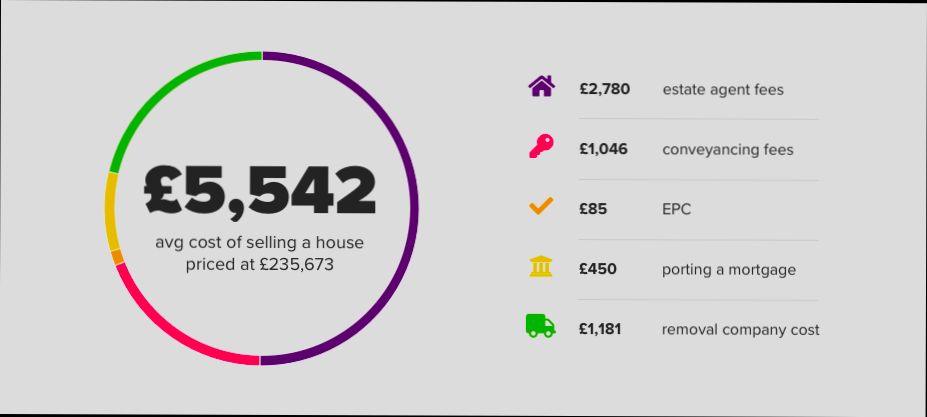

What are the taxes and costs of selling a house in the United States? Selling a house isn’t just about finding a buyer and handing over the keys; it also involves navigating a maze of financial obligations. For starters, you might be looking at capital gains taxes if your home appreciates significantly. In 2021, the National Association of Realtors reported that the median home price jumped to about $347,500, meaning sellers could face hefty tax bills if they sell for a nice profit—especially if the home was bought years ago for a much lower price.

On top of that, there are a bunch of other costs that can sneak up on you. You’re likely to incur expenses like agent commissions, which typically range from 5% to 6% of the selling price, and closing costs that can land between 2% to 5%. If you’re repairing or staging your home, those expenses can add up quickly too—think anywhere from a couple of hundred to several thousand dollars, depending on what you decide to tackle. So, before you dive into the selling process, brace yourself for the financial realities so you aren’t caught off guard when the dust settles.

Understanding Capital Gains Tax Implications

When selling a house, understanding capital gains tax can feel overwhelming, but it’s crucial for your financial well-being. Capital gains tax applies to the profit you make from selling your property, and knowing the implications can help you strategize effectively.

