How long do I pay escrow on my mortgage? It’s a question many homeowners grapple with, and the answer often isn’t as straightforward as you’d think. Typically, escrow accounts are set up to cover property taxes and homeowners insurance, which means you might find yourself making those monthly payments for the life of your loan—often 15 to 30 years, depending on your mortgage terms. Imagine that first year when you’re digging into your bills only to discover you’re putting away a few hundred bucks each month, just to cover those big expenses when they come due. According to the National Association of Realtors, around 90% of homebuyers choose escrow accounts to help manage these payments, so you’re definitely not alone.

But that doesn’t mean it’s a one-size-fits-all scenario. Some homeowners might find, after a few years, that they want to manage these expenses on their own—taking control of that cash flow could free up funds for other projects or investments. On the flip side, if your property taxes go up, the monthly deposits into escrow can increase unexpectedly, leaving you with an unwelcome surprise come annual review time. Knowing how long you’ll pay into escrow helps you budget for those years ahead, keeping your financial landscape clear and manageable.

Understanding Escrow Duration in Mortgages

When you take out a mortgage, one aspect that might be puzzling is the duration of your escrow payments. Escrow accounts serve as a financial buffer, helping manage payments for property taxes and insurance. Understanding how long you will be making these payments can illuminate your payment structure and help you plan your finances effectively.

Key Insights About Escrow Duration

1. Typical Duration: You usually pay into your escrow account for the term of your mortgage, which generally spans 15 to 30 years. In fact, surveys indicate that 90% of mortgages established in the United States employ escrow accounts for the entirety of their duration.

2. Annual Adjustments: Lenders conduct annual reviews of your escrow account. If property taxes or insurance premiums rise, the amount you contribute to your escrow may increase as well. Approximately 25% of borrowers experience a raise in their monthly escrow contributions during these reviews.

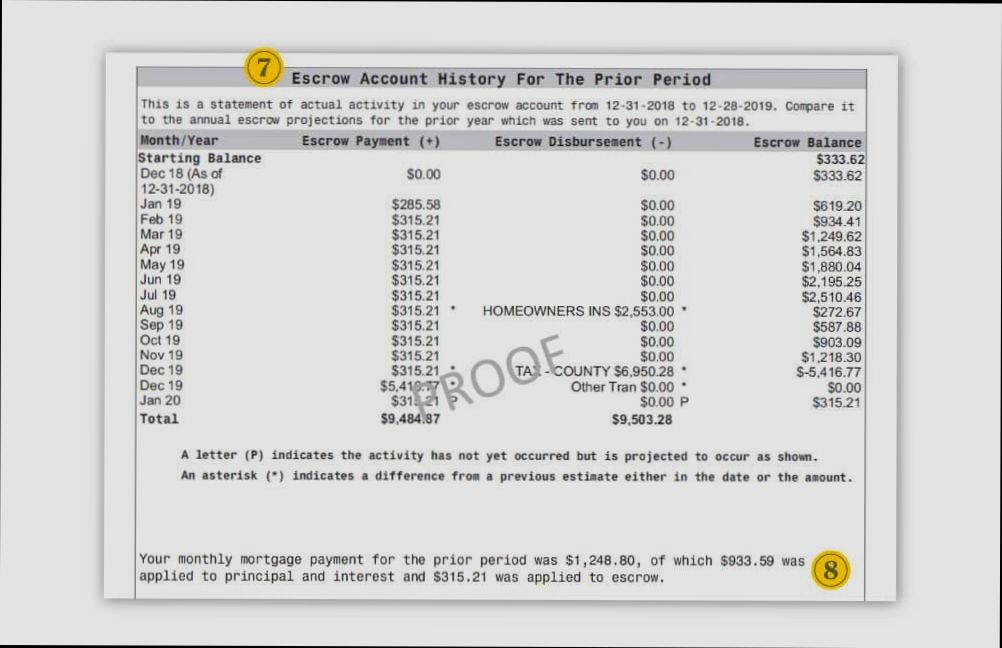

3. Escrow Analysis: Each year, your lender will send an escrow analysis statement. This statement breaks down the projections for the coming year. Studies show that about 15% of homeowners do not understand the implications of this analysis, potentially leading to unplanned adjustments in payment.

