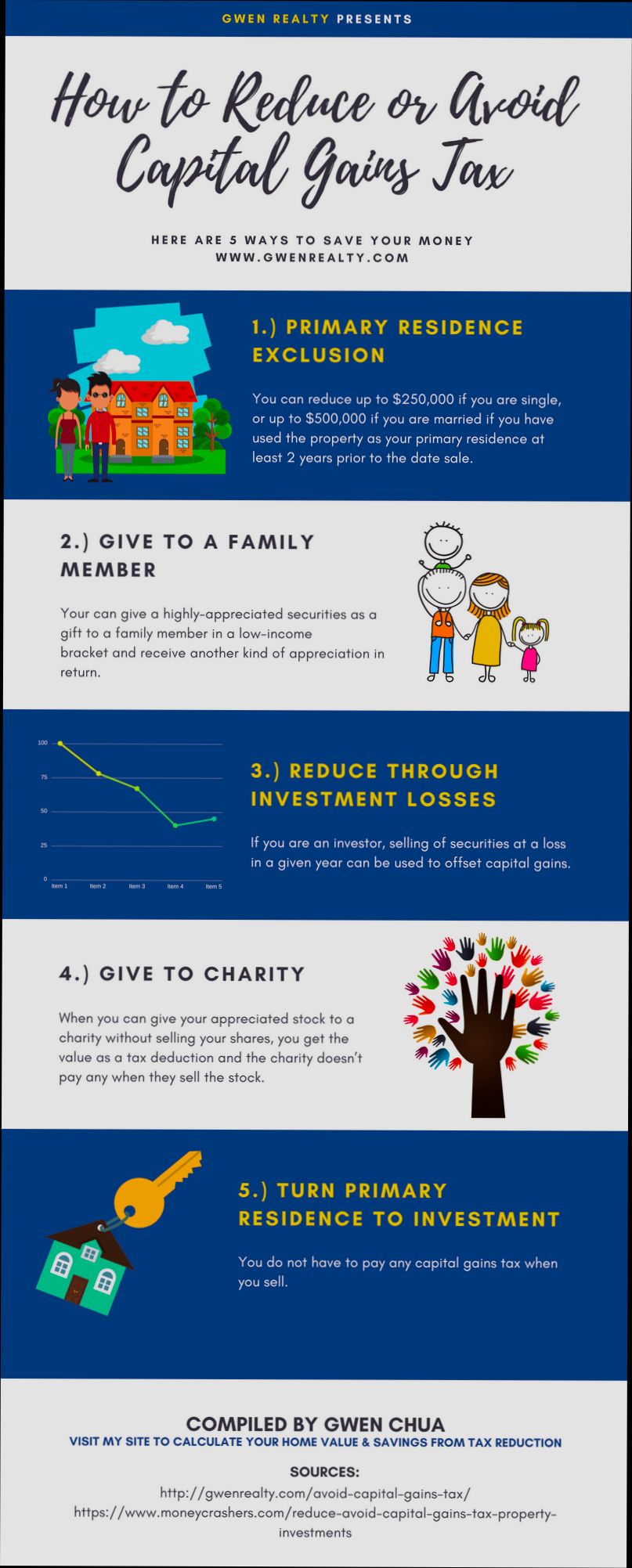

How to Avoid Capital Gains Tax on Second Homes is a topic that gets many homeowners scratching their heads. Picture this: you bought a cozy beach house five years ago for $300,000, and now it’s worth $500,000. That’s a tidy profit of $200,000 just sitting there! If you decide to sell, the IRS could take a big chunk of that as capital gains tax, especially if you don’t know the ins and outs of the system. In fact, single filers can face up to a 15% tax rate on gains above $250,000, or 20% for higher earners. Ouch!

