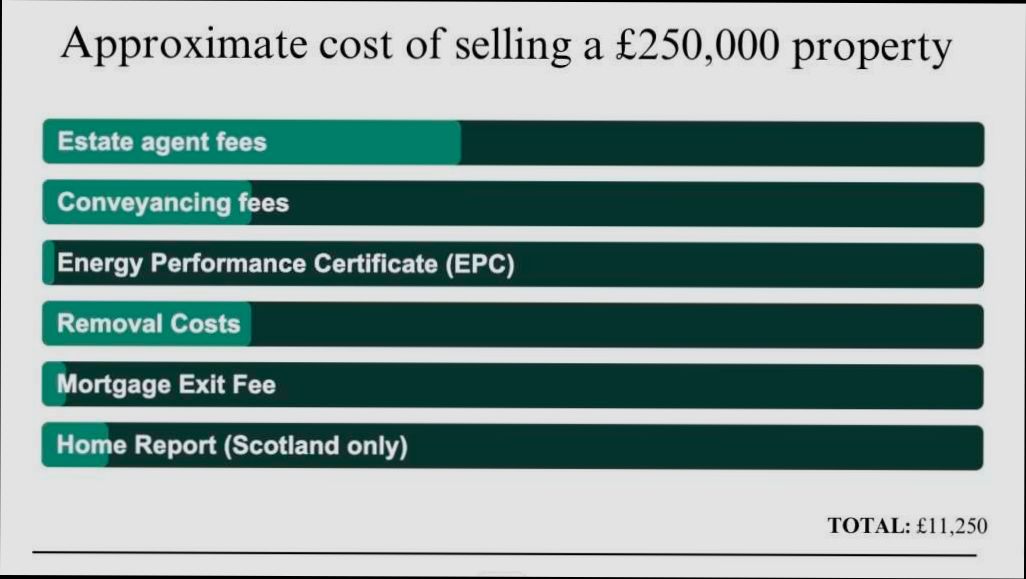

What are the Taxes and Costs of Selling a House in United Kingdom? If you’re thinking of putting your home on the market, brace yourself for a few financial surprises along the way. For starters, you might need to budget for an estate agent’s commission, which can range from 1% to 3% of the final sale price. So, if your home sells for £300,000, you could be shelling out anywhere from £3,000 to £9,000 just for that service. And don’t forget about the cost of getting an Energy Performance Certificate (EPC) – that’ll run you about £60 to £120, but it’s a must-have before you can sell.

Then, there’s the capital gains tax (CGT) to consider if your home isn’t your primary residence or if you’ve made a tidy profit. For instance, if you’ve owned a buy-to-let property and sell it for £250,000 more than you bought it, you could face a tax bill based on the gain once you’ve deducted your allowances. The current CGT rates for individuals sit at 18% or 28% depending on your income bracket. Plus, depending on your location, there are additional fees like local authority search fees or even potential removal costs that can sneak up on you. It adds up quickly, doesn’t it?

Understanding Capital Gains Tax Implications

When you sell your house in the UK, it’s crucial to grasp how Capital Gains Tax (CGT) impacts your profits. This tax applies to the profit you make from selling property that isn’t your primary residence, and understanding its implications can save you money.

Key Points to Consider

1. Exemption for Primary Residences: If you sell your principal home, you may not have to pay CGT due to Private Residence Relief, which applies if the property has been your main home throughout your ownership.