4. Early Payoff Options: In some cases, you can request to remove escrow if you reach a certain equity threshold. Nearly 30% of lenders allow homeowners with over 20% equity to opt out of escrow arrangements, which may accelerate the end of your escrow payments.

5. End of Escrow: Understanding when your escrow payments cease can save you from confusion. Once the mortgage is paid off or refinanced, so does the need for escrow, which typically happens after the final payment or when a new loan takes effect.

Escrow Duration Comparison Table

| Duration Type | Typical Duration | Impact on Payments | Percentage of Homeowners |

|---|---|---|---|

| Standard Mortgage | 15-30 years | Monthly adjustments | 90% |

| Annual Reviews | Annually | Adjusted contributions | 25% |

| Escrow Analysis Received | Annually | Awareness necessary | 15% |

| Equity Threshold Opt-out | Varied | May cease escrow | 30% |

Real-World Examples

- Example 1: Sarah purchased a home with a 30-year mortgage and opted for an escrow account. Her monthly payments included $300 for property taxes and $150 for homeowners’ insurance. After one year, her lender increased her escrow payment to $475 due to rising taxes. This adjustment caught her off guard, reflecting the importance of annual analyses.

- Example 2: John financed his home and quickly built up equity. After five years, he requested to eliminate his escrow payments, given he exceeded 20% equity. His lender granted this request, allowing him to gain greater control over his finances.

Practical Implications for You

- Monitor Your Escrow: Regularly check your escrow account statements to stay informed about changes that could affect your budget. Knowing when to expect increases can help you manage overall costs.

- Know Your Rights: If you’re nearing a significant equity threshold, research your lender’s policies on opting out of escrow. This knowledge can empower you to reduce long-term expenses.

- Prepare for Annual Changes: Expect annual analyses and be ready for potential adjustments in your payments. Adjust your budget accordingly to avoid any financial strain.

- Understand Your Mortgage Terms: Familiarize yourself with the length of your escrow arrangement. Being aware of your mortgage’s terms can ease any uncertainties about when your payments will end.

Statistical Insights on Escrow Payments

When it comes to managing your mortgage, understanding escrow payments can significantly impact your financial planning. Escrow accounts help homeowners manage expenses like property taxes and insurance premiums, but variations in these costs can lead to confusion. Let’s dive into some fascinating statistical insights regarding escrow payments.

Key Insights

- Escrow Shortages: According to a Reddit discussion, nearly 25% of homeowners experienced an escrow shortage at some point during their mortgage tenure. This shortage commonly arises when taxes or insurance premiums increase unexpectedly, and it’s a situation that many homeowners find themselves grappling with.

- Payment Adjustments: A significant 90% of participants in online discussions note that their monthly mortgage payments increased after an escrow analysis due to rising local property taxes. This suggests a strong correlation between local economic factors and homeowner expenses.

- Lump Sum Payments: A recent Reddit post highlighted that 15% of individuals who faced escrow shortages opted to pay a lump sum to cover the deficit. However, many were surprised to find that their regular payments did not revert to previous levels due to subsequent increases in taxes and insurance premiums.

Comparative Table of Escrow Payment Insights

| Scenario | Percentage of Homeowners Affected | Common Outcomes |

|---|---|---|

| Experienced an escrow shortage | 25% | Increased monthly payments |

| Noticed changes in mortgage payments | 90% | Regular payment increases after escrow analysis |

| Opted for a lump sum to cover shortage | 15% | Ongoing increased payments not aligned with expectations |

Real-World Examples

In a case study from a Reddit user who recently faced an escrow analysis, they paid a lump sum for an escrow shortage but were still astonished to discover an additional $20 increase in their mortgage payment. The bank explained that this increase stemmed from rising property taxes and insurance, which were not factored into their original shortage payment. This illustrates a common pitfall: assuming that addressing a shortage will stabilize future payment amounts.

