What Can You Use Home Equity Loans For? Well, imagine tapping into the financial reservoir of your home to fund your dreams and tackle real-life expenses. Home equity loans allow you to borrow against the value of your property, and since the average homeowner has gained about $50,000 in equity over the past decade, it’s no wonder these loans are gaining popularity. You might consider using those funds for a significant home renovation—an upscale kitchen remodel can yield a return of nearly 75% on your investment. Or maybe you’re thinking of consolidating high-interest debt; using equity to pay off credit cards with average rates of 16% or more can save you a bundle in interest.

You could also be eyeing that long-awaited family vacation; with home equity loans offering average rates around 6%, you might find it cheaper in the long run than other borrowing options. Some homeowners leverage these loans for education expenses too—considering that college tuition can easily surpass $30,000 a year, borrowing against your equity might ease that financial strain. Even starting a business can be a viable venture; about 75% of small business owners have reported tapping into personal savings or home equity to launch their startups. The options are diverse, and with careful planning, they can lead to incredible opportunities.

Financing Home Renovations with Equity

When it comes to financing home renovations, leveraging your home’s equity can be a smart move. Home equity allows you to tap into your property’s value to fund upgrades, making it a popular choice for homeowners looking to enhance their living spaces. Let’s dive into some key points about how equity can help you transform your home.