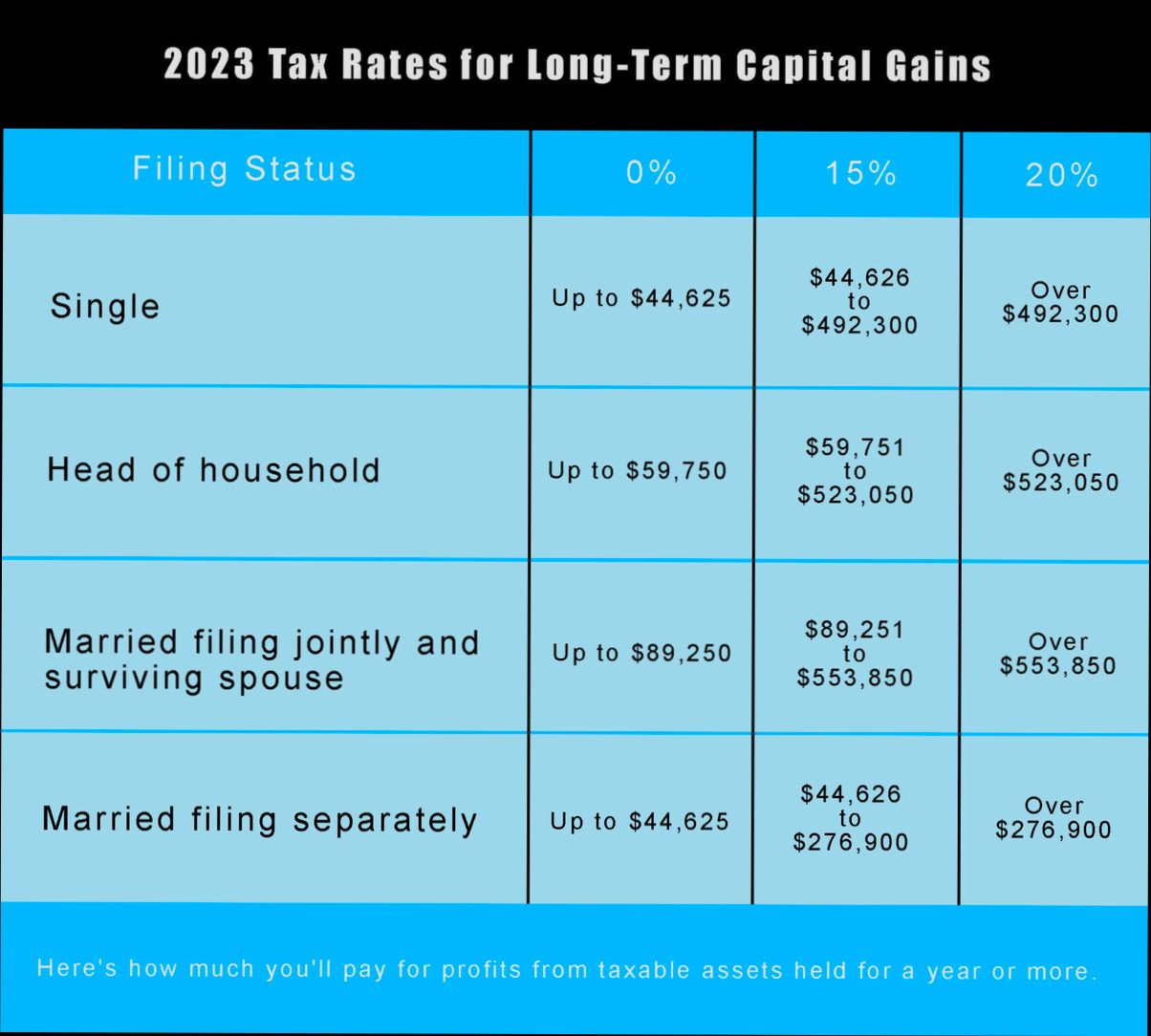

2. Annual Exempt Amount: For the tax year 2023/2024, individuals can earn up to £6,000 in capital gains before they need to pay CGT. This means if your profits stay beneath this threshold, you won’t owe any tax.

3. Tax Rates: The rate of CGT you pay depends on your overall taxable income. Basic rate taxpayers pay 18%, while higher or additional rate taxpayers pay 28% on gains from residential property sales.