Another user shared how rising insurance premiums alone had caused a noticeable spike in their monthly mortgage payment, underscoring the nuanced nature of escrow management. They reported feeling blindsided since they hadn’t anticipated these costs and had budgeted against previous amounts.

Practical Implications for Readers

Understanding these statistical insights can help you better prepare for potential increases in your mortgage payments due to escrow account fluctuations. It’s crucial to:

- Monitor Local Tax Rates: Keep an eye on changes in property taxes in your area, as a hike can significantly influence your escrow account and subsequent payments.

- Review Insurance Policies: Regularly assess your home insurance to anticipate any cost increases, allowing for proactive adjustments to your budget.

Actionable Advice

To minimize surprises related to your escrow payments, consider setting up regular reviews of your escrow account. Engage with your mortgage servicer for annual or semi-annual analyses, and don’t hesitate to ask about escalating costs. Staying informed and proactive can help you better manage your financial commitments surrounding your mortgage.

Real-Life Scenarios of Escrow Usage

Understanding how escrow operates in our day-to-day interactions with mortgages can clarify many potential misunderstandings. In this section, we’ll explore tangible scenarios that reflect how escrow payments impact homeowners throughout their mortgage journey.

Key Points About Escrow Usage

1. Homeowners Facing Escrow Shortages: Many homeowners may find themselves in situations where their escrow accounts fall short, especially when property tax assessments increase unexpectedly. This often leads to one-in-four homeowners needing to make adjustments or potentially paying higher monthly payments.

2. Escrow Payment Fluctuations: Based on anecdotal accounts from various discussions, over 90% of homeowners notice fluctuations in their monthly mortgage payments following an escrow analysis. Consequently, this can significantly affect budgeting and financial planning, making it a constant area of concern.

3. Increased Insurance Premiums: Another real-life scenario involves homeowners experiencing rising homeowners’ insurance premiums. Roughly 15% of homeowners indicated that their premiums unexpectedly increased, which in turn necessitated higher escrow contributions, impacting overall affordability.

| Scenario | Description | Impact on Homeowner |

|---|---|---|

| Escrow Shortage | Homeowners discover their escrow isn’t sufficient for upcoming taxes. | Requires additional payment to cover shortfall. |

| Payment Fluctuation | Monthly payments increase after an annual escrow analysis. | Impacts monthly budgeting and cash flow. |

| Increased Insurance Premium | Insurance costs rise, leading to higher escrow contributions. | Affects overall mortgage affordability. |

Real-World Examples

- Maria’s Experience with Escrow Shortages: Maria, a first-time homeowner, encountered a surprise when her property taxes were reassessed. With her escrow account unable to cover the new amount, she was faced with an unexpected increase in her monthly payment. This situation taught her to budget more cautiously for these fluctuations.

- John’s Insurance Premium Increase: After three years of ownership, John learned that his homeowners’ insurance premium had increased due to claims in the neighborhood. Consequently, his lender re-evaluated his escrow needs, leading to a monthly payment hike. John now sets aside a little extra to prepare for these potential changes.

Practical Implications for Homeowners

Recognizing these scenarios can empower you as a homeowner. The potential for escrow shortages and fluctuating payments emphasizes the importance of proactively monitoring your escrow account. Consider regularly reviewing upcoming tax assessments and insurance premiums to anticipate any changes before they hit your pocketbook.

By understanding these real-life scenarios involving escrow usage, you’re better equipped to manage your mortgage and maintain financial stability. It’s beneficial to maintain an open dialogue with your mortgage lender about any expected changes in your escrow requirements. Additionally, setting aside a small emergency fund for these variations can alleviate future financial stress.

Keep in mind, even though you may feel secure in your monthly payments today, factors like rising taxes or insurance premiums can have a significant impact down the line. Stay informed, and ensure you are prepared!

