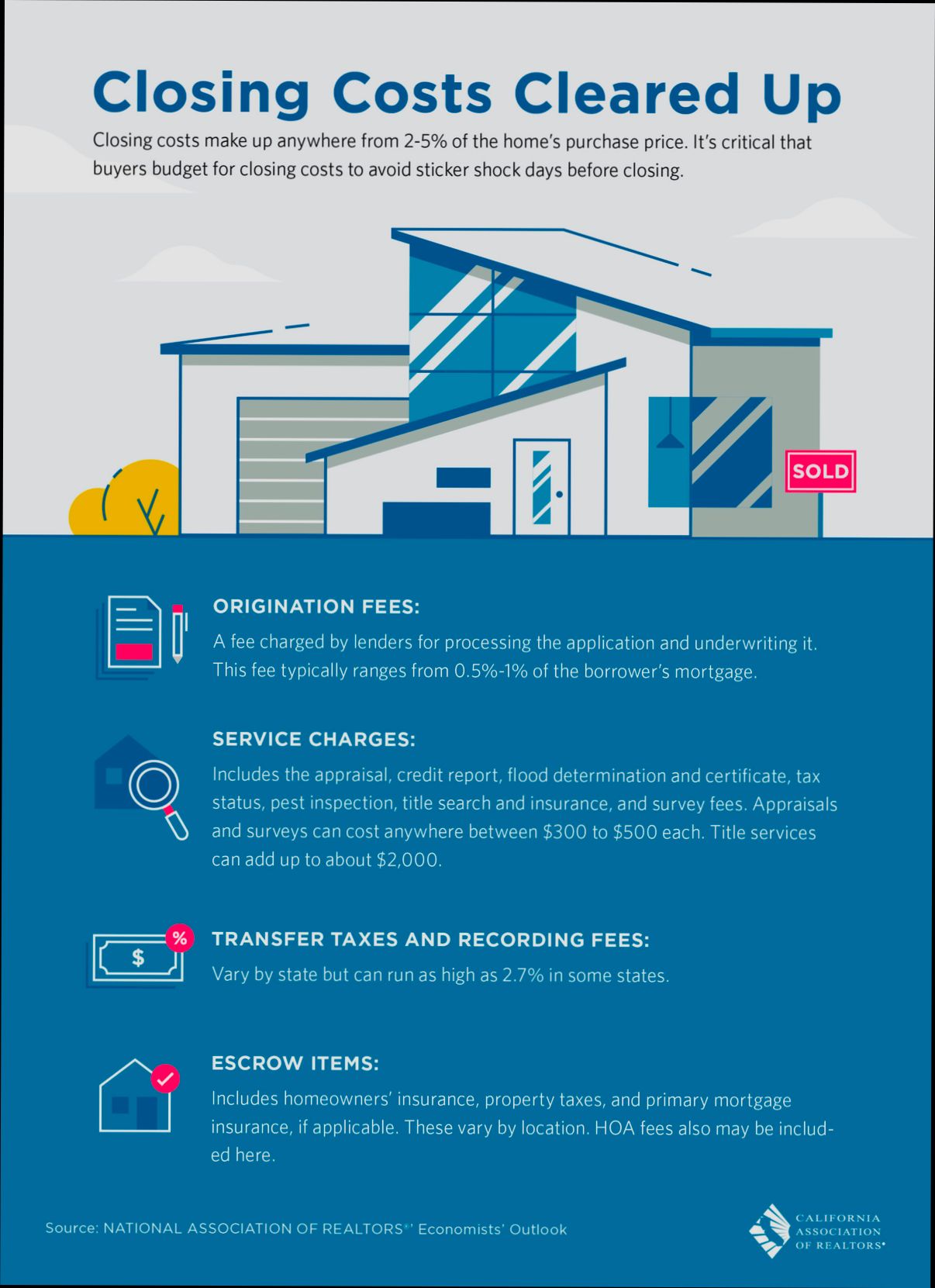

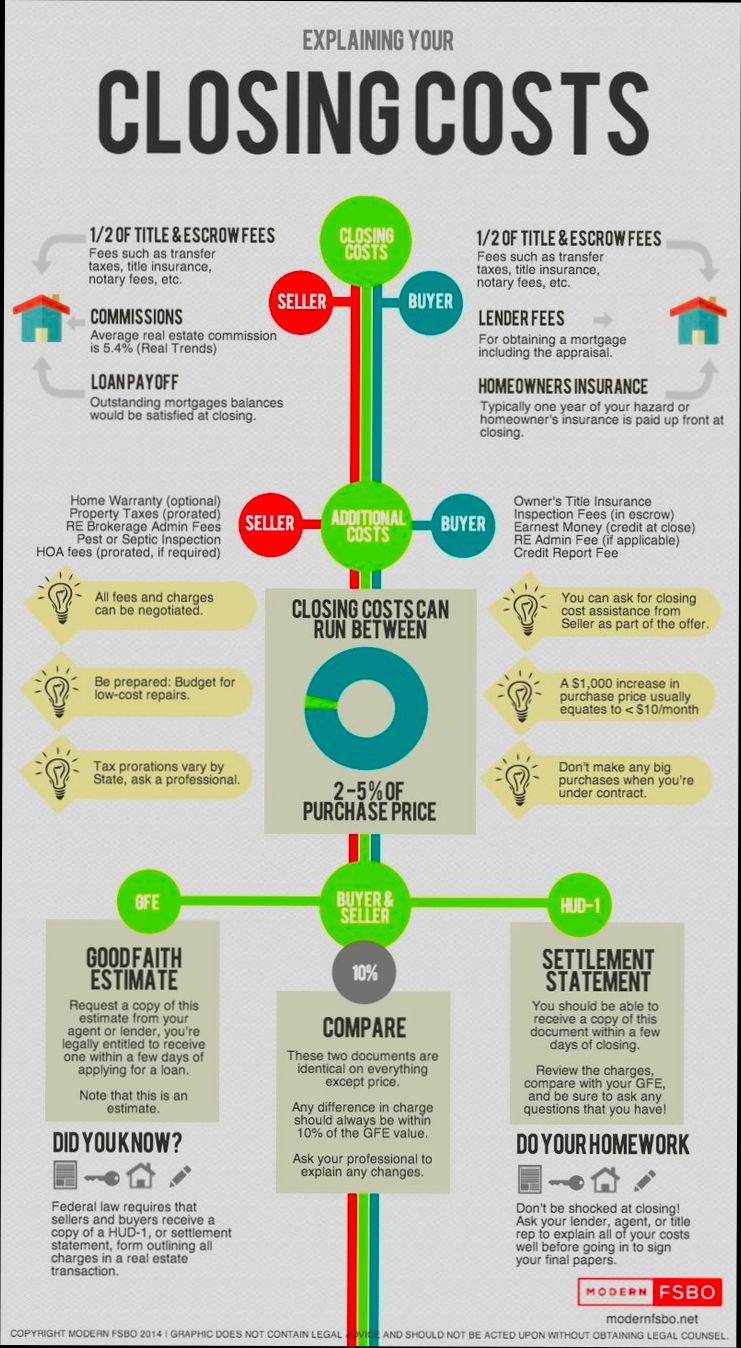

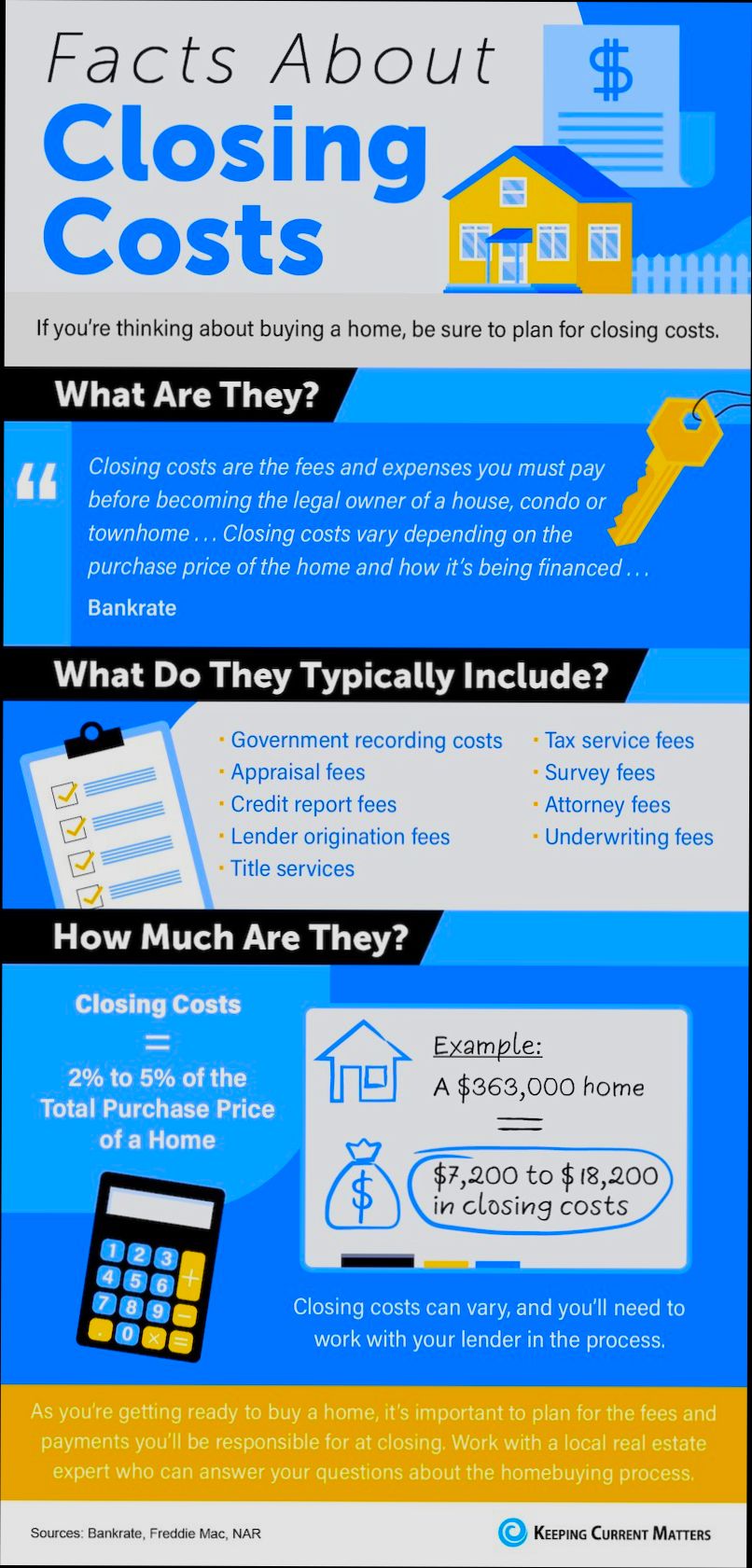

How Much Are Closing Costs in Real Estate? If you’re diving into the world of buying or selling a home, this question will likely pop up more than once. Typically, closing costs range from 2% to 5% of the home’s purchase price. So, if you’re eyeing a cozy $300,000 home, you might need to budget between $6,000 and $15,000 just for those final fees. Sounds like a lot, right? Well, let’s break it down; these costs can include everything from title insurance and appraisal fees to home inspection charges and even loan origination fees if you’re financing your purchase.

It’s not just a random number, either. For example, in some states, you’ll pay for a transfer tax, which could be hundreds to thousands of dollars depending