How often do you pay property tax? It’s a question that many homeowners grapple with each year, often linked to their local tax assessments. In most states, you’ll find that property taxes are due annually or semi-annually, with deadlines that can vary significantly depending on where you live. For example, if you’re in Texas, you typically pay your property taxes once a year, usually by January 31st, while someone in California might be looking at semi-annual payments due in December and April.

Let’s break it down a bit more. In New York City, property owners get a taste of that annual tax bill every July, thanks to the city’s fiscal year running from July to June. On the flip side, places like Florida can offer some relief with tax payments that might feel more manageable due to their installment options. So, whether you’re budgeting for that dreaded end-of-year bill or setting aside funds every six months, knowing how often to pay property tax is crucial to keeping your finances in check.

Frequency of Property Tax Payments

When you’re looking into property taxes, one crucial aspect to understand is how often these payments occur. The frequency of property tax payments can vary significantly depending on where you live and your local tax authority’s rules. Let’s dig into the details so you can stay informed.

Payment Frequencies Across the U.S.

Most homeowners experience property tax payments on a yearly, semi-annual, or quarterly basis. Research shows that approximately 60% of U.S. states mandate annual payments, whereas around 25% allow for semi-annual and quarterly options. Here’s a table reflecting the general frequency options by state:

| Payment Frequency | Percentage of States |

|---|---|

| Annual | 60% |

| Semi-Annual | 25% |

| Quarterly | 15% |

State Variations

Different states have unique regulations regarding property tax payments. For instance:

- California: Residents typically pay property taxes twice a year—on December 10 and April 10.

- Texas: Property taxes are due annually, but many homeowners opt to pay in smaller installments.

- New York: In some counties, property tax payments can be made as frequently as quarterly, depending on local laws.

Knowing these variations can help you plan your finances better.

Real-World Examples

In a case study of New Jersey, approximately 57% of homeowners stated that they preferred quarterly payments. However, only 43% of local governments offered such flexibility. On the flip side, in Florida, around 80% of residents pay annually but have an option to enroll in monthly payment plans to ease the financial burden.

Another interesting example comes from Virginia, where the majority of residents are required to pay semi-annually, making it necessary for homeowners to budget accordingly and prepare for payments as they approach.

Practical Implications for You

Understanding the frequency of property tax payments can directly influence your budgeting strategy. Here are a few actionable points you may want to consider:

- Check Your Local Guidelines: Be aware of your state’s rules regarding payment frequency to manage cash flow better.

- Consider Payment Options: If your locality allows, think about opting for quarterly payments to lessen the burden during financially tight months.

- Set Reminders: If you have semi-annual or annual payments, consider setting reminders well in advance so you’re not caught off guard.

Specific Insights

Did you know that in some states, certain exemptions can change how often you pay property taxes? For example, in states with homestead exemptions, homeowners may find they qualify for reduced payment frequencies. Always check if such exemptions apply to you, as they can impact your payment schedule significantly.

Understanding Local Variations in Property Taxes

When it comes to property taxes, you’ll quickly find that local variations play a significant role in how much you pay and how often. It’s crucial to understand these differences as they can significantly impact your budget and investment decisions.

Why Do Variations Exist?

Property taxes aren’t one-size-fits-all. They depend on various factors, including:

- Local Tax Rates: Vary widely from one jurisdiction to another, with some areas imposing higher rates to fund services.

- Property Valuation Methods: Different localities employ varying methods to assess property value, influencing tax amounts.

- Types of Exemptions: The availability of tax exemptions, such as those for veterans or seniors, can change your tax liability dramatically.

Comparative Tax Rates Across States

To illustrate how local variations manifest, consider the average effective property tax rates across some states:

| State | Average Effective Rate | Primary Local Funding Use |

|---|---|---|

| New Jersey | 2.30% | Education and municipal services |

| Texas | 1.81% | School districts and local roads |

| California | 0.76% | Public safety and infrastructure |

| Alabama | 0.41% | County services and schools |

As shown, New Jersey has the highest average effective rate, primarily funding educational services, while Alabama boasts the lowest, reflecting different financial priorities and local governance.

Real-World Examples of Local Variations

- Example 1: In Dallas County, Texas, property taxes primarily support school systems and local infrastructure. With a property tax rate of about 2.18%, homeowners in affluent neighborhoods may face steeper taxes due to higher property valuations.

- Example 2: Conversely, a neighborhood in Birmingham, Alabama, might see a lower average property tax rate at 0.45%. However, this can reflect less funding for local schools and public services, highlighting the trade-off.