Understanding Home Equity for Renovations

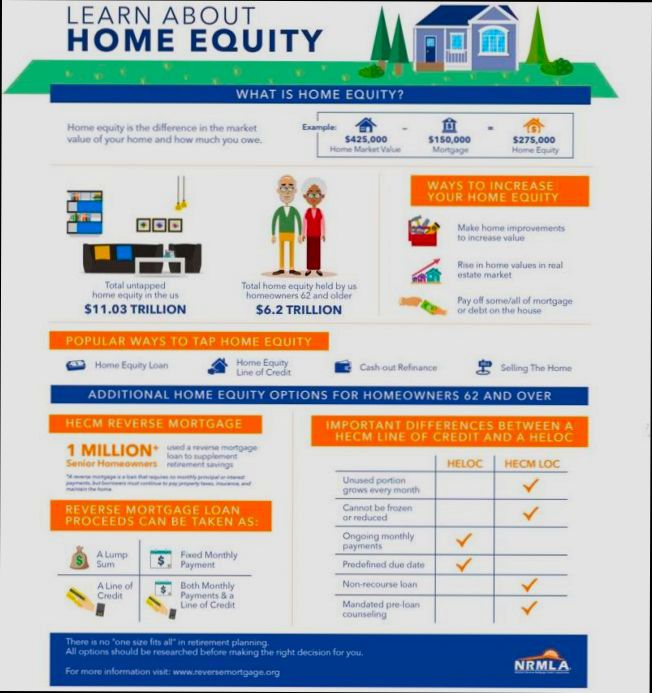

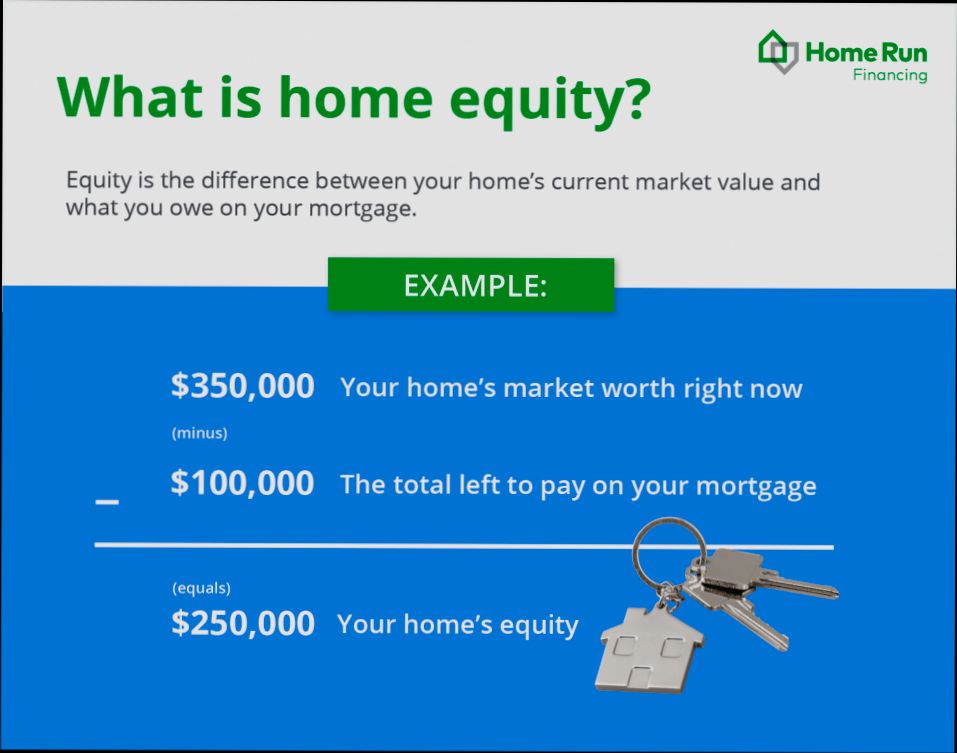

Home equity is the portion of your home that you truly own, calculated by subtracting your mortgage balance from your home’s current market value. If your home is worth $400,000 and you owe $250,000, your equity stands at $150,000. You can typically borrow against this equity, often at lower interest rates than other types of loans.

- Average Loan Amounts: Homeowners can usually access 75% to 90% of their equity. That means if you have $150,000 in equity, you might be able to secure a loan ranging from $112,500 to $135,000 for renovations.

- Renovation Return on Investment (ROI): According to a recent study, kitchen remodels can recoup about 75% of their cost, while bathroom remodels often return around 70%. This means the renovation can significantly increase the home value, justifying the equity loan.

Why Use Equity for Home Renovations?

Using a home equity loan or line of credit gives you several advantages:

- Lower Interest Rates: Typically, home equity loans feature rates around 3% to 5% lower than personal loans or credit cards.

- Tax Deductions: Interest on home equity loans may be tax-deductible if used for renovations that improve the property.

- Longer Repayment Terms: Many equity loans offer terms up to 30 years, making monthly payments more manageable.

Comparative Table of Renovation Costs vs. Equity Loan Potential

| Renovation Project | Average Cost | Potential Home Value Increase | Average Equity Loan Needed |

|---|---|---|---|

| Kitchen Remodel | $25,000 | $18,750 | $18,750 |

| Bathroom Remodel | $15,000 | $10,500 | $10,500 |

| Basement Finishing | $30,000 | $24,000 | $24,000 |

| Roof Replacement | $10,000 | $8,000 | $8,000 |

Real-World Examples

1. The Johnsons’ Kitchen Renovation: The Johnson family had $100,000 in home equity. By taking out a $75,000 home equity loan with a 4% interest rate, they remodeled their kitchen, which increased their home’s market value by $50,000. They now enjoy a beautiful kitchen while their investment grows over time.

2. Emily’s Bathroom Update: Emily had a home equity of $120,000. She utilized a $30,000 equity line of credit to renovate her bathroom. This update not only created a more enjoyable space but also increased her home’s value by approximately $25,000, allowing her financial strategy to pay off.

Practical Tips for Financing Renovations with Equity

- Calculate your available equity before applying for a loan to ensure it meets your renovation needs.

- Assess different lenders for the best interest rates and repayment options using your equity.

- Keep in mind the potential ROI of your renovations; prioritize projects that will add significant value to your home.

Exploring your home equity for financing renovations can be an excellent way to enhance your living space while making a financially sound decision. Be sure to analyze all loan options and choose renovations that will pay off long-term.