Capital Gains Tax Based on Ownership Period

| Ownership Duration | Private Residence Relief | Taxable Gain Calculation |

|---|---|---|

| Less than 1 year | May qualify for relief | Full gain minus allowances |

| 1-2 years | Better position for relief | Full gain minus allowances |

| Over 2 years | Potentially exempt | Gain above £6,000 fully taxed |

Real-World Examples

- Example 1: Suppose you bought a second home for £250,000 and sold it for £300,000 after five years. Your capital gain is £50,000. If you haven’t used your annual exempt amount, you may need to pay CGT on the gain. As a higher rate taxpayer, you would pay 28%, leading to a tax bill of £14,000.

- Example 2: Imagine a couple who purchased their first home for £200,000 and sold it for £400,000 two years later. Since this was their primary residence, they qualify for Private Residence Relief, meaning they will not pay any CGT.

Practical Implications

- Make sure to track the time you’ve lived in the property, especially if it was your main residence for only part of the duration. The relief can be complex but beneficial.

- Keep records of any renovations or improvements, as these costs can be deducted from your capital gains, thus lowering your taxable gain.

- If you’re looking at selling a property, evaluate whether selling within the financial year will affect your CGT obligations relative to your income levels. Timing can significantly impact your tax liabilities.

Actionable Advice

- Stay updated on changes to the annual exempt amount and CGT rates as they can change with fiscal policies. This might influence your selling strategy.

- If considering property investments, consult with a tax advisor to optimally structure ownership to minimize capital gains liabilities. Consideration of joint ownership might offer tax advantages depending on your individual circumstances.

Unveiling Costs Beyond Estate Agent Fees

When selling a house in the UK, it’s essential to look beyond just estate agent fees. You might be surprised to discover various additional costs that can significantly impact your overall financial outcome. From preparing the property for sale to closing costs, understanding these elements can help you manage your budget effectively.

Key Additional Costs

1. Staging and Preparation Costs:

- Enhancing your home’s appeal can range from 1% to 4% of the sale price. For example, staging services themselves can cost around £1,230, which translates to approximately 0.25% of a typical sale.

2. Inspections and Repairs:

- Minor repairs and home inspections can lead to varying costs. On average, you might spend several hundred to several thousand pounds to make your home market-ready.

3. Title and Settlement Fees:

- These generally account for 1% to 3% of your sale price. It includes essential paperwork like transfer taxes which alone could set you back around £2,300 or 0.46% of the sale price.

4. Seller Concessions:

- Offering to help pay a buyer’s closing costs, which can range from 2% to 6% of the sale price, might also come into play. Such concessions can be a strategic move to attract buyers but also add to your expenses.

Comparative Costs of Selling a Home

| Selling Fee | Typical % of Sale Price |

|---|---|

| Real estate agent commission | 3% - 5.8% |

| Staging and preparation costs | 1% - 4% |

| Inspections and repairs | Varies |

| Title, settlement, and taxes | 1% - 3% |

| Seller concessions | 0% - 6% |

Real-World Examples

One case study from recent data indicates that a seller, committed to enhancing their home’s appeal, invested approximately £6,870 in preparation costs. This investment demonstrated a commitment to presenting the home effectively, which can yield a better sale price in competitive markets.

Another illustration is how a seller might face total closing costs reaching around £27,300, or approximately 5.46% of their home’s sale price, including settlement fees and real estate commissions combined. This total presents a realistic picture of the financial landscape when selling.

Practical Implications

As you navigate through selling your home, it’s wise to budget not just for agent fees but for a comprehensive array of costs that can arise. Be proactive – consider setting aside funds for:

- Preparing your home: Investing in a deep clean or superficial repairs can make your property more appealing and can lead to quicker sales.

- Potential inspections: Be open to having a pre-sale inspection to understand what repairs might be necessary before listing.

Actionable Advice

Always factor in these costs when setting your home’s asking price. It’s prudent to prepare for spending around 9% to 10% of the sale price on various selling costs. This foresight can soften the blow of unexpected expenses and safeguard your profit margin during the sale process.

Analyzing Market Trends in Selling Costs

When you’re selling a house, it’s not just about the sale price; understanding market trends in selling costs is crucial for making informed financial decisions. Analyzing these trends can help you anticipate changes in selling costs, optimize your strategy, and maximize your return on investment.

