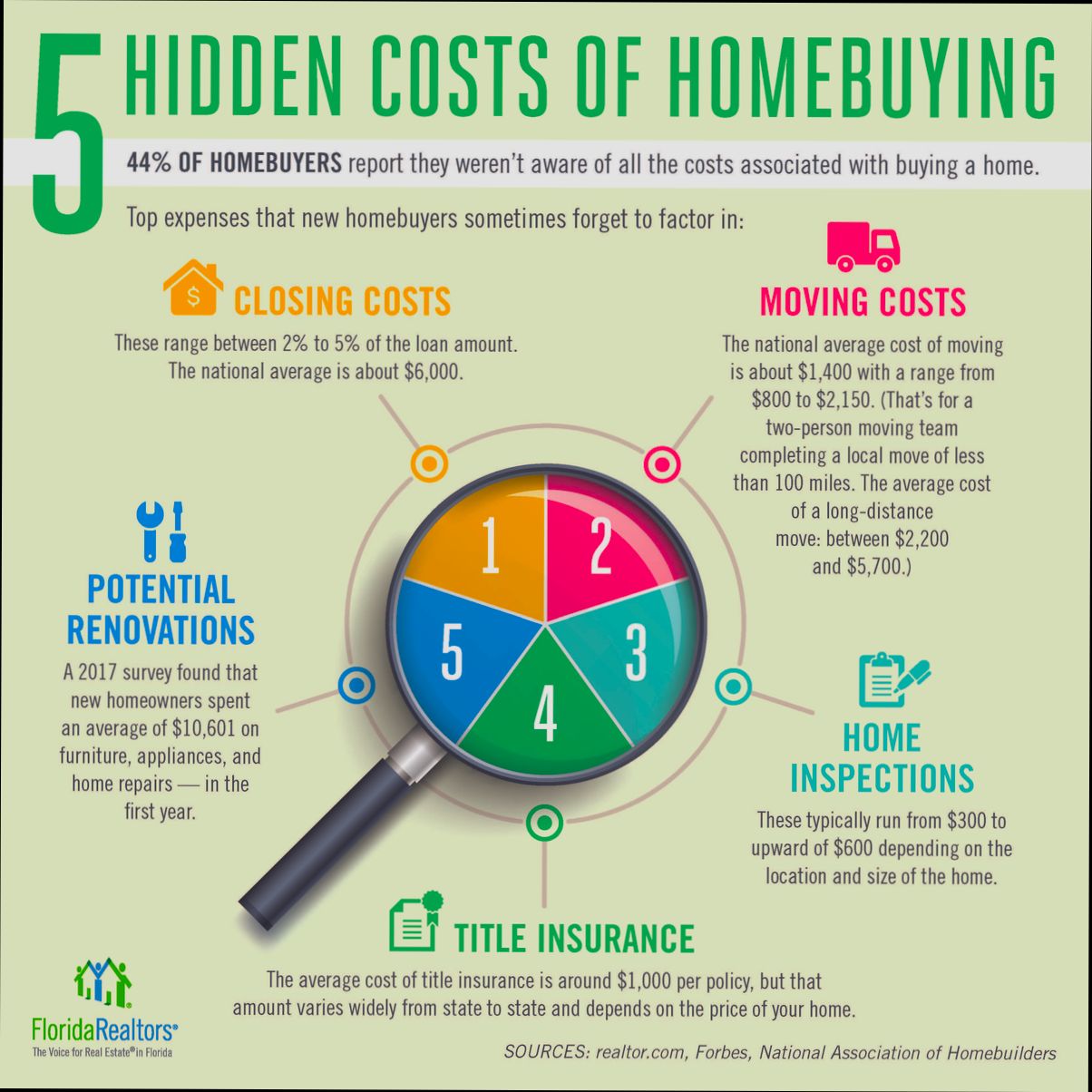

Costs, taxes, and hidden charges when buying property can feel like a minefield if you’re not ready for them. Picture this: you’ve found your dream home listed at $300,000, and you’re already drafting your housewarming invite. But wait—did you factor in closing costs? Depending on where you live, that can add anywhere from 2% to 5% on top of your purchase price. So, suddenly, that dream seems a bit pricier, right? In some states, transfer taxes alone can hit you with a few thousand bucks, and don’t get me started on title insurance. It’s like a surprise fees game that you didn’t sign up for.