Debt Consolidation Benefits of Home Equity

Are you feeling overwhelmed by high-interest debts? Using your home equity for debt consolidation can offer a way to manage your financial obligations more efficiently. Let’s dive into how leveraging your home’s equity can help you reduce your overall debt burden.

Lower Interest Rates

One of the most appealing benefits of using home equity for debt consolidation is access to lower interest rates. Typically, home equity loans have interest rates that are considerably lower than those of credit cards and personal loans.

- Average Credit Card Rate: As of late 2023, the average credit card interest rate hovers around 20%.

- Average Home Equity Loan Rate: In contrast, the average home equity loan interest rate is around 7%.

This difference can translate to substantial savings over time when transferring high-interest debt into a lower-rate home equity loan.

Single Monthly Payment

Debt consolidation with home equity enables you to streamline your finances by consolidating multiple debts into a single monthly payment.

- Simplicity: Instead of juggling several due dates, you only manage one, making it easier to keep track of your payments.

- Improved Cash Flow: By lowering monthly interest payments, you can free up cash for other essential expenses or savings.

Debt-to-Income Ratio Improvement

Using home equity can also improve your debt-to-income (DTI) ratio, a key factor lenders consider when you apply for credit.

- Direct Impact: Lowering your DTI can enhance your eligibility for future loans or credit lines.

- Ideal DTI: A DTI of below 36% is generally considered healthy, and consolidating debts can help you reach this target.

Comparative Overview

| Type of Debt | Average Interest Rate | Monthly Payment for $10,000 Over 5 Years |

|---|---|---|

| Credit Cards | 20% | $250 |

| Personal Loans | 12% | $250 |

| Home Equity Loan | 7% | $198 |

This table shows the stark differences in interest rates and payments between various debt types. Transitioning to a home equity loan can save you money each month, decreasing the financial strain.

Real-World Examples

Consider Sarah, who had amassed $30,000 in credit card debt with an average interest rate of 20%. By using her home equity, she secured a loan at 7%.

- Before: She was paying approximately $600 a month in credit card payments.

- After: By consolidating through home equity, her monthly payment dropped to about $400.

Another example is Mike, who consolidated $15,000 in personal loans averaging 12% interest. After refinancing this with home equity at 7%, he not only reduced his monthly payment but also gained a clearer financial picture.

Actionable Insights

- Assess Your Equity: Determine how much equity you have by calculating the difference between your home’s market value and your mortgage balance.

- Shop Around: Compare rates from multiple lenders to find the best home equity loan terms for your needs.

- Create a Repayment Plan: Work out a solid plan to pay off the home equity loan to prevent falling into a similar debt situation in the future.

Always remember that while debt consolidation can provide immediate financial relief, it’s essential to address the underlying spending habits that led to high debt in the first place.

Using Home Equity Loans for Education

Using home equity loans for education can be an innovative way to finance your or your child’s pursuit of higher learning. This option allows you to tap into your home’s value to cover tuition, books, and other education-related expenses. The great part about leveraging your home equity is that it often comes with lower interest rates compared to traditional student loans.

Key Benefits of Using Home Equity for Education

- Access to Larger Amounts: Home equity loans typically allow you to borrow between 75% and 90% of your home equity, depending on your lender’s policies. This can provide substantial funds for education.

- Lower Interest Rates: Interest rates on home equity loans are generally lower than those on federal or private student loans. With 2023’s average home equity interest rates as low as 7% compared to 4.7% for federal student loans, this can save borrowers significant amounts over time.

- Tax Deductible: The interest on home equity loans may be tax-deductible if the funds are utilized for qualified educational expenses.

| Feature | Home Equity Loan | Federal Student Loan |

|---|---|---|

| Average Interest Rate | 7% | 4.7% |

| Maximum Loan Amount | Up to 90% of equity | Up to $57,500 (for 4 years) |

| Tax Deductibility | Yes (under certain conditions) | No |

| Repayment Period | 5-30 years | 10-25 years |

Real-World Examples

- Case Study 1: A couple in their 40s decided to use a home equity loan of $60,000 to fund their daughter’s college education. This was calculated based on 80% of their home equity. They benefited from a fixed interest rate of 6.5%, allowing them to pay off the loan over 15 years while their daughter graduated with minimal student loan debt.