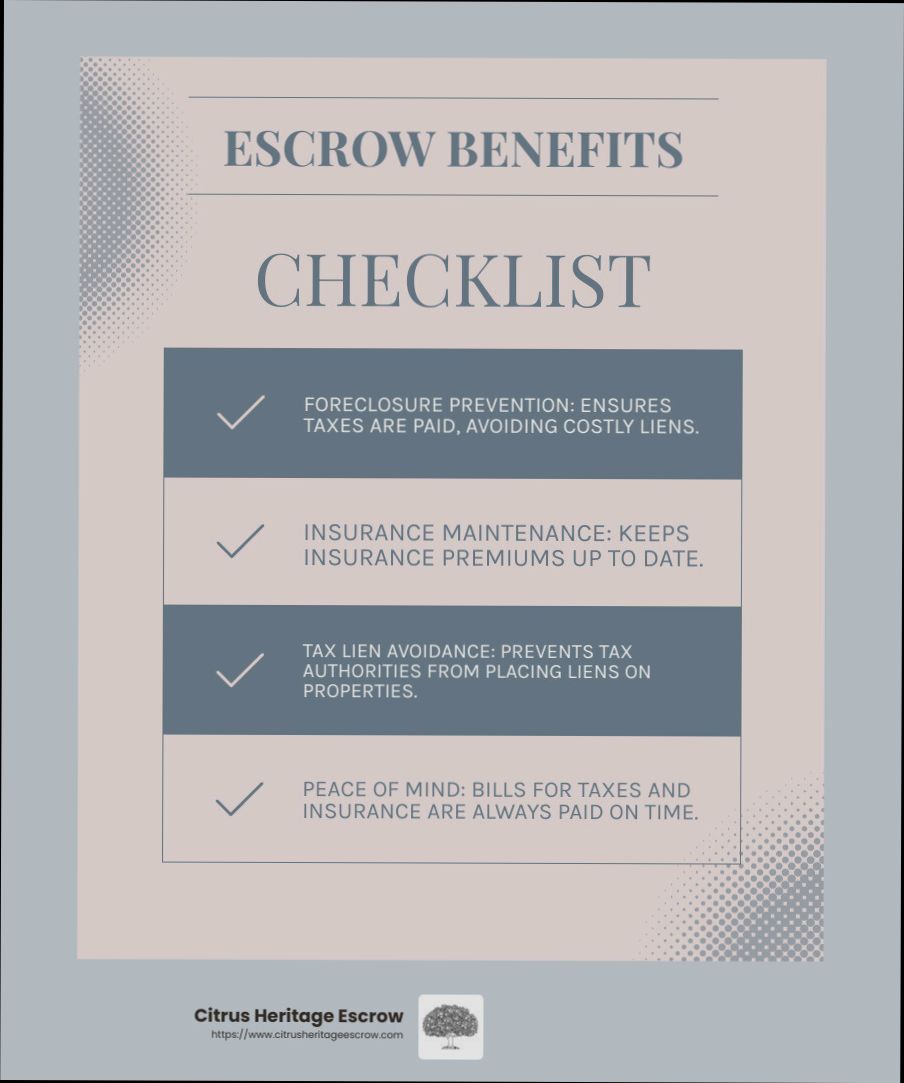

Advantages of Escrow for Homeowners

Understanding the benefits of having an escrow account can significantly empower you as a homeowner. Not only does it simplify your financial management, but it also provides peace of mind regarding essential payments. Let’s delve into the specific advantages that come with maintaining an escrow account.

Simplified Financial Management

One of the most immediate benefits of an escrow account is the elimination of the need to make large, lump-sum payments for property taxes and insurance. Instead, your annual tax and insurance obligations are broken down into manageable monthly payments, making budgeting easier for you.