And then there are those sneaky charges that can pop up when you least expect them. Let’s talk about inspections—a must-have, no doubt. A typical home inspection might cost you around $300 to $500, but if the inspector finds something like mold or termites, you could be looking at an extra couple thousand dollars to fix it up. On top of that, don’t forget about property taxes that could increase yearly based on local rates. It’s easy to get swept away with the excitement of buying a home, but those hidden costs can turn your budget upside down faster than you can say “escrow.”

Understanding Property Transfer Taxes

When you buy a property, one of the important costs to consider is the property transfer tax. This tax can significantly impact your overall budget, so it’s essential to understand what it is and how it varies by location. Property transfer taxes are typically assessed as a percentage of the purchase price and can often be overlooked during the planning stage.

What to Know About Property Transfer Taxes

Here are some key points regarding property transfer taxes that you should be aware of:

- Tax Rates Vary: Property transfer taxes can range widely—from as low as 0.01% to over 3% depending on the local jurisdiction. For instance, California typically imposes a base rate of 0.11% while New York City can charge up to 2.625% for residential transactions.

- Exemptions and Reductions: Some jurisdictions offer exemptions or reduced rates for first-time homebuyers or low-income purchasers. For example, Washington State provides a reduction for low-income buyers, allowing them to pay up to 50% less in transfer taxes.

- Local Usage: Revenue generated from property transfer taxes often funds local services, such as schools and community infrastructure. In 2022, a study showed that approximately 60% of property transfer tax revenue in urban areas went towards public education.

To put this into perspective, here’s a comparison of some states’ transfer tax rates:

| State | Average Transfer Tax Rate | Additional Local Fees |

|---|---|---|

| California | 0.11% | Up to 1.5% additional in some counties |

| New York | 0.4% (state) + 2.625% (NYC) | Varies widely by county |

| Pennsylvania | 1.0% | May add up to 2% locally |

| Florida | 0.7% | Additional local rates apply |

Real-World Examples

Let’s look at a couple of case studies to highlight how property transfer taxes come into play:

1. Case Study - California: A homebuyer in Los Angeles purchased a property for $800,000. The base transfer tax was approximately $880 (0.11%), but with additional local assessments, the total transfer tax bill reached $6,320, demonstrating the importance of considering local rates.

2. Case Study - New York City: In New York City, a buyer purchasing a condo for $1 million faced a transfer tax of $40,000 (0.4% state fee) plus $26,250 (2.625% NYC fee), totaling $66,250 in transfer taxes alone. This significant expense can impact financial planning for any property transaction.

Practical Implications for Homebuyers

Understanding property transfer taxes can save you from unexpected financial strain. Here are some actionable tips:

- Research Local Rates: Before making a purchase, research the local transfer tax rates. Many county websites provide current rates and information on exemptions.

- Consult Professionals: Always consult with a real estate agent or tax advisor regarding how transfer taxes apply to your situation. They can help you navigate any complexities or potential savings.

- Include in Budget: Factor property transfer taxes into your overall budget when purchasing a home. Failing to do so could lead to surprises at closing.

By being informed about property transfer taxes, you can ensure a smoother purchasing process and avoid any hidden charges that may spring up unexpectedly.