Key Points to Consider

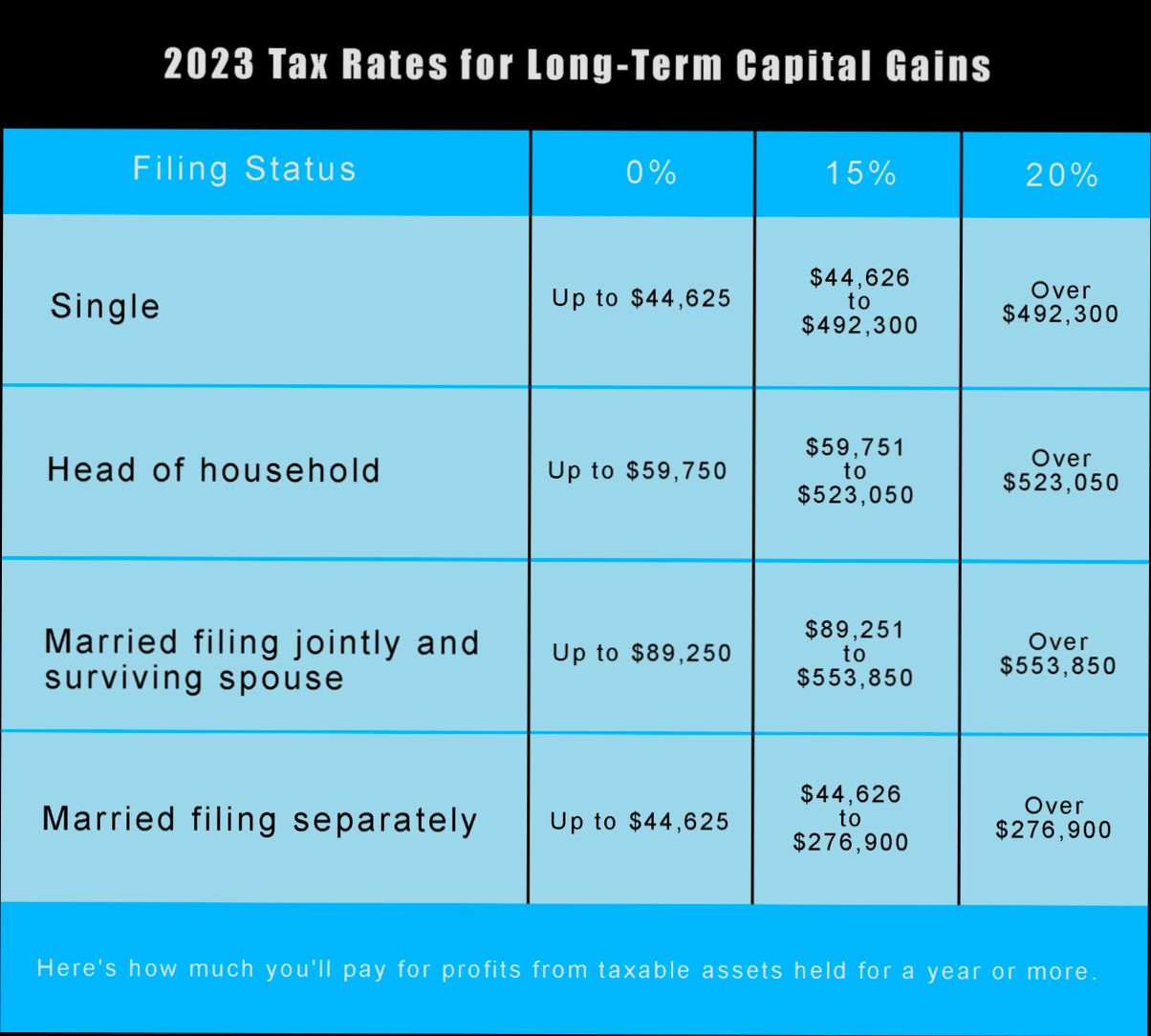

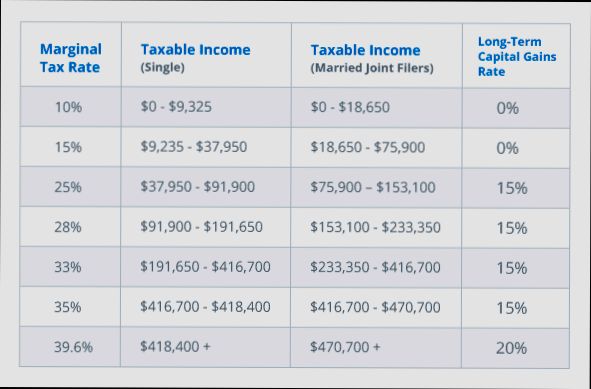

- The current federal capital gains tax rate varies between 0%, 15%, and 20%, depending on your income level. For example, individuals with a taxable income up to $44,625 may be taxed at 0%, while those earning over $492,300 fall into the 20% bracket.

- Homeowners can exclude up to $250,000 of capital gains from taxation if they have owned and lived in the property for at least two of the last five years. For married couples filing jointly, the exclusion can be as much as $500,000.