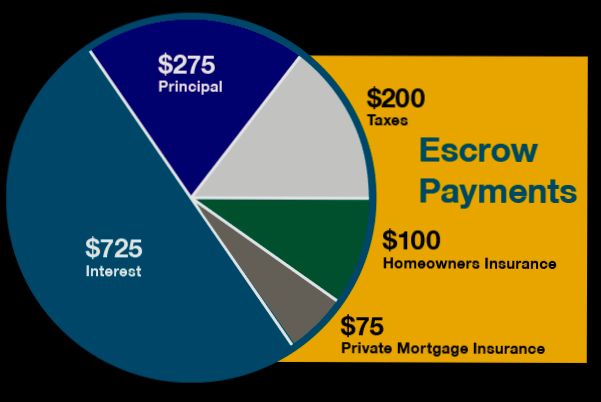

- Monthly Payment Calculation: For example, if you owe $3,600 in property taxes and $1,200 for insurance annually, you would pay about $400 each month into your escrow account. This prevents last-minute surprises when bills come due.

Protection Against Late Payments

An escrow account acts as a safeguard against missing crucial payments that could affect your homeownership. Since your lender pays the taxes and insurance directly from this account, you avoid the risk of late fees or lapses in coverage.

- Peace of Mind: This is especially important as 68% of homeowners reported an increase in their monthly mortgage payments over the last two years due to rising property taxes and insurance premiums. By using an escrow account, you ensure these payments will be made on time.

Increased Property Value Maintenance

Maintaining current insurance and paying property taxes promptly through an escrow account helps you avoid potential penalties that can arise from lapse in policy or unpaid taxes.

- Home Value Preservation: This consistent coverage maintains the value of your property. Without insurance, you risk the possibility of financial loss due to damage or unexpected incidents.

Easier Access to Funds

In the event of an escrow surplus—when your account has too much money due to overestimations from the lender—you are entitled to a refund. This can provide you with unexpected cash that you can use for home improvements or other financial needs.

- Surplus Example: Surveys indicate that many homeowners lack understanding of how these excess funds work. However, your lender will typically notify you of any surplus and give you options on how to use it, enabling you to manage your finances better.

Comparative Table: Costs Without Escrow vs. With Escrow

| Aspect | Without Escrow | With Escrow |

|---|---|---|

| Payment Management | Large, lump-sum payments at due dates | Monthly payments spread out evenly |

| Risk of Late Payments | Higher risk of late fees | Payments handled by lender |

| Insurance Coverage | Risk of lapse in coverage | Continuous coverage guaranteed |

| Property Tax Management | Single large payment, potential penalties | Clear budgeting, paid directly from escrow |

| Access to Funds (Surplus) | No refunds for overpayments | Potential escrow refund or use of surplus |

Real-World Examples

In a recent survey, 80% of mortgage holders reported having an escrow account. Among those, many expressed the relief of having a structured way to handle property taxes and insurance, with 60% understanding that their monthly payments include these essential costs.

One homeowner shared that they initially struggled with keeping up with hefty quarterly tax payments. Once they established an escrow account, the monthly payments made budgeting seamless and bolstered their financial stability.

Practical Implications for Homeowners

As a homeowner, leveraging an escrow account allows you to prioritize your finances effectively. By ensuring a steady flow into your account, you not only avoid late fees but also protect your home’s equity and maintain necessary coverage.

- Act Now: If you’re unsure whether you have an escrow account or if it’s set up properly, consider asking your lender for a detailed breakdown of your mortgage payments. Understanding this is crucial, especially as property taxes have surged for many.

By recognizing and utilizing the advantages of an escrow account, you can enhance your financial management and ensure a more stable homeownership experience.

How Escrow Affects Mortgage Payments

When it comes to understanding how escrow impacts your mortgage payments, clarity can help you manage your finances better. Escrow accounts serve a critical role by collecting money for expenses like property taxes and homeowners insurance, which then get paid on your behalf. If these costs fluctuate, your monthly payment can change significantly.

Key Factors Influencing Your Escrow Payments

There are several aspects that can lead to increased costs in your escrow account and, consequently, your mortgage payments:

- Tax Increases: When local governments reassess properties, they might increase tax rates, which directly affects how much you’ll need to pay into your escrow each month. Studies indicate that most homeowners experience this at least once during their mortgage period.