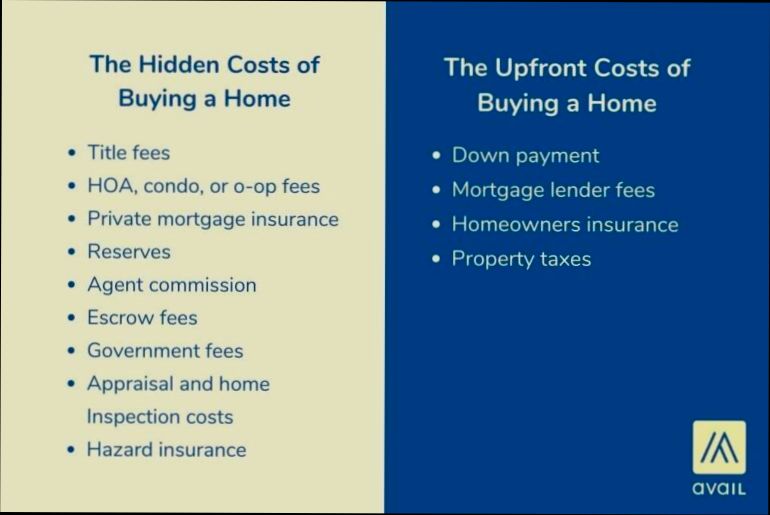

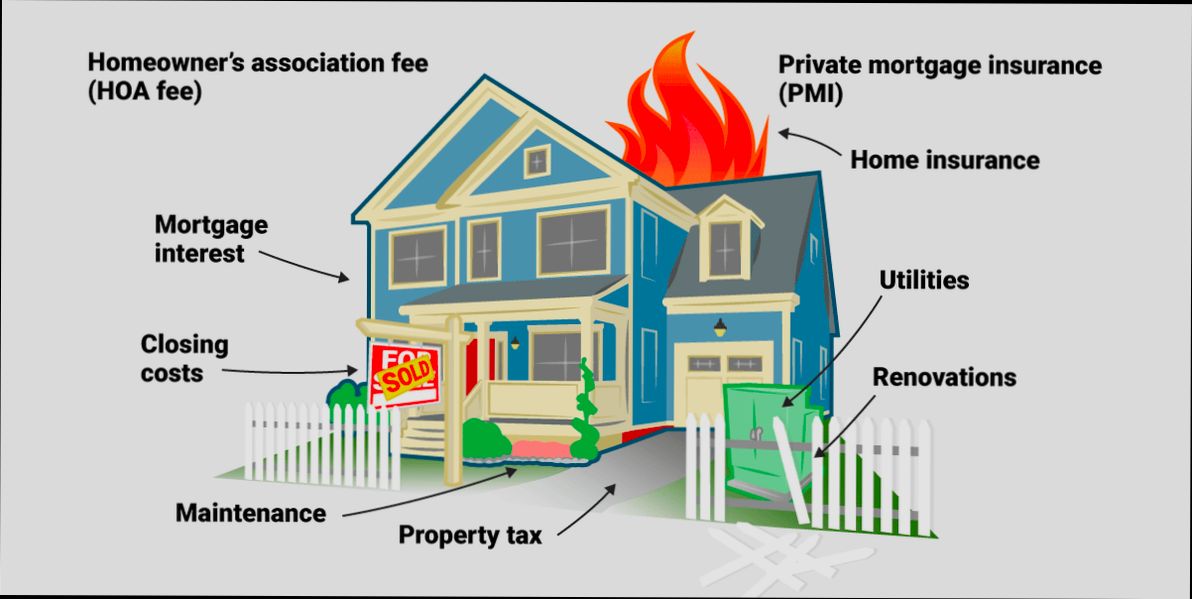

Identifying Hidden Fees in Real Estate

When diving into real estate, you might think you’ve accounted for all costs, but hidden fees can sneak up on you. Identifying these hidden fees is crucial to avoid financial headaches down the road. Let’s explore what to look for so you can be financially savvy and prepared.

Common Hidden Fees to Watch For

Hidden fees in real estate can come from various sources. Here are some common ones to be aware of:

- Home Inspection Fees: While not technically hidden, these can range from $300 to $500 or more, depending on the property’s size and location. It’s easy to overlook this, especially if inspections are optional.

- Homeowners Association (HOA) Fees: If you’re buying in a community with an HOA, be aware that fees can go up to 1% of your home’s value per year. Always ask for full disclosure of any HOA dues and potential increases.

- Closing Costs: Often ranging between 2% to 5% of the loan amount, closing costs include numerous fees like title insurance, recording fees, and more. Sometimes buyers only budget for the down payment.

- Escrow Fees: These fees can add anywhere from $500 to $2,000 depending on the transaction’s complexity. Knowing if your agreement stipulates who pays these fees can save you a surprise.