on local rules. And don’t forget about things like escrow fees; they can hit your wallet hard, too. It’s all part of the elaborate dance of real estate transactions. So when you’re getting excited about that dream home, remember to factor in these necessities because they can seriously affect what you’ll end up shelling out once the deal is done.

Understanding Closing Cost Components

Closing costs can be a bit overwhelming if you don’t know what to expect. These costs cover various fees associated with processing a mortgage and may vary based on different factors. It’s important for you to understand the components that make up these costs so you can better prepare for the financial commitment of buying or refinancing your home.

Key Closing Cost Components

When considering closing costs, it’s essential to break them down into their components. Typically, closing costs average around 2-5% of the loan amount but can differ based on loan type and geographical location. Here are the main components to keep in mind:

- Loan Origination Fee: This fee usually ranges from 0-1% of the loan amount, serving as a charge for processing the loan application.

- Mortgage Broker Fee: Similar to the origination fee, this also generally accounts for 0-1% of the loan amount if you use a mortgage broker to assist you.

- Discount Points: Paying one discount point can reduce your interest rate; this typically costs 1% of the loan amount. For example, if you’re borrowing $250,000, one discount point would cost you $2,500.

- VA Loan Upfront Fee: If you’re obtaining a VA loan, anticipate an upfront fee ranging from 1.4% to 3.6% depending on your specific eligibility and prior usage of the benefit.

