- Exploring Regional Market Trends in Europe

- Navigating Financing Options for European Real Estate

- Evaluating Tax Implications for Foreign Buyers

- Practical Case Studies of Successful Transactions

- Identifying Key Benefits of Investing in European Properties

- Essential Steps in the Property Acquisition Process

How to Buy a Property in Europe can seem like a daunting task, but it’s an adventure many have successfully tackled. Imagine strolling through the charming streets of Barcelona, sipping coffee while eyeing a quaint apartment with a balcony overlooking the bustling plaza. Or think about snagging a rustic villa in Tuscany, surrounded by rolling hills and vineyards. With the right information, those picturesque dreams can become a reality. Did you know that property prices in Madrid have surged by around 7% in the past year, making it a hot spot for investment? Meanwhile, cities like Lisbon remain relatively affordable compared to other EU capitals, with average home prices around €2,500 per square meter.

Understanding the quirks of different regions is crucial. For instance, buying a one-bedroom flat in Paris could set you back an average of €10,000 per square meter, while a similar property in Berlin might cost you only €4,500. Plus, each country comes with its own set of rules and regulations – did you know that in Italy, non-EU buyers face stricter restrictions, while Spain offers a Golden Visa to investors? It’s essential to dig into each locale’s market dynamics to make a savvy choice. You could even tap into the growing trend of remote work, turning a cozy cottage in the Scottish Highlands into your new office. Keep these scenarios in mind as we explore the exciting journey of property ownership across Europe!

Understanding Legal Frameworks for Property Purchase

When considering purchasing property in Europe, understanding the legal frameworks governing transactions is crucial. Each country has its own set of laws, fees, and requirements that can impact your buying process, making it essential for you to navigate these intricacies effectively.

Key Legal Aspects of Property Purchase

1. Buyer’s Rights and Obligations: In most European countries, buyers have specific rights, such as the right to a written contract and disclosure of all relevant property details. However, it’s also your responsibility to conduct thorough due diligence.

2. Role of Notaries: In many European nations, notaries play a pivotal role in property transactions. Their fees generally range from 1% to 3% of the property’s value. For example, in France, a notary is responsible for ensuring that the contract meets legal standards, verifying the property’s title, and collecting the necessary taxes.

3. Purchase Taxes: The purchase tax reflects different legal obligations across countries, usually ranging from 2% to 10% of the property’s value. Countries like Portugal typically have a lower rate, appealing to foreign buyers. You should account for this expense in your budget early on.

4. Registration Fees: Registering the property in your name is another legal requirement that typically involves fees ranging from 1% to 3% of the property value. Failing to register the property can lead to ownership disputes in the future.

Comparative Table of Purchase Costs

| Country | Purchase Tax (%) | Notary Fees (%) | Registration Fees (%) | Total Estimated Transaction Fees (%) |

|---|---|---|---|---|

| Portugal | 2-8 | 1-2 | 0.8-1.5 | 4-11.5 |

| Spain | 6-10 | 1-2 | 1-2 | 8-14 |

| France | 5-7 | 1.5-2.5 | 0.7-1.5 | 7.2-11.5 |

| Italy | 2-4 | 1-2 | 0.5-1.5 | 3.5-7.5 |

Real-world Examples

In Portugal, the popular Golden Visa program allows foreign buyers to gain residency through property investment, benefiting from favorable tax rates and legal simplicity. A buyer purchasing a property for €300,000 would face estimated total fees of about €15,000 if we assume an average purchase tax of 5% and notary fees around 1.5%.

In France, when buying a luxury apartment in Paris priced at €1 million, buyers often need to prepare to pay approximately €70,000 to €150,000 in taxes and fees due to the high notary fees and registration costs associated with luxury real estate transactions.

Practical Implications for Buyers

Navigating the legal frameworks involves understanding local customs, obtaining the appropriate permits, and ensuring compliance with tax obligations. It’s advisable to engage local legal counsel familiar with real estate law in the specific region where you’re buying. This will help protect your interests and streamline the process.

If you’re financing your purchase through a mortgage, be aware that various fees associated with securing a loan, including mortgage broker fees, often add another 1% of the loan amount or a flat fee, depending on the lender.