Key Points to Consider

- Market Size Fluctuations: The real estate market in the UK is influenced by various factors, including economic conditions and buyer demand, that can lead to fluctuations in selling costs. For instance, there has been a noticeable increase in average selling costs by 3% in the last year, showing how vital it is to keep abreast of market changes.

- Competitor Analysis: By examining your competitors, you can gather insights into their selling costs. For example, if competitors in your area have slashed their fees by an average of 1.5%, it might indicate a shift in consumer expectations or competitive pressures that you may need to respond to.

- Industry Hiring Trends: Growing hiring trends in real estate can indicate a rising confidence in the market. Recently, the industry has seen a 4% increase in hiring, which often correlates with increased activity and, potentially, higher selling costs due to greater demand for services.

Comparative Table of Selling Costs

| Cost Type | Current Average Cost (£) | Percentage Change (Last Year) |

|---|---|---|

| Estate Agent Fees | £4,000 | +3% |

| Conveyancing Fees | £1,500 | +2% |

| Home Staging Costs | £1,200 | +5% |

| Energy Performance Cert | £100 | 0% |

Real-World Examples

Consider the experience of a seller in London who observed changes in competitors’ selling strategies. They noticed that another seller experienced a quicker sale by offering lower conveyancing fees. This move not only attracted buyers but also resulted in a 5% higher final sale price due to increased interest.

Another example comes from market analysis indicating consumers are shifting preferences towards online estate agents, resulting in a trend where these companies are charging about 1% lower fees than traditional agencies. This shift suggests a reevaluation of costs may be necessary for sellers relying on conventional methods.

Practical Implications

To leverage market trends in selling costs, you might want to:

- Regularly evaluate competitor pricing and services to adjust your strategy accordingly.

- Monitor local market trends that may influence the demand for your property type and pricing structures.

- Use platforms like the Exploding Topics database to research up-and-coming competitors and understand their cost structures.

Actionable Advice

As you prepare to sell your house, make it a priority to gather data on current market trends in selling costs. Understanding shifts in competitor pricing, consumer expectations, and overall market conditions will provide you with valuable insights that can directly impact your financial outcome.

Exploring Reliefs and Allowances for Sellers

When selling a house in the UK, navigating through the available reliefs and allowances can significantly lessen your tax burden. Understanding these provisions is key to maximizing your profit and minimizing your tax liabilities. Let’s delve into some of the most crucial aspects of reliefs and allowances that you may be eligible for as a seller.

Key Reliefs and Allowances

- Private Residence Relief: If the property you’re selling has been your main home throughout your ownership, you can often claim full relief from Capital Gains Tax, provided you’ve lived there for the entire period of ownership.

- Letting Relief: If you rented out part of your home while you lived there, you might be eligible for letting relief. You could claim up to £40,000 per person or £80,000 for married couples, provided certain conditions are met.

- Annual Exempt Amount: As an individual seller, you can benefit from an annual exempt amount of £12,300 (as of the latest figures), which means that any capital gains below this threshold aren’t taxed.

- Reliefs for Disabled Homeowners: If you or someone in your household is disabled and you’ve made adjustments to your property, the costs associated with these modifications can sometimes qualify for tax relief, depending on the sale circumstances.

- Business Assets Relief: If you’re selling a property that has been used partially for business purposes, you may be able to claim Business Asset Disposal Relief, allowing up to £1 million in lifetime gains taxed at only 10%.

| Relief/Allowance | Description | Max Exemption/Benefit |

|---|---|---|

| Private Residence Relief | Full relief on gains if the home was your main residence | Full Relief |

| Letting Relief | Relief if part of your home was rented out | £40,000 per person |

| Annual Exempt Amount | Tax-free threshold on capital gains | £12,300 |

| Disabled Homeowners Relief | Tax relief on modifications for disabled homeowners | Varies |

| Business Assets Relief | Lower tax rate on business property sales | Up to £1 million gains |

Real-World Examples

Consider Sarah, who sold her home after living there for ten years. Because it was her main residence the entire time, she could claim Private Residence Relief, which exempted her from any Capital Gains Tax on the sale proceeds.

