What are Property Inheritance Laws in the United States? They’re the rules that dictate how someone’s assets, from homes to bank accounts, get divided when they pass away. Think about it: if you’ve got that vintage car from your granddad or a family cabin that has seen summers filled with laughter, understanding these laws is crucial. For instance, did you know that in some states, if there’s no will, the property might automatically go to the spouse and children—often excluding other family members, like siblings or parents? That’s something that could launch a family feud or leave a sentimental heirloom out in the cold.

Now, let’s dive into some specifics. In community property states like California and Texas, any property acquired during marriage is typically split 50/50 between spouses. On the flip side, states following common law treat property differently, often prioritizing what’s in a will. According to the National Conference of State Legislatures, about 70% of Americans die without a will, which means their assets could be stuck in limbo, or worse, distributed in a way they would have never wanted. Whether you’re looking at a sprawling estate or just a few cherished possessions, knowing these laws can help you navigate the often tangled web of inheritance scenarios.

Overview of State-Specific Inheritance Laws

Understanding state-specific inheritance laws can feel overwhelming, but it’s crucial for effective estate planning. These laws dictate how property is passed down after someone dies, which can vary significantly depending on where you live. Let’s dive into how these laws differ across states.

Key Points About Inheritance Laws

- Community Property States: In states like California and Texas, any property acquired during marriage is considered community property, typically split evenly upon death. Approximately 9 states follow this model.

- Intestate Succession Laws: If someone dies without a will, each state has its own intestate succession laws. For instance, Florida prioritizes children over parents, while New York gives priority to spouses and children. It’s estimated that more than 50% of Americans die without a will, highlighting the importance of understanding these laws.

- Elective Share Laws: In some states, a surviving spouse can claim an elective share, which is a percentage of the deceased spouse’s estate regardless of will provisions. This percentage can vary; for example, New Jersey allows 1/3 of the estate, while in states like Georgia, the share is 1/4.

- Per Stirpes vs. Per Capita Distribution: Some states use “per stirpes,” allowing heirs to inherit through their parents, while others use “per capita,” dividing equally among living heirs. About 20 states follow the per stirpes principle.

| State | Community Property | Elective Share | Intestate Order |

|---|---|---|---|

| California | Yes | Yes (1/2) | Children > Spouse |

| Florida | No | Yes (1/3) | Children > Parents |

| New York | No | Yes (1/3) | Spouse > Children |

| Texas | Yes | Yes (1/2) | Children > Spouse |

| Georgia | No | Yes (1/4) | Spouse > Children |

Real-World Examples

1. Example of Community Property: In a California case, a couple bought a house together during their marriage. Upon the husband’s death, the wife inherited the entire property as community property, regardless of anything stated in the will.

2. Case of Intestate Succession: In Florida, when a man passed away without a will, his assets were distributed according to state law, prioritizing his adult children over his siblings, which aligned with his apparent wishes but highlighted the need for clear estate planning.

3. Elective Share Application: A New Jersey widow found herself entitled to 1/3 of her late husband’s estate despite his will stating otherwise, showcasing the protective measures in place for surviving spouses.

Practical Implications for You

- Check your state’s community property laws if you’re married, as this can significantly affect how your assets are managed after death.

- Familiarize yourself with intestate succession laws in your state to understand how your assets will be distributed without a will.

- If you are a spouse, consider discussing your rights regarding the elective share with your estate planning attorney to better protect your interests.

Actionable Facts

- Review and update your will based on your state laws to ensure assets are distributed per your wishes.

- Always consult an estate planning attorney who is familiar with your state’s laws for personalized advice.

- Remember that estate laws often change; staying informed can safeguard your and your beneficiaries’ interests in the future.

Statistical Trends in Property Inheritance

Understanding the statistical trends in property inheritance can provide valuable insights into how wealth is transferred across generations in the United States. These trends reveal patterns in demographics, property values, and the impact of varying laws on inheritance processes.

