Financing options for buying a house can feel like a maze at times, but understanding your choices is key to finding the right fit. Did you know that nearly 90% of homebuyers rely on a mortgage to make their dreams a reality? From traditional fixed-rate loans, which often hover around 3% to 4%, to adjustable-rate mortgages that might start lower but can rise as the years pass, there’s a lot to consider. If you’re a first-time buyer, programs like FHA loans can open doors with down payments as low as 3.5%, while veterans have the unique opportunity of VA loans that come with no down payment at all.

If you’re looking to buy in a bustling market, cash offers are another story altogether—they can make your bid more appealing, as they simplify the process without the need for mortgage approval. However, most folks will leverage other financing methods, including the increasingly popular USDA loans that cater to rural buyers with minimal requirements. Local banks and credit unions often have tailored programs that might not make headlines but can offer competitive rates and personalized service. With so many paths to choose from, getting your financing sorted early can give you a leg-up in the home-buying race.

Exploring Government-Backed Loan Programs

When it comes to financing options for buying a home, government-backed loan programs serve as invaluable tools for many potential homeowners. These loans are designed to make homeownership more accessible, particularly for first-time buyers, low-income families, and those with less-than-perfect credit. Let’s dive into the details and see how these programs can benefit you.

Key Government-Backed Loan Programs

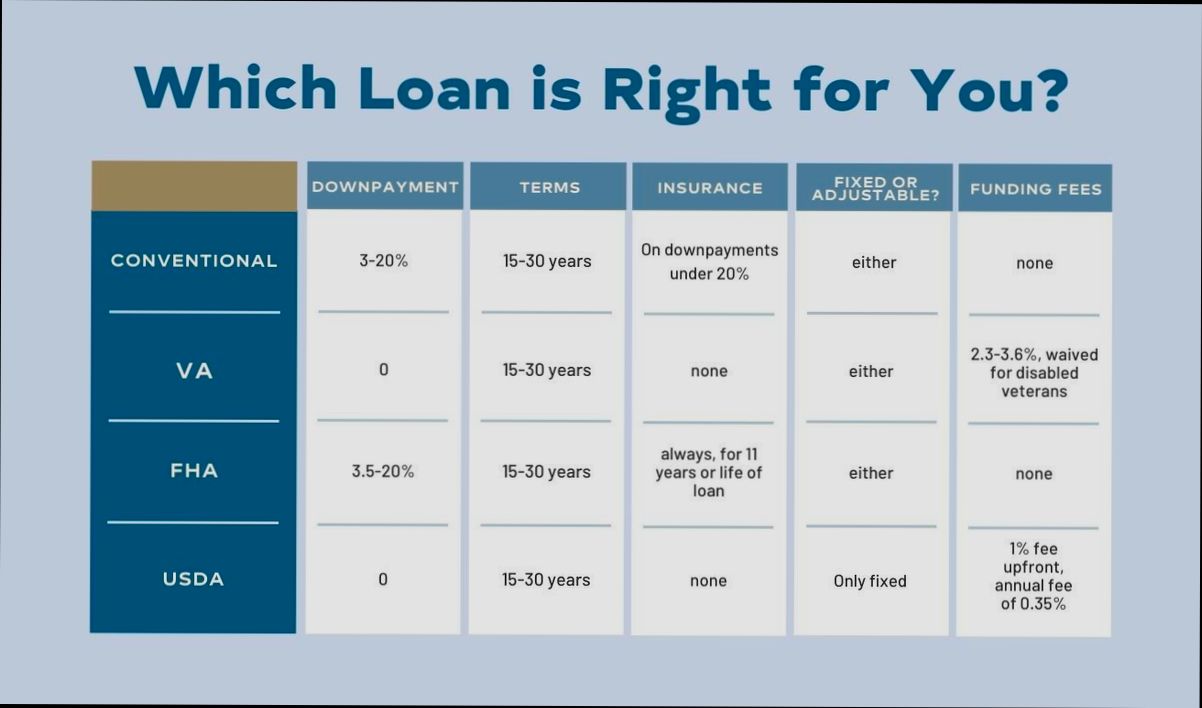

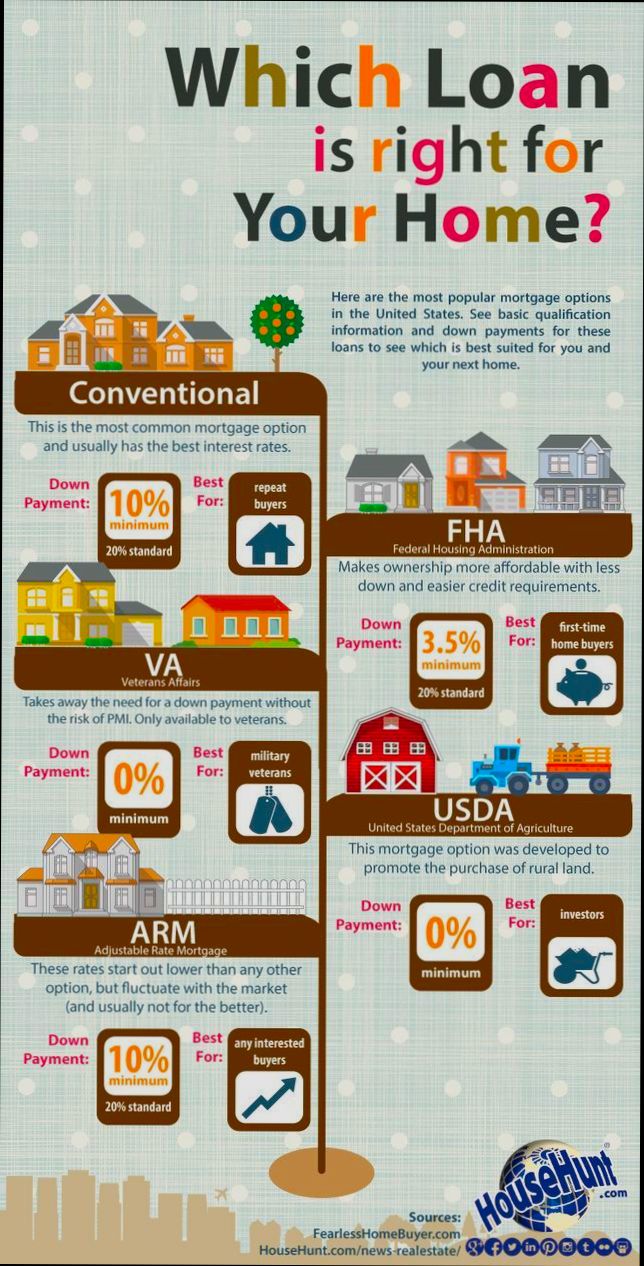