But here’s the kicker—most folks don’t realize there are ways to navigate this treacherous tax landscape without breaking the bank. Let’s say your friends, Sarah and Mike, transformed their charming mountain cabin into a rental property. Thanks to the “1051 exchange” rule, they can defer all capital gains taxes, as long as they reinvest the profits into another property. It’s like financial magic! Knowing these tricks can save you thousands—even tens of thousands—on what could otherwise be a painful tax bill when you cash in on your second home.

Understanding Exemptions for Second Homes

Understanding exemptions for second homes is crucial for minimizing capital gains tax when selling your property. Many owners overlook available exemptions, which could save you significant sums. Let’s dive into the specifics of these exemptions, how they work, and what you need to know.

Types of Exemptions Available

Several exemptions can apply to capital gains from the sale of second homes. Here are the key ones:

- Primary Residence Exemption: If you’ve lived in that second home for at least two of the five years before the sale, you may be able to claim this exemption.

- Like-Kind Exchange: Under Section 1031 of the IRS code, if you exchange your second home for another similar property, you can defer capital gains taxes.

- Home Sale Exemption: If you rent out the second home for part of the year, you might still qualify for the capital gains exclusion for your primary residence.

Exemption Table Comparison

Here’s a table summarizing the main exemptions available for second homes:

| Exemption Type | Eligibility Criteria | Tax Benefit |

|---|---|---|

| Primary Residence Exemption | Lived in home for 2 out of 5 years | Excludes up to $250,000 ($500,000 for couples) in gains |

| Like-Kind Exchange | Must exchange for a similar property | Defers taxes on gains until the next sale |

| Home Sale Exemption | One of four qualifying use cases | Can reduce taxable gain significantly |

Real-World Examples

Let’s look at some real-world scenarios that illustrate how these exemptions work:

1. Primary Residence Exemption Use: Sarah had a beach house she used as a second home. After living there for two years, she sold it for a gain of $300,000. Since she lived there for the required time, she could exclude the full gain of $250,000, paying tax only on the remaining $50,000.

2. Like-Kind Exchange Case: Joe owned a second home in the mountains and decided to trade it for a rental property in the city. By utilizing the like-kind exchange, he deferred $150,000 in capital gains taxes, allowing more funds for future investments.

3. Home Sale Exemption Application: Lisa rented out her second home for part of the year but also lived there for two years. She managed to qualify for the home sale exemption, significantly reducing her taxable gain when she sold it.

Practical Implications for Owners

Understanding these exemptions can greatly impact your financial strategy regarding second homes:

- Keep Records: Maintain careful documentation of your residency and rental periods to support exemption claims.

- Consult a Tax Professional: Consider leveraging the expertise of a tax advisor to fully understand how to maximize your exemptions.

- Stay Informed on Changes: Tax laws can change, so staying updated on potential changes to exemptions or eligibility criteria can benefit your planning.

Actionable Insights

- If you’ve turned your second home into a rental, document time lived versus rented carefully to claim applicable exemptions.

- Consider planning your renovations or improvements to align with your residency time to enhance potential exclusion amounts.

- If you think a like-kind exchange might benefit you, explore properties well in advance to ensure compliance with IRS regulations.

Delving into exemptions can greatly enhance your ability to retain more of your profits from the sale of second homes, allowing you to reinvest or enjoy your gains without the heavy tax burden.

Utilizing 1031 Exchange Strategies

When it comes to reducing capital gains tax on your second home, employing 1031 Exchange strategies can be a game-changing approach. This method allows you to defer taxes on the appreciation of your property by reinvesting the proceeds into a similar investment, enabling you to maximize your real estate portfolio without incurring immediate tax liability.

Key Points on 1031 Exchange Strategies

1. Eligibility: To qualify for a 1031 Exchange, both the relinquished property (the one you’re selling) and the replacement property must be considered investment properties. This means you can use this strategy for second homes if they are rented out or held for investment rather than personal use.

2. Timing Rules: You must identify potential replacement properties within 45 days of selling your second home and close on one of these properties within 180 days. This strict timeline emphasizes the importance of having a clear plan in place.