- It’s important to note that the IRS considers anything beyond the threshold as a capital gain, which means if you sold your home for significantly more than you purchased it, you may owe taxes on that difference.

| Income Level | Capital Gains Tax Rate | Exclusion Threshold |

|---|---|---|

| Up to $44,625 | 0% | $250,000 (single) |

| $44,626 - $492,300 | 15% | $500,000 (married) |

| Over $492,300 | 20% | N/A |

Real-World Examples

- If you bought your home for $200,000 and sold it for $500,000, you’d have a profit (or capital gain) of $300,000. If you’ve lived in the house for at least two out of the last five years, you could exclude $250,000 from your taxable income, only paying capital gains tax on the remaining $50,000.

- For a couple who successfully sells their home for a $600,000 profit after owning it for three years, they could exclude up to $500,000 of that gain, leaving them with a taxable gain of only $100,000, significantly lowering their tax liability.

Practical Implications

Understanding these implications can help you make informed decisions when selling your home. Here are some actionable insights:

- Consider timing your sale to maximize your exclusion; if you can, aim to sell after living in the home for two years.

- Keep records of home improvements, as these can increase your adjusted basis, effectively reducing your taxable capital gains.

- Consult with a tax professional to ensure you understand how your specific financial situation interacts with capital gains tax.

- If you anticipate your capital gains exceeding the threshold, strategize selling your home in a tax year when your income is lower to potentially reduce your capital gains tax.