Government-backed loans typically include FHA, VA, and USDA loans. Each program has unique features tailored to different audiences. Here are some essential aspects you should know:

- FHA Loans: These are ideal for first-time homebuyers and those with lower credit scores. You can secure these loans with a down payment as low as 3.5%.

- VA Loans: Designed for veterans and active military personnel, VA loans require no down payment and do not necessitate private mortgage insurance (PMI).

- USDA Loans: Perfect for rural homebuyers, USDA loans offer 100% financing for eligible applicants, making it an attractive option for those looking to settle in less urbanized areas.

Here’s a concise comparison of these loans focusing on their primary benefits:

| Loan Type | Minimum Down Payment | Credit Score Requirement | Mortgage Insurance |

|---|---|---|---|

| FHA | 3.5% | 580 or higher | Required |

| VA | 0% | No minimum | None |

| USDA | 0% | 640 or higher | Required in some cases |

Real-World Examples

Examining prior data can illuminate how these loans positively affect communities. For instance, the recent surge in government-backed loans facilitated by the Small Business Administration (SBA) showcases the transformative potential of such financial support. SBA’s commitment to small business funding illustrates how similar government programs uplift underrepresented demographics:

- In the last fiscal year, the SBA enabled 5,200 loans amounting to $1.5 billion for Black-owned businesses, a significant increase in loan availability.

- Latino-owned businesses reportedly received 9,600 loans totaling $3.3 billion, showing a remarkable enhancement in financing access.

- Moreover, majority women-owned businesses saw 15,500 loans worth $5.6 billion, reflecting a doubling of participation compared to the previous fiscal year.