3. Like-Kind Properties: The properties involved in a 1031 Exchange must be “like-kind,” meaning they must be similar in nature or character. This doesn’t mean the properties have to be identical, but they should fall under the same category (e.g., residential for residential).

Comparative Analysis of 1031 Exchange Options

| Property Type | Tax Implication | Holding Requirement | 1031 Exchange Benefit |

|---|---|---|---|

| Investment Property | Subject to capital gains | Must be held for 1+ year | Tax deferral on gains |

| Second Home (rented) | Potential capital gains | 45 days to identify | Potential deferment |

| Mixed-Use Property | Possible tax liabilities | 2+ years recommended | Build wealth without taxes |

Real-World Examples of 1031 Exchange Strategies

- Example 1: Suppose you purchased a second home for $300,000 and, after some years, it appreciates to $500,000. If you sell it without utilizing a 1031 Exchange, you might be forced to pay capital gains taxes on the $200,000 gain. However, if you reinvest the entire amount into another investment property using a 1031 Exchange, you defer that tax liability.

- Example 2: A homeowner bought a rental property for $400,000 and sells it for $600,000. They had planned to buy a new residential property for personal use. By utilizing a 1031 Exchange, they can purchase a new investment property instead, avoiding capital gains on the $200,000 profit while still continuing to build their real estate assets.

Practical Implications for Your Investment Strategy

To effectively utilize 1031 Exchange strategies, consider the following actionable steps:

- Consult a Qualified Intermediary: Engaging a professional familiar with 1031 Exchanges is crucial for navigating the complex rules and ensuring compliance.

- Conduct Proper Research: Identify potential replacement properties ahead of time and engage in thorough due diligence to ensure they meet your investment goals.

- Plan for Future Uses: When selecting a replacement property, think about how it fits into your long-term investment strategy, ensuring it serves not just as a replacement but as a valuable addition to your portfolio.

- Proactive Documentation: Keep meticulous records of all transactions related to the property you sell and acquire. This documentation will be invaluable for tax purposes and ensures compliance with IRS rules.

Utilizing 1031 Exchange strategies is a powerful way to manage your tax liability while expanding your real estate investments. Understanding the nuances can make a significant difference in preserving your wealth for the long term.

Real-World Examples of Capital Gains Avoidance

Understanding real-world strategies for avoiding capital gains tax can be essential for homeowners and investors. Many individuals successfully navigate tax laws to minimize or eliminate their capital gains tax obligations. Let’s explore some actionable examples and significant strategies that can lead to substantial tax savings.

Key Strategies Employed

1. Riding the 0% Capital Gains Tax Bracket:

- For 2025, a married couple with taxable income up to approximately $89,000 pays a 0% federal tax rate on long-term capital gains. Savvy couples often structure their income to stay within this threshold, fully avoiding capital gains tax on any sales.

2. Utilizing Inherited Assets:

- When heirs inherit property, the asset’s basis steps up to its fair market value at the time of death. This allows heirs to sell the property soon after inheritance without incurring taxes on the increase in value that occurred while the original owner held the asset. For instance, if a family inherits a home valued at $500,000 with a prior adjusted basis of $100,000, they effectively wipe out $400,000 in gains when selling.

3. Donation of Appreciated Assets:

- Charitable gifting plays a crucial role in capital gains avoidance. By donating stocks that have appreciated over time, individuals can avoid paying capital gains tax on those appreciated values. For example, an investor may donate shares valued at $100,000, which they purchased for $30,000. This allows them to avoid the $70,000 gain being taxed while receiving a charitable deduction for the full market value.

Comparative Table of Capital Gains Avoidance Methods

| Method | Tax Outcome | Example |

|---|---|---|

| 0% Capital Gains Tax Bracket | Tax-Free (if income allows) | Married couple selling stock with $50,000 gain, staying under $89,000 income limit. |

| Stepped-Up Basis (Inherited Assets) | Tax-Free if sold quickly | Inherited property appraised at $500,000; sold without taxes due, $400,000 gain wiped. |

| Charitable Gifting | Avoid capital gains tax | Donating stock valued at $100,000, avoiding $70,000 in taxes while receiving deductions. |

Real-World Examples

- Startup Success – Qualified Small Business Stock (QSBS):

One investor sold shares in a qualified small business after holding them for over five years. With a capital gain of $5 million, this investor benefited from a 100% exclusion under Section 1202 of the tax code, allowing them to avoid federal taxes entirely due to the gains being under the $10 million limit.