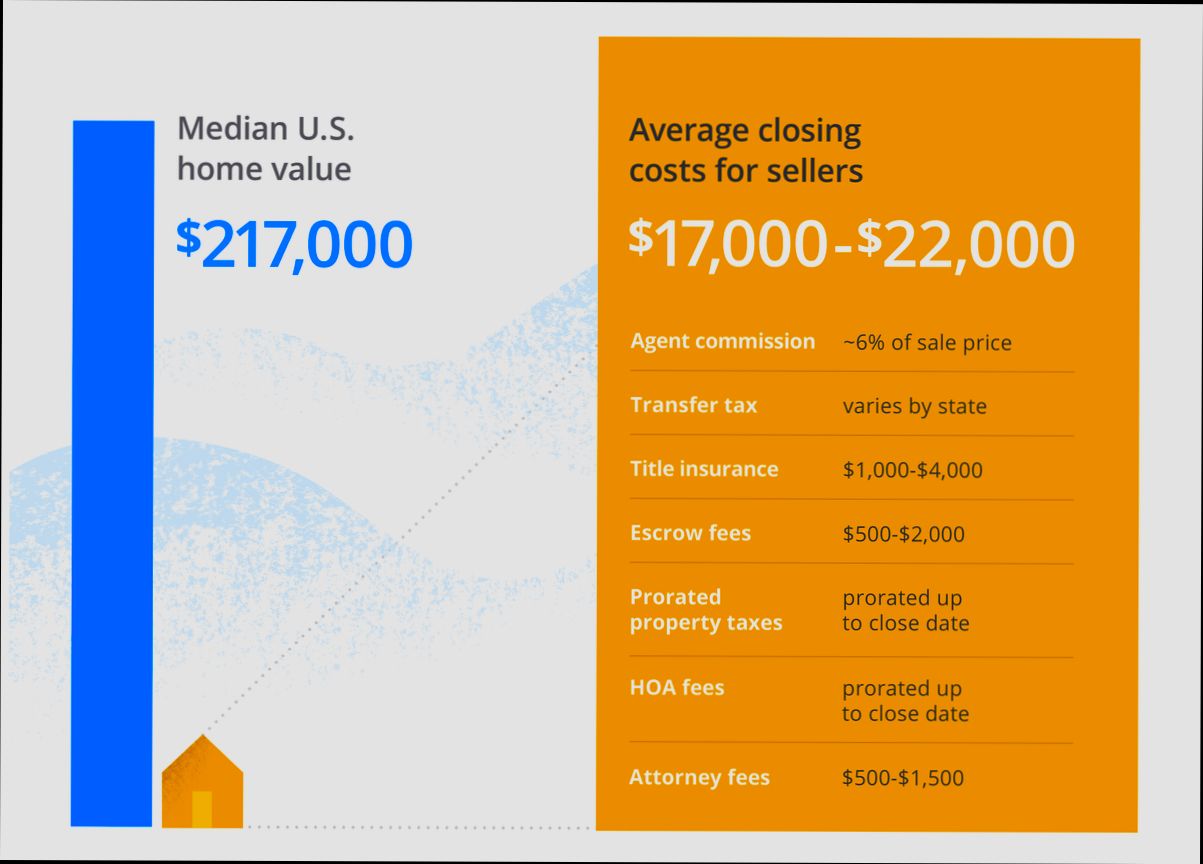

Exploring Closing Costs and Fees

When you’re preparing to sell your house, it’s essential to understand the closing costs and fees that come into play. These costs can significantly impact your overall profit from the sale, and being informed allows you to budget effectively.

Key Points to Consider

Closing costs typically range from 2% to 5% of the sale price, which can add up significantly. Here’s a closer look at some common fees you’ll encounter:

- Real Estate Agent Commissions: Generally, this is among the largest fees, often around 5% to 6% of the home’s selling price, split between the buyer’s and seller’s agents.

- Title Insurance: This protects against claims on your property after the sale and can cost between $1,000 and $1,500, depending on your location and the sale price.

- Transfer Taxes: Many states and localities impose a transfer tax, which can vary widely. For example, in New York City, it’s approximately 1.425% of the sale price.

- Escrow Fees: This fee varies but typically costs around 1% of the home’s sale price and covers the services of an escrow company handling the transaction.

Closing Costs Breakdown

| Type of Cost | Percentage/Amount | Description |

|---|---|---|

| Real Estate Agent Commission | 5% - 6% of sale price | Fees paid to agents involved in the sale |

| Title Insurance | $1,000 - $1,500 | Insurance against claims on the title |

| Transfer Taxes | Varies by location | Taxes charged by the state/local jurisdiction |

| Escrow Fees | Approximately 1% | Fee for the escrow service handling the sale |

Real-World Example

Imagine you’re selling a home for $300,000. If we estimate:

- Real Estate Agent Commission: 6% = $18,000

- Title Insurance: $1,200 (average)

- Transfer Tax: 1.5% of $300,000 = $4,500

- Escrow Fees: 1% of $300,000 = $3,000

Your total closing costs in this scenario would be approximately $26,700, which significantly reduces your profits.

Practical Implications for Sellers

Understanding these fees allows you to negotiate better or make informed decisions on accepting offers. For instance, knowing the typical costs can empower you to ask buyers to cover certain fees or adjust your listing price appropriately.

- Budgeting for Closing Costs: As you arrange your sale, include an estimate of these costs in your financial planning.

- Preparation and Negotiation: Don’t hesitate to discuss these costs with your real estate agent to evaluate which fees can be mitigated or negotiated.

Actionable Advice

Before listing your home, gather as much information as possible about closing costs in your area. Research can reveal particular fees that might apply, allowing you to prepare adequately. Always consult local regulations and seek clarification from your agent to ensure you’re fully aware of any hidden fees that may arise during the closing process.

Analyzing State-Specific Tax Regulations

Understanding the intricacies of state-specific tax regulations is essential when selling your home. Each state has varying rules and rates that can significantly impact your overall profit from the sale. Let’s break down how these regulations play a crucial role in your selling process.

Key Points to Consider

- State Income Taxes: Some states, like California and New York, implement additional state income taxes on capital gains. You might encounter rates up to 13.3% in California depending on your taxable income.

- Transfer Taxes: Many states and even local jurisdictions impose transfer taxes upon selling a property. For example, in New York City, sellers face a transfer tax of 1% for sales under $500,000 and 1.425% for sales over $500,000.

- Exemptions and Credits: Certain states offer exemptions that can reduce your tax burden. In Oregon, sellers may qualify for a primary residence exemption that could eliminate some state-level capital gains taxes.