- Case Study 2: A single parent leveraged a home equity loan to pay for community college for their child. By borrowing $25,000, they locked in a lower interest rate than available from federal student loans, saving thousands over the life of the loan. The taxpayer also enjoyed deductions, making the decision financially advantageous.

Practical Implications for Readers

When considering using a home equity loan for education, it’s crucial to assess your current financial situation. Here are some actionable tips:

- Review the equity in your home and get a professional appraisal to understand how much you can borrow.

- Compare rates from multiple lenders to ensure you get the best deal on interest rates.

- Consult a tax advisor to confirm the tax implications and potential deductions you may receive.

If you choose this route, make a detailed plan on how you will manage repayment alongside your mortgage, ensuring you don’t jeopardize your home.

Statistics on Home Equity Loan Usage

Understanding the landscape of home equity loans is crucial for anyone considering leveraging their home’s value for financial needs. This section highlights relevant statistics that illustrate how homeowners use these loans, providing a clearer picture for potential borrowers.

Key Usage Statistics

- Approximately 45% of homeowners have accessed funds through home equity loans or lines of credit in the past five years.

- A staggering 73% of respondents in a recent survey indicated that they prefer home equity loans over personal loans for large expenses, primarily due to the lower interest rates and manageable terms.

- In 2023, the average home equity loan amount was around $54,000, demonstrating a significant shift toward larger borrowing as housing prices rise.

- An analysis found that approximately 35% of home equity loans were utilized for significant home improvements, making it a popular choice among homeowners.

- Data also showed that 32% of borrowers used their home equity loans for life events, including weddings, medical expenses, and emergencies.

Comparative Table of Home Equity Loan Usage

| Usage Purpose | Percentage of Borrowers |

|---|---|

| Home Improvements | 35% |

| Debt Consolidation | 20% |

| Education Expenses | 15% |

| Life Events (Weddings, etc.) | 32% |

| Other Uses | 18% |

Real-World Examples

To understand the practical implications of these statistics, consider this scenario: a homeowner in need of significant structural repairs found themselves with equity that allowed them to take out a home equity loan of $65,000. They reported using the majority for renovation, which ultimately increased their home’s value by nearly 20%, demonstrating the potential for home equity to fund profitable investments.

Another example involves a couple utilizing their equity to finance their child’s college education. They accessed a home equity loan of $30,000, which provided a timely solution amidst rising tuition costs. This case underscores how home equity can provide much-needed funding during life’s pivotal moments.

Practical Implications

For homeowners, the statistics on home equity loan usage reveal several actionable insights:

- If you’re contemplating a home improvement project, reviewing the 35% usage for renovations can help you gauge how others are leveraging their equity effectively.

- Considering that 73% prefer home equity loans, you might want to explore this option over personal loans or credit cards for any large expenses, given the potentially lower interest rates.

- Be aware that tapping into your equity may limit your future borrowing capacity; thus, it’s essential to plan accordingly based on your long-term financial goals.

These insights emphasize the importance of understanding statistics around home equity loans, as they not only reflect current trends but also guide financial decisions you may face in the near future.

Real-Life Success Stories of Home Equity

Home equity holds the potential to transform your life in various ways, as illustrated by numerous real-life success stories. These examples demonstrate how individuals have effectively utilized their home equity to achieve significant milestones, from improving their living conditions to securing their financial futures.

Success Through Home Improvements

1. The Johnson Family’s Expansion

- The Johnsons, a family living in suburban Maryland, leveraged their home equity to finance a major home expansion. By accessing $100,000 in home equity, they added a new bedroom and a sunroom, which not only enhanced their living space but also increased their property value by approximately 15%.