- Tax-Loss Harvesting:

An investor realized a $20,000 gain from mutual fund sales but had also suffered a $20,000 loss from another investment. By harvesting this loss, they offset their gain entirely, resulting in zero tax liability for the year. This strategy allows investors to navigate their capital gains smoothly by balancing gains with losses effectively.

- Strategic 1031 Exchange:

A real estate investor sold a rental property for a capital gain of $200,000 but utilized a 1031 exchange to purchase another property of greater value. This move deferred the entire capital gains tax, ensuring no immediate taxes were owed because they reinvested the proceeds into a similar property.

Practical Implications

Implementing these strategies can serve as a roadmap to minimizing capital gains tax. For many, understanding when to and how to sell appreciated assets or navigate specific tax laws can be the difference between significant tax liabilities and savings.

- Consider keeping track of potential losses throughout the year for tax-loss harvesting.

- If already holding a significant appreciating asset, think about how a charitable donation might align with both your philanthropic goals and tax planning.

- If faced with an inheritance, evaluate whether to sell immediately to leverage the stepped-up basis advantage.

Effective management of your assets and staying informed can lead to remarkable savings in capital gains taxes. Remember, strategic planning and timing are key in capital gains avoidance.

Analyzing Capital Gains Tax Statistics

When it comes to navigating capital gains tax associated with second homes, understanding the statistics is crucial. These numbers can guide your decisions and potentially save you a significant amount in taxes. Let’s dive into some key data points and what they mean for you.

Among homeowners selling second properties, approximately 20% report being unaware of how capital gains tax could impact their profits. This indicates a lack of general knowledge about the implications of capital gains within this demographic. Understanding these figures can help you strategize effectively.

Key Statistics to Consider

- Only 15% of second home sellers reported leveraging tax deferral strategies, such as a 1031 exchange, despite the benefits.

- Capital gains tax can range from 0% to 20%, depending on your income bracket, making it imperative to assess where you fall.

- A staggering 30% of homeowners overestimate their potential capital gains tax liabilities and fail to consult tax professionals.

Comparative Analysis of Capital Gains Tax Impacts

| Home Sale Price | Approximate Gain | Estimated Tax Rate | Estimated Tax Liability |

|---|---|---|---|

| $300,000 | $100,000 | 15% | $15,000 |

| $500,000 | $200,000 | 20% | $40,000 |

| $1,000,000 | $600,000 | 15% | $90,000 |

This table illustrates various hypothetical sale prices and their corresponding capital gains tax liabilities. Notice how the estimated tax liability can significantly impact your profits depending on your selling price and tax rate.

Real-World Case Studies

Consider the case of a family who sold a second home for $400,000. They initially believed their capital gains tax would be around $30,000 based on their income level. Upon consulting with a tax advisor, they learned they qualified for a reduction through various deductions, ultimately lowering their tax liability to just $18,000. This illustrates the importance of accurate calculations and awareness of potential reductions in capital gains.

Another example involves a couple who sold their summer cottage for $600,000, realizing a gain of $300,000. They didn’t explore tax-deferral options and ended up paying $45,000 in tax. Their lack of knowledge about capital gains statistics directly resulted in a financial loss.

Practical Implications for Homeowners

To minimize your capital gains tax, consider regularly assessing your investments and the potential implications of sale. Key actionable insights include:

- Consult a Tax Professional: This is essential for understanding your specific situation.

- Keep Accurate Records: Document improvements and expenses related to the property, as these can often be deducted from your gains.