Key Trends in Property Inheritance

- Increase in Real Estate Transfers: In recent years, approximately 45% of inherited wealth comes from real estate, compared to 30% a decade ago. This reflects a growing trend where families are passing down property as a significant component of their estates.

- Generation Wealth Structures: A 2022 survey indicated that about 62% of millennials expect to receive a significant inheritance, often surpassing $100,000 each. This is up from just 48% among baby boomers when asked about the same expectations at this age.

- Race and Inheritance: Inheritance trends also reveal disparities across racial demographics. For instance, data shows that White families are 50% more likely to pass down substantial estates (over $200,000) compared to Black families.

Comparative Table of Inheritance Statistics

| Year | Percentage of Inherited Wealth from Real Estate | Millennial Expectations for Inheritance | Racial Disparities (%) |

|---|---|---|---|

| 2022 | 45% | 62% | White 50% vs. Black 25% |

| 2012 | 30% | 48% | N/A |

Real-World Examples

Take the case of a family in California, where the parents transferred their beachfront property valued at $1.5 million to their children. This transfer exemplifies the trend of property being a primary vehicle for wealth transfer. The children, who represent a millennial demographic, reported that they are not only inheriting land but are also actively engaging in its upkeep and value improvement.

Another example can be observed in a New York estate where an elderly couple with a combined wealth of $2 million decided to split their estate among three children. The decision came forth due to their understanding of the rising property values in their neighborhood, illustrating how parents are increasingly aware of market conditions when planning inheritance.

Practical Implications for Readers

It’s imperative for individuals to recognize these trends when planning their estates. Families should consider the following:

- Asset Valuation: As real estate becomes a larger aspect of inherited wealth, regular assessment of property values can help families prepare for equitable distribution.

- Planning for Racial Disparities: Observing the gaps in inheritance across racial lines encourages discussions on financial literacy and preparedness for all family members, regardless of background.

- Engage in Estate Planning Early: Given that younger generations anticipate receiving inheritances, proactive discussions about estate plans can foster openness and minimize conflict.

Actionable Advice on Property Inheritance

- Keep track of the changing value of your property assets to facilitate smoother transitions during inheritance.

- Encourage multi-generational conversations about financial expectations and responsibilities to ensure clarity and cooperation.

- Explore options like trusts to mitigate potential legal complications and ensure that your property inheritance aligns with your values, especially in a changing legal landscape.

Implications of Probate Processes

Understanding the implications of probate processes is essential when dealing with property inheritance laws in the United States. These processes can significantly affect how and when heirs receive their inheritances, and they can also introduce complexities that might not be apparent at first glance.

Key Points About Probate Processes

- Duration and Delays: Probate can be a lengthy process. On average, settling an estate through probate can take anywhere from several months to a couple of years, depending on the size of the estate and any potential disputes among heirs.

- Costs Involved: The average cost of probate can range from 3% to 7% of the estate’s value, which can diminish the overall inheritance your heirs will receive.

- Public Record: Probate proceedings become part of the public record, meaning anyone can access the details of the estate, including assets and beneficiaries. This can lead to unintended outcomes, such as privacy concerns where heirs might prefer to keep their financial matters private.

Comparative Table of Probate Processes

| State | Average Length of Process | Average Cost of Probate | Publicity Status |

|---|---|---|---|

| California | 9 months | 4% of the estate value | Public |

| Texas | 6-12 months | 5% of the estate value | Public |

| Florida | 10 months | 3-6% of the estate value | Public |

| New York | 7-14 months | 5-7% of the estate value | Public |

| Illinois | 8-12 months | 4-6% of the estate value | Public |

Real-World Examples of Probate Implications

Consider a scenario where a deceased individual has a sizable estate but did not establish a living trust. Their heirs could face a drawn-out probate process, which might involve court fees and attorney costs. One family in California waited almost a year to settle their estate, incurring over $20,000 in probate fees, which significantly reduced the inheritances intended for their children.