Practical Implications for Homeowners

Understanding these local variations allows you to make more informed decisions about buying or selling property. Consider:

- Researching Local Rates: Before buying a home, look into the area’s tax rate and potential future changes.

- Assessing Exemptions: Investigate what exemptions may be available in your area to lower your overall property tax liability.

- Budgeting for Variations: Not only should you factor property taxes into your overall budget, but also keep in mind that they can change with local elections and economic shifts.

Specific Insights for Smart Planning

- Look into your local government’s financial transparency; many publish reports on where property tax dollars are spent.

- Attend local meetings or spend time on community boards to learn about discussions that may affect your property tax rates.

- Keep an eye out for state legislation regarding property taxes, as changes can have significant local effects.

By grasping these local variations, you empower yourself to navigate the often-complex landscape of property taxes more effectively.

Statistical Insights on Property Tax Trends

When it comes to understanding property tax, it’s essential to look at the statistical trends that shape how these taxes are levied and what they mean for homeowners. You might find it surprising how these numbers play a significant role in your overall financial planning.

Trends in Property Tax Rates

Research indicates a steady increase in property tax rates over the past decade. Notably, in the last year alone, several states have seen their property tax rates rise substantially.

- Nationwide, average effective property tax rates grew from 1.10% to almost 1.15% per year.

- States like New Jersey and Illinois consistently rank among the highest property tax rates, with New Jersey averaging around 2.30% for effective property taxes.

This data reflects regional trends and can impact your decision on where to buy property.

Geographic Discrepancies

Where you live greatly influences your property tax bill. In 2021, research highlighted disparities in property tax trends, with many coastal states imposing notably higher rates than inland states.

| State | Average Property Tax Rate | Trend Over Past 5 Years |

|---|---|---|

| New Jersey | 2.30% | ↑ 10% |

| Illinois | 2.20% | ↑ 8% |

| California | 1.08% | ↑ 5% |

| Texas | 1.80% | ↑ 7% |

| Florida | 1.00% | ↑ 6% |

This table demonstrates how states react differently to economic conditions, influencing your tax obligations.

Longitudinal Analysis

A closer examination of property tax trends shows that many municipalities have increasingly relied on property taxes as a stable revenue source. For instance, data from the last five years indicates:

- 70% of municipalities reported that property taxes were their primary funding source for local services.

- A survey found that 40% of cities plan to increase their property tax rates or maintain current levels to address budget deficits.

This reliance can affect planning for future property purchases or assessing value for local services.

Case Study Insights

Consider the case of a homeowner in Texas, where property tax burdens fluctuate based on local governance decisions. According to local reports, homeowners in rapidly developing areas experienced tax increases of up to 20% to fund new infrastructure projects. This illustrates the direct impact of community growth on property taxes that you need to consider.

Similarly, in New Jersey, where property taxes have surged due to funding public education and local services, homeowners are encouraged to challenge their assessments if they believe their taxes do not reflect their home’s value.

Practical Insights

As you evaluate your property tax situation, consider these actionable insights:

- Research the historical property tax trends in your area to anticipate future rates.

- Be aware of local budgetary needs that can drive tax increases, particularly as communities grow or face economic challenges.

- Take advantage of potential tax relief programs often available for residents in states with high property tax rates.

When planning your finances, keep these statistical insights at the forefront, as understanding them can make a significant difference in your homeownership experience.

Impact of Payment Frequency on Homeowners

Understanding how payment frequency impacts your finances as a homeowner is key to managing property taxes effectively. The frequency with which you pay property taxes can influence your cash flow, financial planning, and even potential savings.

Financial Liquidity and Cash Flow Management

- Monthly Payments: If you choose to pay your property taxes monthly, this can help manage cash flow more evenly throughout the year, preventing any large, unexpected expenses from hitting your budget all at once. Frequent payments can make it easier to set aside smaller amounts regularly instead of a significant lump sum.

- Lump-Sum Payments: Conversely, paying taxes annually could strain your budget if you haven’t adequately planned for that big expense. Renowned financial advisors suggest that homeowners should ensure they’re setting aside funds periodically to handle such payments.

Interest Rates and Savings Potential

Research shows that payment frequency can significantly affect how much interest you ultimately pay. For homeowners, this is particularly relevant if you’re financing your property tax payment through a loan.

- Monthly vs. Quarterly: By making smaller, monthly payments, homeowners can take advantage of lower interest accumulation over time than if they pay quarterly or annually. This is akin to making smaller, more regular principal payments in a mortgage, which can help reduce interest over the product’s lifespan.