Breakdown of Costs

| Item | Fee |

|---|---|

| Loan origination fee | $2,500 (1% of loan amount) |

| Mortgage broker fee | $2,500 (1% of loan amount) |

| Discount fee | $625 (0.25%) |

| Processing fee | $450 |

| Underwriting fee | $500 |

| Wire transfer | $25-$50 |

| Credit report | $35 |

| Title insurance | $550 |

| Appraisal | $450 |

| Homeowners insurance premium (1st year) | $700 |

| Estimated Total | $7,985 (3.2% of loan amount) |

Real-World Examples

Let’s consider a scenario where you’re purchasing a home for $250,000:

- Loan Origination Fee: If your lender charges 1%, you’ll pay $2,500.

- Discount Points: Opting for one point might reduce your interest rate, which would cost you another $2,500.

- Additional Fees: Appraisal at $450, title insurance at $550, and a credit report at $35, among others, would add significant costs.

This could result in a total closing cost around $7,985, equaling 3.2% of your loan amount.

Practical Implications for Readers

Understanding these components can help you better budget for closing costs. It’s wise to ask your lender for an itemized closing cost sheet to see how each expense is broken down.

Additionally, you might want to consider negotiating some fees or seeking a lender who offers lower closing costs. Recognizing that closing costs will usually land you somewhere between 1% and 5% of your loan amount gives you a clearer picture of the financial commitment involved.

Being informed can empower you during the purchasing process and help you avoid any last-minute surprises.

Statistical Overview of Closing Costs

When diving into closing costs in real estate, it’s crucial to understand the statistical landscape that shapes these expenses. Closing costs typically fluctuate based on multiple factors, including the loan type, state regulations, and individual lender practices. Let’s explore key statistics that will give you an insightful overview of what to expect.

Key Statistics on Closing Costs

- Average Cost Range: Closing costs generally range from 2% to 5% of the home price. For example, purchasing a $300,000 home could mean closing costs anywhere between $6,000 to $15,000.

- Specific Cost Breakdown: A report from ClosingCorp indicates that the average closing costs for a single-family home have been around $6,800, but estimates suggest this could increase substantially by 2025 due to rising home values.

- Percentage of Loan for Fees: The loan origination fee can be up to 1% of the loan amount, while Realtor commissions could contribute 5%-6% of the home price, impacting your overall closing costs significantly.

- Loan-Specific Fees: For government-backed loans, an FHA loan may include an upfront mortgage insurance premium of 1.75% of the loan amount. In contrast, VA loans have funding fees that can vary from 1.4% to 3.6% of the loan amount.

- Negotiable Fees Opportunities: Many fees are negotiable. For instance, you might find that lender credits could offset some closing costs but at the expense of a slightly higher interest rate, which can be an important consideration in your overall financial strategy.

Breakdown of Common Closing Costs

| Closing Cost Component | Average Range |

|---|---|

| Loan Origination Fee | 0-1% of loan amount |

| Home Appraisal Fee | $500-$1,000+ |

| Title Insurance (Lender’s) | $300-$1,500+ |

| Recording Fee | $20-$250 |

| Prepaid Taxes and Insurance | $1,000-$4,500+ |

| Credit Report Fee | $35 |

| Home Inspection Fee | $300-$500 |

Real-World Examples of Closing Costs

Consider a buyer purchasing a home priced at $400,000. Here’s a rough estimate of the average closing costs they might incur:

- Loan Origination Fee: Approximately $4,000 (1%)

- Home Appraisal Fee: Around $800

- Title Insurance: About $1,000

- Prepaid Taxes and Insurance: Estimated at $2,000

In this scenario, the total estimated closing costs could surpass $7,800, illustrating the importance of budgeting ahead.

Practical Implications for Buyers

Understanding the statistical overview of closing costs helps you prepare financially. Knowing that the average costs can rise depending on your loan type and location allows you to set realistic expectations. Pay attention to the loan estimates provided by lenders, as they can delineate these costs clearly, helping you negotiate or seek concessions.

Actionable Insights on Closing Costs

- Utilize Closing Cost Calculators: Leverage online tools to estimate your specific closing costs based on your particular situation, as these can vary widely.

- Negotiate Fees Where Possible: Don’t hesitate to ask lenders about reducing origination and processing fees, or about obtaining lender credits for covering part of your closing costs.

Being well-informed about the statistical nature of closing costs paves the way for a smoother home-buying journey. Familiarize yourself with what you may encounter at closing, and ensure you budget accordingly.