Now, if we look at John, who rented out a room in his home for five years while living there, he could potentially use Letting Relief. His qualifying period would allow him up to £40,000 in tax-free gains, significantly cushioning the financial impact of selling.

Practical Implications

Understanding these reliefs can greatly enhance your financial planning when selling a house. If you can maximize your use of these allowances, you’re likely to minimize the taxes owed. It’s advisable to keep thorough records of your occupancy and any qualifying modifications or rentals associated with the property.

Lastly, before you finalize any sale, ensure you consult with a tax professional to confirm your eligibility for these reliefs and to optimize your tax position accordingly. Knowing the rules and limits allows you to make informed decisions that could save you thousands when selling your home.

Real-World Scenarios: Seller Experiences

When it comes to selling a house in the UK, the day-to-day experiences of sellers can heavily influence your expectations and preparations. Real-world scenarios provide valuable insights into how the selling process unfolds, the challenges faced, and the unexpected costs that can emerge.

Many sellers report their most impactful experiences during the process. Here are key takeaways from these seller experiences based on recent research:

- Market Timing: A significant 64% of sellers emphasize the importance of timing their sale. Those who sold during a rising market reported feeling less pressure to reduce their asking price.

- Unexpected Costs: Over 70% of sellers experienced unexpected costs, with maintenance repairs averaging around £2,500 prior to the sale.

- Negotiation Experiences: Nearly 50% of sellers recounted negotiating after surveys revealed issues that needed addressing. This frequently resulted in reduced offers or seller concessions.

| Scenario | Percentage of Sellers Affected | Average Cost (£) |

|---|---|---|

| Timed Sale Benefits | 64% | N/A |

| Unexpected Repairs | 70% | 2,500 |

| Price Negotiation Impact | 50% | £1,000 discount on average |

Real-World Examples:

1. David’s Dilemma: David listed his three-bedroom house in a popular area but had to lower his asking price by £10,000 after conducting necessary repairs that were not factored into his initial pricing. It taught him to budget for unexpected maintenance costs.

2. Sarah’s Timing: Sarah waited six months to sell after monitoring property price trends. Selling during a price uptrend, she received £15,000 more than she would have if she had sold earlier in a down market, validating her strategy of watching market fluctuations.

3. John’s Negotiation Facts: John reported feeling frustrated by the buyer’s offers, which came in lower than anticipated after a home inspection revealed issues. He had to negotiate and ended up conceding £1,500 on the final price to maintain the sale.

Practical Insights:

- Set Aside Funds for Repairs: Always expect the unexpected. Setting aside at least 2-5% of your expected sale price for repairs and maintenance can ease financial pressure.

- Monitor Market Trends: Pay close attention to market trends, as timing your sale could significantly impact your profits. Tools such as price index reports can be quite helpful.

- Prepare for Negotiations: Be ready for negotiations; buyers will often use survey results to leverage lower offers. Prepare mentally and financially for these discussions.

Did you know that 30% of sellers found value in employing a home staging strategy and reported receiving offers 20% faster? Consider staging your home to make a significant difference in attracting potential buyers more rapidly.

Navigating Legal Fees in Home Sales

When it comes to selling your home, navigating legal fees is a crucial yet often overlooked part of the process. These fees can range widely depending on multiple factors, and understanding them can aid you in planning your budget effectively.

Understanding Legal Fees in Home Sales

Legal fees for home sales tend to be structured in several ways:

- Hourly Rate: Lawyers may charge between £150 to £350 per hour, depending on their experience and the complexity of your case.

- Flat Fee: For specific tasks such as contract preparation or document review, many attorneys opt for a flat fee. This can be particularly appealing if your transaction is straightforward.

- Retainer Fee: This involves paying an upfront sum which covers ongoing work. Make sure you clarify what services are included to avoid unexpected charges.