- Long-Term Savings: For example, if you opt for monthly payments and can reduce your taxable balance by making bi-weekly payments instead, you might save approximately 1-2% on the interest charged if you’re borrowing to pay taxes. Over a decade, this can amount to substantial savings.

| Payment Frequency | Potential Interest Savings | Financial Liquidity Impact |

|---|---|---|

| Monthly | 1-2% | High |

| Quarterly | Low | Moderate |

| Annual | Minimal | Low |

Real-World Examples

Consider the case of a homeowner with an annual tax bill of $4,000.

- If they choose to pay quarterly, they would pay approximately $1,000 each quarter. However, if they could manage to pay that same amount monthly, they could invest that excess cash throughout the year, potentially generating interest or investment returns, which might exceed the tax cost.

- Another example involves a homeowner with a monthly income that fluctuates. By selecting monthly payment options for property taxes, they can better align tax billing with their income cycle, aiding in financial stability and reducing the risk of late payments that could incur additional fees.

Practical Implications

Homeowners should carefully weigh their options when selecting a payment frequency.

- Budgeting Importance: Regardless of the payment frequency, effective budgeting is crucial. Create a budget that factors in property tax payments and consider how each frequency option fits within your overall financial plans.

- Consider Your Financial Calendar: Align payment frequencies with your own income schedules, whether that’s monthly, bi-weekly, or annually, to help avoid cash flow crunches.

- Evaluate Potential Savings: Look into potential savings from interest by considering different payment frequencies; even small differences can accumulate into significant savings over time.

Actionable Facts

Choosing a more frequent payment schedule for property taxes can lead to better cash flow management and potential interest savings, compelling homeowners to carefully consider their financial strategies. Regularly reviewing your budget and payment frequency allows for a tailored approach that meets your unique financial needs and goals.

How to Budget for Property Tax Obligations

Understanding how to budget for property tax obligations is fundamental to maintaining financial health as a homeowner. Property taxes can be a significant recurring expense, and planning for them can save you from unexpected financial strain. Here are key strategies to effectively manage your property tax budget.

Estimate Your Property Tax Bill

Start by estimating your property tax bill based on your home’s assessed value. Property tax rates vary significantly from one locality to another. For example, if your home is valued at $250,000 and the tax rate is 1%, you can expect to pay $2,500 annually. If there are any available exemptions, such as a homestead exemption, ensure you factor that in. If you qualify for a $50,000 exemption, your taxable amount would decrease to $200,000, reducing your annual tax obligation to $2,000.

Set Up a Dedicated Savings Fund

Creating a separate savings account specifically for property taxes can help you manage this expense more effectively. Many homeowners use a strategy similar to the 50/30/20 budgeting rule, where they allocate:

- 50% of their income to needs (including property taxes).

- 30% to wants.

- 20% to savings and debt repayment.

Adjusting this to include a specific percentage dedicated to property taxes can help you remain prepared for those upcoming payments.