Comparative Table of State-Specific Tax Regulations

| State | Capital Gains Tax Rate | Transfer Tax Rate | Primary Residence Exemption |

|---|---|---|---|

| California | Up to 13.3% | 0.11% - 0.25% | No |

| New York | Up to 10.9% | 1% - 1.425% | Yes (with conditions) |

| Texas | 0% (no state income tax) | Varies by county (up to 1%) | No |

| Oregon | Up to 9% | 1.2% | Yes |

| Florida | 0% | No transfer tax | No |

Real-World Examples

In California, if you sold a home for $700,000 and made a $300,000 profit, you could face a capital gains tax up to $39,900, factoring in the high state tax rate. If you were in New York City, you would also owe approximately $10,975 in transfer taxes, adding to your selling costs.

Conversely, in Texas, where there’s no state income tax, selling the same home would only incur closing costs without additional capital gains taxes, maximizing your overall profit.

Practical Implications

As you navigate the selling process, it’s critical to familiarize yourself with your specific state’s regulations. Use the following tips:

- Research Local Rules: Each state has different tax laws, so take the time to understand the regulations applicable to your situation.

- Consult a Tax Professional: Enlisting the help of a tax advisor can provide tailored insights specific to your financial landscape.

- Plan for Taxes Upfront: Incorporate anticipated state taxes into your overall selling strategy to avoid surprises later.

Knowing these regulations can save you money and help you make informed decisions while selling your home.

Real-World Examples of Selling Expenses

When you’re selling a house, it’s essential to grasp the various selling expenses that may arise throughout the process. These expenses can substantially affect your net proceeds, so knowing what they entail can help you prepare better financially.