Comparative Analysis of Regional Costs

When it comes to understanding closing costs in real estate, regional differences play a significant role. Various factors, including local taxes, market conditions, and state regulations, can significantly impact how much you might pay at closing. Let’s dive into some of these regional variations and what they might mean for you.

Key Regional Insights

- Northeast vs. Southeast: In the Northeast, closing costs can range up to 4-6% of the home’s price due to higher taxes and fees related to municipal regulations. Conversely, the Southeast might see these costs hovering closer to 2-4%, primarily because certain states have lower tax rates.

- Midwest vs. West Coast: The Midwest typically enjoys a more affordable closing cost structure, averaging around 3%, while the West Coast may experience costs rising to 5-7% due to expensive real estate markets and higher average state taxes.

- Southwest Trends: In states like Arizona and Nevada, closing costs can climb to approximately 4%, driven by increasing property values and additional fees associated with new developments.

Comparative Costs Table

| Region | Average Closing Cost (%) | Typical Fees |

|---|---|---|

| Northeast | 4-6% | High local taxes, recording fees |

| Southeast | 2-4% | Lower taxes, minimal state fees |

| Midwest | 3% | Affordable market conditions |

| West Coast | 5-7% | High property prices, extensive fees |

| Southwest | 4% | Growth-related surcharges |

Real-World Examples

Consider two contrasting cases:

1. A Home Purchase in Massachusetts: Homebuyers in Massachusetts might face closing costs of around 5%, influenced by high state income taxes and significant local fees. For a $400,000 home, this would amount to $20,000 in closing costs.

2. A Home Purchase in Florida: On the other hand, in Florida, an equivalent $400,000 home might incur closing costs as low as 3%, totaling $12,000. This reduction is largely due to lower average state fees and taxes.

Practical Implications

Understanding these regional costs allows you to budget effectively while planning your home purchase. Researching the average closing costs in your targeted area can help prevent financial surprises at closing. When negotiating, always take local variances into account to make more informed decisions.

- Tip: If you’re moving to a state with higher closing costs, set aside additional funds to cover these upfront expenses.

- Action Point: Check with local real estate professionals for the most accurate, region-specific closing cost estimates to ensure your budgeting reflects current conditions.

By keeping these regional variations in mind, you stand a better chance of effectively managing your real estate transaction’s financial aspects.

Real-World Scenarios of Closing Expenses

Navigating closing expenses in real estate can be an eye-opener for many homebuyers. Understanding how these costs manifest in real-world scenarios will help you prepare better and make informed decisions.

Key Scenarios to Consider

1. Home Purchase with Minimal Negotiation:

- Imagine you find your dream home listed at $300,000. If you factor in a closing cost percentage of around 3%, you could expect to shell out approximately $9,000 in closing expenses. This situation is common when buyers want to close quickly, often foregoing negotiations to expedite the process.

2. Investment Property Scenario:

- Let’s say you’re purchasing a rental property for $500,000. Closing costs may rise to 4% due to additional fees linked to the property’s investment status, totaling around $20,000. It’s crucial in these cases to anticipate potential expenses upfront to ensure your ROI remains viable.

3. First-Time Homebuyer with Down Payment Assistance:

- Consider a first-time buyer eligible for a state grant that covers the down payment. They find a home priced at $250,000, but must still pay about 2.5% in closing costs. This would equal roughly $6,250, showing that even with assistance, closing costs remain a significant financial consideration.

Comparative Table of Closing Expenses

| Scenario | Home Price | Closing Cost % | Estimated Closing Costs |

|---|---|---|---|

| Dream Home Purchase | $300,000 | 3% | $9,000 |

| Rental Property Investment | $500,000 | 4% | $20,000 |

| First-Time Homebuyer | $250,000 | 2.5% | $6,250 |

Real-World Examples

- Example 1: A couple purchases a home for $400,000 and encounters closing costs of 3.5%. Their total expenses reach $14,000. They were surprised when additional costs, such as title insurance and home inspection fees, added to their overall financial burden.

- Example 2: A military veteran utilizes a VA loan to buy a home for $450,000. While VA loans often have lower closing costs, this particular buyer still came across about $8,000 in expenses due to appraisal fees and local taxes, impacting the final amount due at closing.

- Example 3: A buyer in a competitive market pays $600,000 for a home with an expected closing cost of around 3%. The final tally of $18,000 in closing expenses reflects their urgent purchasing decision, stressing the importance of projections when making offers.