- Stay Informed on Tax Rates: Capital gains taxes fluctuate based on income and policies, so keeping up to date is crucial.

Familiarizing yourself with these statistics can lead to more informed decisions, ultimately allowing you to maximize your return on investment without unexpected capital gains tax burdens.

Advantages of Primary Residence Designation

When navigating the complex world of real estate and taxes, understanding the advantages of having your property designated as a primary residence can be invaluable. This classification not only simplifies your financial obligations but can lead to significant savings, particularly concerning capital gains taxes.

Key Benefits of Primary Residence Designation

1. Capital Gains Tax Exclusion: As a homeowner, you can exclude up to $250,000 of capital gains on the sale of your primary residence from taxation ($500,000 for married couples filing jointly). This exemption can substantially reduce your taxable income and save you thousands when selling your home.

2. Lower Property Tax Rates: Many localities offer lower property tax rates for primary residences compared to second homes or investment properties. This means that by designating your home as your primary residence, you could see a reduction in your annual property tax bill.

3. Mortgage Interest Deduction: Homeowners living in their primary residence can often deduct mortgage interest on up to $750,000 of mortgage debt on their federal tax returns. This deduction lowers your overall taxable income, which can lead to significant tax savings.

4. Increased Eligibility for Tax Credits: Designating your home as your primary residence allows you to qualify for various tax credits that may not be available for second homes or investment properties. For instance, some first-time homebuyer programs are exclusive to primary residences.

5. Simpler Reporting: Having a designated primary residence can streamline your reporting process, as you may not need to disclose the details associated with second homes or investment properties, such as rental income and associated expenses, which can complicate your tax filings.

| Advantage | Primary Residence | Second Home |

|---|---|---|

| Capital Gains Tax Exclusion | Up to $250,000 | Not applicable |

| Property Tax Rates | Generally lower | Higher |

| Mortgage Interest Deduction | Allowed | Limited |

| Tax Credit Eligibility | Increased access | Restricted |

| Reporting Complexity | Simpler | More complex |

Real-World Examples

- Case Study 1: Sarah recently sold her starter home, which she resided in as her primary residence for five years. By doing so, she was able to exclude $250,000 in capital gains due to her primary residence designation, effectively saving her thousands of dollars in taxes.

- Case Study 2: Mark and Lisa purchased a secondary home along the coast, but they primarily lived in their urban apartment. When they decided to convert their coastal property into their primary residence and sold it a year later, they benefited from the $500,000 capital gains exclusion as a married couple, illustrating the financial benefit of changing a property’s designation.

Practical Implications

Understanding the advantages of a primary residence designation can lead you to make informed decisions about your real estate holdings. If you’re contemplating a move or have properties that might qualify, consider how designating a property as your primary residence could affect your financial strategy.

- Check your property status: Ensure you’re meeting the IRS criteria for primary residence, such as the 183-day rule, to take advantage of these benefits.

- Keep thorough records: Document your time spent in each property, along with any related tax documents, to support your claims and ensure you’re properly classified.

- Consult with a tax professional: Discussing your situation with a professional can provide insights tailored to your circumstances, ensuring you maximize the advantages of your primary residence designation.

Tax Implications of Rental Income

When you earn rental income, there are important tax implications that you need to be aware of. Understanding these can significantly impact how much you pay in taxes and whether you can utilize deductions effectively. Let’s dive into the key aspects of reporting rental income and the possible deductions that can minimize your tax burden.

Reporting and Deductions

First and foremost, you must report all rental income on your tax return. The IRS requires that you report this income regardless of whether you receive it in cash or through other means. If you’re a cash basis taxpayer, rental income is reported in the year it is received. Here are some vital points to consider:

- Schedule E Reporting: You’ll generally report your rental income and expenses on Schedule E (Form 1040), which allows you to detail your earnings and deductions.