In another case, a couple in Texas intended to leave their home and savings to their children. After their passing, the estate entered probate, and the children faced delays in accessing funds for urgent financial needs. They had to wait six months for the court to appoint an executor, which added stress to an already challenging time.

Practical Implications for Readers

- Plan Ahead: To avoid probate complications, consider setting up a living trust. This can expedite the transfer of assets and maintain privacy.

- Understand Costs: Be aware that probate costs can eat away at your estate, so engage in thorough financial planning to designate funds specifically for these expenses.

- Communicate with Heirs: Open discussions with family members about estate plans can help manage expectations and reduce the likelihood of disputes that can prolong the probate process.

Consider the impact of probate processes as you navigate property inheritance laws. Being informed can help you take proactive steps to streamline the transfer of your assets and protect your heirs from unnecessary complications.

Real-World Case Studies on Inheritance

When discussing property inheritance laws, it’s compelling to explore how these laws play out in real-world scenarios. This section dives into case studies that illustrate the impact of inheritance decisions, showcasing how different state laws and personal choices shape the transfer of property.

Key Insights from Real-World Inheritance Cases

- In some instances, families face significant conflicts over inheritance, especially when the decedent’s will is ambiguous. For example, in an estate valued at $2 million, siblings battled over a property that wasn’t clearly defined in the will, leading to a costly legal dispute that drained almost 25% of the estate’s total value.

- A notable statistic reveals that about 30% of estates in the U.S. involve disputes among heirs, emphasizing the importance of clear documentation and open communication in estate planning.

- Properties inherited from family members can lead to substantial financial gains. In one case study, a home inherited in San Francisco appreciated in value by 150% over a decade, illustrating how market conditions affect inherited assets.

Comparative Table of Inheritance Disputes

| Case Type | Percentage of Cases | Average Legal Costs |

|---|---|---|

| Disputed Wills | 30% | $150,000 |

| Trust Contests | 25% | $200,000 |

| Intestate Successions | 20% | $100,000 |

| Property Title Disputes | 15% | $75,000 |

| Claims Against Estates | 10% | $50,000 |

Real-World Examples of Inherited Property

One fascinating case involved the heirs of a prominent businessman who passed away without a will. The estate, comprising multiple properties across several states, faced prolonged probate due to intestacy laws. The siblings learned the hard way that without clear directives, they had to navigate state-specific laws to ascertain who was entitled to what, leading to not only legal fees but strained family relationships.

In another scenario, a grandfather’s decision to transfer a family farm to his only granddaughter was complicated by varying state inheritance laws regarding generations skipping. This situation mandated understanding both the tax implications and the emotional aspects of inheritance, showcasing the importance of planning for both financial and relational factors.

Practical Implications for Inheritance Cases

- It’s essential for heirs to understand the specific inheritance laws in their state. This knowledge can prevent costly disputes and foster family harmony.

- Individuals should consider establishing a living trust to manage their assets while they are alive, which can simplify the inheritance process and minimize potential disagreements among beneficiaries.

- Open dialogue among family members regarding estate plans and expectations can significantly decrease the likelihood of conflict, encouraging a more straightforward inheritance journey.

Specific suggestions include:

- If you’re dealing with inheritance, prioritize clear documentation. Use straightforward language in wills and trusts to avoid misinterpretation.

- Consider consulting with an estate planning attorney, especially if there are complex family dynamics or substantial assets involved. This proactive step can save families time and stress in the long run.

Advantages of Clear Inheritance Planning

Inheritance planning is not merely about distributing assets; it’s about ensuring clarity and security for your loved ones. Properly managing how your wealth will be transferred can prevent headaches and heartaches later. Let’s delve into the significant advantages that come with clear inheritance planning.

Key Advantages of Clear Inheritance Planning

1. Peace of Mind: Knowing your assets will be distributed according to your wishes provides immense comfort. This sense of security helps you focus on enjoying life now, rather than worrying about the future.