Practical Implications

Understanding these scenarios equips you with the knowledge to budget effectively. By anticipating a range of closing costs, you can:

- Build a solid financial plan that includes these expenses in your total purchase budget.

- Discuss potential closing cost contributions with the seller, especially if you are in a less competitive market.

- Gain clarity on what fees might be negotiable, like lender fees or certain inspection costs.

Actionable Advice

- Always ask for a detailed breakdown of expected closing costs prior to closing day. Knowledge is power, and this awareness can prevent surprises.

- Consider obtaining multiple quotes for title insurance and other services to potentially lower your overall closing expenses.

- Keep an eye on industry trends, as closing costs fluctuate; knowing the market can guide your negotiations effectively.

Advantages of Anticipating Closing Costs

Understanding the advantages of anticipating closing costs in real estate can significantly enhance your buying experience. By preparing for these expenses, you can streamline the process and avoid common financial pitfalls.

One of the primary benefits of anticipating closing costs is effective financial planning. Knowing that closing costs can range from 2% to 5% of the home price empowers you to budget appropriately, which means you can allocate funds without getting blindsided at the closing table. For example, if you’re purchasing a $300,000 home, you could estimate your closing costs to be between $6,000 and $15,000.

Another advantage is improved negotiation power. When you have a clear understanding of the potential closing costs, you can negotiate better terms with the seller or your lender. If you’re aware that certain fees—such as loan origination fees—may reach up to 1% of the loan amount, you can factor this into your overall negotiation strategy. Instead of merely focusing on the home’s price, you can discuss covering part of the closing costs in the final sale agreement.

Planning for these expenses also helps in building a positive relationship with your lender and real estate agents. When you approach the transaction with knowledge, they are more likely to trust your judgment, which can lead to better service or even potential discounts on fees.

| Closing Cost Category | Estimated Percentage | Example Fee for a $300,000 Home |

|---|---|---|

| Loan Origination Fee | 0% - 1% | $0 - $3,000 |

| Title Insurance | 0.5% - 1% | $1,500 - $3,000 |

| Appraisal Fee | Fixed Fee | $400 - $700 |

| Government Fees | Varies by location | $800 - $1,500 |

Real-world examples highlight the advantages of anticipating these fees. One homebuyer, Sarah, learned early on that her closing costs would total around $10,000. By saving this amount in advance and factoring it into her budget, Sarah avoided any last-minute scrambles, allowing her to focus on the excitement of her new home.

Another buyer, Tom, effectively negotiated with the seller to cover $2,500 in closing costs after he did his research and presented a solid case based on local market trends. This negotiation eased Tom’s financial burden and highlighted the importance of being informed about potential expenses.

For you, the practical implications of anticipating closing costs mean that you won’t be facing unexpected surprises that can derail your plans. Knowing these expenses ahead of time allows you to consider additional options, such as adjusting your offer price or exploring different financing strategies.

Taking the time to research and anticipate closing costs puts you in the driver’s seat. Start by asking your real estate agent for a detailed estimate of closing costs based on the property you’re interested in to get started on the right foot.

Hidden Fees in Real Estate Transactions

Navigating the world of real estate can be tricky, especially when it comes to hidden fees that can sneak up on you during a transaction. Understanding these fees is crucial to ensure you’re fully prepared for the actual cost of buying or selling a property. Let’s dive into some common hidden fees that you might encounter.

Common Hidden Fees to Watch Out For

Many buyers and sellers overlook certain fees that can significantly impact your overall costs. Here are some hidden fees to consider:

- Prepayment Penalties: If you pay off your mortgage early, some lenders might charge a fee which can range from 2% to 5% of the remaining principal balance.

- Title Insurance: While this is often included in closing costs, it might also be an additional expense. Title insurance fees can vary, with costs typically between $1.50 to $3.50 per $1,000 of the home’s value.

- Transfer Taxes: Many states impose transfer taxes when ownership changes hands. This can be anywhere from 0.1% to 2% of the home’s purchase price, depending on your location.

- Homeowners Association (HOA) Fees: If you’re buying in a community with an HOA, be aware that there may be one-time fees, transfer fees, or delinquent fees you could be responsible for upon closing.