These examples underline the critical role of government initiatives in enhancing economic opportunity, much like the assistance provided through government-backed home loans.

Practical Implications

By exploring and utilizing government-backed loan programs, you can significantly reduce the barriers to homeownership. These loans allow for lower upfront costs and provide flexible credit requirements, making them appealing to a broader range of potential homeowners.

Here are some actionable insights based on these programs:

- Research Eligibility: Review the specifics of each program to determine which one aligns best with your financial situation.

- Prepare Your Finances: Focus on improving your credit score and gathering necessary documentation to enhance your chances of loan approval.

- Engage with Professionals: Consider seeking advice from a mortgage broker or a financial advisor who specializes in government-backed loans to navigate the application process.

Looking at these details reinforces the notion that government-backed loan programs aren’t just financial products; they’re gateways to homeownership that can change lives. Remember, understanding these options is the first step to making your homeownership dream a reality.

Analyzing Current Mortgage Interest Rates

Understanding current mortgage interest rates is crucial for anyone looking to buy a house. These rates fluctuate based on various economic factors, impacting monthly payments and overall affordability. Let’s break down the current landscape and its implications for homebuyers.

Current mortgage rates have seen a significant rise, with the 30-Year Mortgage Rate currently at 6.65%. This is a slight decrease from 6.67% last week but still notably higher than the long-term average of 7.71%. Such fluctuations can make a substantial difference in your overall financing strategy.

Key Statistics to Consider

- Historical Context: Between January 2021 and October 2023, mortgage rates escalated from a record low of 2.65% to a peak of 7.79%. This rise has made it essential for borrowers to constantly analyze their options.

- Refinancing Opportunities: With interest rates easing to around 6.5%, approximately 2.5 million borrowers are currently eligible to refinance and save on their monthly payments. If rates were to dip further to 5.5%, over 7 million borrowers could take advantage of refinancing opportunities.

- Monthly Income Impact: A typical household is expected to allocate about 26% of their income towards the principal and interest payments. However, at current rates, many would need to exceed 36% of their income, highlighting affordability challenges.

Comparative Mortgage Rates

| Interest Rate Category | Current Rate | Last Week | Last Year | Long-Term Average |

|---|---|---|---|---|

| 30-Year Fixed Mortgage | 6.65% | 6.67% | 6.87% | 7.71% |

Real-World Examples

- Impact on Homebuyers: Imagine you are looking to purchase a home with a $400,000 mortgage. At the peak rate of 7.79%, your monthly payment could increase by over $1,200 compared to the payments at lower rates. This drastic difference illustrates the importance of timing your mortgage.

- Refinancing Success Stories: Many borrowers who took advantage of the historically low rates in early 2021 have already benefitted significantly. For instance, those who refinanced during that period saved around $5.3 billion annually due to lower interest charges.

Practical Implications for Readers

1. Stay Informed: Regularly track mortgage rates as they can change weekly, impacting your potential payments significantly.

2. Evaluate Your Options: If you secured a mortgage at a higher rate, consider exploring refinancing when rates dip. Utilize resources and calculators available online to assess your potential savings.

3. Consult with Professionals: Speak with mortgage brokers or financial advisors to tailor a financing plan that suits your current financial situation and goals.

As you navigate the current mortgage landscape, remember that even a seemingly small change in interest rates can have profound effects on your budget and long-term wealth-building strategy. Always assess your timing, options, and willingness to adapt to varying market conditions.

Evaluating the Advantages of FHA Loans

When considering financing options for buying a house, FHA loans present unique benefits that cater specifically to various needs. These loans are designed with flexibility and accessibility in mind, making them ideal for many first-time homebuyers and individuals with less-than-perfect credit histories.

Key Advantages of FHA Loans

1. Lower Down Payment Requirements: FHA loans allow you to put down as little as 3.5%. This is a significant advantage if you’re looking to minimize your upfront costs.

2. Flexible Credit Score Requirements: With a minimum credit score of 580 for maximum financing, FHA loans open doors for many potential buyers who may struggle to qualify for conventional loans.