Key Selling Expenses to Consider

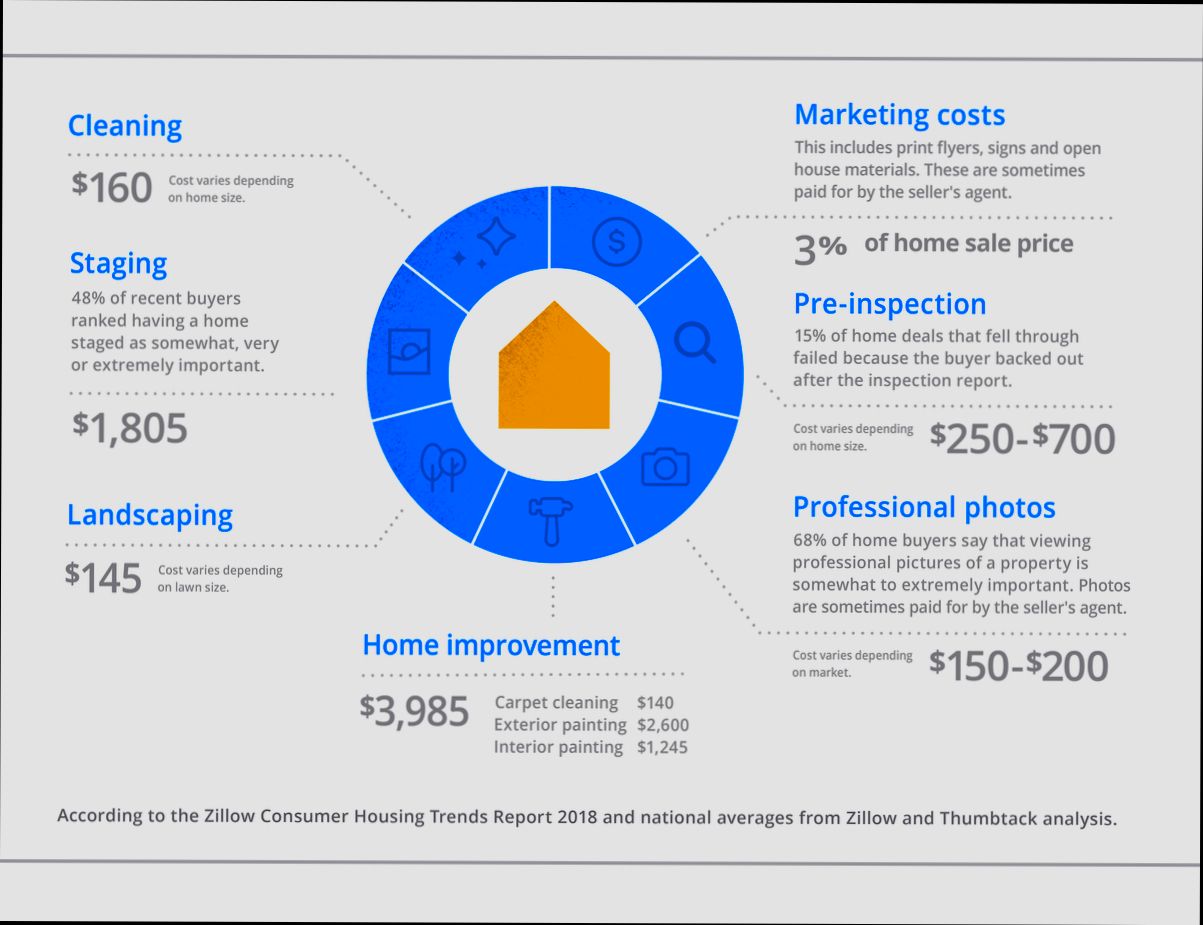

1. Sales Commissions: Agents typically earn between 5% to 6% of the home’s sale price as commission. For example, on a $300,000 home, that could amount to $15,000 to $18,000.

2. Marketing Costs: Engaging in marketing and advertising can vary based on the strategies employed. Costs for brochures, online ads, or open house events could easily reach $1,000 to $5,000.

3. Home Repairs and Staging: Before listing, many sellers invest in minor repairs or staging to enhance appeal. This could range from $2,000 to $10,000 depending on the extent of work done.

4. Closing Costs: Selling your home incurs closing costs, typically between 2% to 5% of the sale price. If you sell for $300,000, expect to budget $6,000 to $15,000 just for closing costs.

5. Miscellaneous Fees: There can also be several smaller fees, such as inspection costs, appraisal fees, and title insurance, that can add up to hundreds or even thousands of dollars.

Comparative Table of Common Selling Expenses

| Selling Expense | Estimated Cost Range |

|---|---|

| Sales Commissions | 5% - 6% of sale price |

| Marketing and Advertising | $1,000 - $5,000 |

| Home Repairs and Staging | $2,000 - $10,000 |

| Closing Costs | 2% - 5% of sale price |

| Miscellaneous Fees | $500 - $3,000 |

Real-World Examples of Selling Expenses

Consider the case of a couple selling their home for $400,000. They decide to hire a real estate agent, costing them $24,000 in commissions. To make their home more marketable, they invest $3,000 in staging and repairs. Additionally, they budget about $8,000 for closing costs.

- Total Selling Costs for the Couple:

- Real Estate Commissions: $24,000

- Repairs and Staging: $3,000

- Closing Costs: $8,000

- Total: $35,000

This significant cost highlights how expenses can eat into the profit from selling a house.

Practical Implications for Readers

When planning to sell your home, consider these selling expenses as part of your financial equation. Make sure to factor in all potential costs to avoid surprises down the line. Connecting with a knowledgeable real estate agent can also help clarify what you might expect based on your particular listing and market conditions.

Specific Facts About Selling Expenses

- Be prepared to discuss your seller agent’s commission upfront to avoid confusion during closing.

- Keep track of all your expenses associated with selling; some may be tax-deductible.

- Explore various marketing avenues to weigh costs against the potential selling price, ensuring you get the best value for your investments.

Statistics on Average Selling Costs

When preparing to sell your home, understanding the average selling costs can be a huge help. It allows you to plan ahead and manage your finances effectively. In this section, I’ll break down key statistics that reflect the cost landscape sellers might encounter throughout their selling journey.