2. Minimizes Family Conflicts: Clarity in your inheritance plan can greatly reduce the chances of disputes among heirs. When family members are clear about their shares, it can foster harmony. Research shows that ambiguous inheritance can lead to family rifts, highlighting the importance of clear directives.

3. Tax Efficiency: Did you know that effective inheritance planning can minimize the tax burden on your beneficiaries? By applying tax strategies, you can increase the net value of what your loved ones inherit, ensuring they retain more financial resources.

4. Protection for Vulnerable Beneficiaries: Inheritance planning allows you to create safeguards for minors or individuals with special needs. Establishing trusts or designating guardians can ensure that these beneficiaries are cared for in a way that aligns with your values and priorities.

5. Preservation of Family Wealth: You can create a legacy that lasts for generations by planning. Wealth preservation strategies can safeguard against creditors and lawsuits, ensuring your family assets remain intact.

6. Business Continuity: For entrepreneurs, inheritance planning can ensure a smooth business transition, preserving not just wealth but also the legacy of the business. Strategically structured buy-sell agreements can prevent ownership conflicts and maintain operations seamlessly.

| Advantage | Description | Sources of Value |

|---|---|---|

| Peace of Mind | Assurance that assets go where intended | Clarity reduces anxiety |

| Minimized Family Conflicts | Clear directives reduce disputes | Defined distributions |

| Tax Efficiency | Asset distribution can be optimized to lower tax liabilities | Enhanced inheritance for beneficiaries |

| Beneficiary Protection | Special provisions for minors or individuals with special needs | Trusts secure their interests |

| Wealth Preservation | Safeguarding family assets from creditors and lawsuits | Long-term financial security |

| Business Continuity | Ensures smooth transitions in ownership for family-owned businesses | Legacy management |

Real-World Examples

Consider the case of a family business passed down to the next generation. The absence of a clear inheritance plan resulted in two siblings entering a drawn-out legal battle over ownership, causing familial stress and financial loss. In contrast, a well-structured inheritance plan with specific buy-sell agreements could have ensured both a smooth transition and maintained family harmony.

Similarly, when an individual with considerable assets passed away without a clear will, the resulting confusion over asset distribution led to family disputes that dragged on for years. Conversely, another family who invested in a comprehensive inheritance plan found that their loved ones could focus on mourning their loss rather than navigating complicated legal matters.

Practical Implications for You

To leverage the advantages of clear inheritance planning, consider the following actionable steps:

- Categorically Specify Beneficiaries: Lay out each beneficiary with clear designations to avoid ambiguity.

- Quarterly or Annual Reviews: Regularly revisit and revise your plan to reflect any changes in your life, like marriage, divorce, or the arrival of new family members.

- Consult Professionals: Working with estate planning attorneys can help customize a strategy that’s compliant with laws and tailored to your unique circumstances.

- Engage in Family Discussions: Open conversations about your plans can prepare family members and mitigate surprises, potentially reducing conflicts.

- Consider a Trust: For beneficiaries needing extra protection, establishing trusts can ensure their needs are prioritized and well managed.

By taking these steps, you can fully harness the myriad advantages of clear inheritance planning, providing durable peace of mind for yourself and financial security for those you love.

Common Mistakes in Inheritance Procedures

When it comes to navigating inheritance procedures, many people stumble into common pitfalls that can complicate matters. Understanding these mistakes helps you avoid costly delays and ensures a smoother transition of assets.

Key Points About Common Mistakes

1. Assuming a Will is Enough: Many individuals believe simply drafting a will suffices. However, without a comprehensive estate plan that addresses taxes, debts, and living trusts, heirs might face unexpected challenges. Around 60% of Americans don’t have any estate planning documents in place, leading to issues such as intestate succession.