3. Assumable Loans: FHA loans are assumable, which means that if you decide to sell your home, the buyer can take over your mortgage. This can make your property more attractive in a competitive market, especially if interest rates rise.

4. Gift Funds for Down Payment: FHA guidelines allow for the down payment to be covered through gifts from family members, making homeownership feasible for those without substantial savings.

5. Higher Debt-to-Income Ratios Allowed: FHA loans permit higher debt-to-income ratios—up to 57%—enabling buyers to qualify for a loan even with other financial obligations.

| Advantage | FHA Loans | Conventional Loans |

|---|---|---|

| Minimum Down Payment | 3.5% | 5% - 20% |

| Minimum Credit Score | 580 | 620 - 640 |

| Assumable Loans | Yes | No |

| Gift Funds Allowed | Yes | Limited options |

| Maximum Debt-to-Income Ratio | 57% | Typically 43% |

Real-World Examples

- Case Study: Sarah’s Home Purchase: Sarah, a first-time homebuyer with a credit score of 590, utilized an FHA loan to purchase her home with only a 3.5% down payment. By securing FHA financing, she avoided the higher rates and down payment requirements seen in conventional loans, allowing her to buy her dream home sooner.

- Example: The Johnson Family: The Johnson family wanted to buy a larger home but had existing student loans. They opted for an FHA loan because it allowed them to maintain a debt-to-income ratio of 55%, making it possible for them to purchase a house that met their family’s needs.

Practical Implications for Readers

Understanding the unique advantages of FHA loans means you can make informed decisions when stepping into the housing market. If you’re a first-time buyer or someone with limited savings or credit history, an FHA loan might be your best option. Ensure that you explore the possibility of using gift funds for your down payment, as this can substantially reduce the financial burden associated with buying a home.

At this point, consider looking into various lenders to find the best terms for FHA loans. Remember, specific advantages such as assumability could offer added value down the line when you decide to sell or refinance. Understanding these elements can greatly influence your purchasing power and overall financial well-being when buying your home.

Understanding Down Payment Assistance Options

Thinking about buying a home but worried about affording a down payment? You’re not alone! Down payment assistance options can be a game-changer, helping you bridge the gap between your savings and the upfront costs of homeownership. Let’s dive into the various forms of assistance available and how they can support your journey to homeownership.

Types of Down Payment Assistance Programs

When exploring down payment assistance options, you’ll find several avenues to consider:

- Grants: These are funds you don’t have to repay, often provided by state or local governments. They can cover a portion or even the entirety of your down payment.

- Forgivable Loans: Also known as second mortgages, these loans are designed to be forgiven after a set period if you continue to live in the home. For instance, some programs forgive the loan after five years of residency.

- Deferred Loans: These loans allow you to postpone repayment until you sell the home or refinance. This option is helpful if you need immediate help but anticipate a stronger financial position down the line.

Eligibility Criteria

Many down payment assistance programs have specific eligibility requirements that can include:

- Income limits: Typically set at a certain percentage of the area median income.

- Homebuyer education courses: Some programs require you to complete a course that teaches you about the homebuying process.

- First-time homebuyer status: Many programs are specifically designed for individuals or families purchasing their first home.

Comparative Table of Down Payment Assistance Options

| Assistance Type | Repayment Requirement | Typical Amount Available | Specific Eligibility |

|---|---|---|---|

| Grants | None | Up to $10,000 | Varies by program |

| Forgivable Loans | Forgiveness after 5 years | Up to $15,000 | Must live in home |

| Deferred Loans | Due upon sale/refinance | Up to $20,000 | Income limits apply |

Real-World Examples

Let’s examine how down payment assistance options have helped some recent homebuyers:

- Maria’s Home Journey: Maria, a single mother, utilized a local grant program that provided $7,500 to help with her down payment. Her application was accepted due to her income being 80% of the area median, which qualified her for the grant.

- James and Kelly’s Forgivable Loan: This couple secured a forgivable loan of $15,000 from a state program. After living in their new home for five years, the loan was wiped away, allowing them to use their funds for future savings.

Practical Implications for You

Understanding the various down payment assistance options means you can take action towards homeownership more effectively. Here are a few tips:

- Research programs specific to your state or locality; they often offer substantial help.