2. Renovations for Rental Income

- Sarah, a homeowner in Austin, Texas, used her home equity to fund a stylish renovation of her basement into a rental unit. Investing $60,000 resulted in monthly rental income of $1,200, effectively covering her mortgage payments and providing her with a secondary income stream.

Educational Empowerment

1. Student Success Story

- The Rodriguez family from California decided to use their home equity as a means to finance their daughter’s college education. By borrowing $50,000, they were able to pay for her tuition upfront, saving her from potential student loan interest rates. Their daughter graduated debt-free, allowing her to launch her career without the burden of education debt.

Financial Security Enhancement

1. Planning for Retirement

- After realizing they could access some of their home’s value, the Smiths took a home equity loan of $75,000 to invest in a diversified portfolio that would secure their retirement. By choosing this option, they anticipated over 30% growth over ten years, enhancing their financial independence as they approached retirement age.

| Success Story | Amount of Equity Used | Reason for Loan | Outcome |

|---|---|---|---|

| Johnson Family Expansion | $100,000 | Home renovations | Increased property value by 15% |

| Sarah’s Basement Rental | $60,000 | Renovate basement for rental | Earns $1,200/month rental income |

| Rodriguez Family Education | $50,000 | Daughter’s college tuition | Graduated debt-free |

| Smith Family Retirement Planning | $75,000 | Investment for retirement | 30% expected growth in ten years |

Real-World Outcomes

Homeowners across the nation are turning equity into tangible benefits. For example, Mary from Florida transformed her kitchen with a $40,000 equity loan. This renovation not only expedited her home sale but also increased her asking price by 20%, maximizing her return on investment.

Similarly, the Andersons used $90,000 in home equity to consolidate home improvement and student loans, decreasing their interest rates from 15% to 5%. This made a significant difference in their monthly budget, freeing up funds for family vacations and savings.

Practical Takeaways

- Evaluate your home’s market value regularly; this gives you clarity on the equity available.

- Identify your financial goals—whether it’s improving your home, funding education, or investing for retirement—before tapping into your equity.

- Ensure that the projects you finance with home equity can bring a return on investment, whether it’s through increased home value, rental income, or saved interest payments.

These real-life successes demonstrate the power of home equity and inspire many homeowners to take informed steps towards their financial aspirations.

Home Equity Loans for Emergency Expenses

Home equity loans can be a lifeline when you face unexpected expenses like medical emergencies, car repairs, or urgent home repairs. Using your home’s equity wisely in these situations can help you avoid financial strain while providing instant access to cash when you need it most.

Understanding Emergency Expenses

Emergency expenses vary widely, but they often crop up when you least expect them. Here are some common scenarios where funding becomes necessary:

- Medical Bills: Sudden health issues can lead to significant medical costs, even with insurance.

- Car Repairs: A car breaking down can disrupt daily life and require immediate cash outlay.

- Home Repairs: Issues like roof leaks or plumbing failures must be addressed quickly to prevent further damage.

Key Insights and Statistics

Leveraging a home equity loan for emergencies can provide several advantages. Consider these important statistics:

- Quick Access to Funds: Home equity loans can often be approved and funded within a few weeks, allowing you to tackle urgent needs swiftly.

- Loan Amounts: You can typically borrow up to 85% of your home equity, providing substantial cash flow for emergencies.

- Average Interest Rates: As of late 2023, average interest rates may hover around 7%, which is often more favorable than credit card rates, which can exceed 20%.

Comparative Table of Emergency Expenses Financing Options

| Financing Option | Average Interest Rate | Typical Loan Amount | Approval Time |

|---|---|---|---|

| Home Equity Loan | 7% | Up to 85% of home equity | 1-4 weeks |

| Personal Loan | 10-15% | Varies | 1-7 days |

| Credit Card Cash Advance | 20%+ | Typically low | Instant |

Real-World Examples

1. Case Study: Medical Emergency

A homeowner was faced with an unexpected surgery requiring out-of-pocket costs exceeding $15,000. By utilizing a home equity loan, they secured funding at a lower interest rate compared to credit cards, allowing them to manage payments without draining their savings.

