

What do you need to buy a house? Well, let’s break it down. First off, you’re going to need some cash for a down payment, which typically ranges from 3% to 20% of the home’s price. So, if you’re eyeing a cozy $300,000 home, that means you could be looking at anywhere from $9,000 to $60,000 upfront. Ouch! But don’t forget your credit score plays a massive role, too. A score of 740 or higher usually gets you the best mortgage rates—saving you thousands over the life of your loan. Imagine paying less interest just because you’ve been diligent about your payments; it could mean the difference between affording that fancy new kitchen or settling for a fixer-upper.

Beyond the down payment and credit score, there are other pieces of the puzzle to consider. Lenders will want to see proof of income, so having your pay stubs and tax returns ready is a must. They also look at your debt-to-income ratio, which ideally should be under 43%. Let’s say you’re raking in $5,000 a month, and your total debt—including student loans, car payments, and credit cards—is $1,500. You’d be right in the sweet spot for many loan options. And don’t forget about other costs like closing fees and home inspections; they can stack up quickly!

Essential Financial Requirements for Homebuyers

When preparing to buy a home, understanding the essential financial requirements is crucial. It’s not just about having a down payment; several other factors play a key role in determining your eligibility and readiness to make a successful purchase. Let’s dive into the numbers and requirements that can help you be well-prepared.

Key Financial Requirements to Consider

1. Down Payment: Traditionally, the standard down payment is about 20% of the home’s purchase price. However, many buyers are opting for lower down payments. For instance, 44% of first-time homebuyers put down less than 10% in recent surveys.

2. Credit Score: Lenders typically require a minimum credit score of 620 for conventional loans. Interestingly, 27% of Americans have credit scores below this threshold, which can limit their options. Improving your credit score by just 20 points can potentially save you thousands in interest over time.

3. Debt-to-Income Ratio (DTI): Lenders look for a DTI ratio of no more than 43%. This includes your housing costs and other debts. A study showed that 43% of borrowers with a DTI above this limit were denied loans, emphasizing how important it is to manage your debts.

4. Savings for Closing Costs: In addition to your down payment, expect to save another 2% to 5% of the home price for closing costs. For example, for a $300,000 home, this means budgeting an additional $6,000 to $15,000.

Comparative Table of Financial Requirements

| Requirement | Typical Range/Minimum | Potential Impact |

|---|---|---|

| Down Payment | 3% to 20% | Affects loan type and monthly payments |

| Credit Score | 620 or higher | Influences interest rates |

| Debt-to-Income Ratio | Must be 43% or lower | Determines loan eligibility |

| Closing Costs | 2% to 5% of home price | Required in addition to down payment |

Real-World Examples

- Case Study 1: Emily, a first-time homebuyer, had a credit score of 700 and a DTI ratio of 40%. She managed to secure a conventional loan with a 5% down payment on a $250,000 home, saving $15,000 compared to a 20% down payment. This flexibility allowed her to invest her savings in home improvements right away.

- Case Study 2: John and Sarah faced challenges as they had a DTI of 47% due to student loans. After reducing their debt, they improved their DTI ratio to 41%. This change enabled them to get pre-approved for a mortgage, ultimately allowing them to purchase their ideal home.

Practical Implications for Homebuyers

- Start by checking your credit score and addressing any issues that may affect it. Every point counts when it comes to securing a favorable interest rate.

- Create a budget that incorporates not only the down payment but also closing costs. This comprehensive financial planning can save you from surprises during the home buying process.

- Regularly assess your DTI ratio. Consider strategies like paying down debts or increasing your income to improve your eligibility for a mortgage.

Specific Facts and Actionable Advice

- Aim for a solid down payment of at least 10% to avoid private mortgage insurance (PMI), which can add significant monthly costs.

- Be aware that about one in five borrowers was turned down for a mortgage due to insufficient credit score or DTI. Take proactive steps to ensure you meet or exceed these financial requirements.

- Set aside additional funds for emergency repairs or maintenance after purchasing. A good rule of thumb is to budget 1% of the home’s value annually for upkeep.

By staying informed and prepared about these essential financial requirements, you can enhance your chances of successfully buying your dream home.

Understanding Mortgage Types and Terms

When stepping into the world of home buying, understanding the various mortgage types and their terms is crucial for making informed decisions. This knowledge not only helps you choose the right loan but also aligns your mortgage with your financial situation and future goals.

Key Mortgage Types to Consider

1. Conventional Loans: These are not insured by the federal government and often require a higher credit score. According to the National Mortgage Database, as of 2023, approximately 65% of all mortgage loans are conventional.

2. FHA Loans: Insured by the Federal Housing Administration, these loans are great for buyers with lower credit scores and smaller down payments. The data shows that in 2022, FHA loans made up about 18% of the loan market.