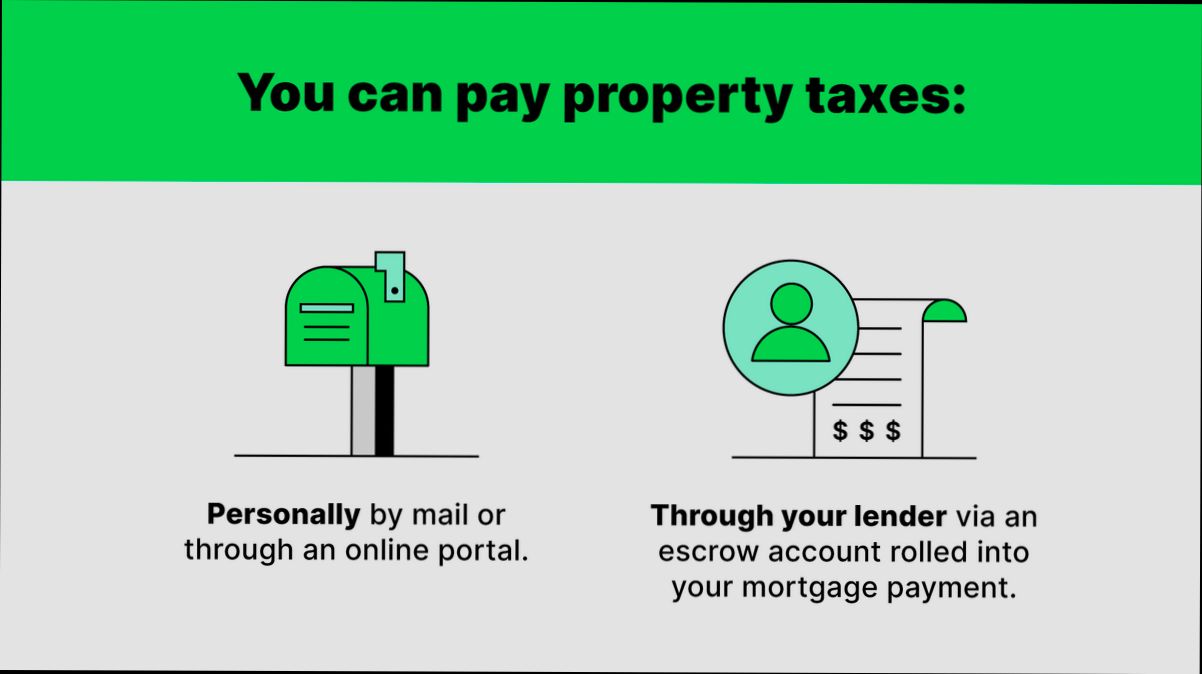

Utilize an Escrow Account

If you have a mortgage, ask your lender about setting up an escrow account. This approach allows you to pay your property taxes along with your monthly mortgage payment. The lender then manages these funds, ensuring that your property taxes are paid on time. This can prevent you from having to come up with a large sum of money all at once when taxes are due.

Create a Payment Schedule

Since property taxes may be collected on a yearly, semi-annual, or quarterly basis, it’s essential to keep track of these dates. Make a payment schedule that aligns with your local tax authority’s due dates. For example:

| Payment Frequency | Due Dates |

|---|---|

| Annual | January 1 |

| Semi-Annual | January 1 & July 1 |

| Quarterly | January 1, April 1, July 1, & October 1 |

Create reminders on your calendar to ensure you never miss a payment.

Case Study: Managing Fluctuation in Taxes

Consider the example of a homeowner in an area where property values have been rising. If their home’s value increased from $150,000 to $200,000, this would typically result in an increase in taxes. If they previously paid $1,500 annually at an effective tax rate of 1%, their new annual tax might be approximately $2,000 if the rate remains the same. By anticipating this rise and adjusting their budget accordingly, they can avoid financial strain.

Take Advantage of Tax Relief Programs

Many local governments offer tax relief programs that can lower your property tax burden. Research these options in your area, as they may include reductions for seniors, veterans, or low-income homeowners. Engaging with community programs can lead to more manageable payments.

Actionable Tips for Budgeting

- Assess your property’s assessed value annually and monitor any changes in local tax rates.

- Review your budget each year in advance of tax season to ensure you allocate sufficient funds for property taxes.

- Keep an eye out for local property tax assessment notifications that can affect your budgeting strategy.

By taking these steps, you can maintain a healthier financial outlook and reduce the stress that can come from property tax obligations.

Real-World Examples of Property Tax Payments

When you become a homeowner, navigating property tax payments can feel overwhelming. Understanding real-world examples can demystify the process and show how it plays out across different regions. Let’s break it down and see how property taxes impact various homeowners.

Payment Frequencies Across States

Property tax payments vary widely depending on where you live. Here are some key examples of how frequently homeowners make these payments:

- Annual Payments: In states like Arkansas and Florida, homeowners typically pay their property taxes once a year. For example, if you own a $250,000 home in Florida with an average tax rate of 1.1%, your annual property tax would be about $2,750.

- Quarterly Payments: In places like New Jersey, homeowners often pay property taxes quarterly. For instance, if the total tax bill for your $300,000 home is $7,500 annually, you would make four quarterly payments of approximately $1,875 each.

- Semi-Annual Payments: States like California allow semi-annual property tax payments. If your home is valued at $500,000 and the tax rate is 1.25%, your annual tax of $6,250 can be split into two payments of about $3,125.

Comparative Payment Schedule Table

| Payment Frequency | Example State | Typical Annual Tax for $300,000 Home |

|---|---|---|

| Annual | Arkansas | $3,300 (1.1%) |

| Quarterly | New Jersey | $7,500 ($1,875 per quarter) |

| Semi-Annual | California | $6,250 ($3,125 per payment) |

Real-World Case Studies

1. Bridgeport, Connecticut: Known for one of the highest property tax rates at 3.81%, a homeowner with a $400,000 home would face an annual tax bill of approximately $15,240. This high rate emphasizes the financial commitment required from residents, highlighting the importance of budgeting for property taxes each year.