2. Case Study: Urgent Home Repair

After a severe storm, a homeowner’s roof sustained significant damage. With repair costs estimated at $10,000, they opted for a home equity loan, granting them the necessary funds quickly to avoid further damage and inconvenience.

Practical Implications for Homeowners

When considering a home equity loan for emergency expenses, keep the following points in mind:

- Evaluate Your Equity: Before applying, assess how much equity you have in your home to understand your borrowing capacity.

- Research Lenders: Interest rates can vary among lenders. Shop around to find the best rate that fits your situation.

- Plan for Repayment: Ensure you have a clear repayment plan, as failing to repay the loan can lead to the risk of losing your home.

Utilizing a home equity loan for emergencies can provide the financial relief you need quickly and effectively, allowing you to address critical bills without the burden of high-interest debt from other sources.

Investment Opportunities with Home Equity Financing

Home equity financing can open doors to various investment opportunities, allowing homeowners to leverage their existing property value. By tapping into home equity, homeowners can access funds for investments that may yield higher returns than traditional savings accounts or other low-risk options.

Understanding Home Equity for Investment

Home equity financing products, such as home equity lines of credit (HELOCs) and home equity contracts, provide the cash needed for investment purposes. With more than $35 trillion in total home equity in the U.S., this represents a potentially untapped resource for investors looking to grow their wealth.

- Home equity contract companies issued about $1.1 billion backed by 11,000 home equity contracts in just the first ten months of 2024.

- In comparison, 1.2 million HELOCs were originated between 2023 and 2024 Q2, which illustrates the increasing popularity of these financing tools among homeowners.

Investment Potential

Investing via home equity can be particularly attractive for homeowners seeking to diversify their portfolios or invest in significantly larger markets. Here are some of the key benefits:

- Real Estate Investing: Many individuals use home equity loans to invest in rental properties, allowing them to generate passive income. Consumer reports indicate that some homeowners used these funds specifically for building up investment portfolios.

- Stock Market Diversification: Home equity can provide funds for investing in stocks or mutual funds. Utilizing a portion of your home equity for investment can yield higher returns, especially if used wisely.

- Retirement Savings: Some homeowners aim to bolster their retirement funds using home equity financing, enabling them to invest in opportunities that can generate income during retirement.

Comparative Analysis of Financing Options

| Financing Option | Initial Cash Received | Monthly Payments | Settlement Amount after 10 Years |

|---|---|---|---|

| Home Equity Contract | $50,000 | $0 (no monthly payments) | $94,074 to $215,892 |

| HELOC | $50,000 | $375 | $50,000 |

This table illustrates that while home equity contracts require no monthly payments, they can result in a substantially higher settlement amount than a HELOC after 10 years. This can be important in assessing the long-term implications of using home equity for investment.

Real-World Examples

1. Rental Property Investment: A consumer used a home equity loan to purchase a rental property, effectively utilizing $50,000 from her home equity. This investment not only covered the down payment but also provided potential monthly rental income, thus expanding her financial portfolio.

2. Stock Market Investment: Another homeowner tapped into her home equity to invest in diversified stocks. With the recent appreciation in her home’s value, she transformed the home equity into substantial stock market gains that surpassed traditional savings returns.

Practical Implications for Homeowners

When considering home equity for investment opportunities, you should keep in mind:

- Market Awareness: Stay informed about the local real estate market and stock trends to make educated choices when investing home equity.

- Financial Goals: Clearly define your investment goals and risk tolerance. Investing through home equity should align with your long-term financial strategy.

- Understanding Terms: Familiarize yourself with the specific terms of your home equity financing option. Variances between contracts can lead to unexpectedly large repayment amounts.

Utilizing home equity financing for investment can be a powerful tool in wealth generation. Being strategic about its use can lead to significantly greater financial freedom and future stability.