Hidden Fees Breakdown Table

| Fee Type | Description | Typical Cost Range |

|---|---|---|

| Prepayment Penalties | Fee for paying off mortgage early | 2% to 5% of remaining principal |

| Title Insurance | Protects against disputes over property ownership | $1.50 to $3.50 per $1,000 |

| Transfer Taxes | State-imposed fees on property transfer | 0.1% to 2% of purchase price |

| HOA Fees | One-time or transfer fees for community living | Varies significantly by community |

Real-World Examples of Hidden Fees

Consider Jane, who decided to purchase a condo in Florida. While she budgeted for regular closing costs, she was surprised to find out about a $1,200 transfer tax specific to her county. Had she not asked her realtor about fees that might not be included in her initial quote, she would have been caught off guard.

Similarly, Mike prepared to buy a home in a planned community. He understood there would be HOA fees, but didn’t account for the additional $300 transfer fee just to become a member of the community. This unexpected cost made him rethink his budgeting strategy.

Practical Implications for Buyers and Sellers

Being aware of potential hidden fees allows you to better prepare your finances. Here’s how you can mitigate the impact of hidden fees:

- Ask Questions: Always clarify any fees with your real estate agent or lender. Understanding your options can help you avoid surprises.

- Review the Closing Disclosure: This document should itemize all your costs, including hidden fees. Make sure to read it carefully before closing.

- Do Your Research: Familiarize yourself with common local fees, such as transfer taxes and HOA fees, to anticipate costs that might not be obvious.

Actionable Advice on Hidden Fees

As you navigate your real estate transaction, keep a close eye on the details. Research and prepare for the possibility of prepayment penalties, title insurance, and various local taxes. Establish a contingency fund to cover unexpected expenses that may arise during the closing process, ensuring you’re not left scrambling at the last minute.

Negotiating Closing Costs Effectively

Successfully negotiating closing costs can significantly impact your overall financial picture when purchasing a home. Understanding how to navigate this part of the real estate transaction can not only save you money but also provide flexibility in an often rigid process.

Key Strategies for Negotiation

To effectively negotiate closing costs, consider the following strategies:

- Research and Compare Estimates: Before starting negotiations, gather multiple closing cost estimates from different lenders or service providers. This will give you leverage, as you can present a more competitive offer.

- Negotiate with the Seller: Don’t hesitate to ask the seller to cover certain closing costs, especially if you find the property has been on the market for a while. Sellers might be willing to pay as a way to incentivize a quick sale.

- Use Strong Financing Offers as Bargaining Chips: If you have a strong financial position—such as a pre-approved mortgage or a larger down payment—use this as leverage in your negotiations. Sellers often prefer buyers who can close quickly and reliably.

- Ask for Itemized Fees: Request a breakdown of all closing fees. This will help identify areas where you can negotiate, whether it’s a loan origination fee or title insurance costs.

- Get Quotes from Multiple Service Providers: Sometimes, individual services associated with closing costs can be negotiated. By obtaining different quotes, you can request the lender or agent to match or beat a lower price.

Comparative Table of Negotiation Potential

| Fee Type | Average Negotiability | Tips for Lowering Costs |

|---|---|---|

| Loan Origination Fee | 0-1% | Shop around for lenders, negotiate based on competitor rates |

| Title Insurance | Up to 20% | Compare quotes, ask for bundled discounts with other services |

| Appraisal Fee | Limited (can’t change lender policies) | Request fee waivers if a similar appraisal was completed recently |

| Home Inspection Fee | Often negotiable | Discuss with your agent for recommendations on lower-cost inspectors |

Real-World Examples

For instance, one homebuyer in Texas managed to negotiate a $1,500 reduction in appraisal fees by showing competing offers from other appraisal companies. Meanwhile, a buyer in Florida successfully negotiated for the seller to cover the title insurance fee, which typically can reach several thousand dollars. This kind of negotiation can significantly reduce your out-of-pocket costs when closing.

Practical Implications for Readers

Engaging in negotiations related to closing costs requires a proactive approach. Make sure you keep an open line of communication and express your willingness to collaborate with your lender and the seller. This not only helps in securing favorable costs but also strengthens your position as a serious buyer.

Actionable Advice for Negotiating Closing Costs

- Always negotiate multiple aspects of closing costs; don’t settle for the first offer you receive.

- Leverage your financing strength as a bargaining tool.

- Be straightforward about your budget and highlight areas where you require assistance.

This approach empowers you to maximize your savings as you complete your real estate transaction.