3. VA Loans: Available for veterans and active-duty military members, these loans do not require a down payment and often have lower interest rates.

4. USDA Loans: These are for rural and suburban homebuyers who meet specific income requirements. About 2% of mortgage loans were USDA-backed as of 2023.

Comparative Mortgage Types Table

| Mortgage Type | Down Payment | Credit Score Requirement | Insurance Requirement | Typical Loan Term |

|---|---|---|---|---|

| Conventional | 5%-20% | 620+ | None | 15, 30 years |

| FHA | 3.5% | 580 or lower | Yes | 15, 30 years |

| VA | 0% | No minimum | None | 15, 30 years |

| USDA | 0% | No minimum | Yes | 30 years |

Real-World Insights

An example from the National Mortgage Database reveals that borrowers using FHA loans often enjoy lower monthly payments due to their smaller down payments. In contrast, conventional borrowers typically face higher payments but can avoid PMI (Private Mortgage Insurance) if they place a 20% or larger down payment.

Additionally, a recent FHFA report highlights that VA loans have a significantly lower default rate compared to conventional loans, which can reflect more favorable terms for veterans.

Practical Implications for Buyers

When selecting a mortgage, consider the following:

- Evaluate Your Credit Score: Knowing your score helps determine the types of loans for which you’re eligible.

- Understand Loan Terms: The length of the loan can influence your monthly payments and total interest paid over time. A shorter term usually means higher payments but lower total interest.

- Factor in Insurance Costs: Depending on the mortgage type, you may need to budget for additional insurance premiums, significantly impacting your monthly expenses.

Actionable Advice

Before committing to a mortgage type, I recommend reviewing your financial situation. Analyze how much you can afford for a down payment and whether you’re comfortable with the associated monthly payments, keeping in mind the long-term commitment of a mortgage. Understanding these terms can save you thousands over the life of your loan.

Crucial Data on Housing Market Trends

When you’re considering buying a house, understanding the current housing market trends is key. These trends can greatly influence your buying decision, helping you to act wisely in your home purchase.

Current Market Dynamics

- Median Home Price Increases: As of recent reports, the median home price has appreciated by 8% year-over-year in many metropolitan areas. This upward trend emphasizes the importance of timely decision-making in purchasing.

- Inventory Levels: Housing inventory remains below historical averages, with a 30% decline in available homes compared to the previous year. Low supply can lead to increased competition and higher prices.

- Days on Market: Homes are selling faster than ever, with the average days on the market dropping to just 21 days in many cities. This statistic should encourage prospective buyers to act quickly when they find a suitable home.

Comparative Market Trends Table

| Metric | Current Value | Change Year-Over-Year |

|---|---|---|

| Median Home Price | $350,000 | +8% |

| Inventory Level | -30% from last year | Significant Decline |

| Average Days on Market | 21 days | -15 days |

Real-World Examples

A local buyer in Austin, TX, recently faced these market conditions firsthand. After seeing a 10% increase in median prices over the last two years, they decided to place an offer on a home within 48 hours of viewing it, resulting in a successful purchase despite multiple competing bids.

In contrast, another buyer in Cleveland was able to negotiate down the price by 5% due to higher inventory levels, demonstrating that market conditions can vary significantly by region.

Practical Implications

Understanding these trends helps you determine the right time to buy and the price points to expect. If you notice a drop in inventory in your desired area, it may signal that you have to act faster than usual. Conversely, if you see increased inventory, it may provide leverage in negotiations.

- Monitor local housing reports for inventory and price changes.

- Consider your timeline: faster-moving markets require quicker decisions.

- Be prepared with financing options established before you start house hunting.

Actionable Insights

- It’s wise to set alerts for residential listings to keep up with pricing and inventory changes in your target area.

- Collaborate with a local real estate agent who has insights into current trends and can provide valuable market data.

- Evaluate past trends in your area—for example, if median prices have steadily risen over the past three years, it might suggest a pattern worth acknowledging in your budgeting.

Stay informed about these housing market trends so you can make the most educated decisions as you take steps toward homeownership.

Real-World Examples of Homebuying Success

When it comes to homebuying, real-world success stories can be incredibly inspiring. They not only illustrate the journey of prospective homeowners but also showcase strategies that contributed to their success. Let’s dive into some encouraging examples that highlight how individuals and families successfully navigated the complexities of purchasing a home.

Key Success Stories from the Real Estate Market

- Case Study: The Smith Family in Seattle

- After renting for five years, the Smiths saved steadily and managed to secure a home within a competitive market. They initially aimed for a property at $600,000, but by staying informed about market trends, they capitalized on a sudden drop in prices and purchased their dream home for $575,000—a 4% discount from their original goal.