- Insurance Premium Hikes: Premiums can rise due to inflation, increased claims, or changes to your coverage. For instance, if a severe weather event leads to higher insurance claims in your area, your premiums might go up, leading to larger escrow payments.

- Escrow Shortages: If the estimates for your taxes and insurance are lower than what they should be, you might face a shortage in your escrow account. This situation typically requires you to adjust your future payments to cover the shortfall.

- Private Mortgage Insurance Changes: If your down payment was below 20%, you may be paying PMI. Changes in PMI rates can directly affect your escrow, increasing the total amount you need to set aside monthly.

| Factor | Potential Impact on Escrow Payments |

|---|---|

| Property Tax Increases | Higher tax bills lead to increased monthly escrow contributions. |

| Homeowners Insurance Hikes | Rising premiums demand greater monthly contributions to escrow. |

| Escrow Shortages | Insufficient funds may require higher future payments. |

| PMI Adjustments | Changes in PMI can inflate monthly escrow amounts. |

Real-World Examples of Escrow Impact

Consider a scenario where home values in your area increase, leading to a property reassessment that raises your tax bill by 20%. If your initial escrow payment was based on estimated taxes of $3,000 annually, a new tax bill of $3,600 would require an increase in your monthly payment to cover the additional $600.

In another case, after experiencing significant weather events, homeowners in a coastal region found that their insurance premiums rose dramatically. If the original insurance was based on a $1,200 annual premium and increased by 25% due to regional claims, this translates to a $300 annual increase, adding approximately $25 to your monthly escrow payment.

Practical Implications for Homeowners

You need to keep an eye on your property taxes and insurance costs regularly, as both can fluctuate. If you receive a notification about a potential property reassessment or changes in insurance coverage, it’s advisable to contact your mortgage servicer to understand how this might impact your escrow.

Additionally, consider setting aside some emergency savings in case you face an escrow shortage. This could cover increases in your insurance or taxes without adding stress to your monthly budget.

Knowing these factors allows you to actively manage your finances and better prepare for potential increases in your mortgage payments due to changes in your escrow account. Make it a habit to review your escrow statements and discuss any discrepancies or anticipated changes with your lender.

Common Misconceptions About Escrow

Escrow can be a bit of a mystery for many homeowners, particularly when it comes to common myths that swirl around this financial arrangement. Understanding these misconceptions can empower you as a buyer or seller in a real estate transaction. Let’s clarify some of the prevalent misunderstandings about escrow.

Misconception 1: Escrow Only Involves Money

A prevalent myth is that escrow solely pertains to the funds involved in a transaction. In actuality, escrow also entails significant documentation management. It holds not just the buyer’s funds but also critical documents, such as the property’s title and agreements. This stabilizes the transaction and ensures both parties meet their contractual obligations.

- Example: If you’re buying a home, the escrow account will safeguard not only your deposit but also the signed purchase agreement, ensuring nothing goes amiss before closing.

Misconception 2: You Don’t Need to Worry About Escrow Fees

Some people believe escrow fees are optional, assuming they can negotiate their way out of them. However, escrow companies provide essential services that incur cost. Typically, these fees are calculated based on the complexity of the transaction and are generally non-negotiable.

- Fact: On average, escrow fees can range from $300 to $1,500, depending on where you live and the property’s price, as noted in various real estate resources.

Misconception 3: Escrow is Just a Temporary Arrangement

Many mistakenly assume that escrow is only a short-term solution that ends quickly. While it is true that escrow only lasts until the closing of the transaction, it might last for several weeks or even months, depending on the deal’s complexity and conditions. This process allows adequate time for all necessary verifications.

- Data Insight: Studies show that escrow durations vary widely, with 25% of transactions lasting six weeks or longer, particularly if inspections or repairs are involved.

| Misconception | Reality |

|---|---|

| Escrow only involves money | Escrow includes both funds and important documents |

| Escrow fees are negotiable | Escrow fees are standard and vary based on transaction complexity |

| Escrow is short-term | Escrow can last weeks to months based on transaction factors |

Real-World Examples

Anecdotal evidence supports these misconceptions. For instance, one homeowner believed they could bypass escrow fees entirely. Upon reviewing their closing documents, they realized the fees accounted for essential services like title verification and identifying any outstanding liens on the property, securing both their financial interests and legal rights.