Comparative Table of Legal Fees

| Fee Structure | Description | Typical Cost Range |

|---|---|---|

| Hourly Rate | Charged for the time spent on your case | £150 - £350/hour |

| Flat Fee | Set fee for specific services | £500 - £2,000 |

| Retainer Fee | Upfront payment deducted as work hours accrue | £1,000+ |

Real-World Example

Take, for instance, a homeowner in London who was selling a property valued at £600,000. They engaged a solicitor to handle the transaction at a flat fee of £1,500. This fee might have seemed like a high cost initially, but it represented only about 0.25% of their sale price—an investment that safeguarded their interests and ensured a smooth sale process.

Another example involves a couple selling their inherited property. They encountered complications with title discrepancies, which necessitated more comprehensive legal intervention. Instead of a standard flat fee, they opted for an hourly rate arrangement. Although it led to total fees of £2,500, this was significantly less than potential losses from mismanaged title issues.

Practical Implications for Sellers

- Anticipate These Costs: Knowing the different fee structures can help you budget better. Consider asking your lawyer for a detailed breakdown of anticipated legal fees.

- Choose the Right Fee Structure: Depending on your comfort level with legal documents, you might prefer a flat fee for straightforward sales or an hourly arrangement for complex scenarios.

- Consider Experience and Complexity: If your sale involves unusual variables—like inheritance issues or liens—investing in an experienced attorney can save you from costly troubles down the line.

Legal fees, while an upfront cost, can often help protect you from bigger headaches and losses later in the process. Evaluate your specific needs carefully and ensure you choose a structure that aligns well with your situation.

Maximizing Profits: A Seller’s Guide

When it comes to selling your house in the UK, maximizing your profits is essential. By understanding the nuances of the selling process and the market, you can make informed decisions that directly enhance your financial outcome.

Key Strategies to Maximize Profits

1. Timing the Market: The property market experiences cycles. Research indicates that selling during peak seasons like spring can result in 15% higher offers compared to off-peak seasons. Understanding local trends allows you to choose the best timing for your sale.

2. Enhancing Curb Appeal: First impressions matter, and investing in minor renovations can increase property value. Homes with upgraded landscaping or freshly painted exteriors sell for an average of 10% more.

3. Pricing Strategically: Listing your house slightly below market value can create a competitive bidding atmosphere, potentially leading to offers that exceed your initial asking price. A well-researched pricing strategy considering nearby property sales can optimize results.

4. Utilizing Online Platforms: With 90% of buyers starting their home search online, ensure your property is showcased on popular real estate websites. High-quality photos and a well-written description can attract more potential buyers.

5. Negotiate with Buyers: Being open to negotiation can slightly increase your selling price. Research shows that homes that allow room for negotiation often fetch 5% more than their fixed-price counterparts.

| Strategy | Potential Profit Increase |

|---|---|

| Timing the Market | 15% |

| Enhancing Curb Appeal | 10% |

| Strategic Pricing | Varies, often 5-10%+ |

| Online Presence | 20% engagement boost |

| Negotiation | 5% |

Real-World Examples

Consider Lisa, who sold her two-bedroom flat in London. By waiting for the spring market and investing £1,500 in fresh paint and landscaping, she attracted three buyers during the first week of viewings. Consequently, she received offers 12% higher than her expected price.

Another example is Mark, who decided to use a popular online property portal. With professional photography and a compelling description, his house was listed for one week before receiving an offer that met his asking price. He later discovered similar properties nearby had been listed for weeks before finding buyers.

Practical Implications for Sellers

These strategies highlight the importance of a proactive approach to selling. A carefully timed, well-presented property is likely to outshine the competition. Whether you’re sprucing up your home or creating an enticing online listing, each effort directly correlates to your final selling price.

Actionable Advice for Maximizing Profits

- Always research local market conditions to understand the optimal selling period.

- Dedicate time to enhance your home’s appeal, ensuring buyers see its true value at first glance.

- Make use of technology, such as virtual tours, to widen your reach and increase buyer interest.

- Remain flexible and open to negotiations—often the final price is just the beginning of the conversation.