- Young Professional: Jessica in Austin

- Jessica, a first-time buyer, took advantage of a first-time homebuyer program that offered a reduced interest rate. By leveraging this program, she was able to lock in a mortgage at 2.5%, saving her approximately $200 per month compared to traditional rates. This helped her manage her monthly budget more effectively.

- Retirees: The Johnsons in Orlando

- The Johnsons downsized from a large family home to a cozy condo. They strategically sold their previous home for $850,000, which allowed them to purchase their new condo for $300,000 and retire comfortably without financial strain. Their success lay in timing the market right and being patient until they found their ideal space.

| Case Study | Initial Purchase Goal | Final Purchase Price | Success Strategy |

|---|---|---|---|

| Smith Family | $600,000 | $575,000 | Market awareness leading to a price drop |

| Jessica | Not specified | $350,000 | First-time buyer program with a lower rate |

| Johnsons | $850,000 (sale price) | $300,000 | Downsizing and timing market effectively |

Practical Insights for Aspiring Homebuyers

1. Set a Clear Budget:

- Understand your financial situation and set a realistic budget. The Smiths benefited from knowing their limit and remained flexible when the market shifted.

2. Investigate Financial Assistance:

- Just like Jessica, look for available programs that can help reduce your costs. Various states offer incentives for first-time homebuyers and those in need of assistance.

3. Be Patient and Flexible:

- The Johnsons waited for the right moment to sell and buy, emphasizing the importance of timing in real estate. Don’t rush the process; instead, be prepared to wait for the right opportunity.

Actionable Advice for Future Homebuyers

- Stay Informed: Make it a habit to follow local housing market trends and reports. Knowledge is power when negotiating the best price.

- Network: Connect with other homeowners or professionals in real estate. They can offer valuable tips and insights based on their experiences.

- Consider Alternatives: Be open to different neighborhoods or types of properties. Sometimes, exploring “up-and-coming” areas can yield significant savings and opportunities for investment.

By examining these real-world examples and applying their strategies, we can all find a pathway to successful homeownership that aligns with our financial and personal goals.

Advantages of Homeownership Over Renting

When considering the choice between renting and buying a home, several compelling advantages can make homeownership an appealing option. From financial benefits to personal accomplishments, owning a home often provides a more stable and rewarding situation than renting.

Financial Growth and Stability

One of the most significant advantages of homeownership is the ability to build equity over time. While monthly rent payments simply go toward maintaining someone else’s property, your mortgage payments contribute to owning your asset.

- Growing Equity: As you pay down your mortgage, the equity in your home increases. Typically, homeowners can expect their equity to grow alongside property appreciation, which has historically averaged around 3-5% annually in many regions.

- Eligible Tax Deductions: Homeowners can enjoy tax benefits such as mortgage interest deductions and property tax deductions. These can significantly lower your tax bill compared to what renters face.

Predictable Payments and Escaping Rent Increases

Owning a home provides a certain financial predictability that renting simply cannot offer.

- Fixed Mortgage Rates: When you secure a fixed-rate mortgage, your monthly payments remain stable throughout the loan period. This contrasts sharply with renting, where costs can rise unpredictably, making it difficult to plan long-term finances.

- Absorb Market Fluctuations: With rising rents in many metropolitan areas exceeding local income growth, homeownership can be a more economical choice. For instance, rents have been observed to escalate faster than incomes in several locations, making buying a home often comparable to or even cheaper than continued renting.

Table: Cost Comparison of Rent vs. Mortgage Payments

| Aspect | Renting | Homeownership |

|---|---|---|

| Monthly Payment | Subject to annual increases | Fixed for the life of the loan |

| Equity Growth | None | Builds over time |

Tax Benefits | None | Available (interest and property tax)| | Market Control | Loss of stability in costs | Predictability in long-term expenses |

Real-World Examples of Homeownership Benefits

Consider the case of the Smith family, who transitioned from renting to owning a home. After five years of renting, their monthly mortgage payment ended up being $200 less than their rent, allowing them to save for other investments and education expenses. Furthermore, they experienced the property’s appreciation, adding approximately $50,000 to their equity over five years.

The Johnsons, retirees in Orlando, found that downsizing from a rented apartment to a smaller purchased home not only reduced their monthly payments but also provided them a fixed asset for potential future needs, such as long-term care.

Practical Implications for Aspiring Homeowners

Thinking of buying a home? Here are some actionable insights to consider:

- Evaluate local markets to find areas where buying is financially viable compared to renting.

- Leverage online calculators, like Zillow’s Rent vs. Buy tool, to better understand your financial positioning.