Actionable Advice

Before signing any contracts, ensure you understand every legal implication, especially concerning your rights as a buyer. Carry out thorough due diligence to assess all obligations, fees, and required documents specific to the country where you are purchasing property. This will not only make the process smoother but will also safeguard your financial investment in your new European home.

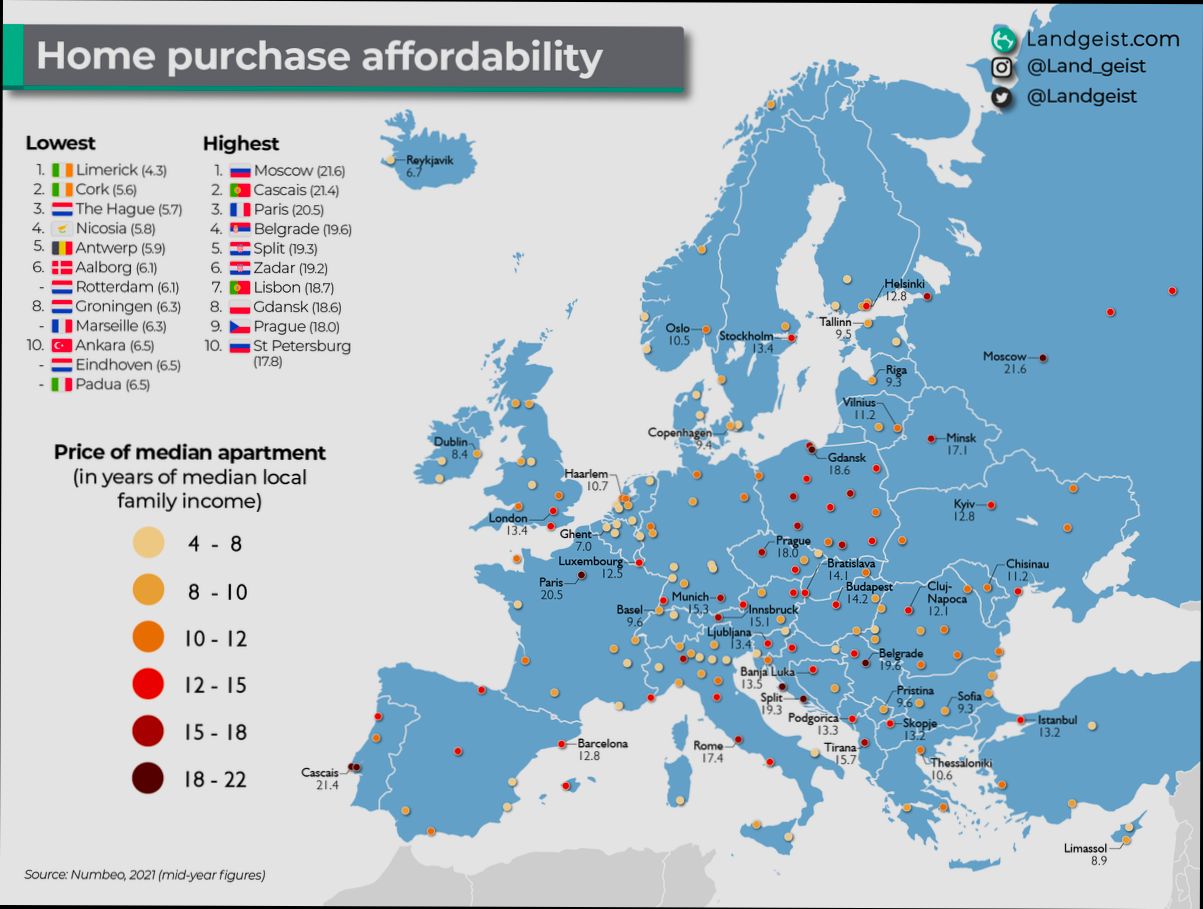

Exploring Regional Market Trends in Europe

When it comes to buying property in Europe, understanding the regional market trends is vital. Each region presents unique opportunities and challenges, influenced by economic factors, cultural preferences, and local regulations. Let’s dive into what’s currently shaping the property landscape across various European regions.