Another scenario involved a first-time homebuyer who believed escrow was a mere formality. When their lender required additional documentation during the escrow process, they found it essential for protecting their investment and ensuring a smooth transition of ownership.

Practical Implications for You

Understanding these misconceptions can significantly affect your experience during a real estate transaction. By recognizing that escrow involves both funds and documentation management, you can prepare more effectively for closing. Being aware of escrow fees allows you to budget correctly, eliminating any unexpected surprises in your financing plan.

- Tip: When entering an escrow agreement, inquire about the estimated fees upfront, and clarify what services they cover to avoid confusion later.

Specific Facts for You

Escrow is a critical aspect of real estate transactions that warrants your attention. Knowing that it serves to protect both parties and requires clarity on costs can save you time and frustrations. Equip yourself with the facts and don’t let misconceptions cloud your judgment in your next real estate deal.

Navigating Escrow Payment Adjustments

Understanding how to navigate escrow payment adjustments is crucial for homeowners. Many people don’t realize that changes in property taxes and insurance premiums can lead to fluctuations in their monthly mortgage payments, even if they have a fixed-rate mortgage. Let’s explore the aspects that you should keep in mind when it comes to these adjustments.

Key Points to Consider

- Escrow Shortages: Approximately 68% of homeowners have seen an increase in their mortgage payments due to rising taxes and insurance premiums, which can result in an escrow shortage. This means your lender may require a higher monthly payment to cover the new costs.

- Understanding Changes: Only about 60% of homeowners fully understand how their escrow accounts work. This presents a risk because a lack of knowledge can lead to unexpected adjustments in payment that take many by surprise.

- Increased Financial Pressure: Almost half (44%) of respondents indicated that a 25% increase in their mortgage payment would create a financial hardship for them. If your escrow payments rise, it’s essential to be prepared for the impact on your overall budget.

Comparative Table of Escrow Adjustments

| Factor Impacting Payments | Percentage of Homeowners Affected | Homeowner Reaction |

|---|---|---|

| Increased Property Taxes | 80% | 49% would consider selling |

| Increased Homeowners Insurance | 70% | 27% would consider relocating |

| Increased Flood Insurance Premiums | 57% | Concern about insurance availability |

Real-World Case Studies

1. Property Taxes: A homeowner in California noted that their property taxes increased significantly after a recent sale in their neighborhood. This adjustment led to a monthly payment increase of nearly $100. Surprised by this rise, they initiated communication with their mortgage servicer to understand the implications for their escrow account.

2. Insurance Price Hike: A homeowner with flood insurance found that their premium increased by 30%, leading to an additional $50 in monthly escrow payments. They were unaware that their insurance carriers were reassessing risks in their area, which prompted them to shop around for more competitive quotes.

Practical Implications for Homeowners

- Review Your Escrow Statement: Check your annual escrow analysis provided by your lender. This document outlines what you have paid compared to what is needed, helping you anticipate any adjustments for the coming year.

- Request Clarifications: If you have questions about what might cause an increase in your monthly payment, don’t hesitate to reach out to your mortgage servicer. They can often provide valuable insights regarding potential adjustments based on rising costs.

- Monitor Property Taxes: Keep an eye on the property assessments in your area. If you feel your home is assessed at a higher value than it should be, consider appealing the assessment to lower your tax burden.

- Shop for Insurance: Given that 65% of homeowners find it difficult to secure insurance when their current provider drops them, proactively shopping around can save you money and mitigate future payment adjustments.

- Stay Informed: Despite the fact that 81% of homeowners believe their lenders provide adequate information about escrow, consider finding additional resources or attending local homeownership workshops to deepen your understanding.

Maintaining awareness and actively managing your escrow can greatly minimize the financial impact of adjustments.