- Consider taking a homeownership education class to enhance your eligibility and understanding of the process.

- Keep track of deadlines and program requirements to ensure you submit applications on time.

Key Facts and Actions

- Up to $10,000 can be available through grant programs; researching these can offer you quick relief.

- Forgivable loans often require you to stay in your home for a period—ensure this aligns with your plans.

- Always double-check eligibility criteria: they can significantly affect your chances of receiving assistance.

Understanding these down payment assistance options can empower you to make informed decisions on your path to homeownership.

Real-Life Success Stories of Homebuyers

When considering your journey to homeownership, real-life success stories can offer hope and inspiration. They often showcase how different financing options allowed individuals and families to achieve their dreams of owning a home. Let’s explore some powerful examples of homebuyers who made it happen against the odds.

Inspiring Homebuyer Journeys

1. Young Couple’s Triumph

- A couple in their late twenties, both teachers, faced a high rental market in their city. They utilized an FHA loan, which allowed them to buy their first home with a low down payment of just 3.5%. After learning about additional state grants, they secured $10,000 in down payment assistance, making homeownership a reality without crippling debt.

2. Single Parent Success

- A single mother of two navigated her way through financial challenges, utilizing a USDA loan due to her rural location. With a 0% down payment and the support of local housing assistance programs, she purchased a charming home that provides stability for her children. This success story highlights how USDA financing options can open doors for those in eligible areas.

3. Veteran’s Journey Home

- A veteran returning from active duty bought his first home through a VA loan, which offered him competitive interest rates and no down payment. With assistance from a local veterans’ organization, he learned about the benefits available to him as a veteran homebuyer, ultimately securing a beautiful home in his preferred neighborhood.

Comparative Success Elements

| Homebuyer Type | Financing Option | Key Benefits | Additional Support |

|---|---|---|---|

| Young Couple | FHA Loan | Low down payment (3.5%) | $10,000 state grant for assistance |

| Single Parent | USDA Loan | 0% down payment | Local housing assistance programs |

| Veteran | VA Loan | No down payment | Resources from veterans’ organizations |

Real-World Examples

- Maria and Jason’s Story: This couple from Arizona faced obstacles with their credit scores. Participating in a housing counseling program empowered them to improve their finances. They applied for an FHA loan and, with a minimal down payment, purchased a cozy home that doubled their living space.

- Mark’s Path: After years of renting, Mark decided it was time to invest in his future. He opted for a conventional loan after consulting a financial advisor, who helped him strengthen his credit. With a 5% down payment, he became a homeowner and now enjoys tax benefits along with his mortgage.

Actionable Insights

- Before you embark on your homebuying journey, seek out local programs that provide down payment assistance or grants. Many homebuyers have eradicated upfront costs by tapping into these resources.

- Consider workshops or counseling sessions on financial literacy to prepare for the credit and financing aspect of homeownership, just like many of the successful buyers.

- Don’t underestimate the power of networking within your community. Local organizations often provide valuable insights and support systems that can lead you to success.

Keep these inspiring success stories at the forefront of your homebuying journey. They highlight that, with the right financing options and support, achieving homeownership is indeed possible for everyone.

Breaking Down Closing Costs and Fees

When it comes to buying a house, closing costs can feel a bit overwhelming. Understanding these costs is crucial to ensure you’re fully prepared for your new financial commitment. Let’s dive into what these costs entail and how they can affect your budget.

What Are Closing Costs?

Closing costs encompass a variety of fees that arise during the home buying process, typically ranging from 2% to 5% of the home’s purchase price. These fees cover several necessary expenditures such as:

- Lender Fees: These are fees charged by the lender for processing the mortgage. This may include an application fee, underwriting fees, or funding fees.

- Title Insurance: Protects you and your lender against legal claims on the property.

- Escrow Fees: Fees charged when a third party holds the funds and documents until closing.

- Property Taxes: Often prorated and paid upfront at closing.

- Home Inspection Fees: These fees are for a professional inspection to assess the property’s condition.