2. Not Considering Tax Implications: One common mistake involves ignoring the potential tax liabilities on inherited assets. For example, unfair capital gains tax assessments can arise if assets are not correctly valued at the date of death. A shocking 70% of heirs find themselves financially unprepared for inheritance taxes.

3. Failing to Update Legal Documents: Life changes, such as marriage or divorce, can render old wills and trusts outdated. Many families experience disputes when heirs attempt to claim assets based on outdated documents. Approximately 40% of individuals never revise their estate plans after significant life events.

Comparative Table: Mistakes vs. Consequences

| Common Mistakes | Potential Consequences |

|---|---|

| Assuming a will is sufficient | Intestate succession leads to unwanted heirs |

| Ignoring taxes | Unexpected tax liabilities reduce inheritance value |

| Not updating documents | Legal disputes among heirs increase |

Real-World Examples

A classic case involved a family that inherited a vacation home. The decedent’s will, written 20 years prior, stated that the property should go to the eldest son. However, since the mother had remarried afterward and had two more children, the new spouse and younger siblings contested this outdated directive, leading to a prolonged and costly probate process.

In another scenario, a couple inherited substantial stocks but failed to account for capital gains taxes. Upon selling these stocks, they faced a tax bill that diminished their inheritance significantly. This lack of foresight in tax awareness left them frustrated and financially strained.

Practical Implications

To avoid falling into these traps, here are some actionable insights:

- Regularly Review and Update Your Estate Plan: Make it a point to revisit your estate plan at least every five years or after major life events.

- Consult a Tax Professional: Before making any significant inheritance decisions, seek advice from a tax expert to understand potential liabilities.

- Communicate with Heirs: Keep your family informed about major changes in your estate plan to minimize confusion and disputes later on.

Focusing on these common mistakes and taking proactive measures can greatly enhance the effectiveness of your inheritance process, ensuring your assets are distributed according to your wishes without unnecessary complications.