Key Regional Highlights

Here are some key trends to consider:

- Eastern Europe: Countries like Bulgaria and Romania are seeing a surge in demand, with property prices increasing by approximately 5% year-over-year. Investors are attracted by lower entry costs and potential for rental income due to rising tourism.

- Western Europe: The competitive markets in cities like Paris and London are witnessing price stabilization after years of soaring increases. Recent data shows that property prices in London have leveled off, with a modest change of only 1.5% over the past year.

- Southern Europe: The Spanish property market is rebounding quickly, with cities like Barcelona and Valencia recording increases in tourist investment, leading to a 7% rise in property values compared to last year. This trend indicates a growing foreign interest, particularly from Northern European buyers.

- Northern Europe: Countries like Sweden and Denmark are experiencing a unique trend where urban areas are becoming less desirable compared to suburban regions, with property values in suburbs rising by about 6% as remote working becomes mainstream.

Comparative Market Trends Table

| Region | Average Price Change (Last Year) | Key Growth Factors | Popular Investment Cities |

|---|---|---|---|

| Eastern Europe | 5% | Rising tourism and affordability | Sofia, Bucharest |

| Western Europe | 1.5% | Market stabilization after rapid growth | London, Paris |

| Southern Europe | 7% | Increased foreign investment | Barcelona, Valencia |

| Northern Europe | 6% (suburbs) | Shift towards remote working and lifestyle changes | Malmö, Aarhus |

Real-World Examples

- Bulgaria: A case study reveals a family purchasing a seaside apartment in Varna—a price rise of 5% was noted amid a seasonal spike in rental demand, highlighting the area’s attractiveness to vacationers.

- Spain: An investor who bought a property in Valencia during the COVID-19 pandemic is witnessing significant rental returns—up to 12%—due to the city’s growing appeal among expatriates and digital nomads.

- Sweden: In Malmo, increased demand for homes outside urban centers has led to a rise in property prices, showing how urban sprawl and telecommuting are influencing investment decisions and lifestyle choices.

Practical Implications

As you explore regional market trends, consider how these indicators might influence your strategy:

- Research Local Markets: Always dig deeper into specific areas rather than generalizing by country. Localized insights can help identify the best investment locations.

- Watch for Tourist Trends: Areas popular with tourists often lead to increased demand for rental properties. This can provide lucrative opportunities for short-term rentals.

- Remote Work Influence: Be mindful of how lifestyle changes driven by remote work can affect property desirability in urban versus suburban settings.

Actionable Insights

- Focus on emerging markets such as Bulgaria or Romania where prices are lower but demand is rising—these might yield great long-term investments.

- Consider the impact of foreign investment in Spain, where a local real estate professional can provide insights into which neighborhoods are developing.

- Pay attention to the changing demographics and lifestyle preferences within Northern Europe, as these shifts can reveal new opportunities in real estate purchases.

Navigating Financing Options for European Real Estate

When it comes to buying property in Europe, the financing options you choose can significantly impact your investment. Understanding the various avenues available is essential for making informed decisions. Let’s explore some of the key financing strategies and what you should consider when navigating this landscape.

Types of Financing Options

1. Local Bank Mortgages:

- Most countries in Europe offer mortgages through local banks.

- Interest rates often vary, ranging from 1.5% to 4%, depending on your creditworthiness and the property type.

2. International Lenders:

- Some lenders specialize in offering loans to foreign investors.

- These often come with higher interest rates but may provide more flexible terms.

3. Equity Financing:

- In some cases, you might consider using equity in another property you own to finance your new purchase.

- This can reduce the amount you need to borrow, potentially leading to lower monthly payments.

4. Crowdfunding Platforms:

- Newer avenues like real estate crowdfunding are becoming popular for investing in European property.

- These platforms typically operate by pooling funds from multiple investors to finance real estate projects.