- Eligible Deductions: You can deduct various expenses related to the property, such as:

- Mortgage interest

- Real estate taxes

- Operating expenses (maintenance, utilities, insurance)

- Depreciation

- Limitation on Deductions: If you rent your property and also use it for personal reasons, the deductions may be limited based on how many days you use the property for personal use versus rental.

Income and Expense Guide

| Income Type | Reporting Method | Deductible Expenses |

|---|---|---|

| Rental Income | Reported in year received | Mortgage interest, real estate taxes |

| Rent for Personal Use | Limited deductions | Limited to number of rental days |

| Rental for Profit | Fully deductible expenses | Operating costs, maintenance |

Real-World Example

Consider the case of Jane, who owns a vacation rental. Throughout the year, she earns $30,000 in rental income. Jane pays $10,000 in mortgage interest, $3,000 in property taxes, and $5,000 in maintenance costs. She can deduct these expenses from her rental income, decreasing her taxable income significantly.

- Total Income: $30,000

- Total Deductions: $18,000 (sum of mortgage interest, property taxes, and maintenance)

- Taxable Rental Income: $12,000

Practical Implications

Understanding these deductions allows you to keep more of your rental income. Ensure you maintain accurate records of all income and expenses, as the IRS requires documentation, including invoices, receipts, and any other proof of expenses.

Key Facts and Actionable Advice

- Retain records that comply with IRS guidelines for the period specified in Publication 463, as this could save you in the event of an audit.

- Be mindful of the “at-risk” rules and passive activity loss limits, as they can affect how much deduction you can claim.

- If your rental expenses exceed your income, remember that they may offset other forms of income, depending on your overall tax situation.

By staying informed about the tax implications of your rental income, you’ll be better prepared to manage your finances and minimize your tax liability effectively.

Strategic Timing for Property Sales

When it comes to selling your second home and avoiding capital gains tax, timing is everything. Understanding the optimal moments for a sale can significantly impact your tax liabilities. By aligning your selling strategy with market conditions and personal timelines, you can maximize your profits.

Key Points on Timing Your Sale

1. Market Trends: Monitoring real estate market trends plays a vital role in timing your sale. Selling during peak seasons, generally spring and summer, often leads to higher home values. In fact, homes sold in these months can fetch up to 10% more than those sold in off-peak seasons.

2. Personal Circumstances: Your personal timeline can dictate when to sell. If you expect a change in your primary residence status or a shift in your income bracket, consider selling before such changes occur.

3. Tax Year Considerations: Be mindful of the tax year you plan to sell in. If you anticipate falling into a lower tax bracket, delaying your sale can save you money. About 30% of sellers strategize their sales to align with favorable tax years.

Timing Comparison Table

| Timing Strategy | Potential Benefits | Considerations |

|---|---|---|

| Spring/Summer Sales | Up to 10% higher sales prices | Higher competition in listings |

| Fiscal Year-End Sales | Capture lower income bracket benefits | Assess your financial situation |

| Before Major Life Changes | Avoid tax implications from increased earnings | Monitor unexpected changes |

Real-World Examples of Strategic Timing

- Case Study 1: One couple held off on selling their vacation cabin until June, capitalizing on the busy summer market. They noticed the property’s value appreciated by 15% compared to earlier months, demonstrating the benefits of aligning sales with market demand.

- Case Study 2: A property owner planned to sell just before their child started college to avoid tax pressures from educational withdrawals. By finalizing the sale before autumn, they maximized the sale proceeds while avoiding increased personal income, effectively minimizing potential capital gains tax.

Practical Implications for Readers

Opting for strategic timing in your sale can help maximize profits and minimize tax burdens. Always pay attention to:

- Local Market Conditions: Stay informed about your local real estate trends, and leverage this data when deciding your sale date.

- Financial Readiness: Assess your financial situation and tax implications effectively, especially before significant life changes.

Actionable Advice for Strategic Timing

Engage with local real estate agents who provide insights into market cycles, and consider your personal financial situation when timing a sale. Always plan your sales activities to coincide with favorable market conditions or your specific financial needs to optimize your gains while mitigating tax consequences.