Average Breakdown of Closing Costs

Here’s a snapshot of the types of fees you can expect and their average percentages:

| Fee Type | Average Percentage of Closing Costs |

|---|---|

| Loan Origination Fee | 0.5% - 1% |

| Title Insurance | 0.3% - 0.5% |

| Property Taxes | 1% - 1.5% |

| Escrow Fees | 0.5% - 1% |

| Inspection Fees | $300 - $500 |

Real-World Examples

Let’s take a closer look at some real-life scenarios to highlight how closing costs can impact your overall home purchase.

- Example 1: A buyer purchasing a $300,000 home could expect to pay around $6,000 in closing costs (at 2%). If the lender’s origination fee is 1% ($3,000), it means the remaining $3,000 would cover other costs like title insurance and inspections.

- Example 2: Another buyer might be closing on a $400,000 home, leading to an estimated $12,000 total in closing costs. If their escrow fees are $2,000 and title insurance costs $1,200, they must still plan for other fees, like property taxes.

Practical Implications

Understanding closing costs allows you to budget more effectively. Here are some actionable points to consider:

- Ask the Seller: In some cases, you can negotiate for the seller to cover part of the closing costs.

- Get Quotes Early: Request estimates from different lenders and title companies to find the best rates.

- Budget Accordingly: Prepare for these costs early in your home-buying process to avoid financial strain.

Specific Facts on Closing Costs

- Closing costs can vary significantly by state. For example, buyers in Texas may encounter different average fees compared to those in Florida.

- Many lenders are required to provide a Loan Estimate form, which breaks down what your expected closing costs will be. Make sure to review these documents.

- Don’t forget about potential ongoing costs after closing, which can influence your budget moving forward.

By being informed and proactive, you can break down closing costs and fees into manageable components, making your home-buying experience much smoother and more predictable.

Leveraging Personal Savings for Home Purchase

When it comes to buying a home, your personal savings play a pivotal role in shaping your financial landscape. By strategically leveraging your savings, you can enhance your purchasing power, lower your debt burden, and ultimately enjoy a smoother path to homeownership.

Understanding the Importance of Personal Savings

Your personal savings serve as a foundation for your home purchase. Not only do they help you meet down payment requirements, but they can also influence your mortgage terms. Here are a few benefits of using your savings:

- Lower Down Payment: Larger savings can allow you to make a more substantial down payment, often reducing your loan amount.

- Better Loan Terms: Significant savings may lead to lower interest rates and better mortgage terms due to reduced risk to lenders.

- Reduced Private Mortgage Insurance (PMI): If your down payment is 20% or more, you can avoid PMI, which can save you hundreds monthly.

Key Savings Statistics

Consider these important data points when utilizing personal savings for your home purchase:

- 20% Down Payment: Aiming for a 20% down payment can reduce your mortgage balance significantly, bringing you closer to being mortgage-free.

- Savings Percentage: Research suggests that individuals with substantial savings (greater than 15% of the home price) can negotiate better terms with lenders, impacting interest rates positively by up to 0.5%.

Comparative Table: Impact of Different Down Payment Percentages

| Down Payment Percentage | Impact on Loan Amount | PMI Required | Monthly Payment Reduction |

|---|---|---|---|

| 5% | Higher loan balance | Yes | Limited |

| 10% | Moderate loan balance | Yes | Moderate |

| 20% | Lower loan balance | No | Significant reduction |

Real-World Examples

- Case Study 1: Sarah accumulated $50,000 in savings over five years. When she decided to buy a $250,000 house, her 20% down payment allowed her to avoid PMI and secure a lower interest rate, bringing her monthly payments down significantly.

- Case Study 2: John and Maria saved $30,000, enough for a 10% down payment on a $300,000 home. While they faced PMI costs, their substantial savings improved their debt-to-income ratio, giving them an edge in negotiating a better mortgage rate.

Practical Implications for Homebuyers

To maximize the benefits of your personal savings:

- Start Early: Begin saving as soon as possible and consider automating your savings plan to build a robust fund.

- Set Clear Goals: Define how much you wish to save and what percentage of the home price that will cover, adjusting your target based on market conditions.

- Invest Wisely: Consider high-yield savings accounts or Certificates of Deposit (CDs) to grow your funds while you save.

Given that 20% down payments can significantly alleviate future financial burdens, aim to match or exceed this benchmark for an optimized purchasing experience.