Comparative Table of Financing Options

| Financing Option | Interest Rate Range | Flexibility | Ideal For |

|---|---|---|---|

| Local Bank Mortgages | 1.5% - 4% | Medium | First-time buyers |

| International Lenders | 3% - 6% | High | Foreign investors |

| Equity Financing | Varies | Medium to High | Existing property owners |

| Crowdfunding Platforms | Varies | High | Small investors seeking entry |

Real-World Examples

- Local Bank Usage: A couple looking to buy a vacation home in rural Portugal secured a 3% mortgage from a local bank. With annual property taxes hovering around 0.5% of their property value, the affordability was an attractive aspect of their investment.

- International Lending: An investor based in the U.S. sought financing through an international lender and faced interest rates of about 5.5%. Despite the higher rate, he valued the ease of acquiring a loan without establishing credit history in the EU.

Practical Implications

- Documentation Requirements: Different financing options will have varying requirements. For instance, local banks often demand comprehensive income proof, whereas international lenders might be more lenient but require higher down payments.

- Currency Fluctuations: If you’re considering foreign lending, keep in mind the risks of currency exchange rates. A slight shift in rates can significantly impact your repayment amount.

Actionable Advice

- Do Your Research: Investigate multiple banks, lenders, and other financing avenues to find the best rates and terms. Comparing options can save you thousands over the loan term.

- Consult Local Experts: Always consider working with a real estate consultant or financial advisor who understands the local market, as they provide valuable insights on the financing landscape specific to your investment goals.

Evaluating Tax Implications for Foreign Buyers

When you’re purchasing property in Europe as a foreign buyer, understanding the tax implications is crucial. Navigating the intricacies between different countries and their unique tax laws can seem overwhelming, but I’m here to break it down for you.

Understanding Tax Responsibilities

1. Capital Gains Tax: Most European countries impose a capital gains tax on profits made from selling properties. For instance, if you buy a property for €300,000 and sell it later for €400,000, you might be taxed on that €100,000 gain. Each country has its rates.

2. Property Tax: As a property owner, you will need to pay annual property taxes, which vary widely. For example, Spain charges between 0.4% and 1.1% of the property value annually.

3. Inheritance Tax: Different countries have different rules surrounding inheritance tax, with rates ranging significantly. In France, it can be as high as 60% for non-residents.

Comparative Table of Key Tax Rates

| Country | Capital Gains Tax Rate | Property Tax Rate | Inheritance Tax Rate |

|---|---|---|---|

| Portugal | 28% (fixed rate) | 0.3% to 0.8% | 10% to 20% |

| Spain | 19% - 23% | 0.4% - 1.1% | 7% - 34% |

| Italy | 26% (fixed rate) | 0.4% - 0.76% | 4% - 8% |

| France | 19% + 17.2% (social contributions) | 0.1% - 1.5% | 5% - 60% |

| Germany | 26.375% | 0.26% - 1% | 7% - 30% |

Real-World Examples

Consider a foreign buyer purchasing a property in Portugal for €250,000. In this scenario, upon selling the property after five years for €350,000, the potential capital gains tax would be approximately €28,000 (28% of the €100,000 gain). This scenario could change dramatically if the property were in France, where the buyer might face a capital gains tax of roughly €36,000 due to additional social contributions.

Another example involves rental income. If you decide to rent out your property in Spain and earn €24,000 annually, you’ll need to factor in a tax liability of approximately €4,560 (19% of €24,000), significantly impacting your income.

Practical Implications for You

- Research Local Tax Laws: Before committing to a property, understand the specific tax obligations in your desired country to avoid unexpected costs.

- Engage a Local Tax Advisor: Hiring a tax professional familiar with expatriate laws can help you navigate complexities and identify opportunities for tax savings.

- Consider Residency Impact: If you live in the property full-time, there may be exemptions or lower tax rates applicable to capital gains or inheritance taxes.

Remember that tax laws can change, and it’s a good idea to stay updated on any alterations that might affect your investment in European real estate. Investing in properties abroad can bring substantial rewards, but understanding the related tax implications will ensure you’re well-prepared for the journey.

Practical Case Studies of Successful Transactions

Navigating the complexities of buying property in Europe can be daunting, but examining practical case studies can shed light on effective strategies. These real-life examples not only illustrate the successes but also highlight common pitfalls and how to avoid them.