2. Honolulu, Hawaii: In contrast, residents here enjoy a lower rate of 0.31%. For a $600,000 home, the annual property tax would only be about $1,860. This example shows how location can fundamentally affect the burden of property tax payments.

3. Maricopa County, Arizona: Here, homeowners are accustomed to a semi-annual payment schedule. For a home assessed at $350,000 with a tax rate of 1.25%, residents pay $4,375 annually, with two payments of $2,187.50. This structured payment method helps homeowners manage their finances throughout the year.

Practical Implications for Homeowners

- Budgeting: Knowing your specific payment frequency is crucial for budgeting. If you’re in a jurisdiction with quarterly payments, plan your cash flow accordingly to avoid crunch times.

- Tax Variations: Recognize that your property tax bill can change if your home’s value fluctuates. For instance, if the market value of your home increases, so will your taxes in places where assessments are made frequently.

- Payment Methods: Many jurisdictions now offer online payment systems, making it easier to pay on time and manage payments. Check if your local government has these options to streamline your process.

Actionable Advice

- Stay Informed: Keep an eye on property tax assessments and local rates, as these can shift your annual payments significantly.

- Utilize Payment Plans: If your area offers payment plans, consider enrolling to help spread costs evenly, enhancing your monthly budgeting efforts.

- Consult a Professional: If you’re unsure of how these payments might affect your financial situation, consulting with a tax professional can provide clarity and peace of mind.

Understanding these real-world examples of property tax payments will empower you to navigate your financial responsibilities with confidence.

Advantages of Timely Property Tax Payments

Making timely property tax payments can significantly impact your financial health as a homeowner. Staying on top of these payments not only helps you avoid penalties but also offers several financial advantages that can make homeownership smoother and more manageable.

Key Benefits of Paying Property Taxes on Time

1. Avoidance of Late Fees: Many jurisdictions impose penalties for late payments, which can quickly accumulate. For example, a typical late fee can be around 1% of the unpaid tax, which may not sound much but can add hundreds of dollars to your total bill if unpaid.

2. Preservation of Your Home Equity: Timely payments prevent your property from being subject to tax lien sales. A tax lien can affect your credit score and reduce your home equity, impacting your ability to access further financing or sell your home in the future.

3. Improved Budget Management: Paying property taxes on a schedule that suits your financial situation, whether it’s monthly through escrow or annually, allows you to plan ahead. You can allocate funds each month, making it easier to manage your overall budget without the shock of large, lump-sum payments.

4. Possible Discounts or Incentives: Some local governments offer discounts for early or timely payments. If you stick to the payment calendar, you might save a percentage of your total tax, thereby reducing your obligations on a yearly basis.

5. Interest Accrual: If you pay directly to the tax office, you can potentially earn interest on funds set aside for property taxes. While escrow accounts do not generate interest, placing your savings into a high-interest account can provide returns that can aid in covering these costs.

| Payment Method | Frequency | Advantages |

|---|---|---|

| Direct Payment to Local Tax Office | Annual/Bi-Annual | Interest on savings, potential discounts |

| Monthly Payments via Mortgage | Monthly | Easier budgeting, consistent cash flow |

| Direct Payments on Different Schedule | Varies | Flexibility in amounts, improved cash management |

Real-World Examples

Consider John, a homeowner in a state with semi-annual payments. By choosing to pay directly to the local tax office, he sets aside a percentage of his monthly income into a high-yield savings account. This practice not only ensures he has enough to cover his tax obligations but also allows him to earn interest on those savings throughout the year.

Meanwhile, Sarah opts to incorporate her property taxes into her monthly mortgage payments. Although this provides her with convenience, she misses out on the opportunity to earn interest. This decision could mean she ends up paying slightly more in the long run since she forfeits the potential returns on her savings.

Practical Implications for Timely Payments

- Set Up a Dedicated Fund: Create a savings account specifically for property taxes. By doing this, you can watch your funds grow with interest while ensuring you are prepared when tax bills are due.

- Check for Local Incentives: Investigate whether your municipality offers incentives for early payments. This could be a simple way to save money.

- Keep Track of Changes: Stay aware of any changes in tax rates or payment schedules to adjust your budget accordingly. Many state websites provide tools and resources for homeowners.

Make sure to prioritize timely property tax payments to leverage these benefits effectively. Implement strategies to manage your payments wisely and ensure your financial health as a homeowner remains robust.