Key Statistics on Selling Costs

1. Agent Commissions: The average real estate agent commission remains a significant cost, typically falling between 5% to 6% of the sale price. This means if you sell your home for $300,000, you could pay anywhere from $15,000 to $18,000 just in commission fees.

2. Home Preparation Costs: Sellers often invest in home improvements to boost appeal. On average, these renovation costs can range from $5,000 to $15,000, depending on the condition of the property and the local real estate market conditions.

3. Closing Costs: Beyond the agent commissions, closing costs can add another 2% to 5% to the total selling price, which amounts to a considerable percentage depending on the home value.

4. Transfer Taxes: Many states impose a property transfer tax during the sale, averaging around 0.1% to 2% of the sale price. For a $300,000 home, this could mean an additional cost of $300 to $6,000.

Overview of Average Selling Costs

| Cost Type | Average Percentage of Sale Price | Estimated Dollar Amount (based on $300,000 sale) |

|---|---|---|

| Realtor Commission | 5% to 6% | $15,000 - $18,000 |

| Home Preparation Costs | Varies | $5,000 - $15,000 |

| Closing Costs | 2% to 5% | $6,000 - $15,000 |

| Transfer Taxes | 0.1% to 2% | $300 - $6,000 |

Real-World Examples of Selling Costs

Consider a homeowner aiming to sell a house valued at $300,000. Here’s how the costs might break down:

- Commission Fees: If the commission is set at 6%, that amounts to $18,000.

- Home Improvements: The seller chose to invest $10,000 in upgrades to make the property more attractive.

- Closing Costs: The estimated closing costs fell at approximately 3%, which totals $9,000.

- Transfer Tax: A transfer tax of 1% applied here would be $3,000.

Putting these examples together, the total average selling cost could reach nearly $40,000, illustrating how significant these expenses can be.

Practical Implications for Sellers

Understanding these statistics empowers you to make informed decisions about your selling strategy. It’s wise to:

- Calculate your expected selling costs early in the process to avoid surprises.

- Consider necessary home improvements that might increase your home’s value, but be sure to weigh the cost against potential returns.

- Compare different agents and their commission rates to find the best fit for your financial goals.

By keeping these statistics in mind, you can better prepare for the financial responsibilities tied to selling your home, ensuring a smoother and more successful sales process.

Benefits of Strategic Pricing Decisions

When you’re selling your house, making strategic pricing decisions can significantly influence your overall financial outcome. A well-thought-out pricing strategy not only attracts potential buyers but can also pave the way for enhanced profitability and reduced selling time.

Key Points on Strategic Pricing Benefits

1. Maximized Profit Potential: By strategically evaluating your listing price, you can align it with market trends, increasing the chance of receiving competitive offers. Homes priced correctly often sell for an average of 5% to 10% more than homes overpriced.

2. Faster Sales: According to recent data, homes priced competitively sell 30% faster than those priced above market value. This rapid turnover can minimize carrying costs, saving you unnecessary expenses like property taxes or maintenance fees.

3. Reduced Negotiation Pressure: Setting a fair price can lower the negotiating friction you might encounter. Studies suggest that homes that start at the right price have a better chance of closing without lengthy negotiations, thereby reducing transactional stress and expenses associated with protracted sales.

4. Enhanced Market Visibility: The right price can increase your listing’s visibility on platforms where buyers search for homes. Properties attract more views and inquiries when listed at competitive prices. Listings priced within 5% of an expected market value generally generate up to 40% more interest.