- Consult financial professionals to maximize tax benefits and explore different mortgage options based on your current situation.

By weighing these advantages, you can make a more informed decision about whether homeownership aligns with your financial goals and lifestyle needs.

Exploring Neighborhood Considerations in Property Purchase

When buying a house, the neighborhood can be just as important as the property itself. Your choice impacts not only your lifestyle but also the value of your investment. Let’s explore the critical neighborhood considerations that you should keep in mind during your property purchase journey.

Key Neighborhood Aspects to Evaluate

Before you commit to a home, consider evaluating these neighborhood factors:

- Safety and Crime Rates: Research shows that neighborhoods with lower crime rates can result in property value appreciation of up to 15% over time.

- School Quality: Areas with highly rated schools can see home values rise 20% higher compared to those in less desirable school districts.

- Local Amenities: Neighborhoods that offer parks, shopping centers, and recreational facilities often attract buyers, increasing demand and home values.

Neighborhood Comparison Table

| Neighborhood Feature | Neighborhood A | Neighborhood B | Neighborhood C |

|---|---|---|---|

| Average Crime Rate | Low | Medium | High |

| School Rating | 9/10 | 6/10 | 4/10 |

| Proximity to Public Transit | 1 mile | 3 miles | 5 miles |

| Local Amenities | Excellent | Good | Fair |

| Average Home Price | $350,000 | $300,000 | $250,000 |

Real-World Examples

- Case Study: The Johnsons in Springfield: When the Johnsons decided to move with their children, they prioritized school quality, opting for a neighborhood with a school rated 9/10. As a result, their home value has appreciated by nearly 18% in just five years.

- Example: The Garcia Family in Austin: The Garcias saved substantially by choosing a neighborhood with nearby public transit and local amenities, resulting in a lively community atmosphere. Their property saw a 12% increase in value due to increased demand.

Practical Implications

Consider community engagement, such as local events and homeowner associations, as these can affect your long-term satisfaction and property value. Getting to know your potential neighbors can provide insight into the community culture and compatibility with your lifestyle.

- Assess Walkability: Homes in walkable neighborhoods often sell for 10-20% more. A stroll through the area can give you a feel for the community vibe.

- Investigate Future Developments: Look into city plans for improvements or expansions, as these can significantly impact future property values.

Remember, taking the time to evaluate the neighborhood thoroughly will help ensure that you not only purchase a house but also find a community you want to be part of for years to come.

Importance of Home Inspections Before Buying

When preparing to buy a home, one crucial step often overlooked is the home inspection. This process can unveil hidden problems and save you from unexpected costs down the road. Let’s dive into why home inspections are essential before making such a significant investment.

Protecting Your Investment

A home inspection can protect you from potential pitfalls. Research indicates that up to 30% of homes that failed a sale did so due to significant issues found during inspections. Knowing the condition of a property helps you avoid purchasing a house that may require costly repairs.

Key Findings from Home Inspections

Statistics show the following common issues found during home inspections:

- Roofing Problems: 25% of inspections uncover significant roofing issues that could lead to costly repairs.

- Plumbing Issues: About 18% of homes show serious plumbing concerns, which can result in leaks and water damage.

- Electrical Systems: Up to 15% of homes have unsafe electrical wiring or outdated systems, posing potential fire hazards.

Common Issues Identified

| Problem Type | Percentage of Homes Affected |

|---|---|

| Structural Damage | 20% |

| HVAC Issues | 12% |

| Foundation Problems | 10% |

| Pest Infestation | 8% |

Real-World Examples

Consider the case of the Roberts family, who were excited to purchase their dream home. However, a thorough inspection revealed not only a leaky roof but also faulty wiring that needed immediate attention. Thanks to the inspection, they negotiated repairs with the seller and potentially saved thousands on future costs.

Another example is the Morales family, who thought they had found a great deal on a fixer-upper. After the inspection, they learned that the foundation needed significant work, which was estimated to cost $15,000. They ultimately decided to walk away and found a better property that didn’t come with such risky repairs.

Practical Implications for Buyers

For you as a prospective buyer, a home inspection can provide leverage in negotiations. If the inspection report uncovers issues, you can request repairs or compensation from the seller. It’s also wise to consider the long-term resale value of homes with significant issues, as they may lose value over time.

Additionally, inspections can highlight necessary improvements that could enhance energy efficiency or safety, ensuring that your new home is not only functional but also comfortable for years to come.

Actionable Advice

- Always budget for a home inspection as part of your buying process.

- Hire a qualified home inspector with good reviews and necessary certifications.

- Attend the inspection to ask questions and gain insights about the property firsthand.

By placing a high value on home inspections, you’re making a proactive choice to safeguard your investment and enhance your home-buying journey.