Successful Transactions and Key Insights

1. Case Study: A French Riviera Purchase

- A couple from Canada purchased a villa in Nice for €750,000 in early 2023. They utilized local real estate agents who understood the intricate market dynamics. Their proactive negotiation skills allowed them to buy below the initial asking price by 8%.

- Key Insight: Engage local experts who can negotiate effectively on your behalf.

2. Case Study: Urban Apartment in Berlin

- An investor from the UK purchased an apartment in Berlin for €380,000, capitalizing on the rising demand in the city’s real estate market. By conducting thorough due diligence and being aware of the local rental laws, they secured a property that yielded a 7% rental return in the first year.

- Key Insight: Research local markets and regulations to maximize rental returns.

3. Case Study: Investment in Lisbon

- A real estate investment group acquired a mixed-use property in Lisbon for €1.2 million in late 2022. They focused on properties outside the traditional tourist areas, identifying neighborhoods experiencing revitalization. Their comprehensive analysis showed potential for a 15% appreciation in value over the next five years.

- Key Insight: Look beyond popular areas to find hidden gems that may provide better growth opportunities.

Comparative Success Rates by Region

| Region | Average Purchase Price | Negotiation Success Rate | Yearly Appreciation Potential |

|---|---|---|---|

| French Riviera | €750,000 | 8% | 4.5% |

| Berlin | €380,000 | 7% | 5% |

| Lisbon | €1.2 million | 6% | 15% |

Real-World Examples and Their Implications

- The French Riviera case indicates the importance of not just relying on online listings but engaging with local agents who can “read” the market. A personal touch can often lead to better deals.

- In Berlin, the focus on understanding local rental laws resulted in a high return on investment (ROI) for the UK investor, highlighting the crucial necessity of knowledge about regulations prior to making a purchase.

- The investment group in Lisbon illustrates the advantage of recognizing emerging neighborhoods. The proactive research into areas poised for growth can yield substantial financial rewards.

Actionable Strategies for Your Transactions

- Consult local real estate experts to leverage their knowledge for negotiating better deals.

- Conduct extensive market research and demand analysis to identify properties with high rental yields.

- Look for up-and-coming neighborhoods where property values are likely to appreciate significantly over the coming years.

Keep these insights handy as you embark on your property-buying journey in Europe! Understanding the landscape through these practical case studies will empower you to make informed decisions and maximize your investment potential.

Identifying Key Benefits of Investing in European Properties

Investing in European properties offers a wealth of advantages that can enhance your portfolio and secure your financial future. Let’s delve into the key benefits that make European real estate an attractive option for many investors.

Strong Capital Growth

One of the most compelling reasons to invest in European real estate is the potential for strong capital appreciation. Data indicates that many European cities are experiencing upward trends in property values. For example, in major markets like Berlin and Lisbon, property prices have surged, with some areas reporting increases of up to 8% annually in recent years.

Diversification Opportunities

Adding European properties to your portfolio can diversify your investments geographically. This aspect protects you against local market fluctuations you might experience in your home country. European markets have shown resilience; for example, even during economic downturns, properties in popular tourist destinations such as Croatia or Greece have maintained their value.

Rental Yield

Investing in European properties can also yield attractive rental income. For instance, some cities in Spain, like Barcelona and Madrid, boast rental yields between 4% and 6%, making them hot spots for investors looking to generate cash flow. Furthermore, short-term rental markets have boomed due to tourism, allowing owners to capitalize on vacation rentals.

Favorable Currency Exchange

For non-European investors, the current strength of the Euro against several currencies can provide attractive purchasing power. Recently, fluctuations in currency rates have made properties in countries like Portugal and Italy even more affordable for foreign buyers. Investors can leverage these advantageous exchange rates to increase their investment potential.

| Country | Average Annual Property Price Increase | Rental Yield | Current Euro Exchange Rate |

|---|---|---|---|

| Spain | 6% | 4%-6% | 1.18 USD |

| Portugal | 8% | 5%-7% | 1.10 USD |

| Italy | 5% | 4%-5% | 1.12 USD |

| France | 3% | 3%-5% | 1.14 USD |

Real-World Examples

Several case studies highlight the benefits of investing in European properties. In 2022, one investor purchased a vacation rental in Lisbon for €250,000. Within a year, due to the increasing demand for short-term rentals, the property’s value appreciated by 10%, while generating a consistent rental income that covered their mortgage and other expenses.