Comparative Table of Pricing Strategies

| Pricing Strategy | Average Time on Market | Estimated Sale Price Difference | Buyer Interest Increase |

|---|---|---|---|

| Overpriced Listing | 90+ days | -5% to -10% | 20% |

| Correctly Priced Listing | 30-60 days | +5% to +10% | 40% |

| Underpriced Listing | 15-30 days | -5% to -10% average | 60% |

Real-World Examples

- Case Study: Competitively Priced Home: In a bustling suburban neighborhood, a homeowner priced their 3-bedroom house at $350,000 after thorough market analysis. The property received three offers within the first week, leading to a final sale price of $365,000—an impressive 4% gain over the asking price, thanks to strategic pricing.

- Case Study: Overpriced Listing Outcome: Conversely, another homeowner listed their similar property at $380,000 in the same market. Despite its prime location, they faced months without offers and finally sold at $360,000, incurring not only a loss but also increased mortgage payments during the extended selling period.

Practical Implications for Readers

When setting your home price, consider:

- Analyzing recent sales of similar homes in your area.

- Consulting with a real estate professional to determine an optimal price strategy.

- Monitoring market trends to adjust your listing as necessary.

Utilizing these strategies can position you for financial success and an efficient sale process. Remember, the benefits of thoughtful pricing can lead to quicker offers and potentially higher final sale prices. Embrace this crucial aspect of home selling for the best results.

Impact of Home Improvements on Taxes

When you’re considering selling your house, you might be thinking about how home improvements could affect your tax situation. Based on your renovations, certain upgrades can influence your tax obligations when you sell the property. Let’s dive into how these improvements can impact your taxes in a tangible way.

Key Points to Consider

- Increase in Basis: One of the most significant outcomes of home improvements is the increase in your “cost basis.” This is the amount you initially paid for the home plus any substantial upgrades. For example, if you spent $30,000 on a kitchen remodel, this amount gets added to your original purchase price.

- Enhanced Exclusion Amount: If you are married and file jointly, you can exclude up to $500,000 of capital gains when selling your primary residence. By improving your home, you’re potentially lowering your taxable gain, thus keeping more money in your pocket.

- Types of Improvements: Not all improvements qualify as tax-deductible or applicable to your basis increase. Typically, the IRS distinguishes between repairs and improvements. While repairs merely maintain your home’s condition (like fixing a leaky roof), improvements that add value—such as adding a deck or finishing a basement—can be added to your cost basis.

Impact on Tax Basis and Potential Gains

| Type of Improvement | Tax Impact | Example |

|---|---|---|

| Major Renovation | Increases cost basis | Kitchen remodel ($30,000) |

| Essential Repairs | No impact on basis | Roof repair ($5,000) |

| Landscaping Enhancements | May increase market value, not basis | New front yard garden ($10,000) |

| Energy-Efficient Upgrades | Eligible for tax credits, not basis | Solar panel installation ($15,000) |

Real-World Examples

Imagine you bought your home for $300,000. Over the years, you invested in several improvements:

1. Finished Basement: This cost you $40,000 and increases your basis to $340,000.

2. New Roof: This $10,000 repair does not impact your basis but ensures the home remains in good condition.

3. Energy-Efficient Windows: If you spent $20,000, you might also benefit from state or federal tax credits.

Now, if you sell your house for $425,000, your taxable gain would be calculated as follows:

- Sale Price: $425,000

- Adjusted Basis: $340,000

- Taxable Gain: $425,000 - $340,000 = $85,000

If you didn’t make those improvements, your basis would remain at $300,000, resulting in a higher taxable gain of $125,000.

Practical Implications for You

Understanding the tax implications of your home improvements can dramatically affect the net profit from your home sale. To maximize your tax benefits:

- Keep Records: Always document your home improvements and retain receipts. This documentation is critical for proving increases to your basis.

- Consult a Tax Professional: Engaging with a tax advisor can provide clarity about what qualifies as an improvement and how it affects your taxes.

- Plan Strategic Upgrades: Consider improvements that not only enhance your living experience but also add significant value and can help reduce your tax burden upon selling.

In summary, by carefully selecting and recording home improvements, you can benefit from significant tax advantages that may not only ease the selling process but also improve your overall financial outcomes.