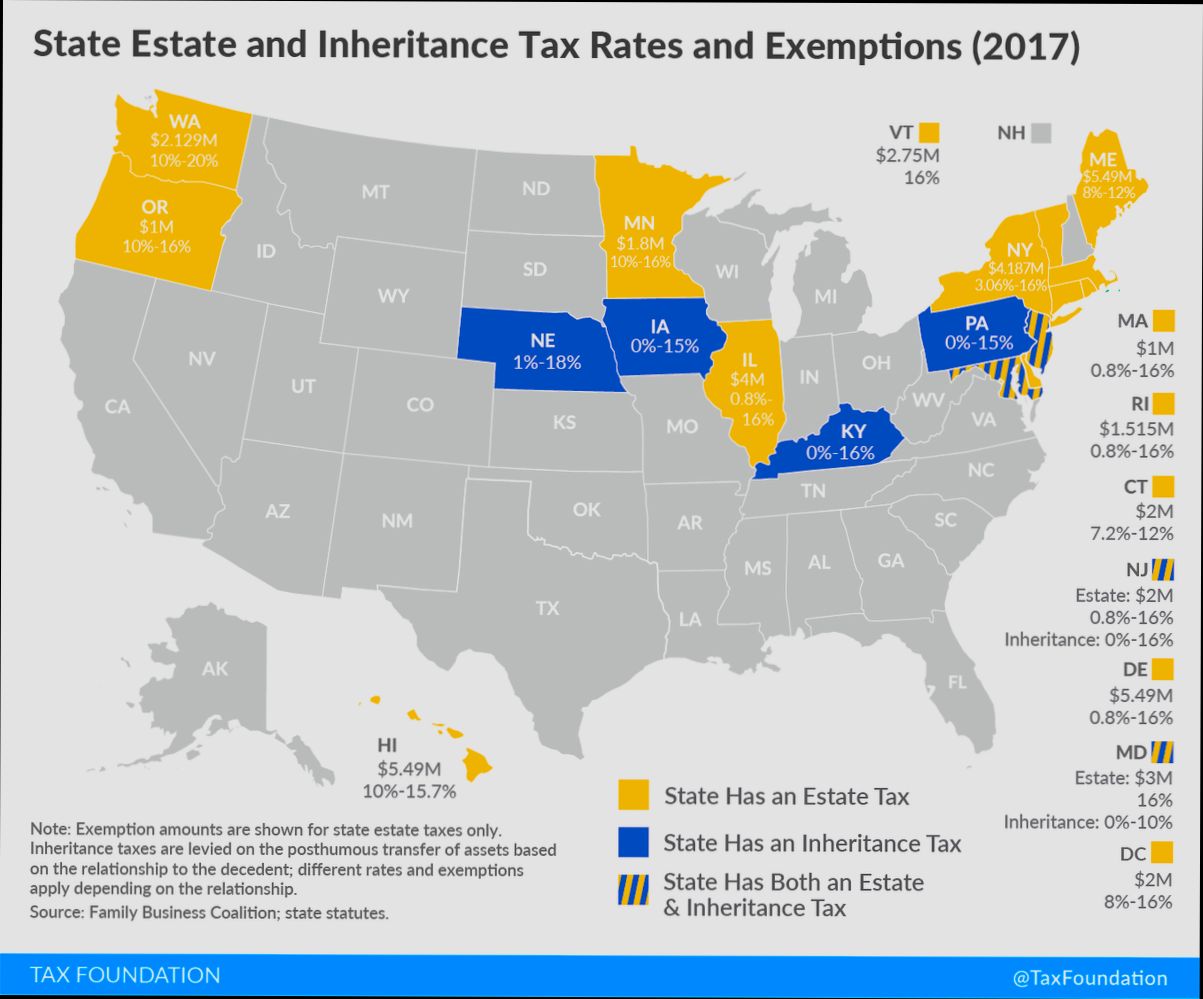

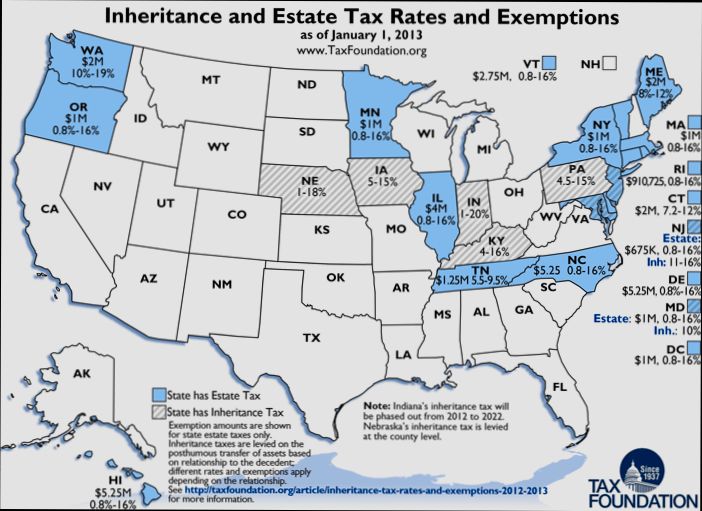

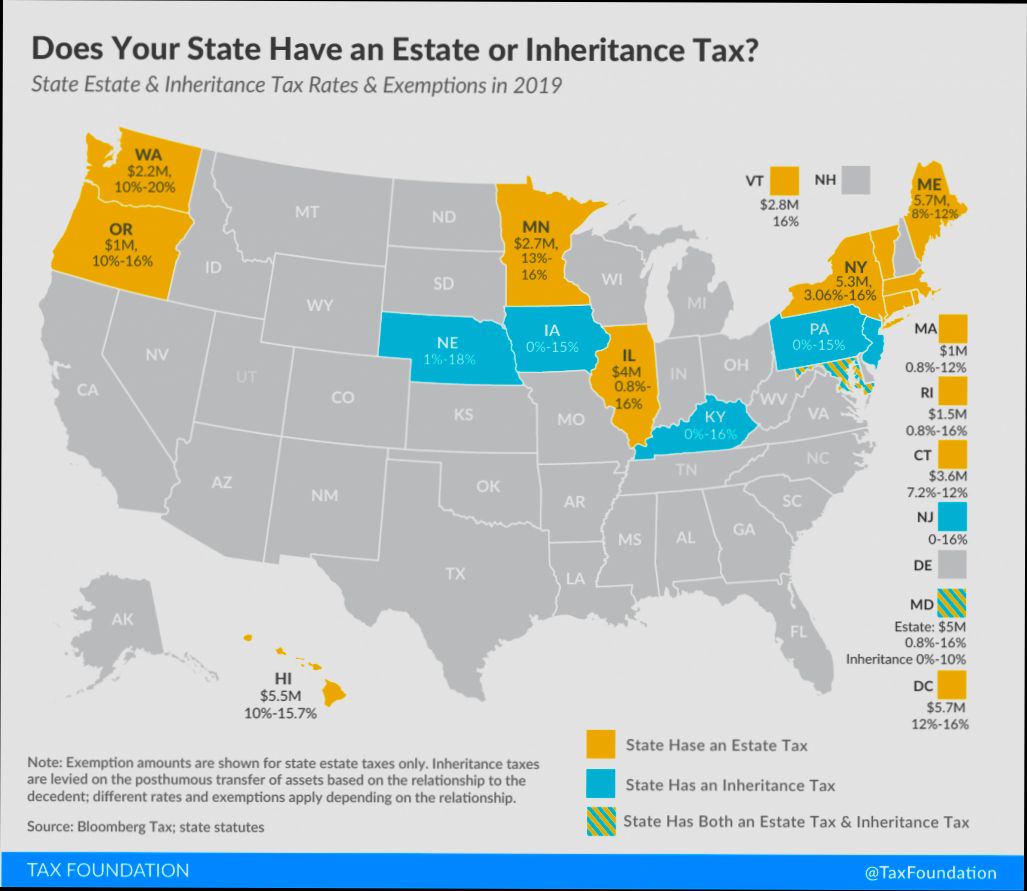

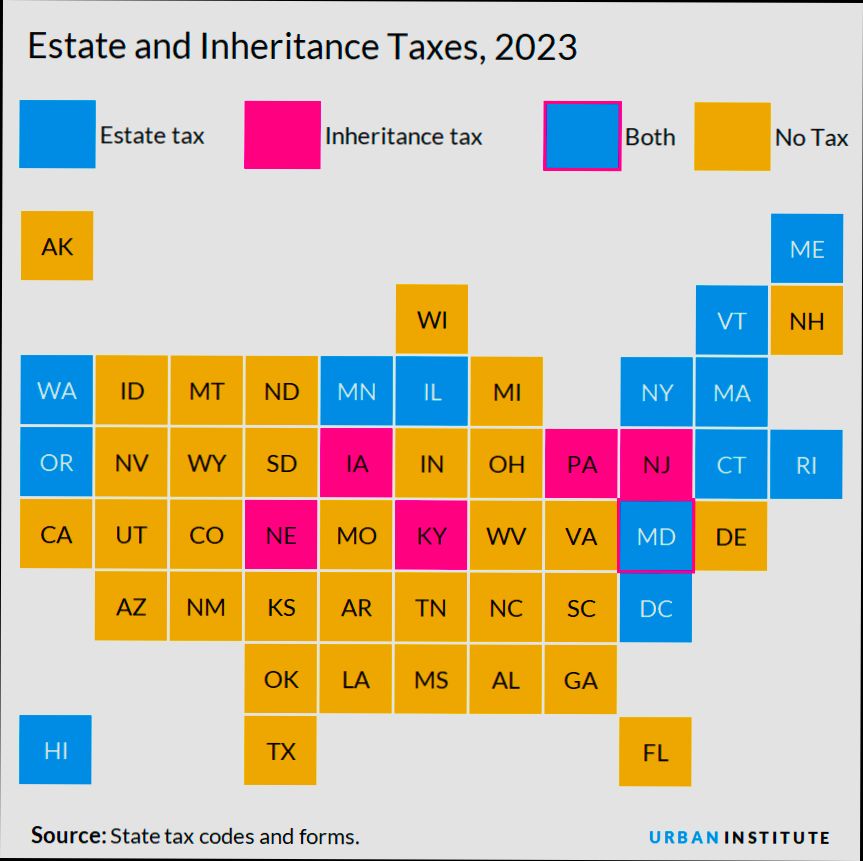

Federal vs. State Inheritance Regulations

When it comes to property inheritance laws in the United States, understanding the distinction between federal and state regulations is crucial. Federal laws primarily address estate taxes, while states often impose their own inheritance taxes and estate tax regulations. This section breaks down these differences and offers practical insights you can apply.

Key Differences in Taxation

1. Types of Taxes:

- Estate Tax: Imposed federally and is based on the total value of the deceased’s estate before the distribution of assets. In 2025, the federal estate tax exemption is set at $13.99 million for individuals and $27.98 million for married couples.

- Inheritance Tax: This is state-specific and applies to inheritances received by beneficiaries, with tax rates varying based on relationships. While close relatives may enjoy exemptions or lower rates, states such as Pennsylvania impose inheritance taxes that can go up to 15% for certain beneficiaries.

2. Exemption Levels:

- The federal estate tax exemption allows large estates to escape taxation entirely if they’re valued below the threshold. In contrast, individual states often have lower exemptions. For example, New York’s estate tax exemption is only $6.93 million as of 2025, less than half of the federal exemption.

3. Who Pays:

- The estate tax responsibility falls on the estate before any distributions. However, inheritance taxes are paid by beneficiaries, meaning if you inherit a significant asset in a state with an inheritance tax, you may owe that tax when you receive your share.

Comparative Table of Federal and State Regulations

| Type of Tax | Federal Estate Tax | New York Estate Tax | Pennsylvania Inheritance Tax |

|---|---|---|---|

| Exemption | $13.99 million | $6.93 million | N/A (Based on value received) |

| Tax Rate | Up to 40% | 3.06% - 16% | 0% - 15% |

| Responsibility | Estate pays | Estate pays | Beneficiary pays |

Real-World Examples

Consider a couple in New York with an estate valued at $15 million. After the federal exemption of $13.99 million, their estate would face taxation on the $1.01 million overage at the federal level, subject to rates that can reach 40%. In addition, they would also be liable for state taxes since New York’s estate tax threshold is significantly lower.

On the other hand, a beneficiary in Pennsylvania who receives an inheritance of $500,000 would be liable for state inheritance taxes based on the relationship to the deceased. For instance, a child inheriting this amount could face a tax burden of up to 4.5%, equating to $22,500 owed.

Practical Implications for Inheritance

Understanding these regulations is vital for effective estate and financial planning. If you live in a state with both inheritance and estate taxes, failing to plan could significantly diminish the wealth passed on to your heirs. Here are some practical steps:

- Evaluate Estate Value: Know your total estate value and understand what portion will be taxable at both federal and state levels.

- Consider Gifting Strategies: To minimize future estate taxes, consider gifting portions of your estate to heirs while living.

- Use Proper Legal Vehicles: Trusts and other estate planning tools can help optimize how assets are distributed and potentially reduce tax obligations.

Actionable Advice

If you are in a state with substantial inheritance taxes, consider consulting with an estate planning attorney familiar with both federal and state laws to devise a comprehensive strategy. Keep abreast of any changes in state tax laws, as they can directly impact your estate planning. It’s critical to know whether your estate exceeds the federal limits, but also how state laws may create additional liabilities that federal laws do not address.