Similarly, investing in upcoming markets like Porto, Portugal, has shown promise, where an investor acquired a property for €180,000 that has already appreciated by 12% since the purchase, while also attracting lucrative rental offers due to its vibrant cultural scene.

Practical Implications

When considering these benefits, assess your financial goals. You might want to focus on high-growth areas to maximize capital gains or choose established markets that offer steady rental income. Keep an eye on market trends and be ready to act when you spot a lucrative opportunity.

Finding the right property at the right price in Europe can be a game-changer for your investment strategy. Look at the data, analyze the potential, and explore the many opportunities that European real estate offers for thoughtful and strategic investments.

Essential Steps in the Property Acquisition Process

Buying a property in Europe involves several crucial steps that require careful planning and attention to detail. Understanding these essential steps can streamline your acquisition and help you navigate the complexities of the European real estate market.

Step-by-Step Guide to Property Acquisition

1. Initial Research and Property Selection

- Start by narrowing down your preferred locations, budget, and type of property. Research various neighborhoods to find the best fit for your lifestyle and investment goals.

- Example: A potential buyer exploring properties in Barcelona may focus on areas like Gràcia for character or Eixample for investment potential.

2. Engaging Professionals

- Hire a local real estate agent who can guide you through the buying process. Look for agents who have a strong track record in your chosen area.

- Consulting with a local attorney is also advisable to help navigate legal documents and conveyancing processes.

3. Due Diligence

- Conduct thorough due diligence on the property. This includes title searches, checking for liens or encumbrances, and evaluating the property’s condition through professional inspections.

- Statistics show that nearly 35% of property transactions experience delays due to issues found during due diligence.

4. Making an Offer

- Once you identify a property, it’s time to make an offer. Be prepared to negotiate, as most sellers may not accept the first offer.

- Many properties in popular cities receive multiple offers; thus, being flexible with your price can be beneficial.

5. Contract Phase

- After your offer is accepted, a preliminary contract is drawn up. This document outlines the terms of the sale and typically requires a deposit, which ranges from 5% to 10% of the purchase price.

- Understanding your rights and responsibilities during this phase is paramount to avoid future complications.

6. Finalizing the Sale

- In the final stages, your lawyer or notary will assist in drafting the deed of sale. Both parties will sign this document in the presence of a notary, officially transferring the property.

- On average, this process can take anywhere from 4 to 10 weeks, depending on the country’s regulations and specific circumstances.

Comparative Table of Key Steps

| Step | Description | Average Timeline |

|---|---|---|

| Initial Research | Narrow down location and budget | Ongoing |

| Engaging Professionals | Hiring agents and attorneys | 1-2 weeks |

| Due Diligence | Comprehensive checks on property and legal title | 3-4 weeks |

| Making an Offer | Negotiation process with seller | 1-2 weeks |

| Contract Phase | Drafting and signing of preliminary contract | 1-2 weeks |

| Finalizing the Sale | Signing the deed with a notary | 4-10 weeks |

Real-World Examples

- A couple looking to buy a vacation home in Tuscany engaged a local agent who introduced them to off-market properties, ultimately leading to a 10% price drop from the original asking price due to strategic negotiations.

- In another case, a buyer interested in a flat in Vienna encountered zoning and historical preservation restrictions. Due diligence revealed these issues early, allowing them to pivot to a different property without losing time.

Practical Implications for Buyers

- Always factor in potential additional costs such as property transfer taxes and notary fees, which can amount to an additional 7% to 10% of the purchase price.

- Stay organized throughout the process by maintaining a checklist of documents needed at each stage, such as proof of income, identity verification, and bank statements.

Paying close attention to these steps can greatly enhance your purchasing experience and lead to a successful property acquisition in Europe.