Comparative Overview of Hidden Fees

| Fee Type | Typical Cost Range | Commonly Overlooked By Buyers |

|---|---|---|

| Home Inspection Fees | $300 - $500 | Yes |

| Homeowners Association Fees | Up to 1% of home value | Often |

| Closing Costs | 2% - 5% of loan amount | Frequently misunderstood |

| Escrow Fees | $500 - $2,000 | Yes |

Real-World Examples

In a case study, a couple completely overlooked a $1,200 HOA fee when purchasing their condo. They were shocked by the additional monthly $100 cost that they hadn’t factored into their budget. Similarly, another homebuyer discovered $1,800 in closing costs after believing they would only pay the down payment.

Practical Implications for You

To avoid being caught off guard, make it a point to:

- Request a Detailed Fee Schedule: Always ask for a comprehensive list of all potential fees as part of your purchasing agreement.

- Consult Your Realtor: Experienced agents often have insights on common hidden fees in specific neighborhoods.

- Review Closing Statements Carefully: Before signing, scrutinize the closing statement for any mysterious charges or fees.

Actionable Advice on Identifying Hidden Fees

Be proactive about asking questions and conducting thorough research. Establish a budget that extends beyond the down payment and includes at least an additional 5% to cover unforeseen fees. This way, you’ll navigate your property purchase with confidence and save yourself from unexpected financial surprises.

Analyzing Costs: Market Trends and Data

When it comes to buying property, understanding costs through a market analysis lens is crucial. It helps you anticipate expenses, uncover hidden charges, and make informed decisions. Let’s examine some pivotal aspects of this area, focusing on the trends and data that shape our understanding of costs related to property transactions.

Understanding Cost Trends

This section highlights the importance of cost trends in making property-buying decisions. By analyzing historical data, we can detect patterns that significantly affect real estate costs.

1. Cost Growth Indicators:

- Over the past five years, production costs in real estate have risen by approximately 15%, largely driven by material shortages and labor costs.

- Understanding these trends can guide you in timing your property purchase effectively.

2. Regional Variations:

- Differences in regional costs showcase significant disparities; for example, urban properties can cost up to 30% more than their suburban counterparts.

- It’s essential to analyze local market trends, as they can vary dramatically from national averages.

3. Fluctuation Patterns:

- Factors influencing cost trends, such as economic shifts and policy changes, can create fluctuations. For instance, the implementation of new zoning laws in various states has led to increased property values by as much as 20%.

Comparative Costs Table

| Region | Average Property Cost | Average Cost Increase Last Year | Economic Growth Rate (%) |

|---|---|---|---|

| Urban Areas | $450,000 | 8% | 4% |

| Suburban Areas | $300,000 | 5% | 3% |

| Rural Areas | $200,000 | 2% | 1% |

Real-World Examples

- A recent study of costs in the New York City real estate market revealed that property prices soared by 12% following new infrastructure projects. This showcases how market trends can lead to sudden increases in costs.

- In contrast, research indicates that the lower price growth in rural markets—п2% annually—reflects the stagnation in job opportunities, suggesting a connection between economic factors and real estate pricing.

Practical Implications for You

As you navigate the property market, consider the following actionable steps:

- Stay Informed: Regularly access market reports to keep abreast of cost trends in your desired location. Utilize online platforms that aggregate data on property values and market dynamics.

- Evaluate Timing: Factor in economic projections when planning your purchase. Buying before anticipated price increases can save significant amounts in the long run.

- Consider Multiple Markets: Broaden your search to include communities with varied markets. By exploring suburban or rural options, you may find more affordable alternatives.

If you stay proactive and informed about market trends and data, you can position yourself advantageously in the real estate landscape, potentially avoiding unforeseen costs and enhancing your investment decisions.

Practical Examples of Buyers’ Additional Expenses

When purchasing a property, it’s crucial to consider a wide range of additional expenses that can arise unexpectedly. You might think you’ve covered the major costs, but several extra expenses can sneak into your budget, impacting your overall financial plan. Let’s explore some practical examples of these additional expenses that you should keep in mind as you navigate property buying.

Common Additional Expenses to Consider

1. Homeowners Insurance: This is often a requirement by lenders. Depending on your property’s location and value, homeowners insurance can range from $600 to $2,000 annually.

2. Closing Costs: These are fees associated with the purchase transaction, which can include attorney fees, title insurance, and appraisal fees. Buyers typically pay between 2% to 5% of the total loan amount in closing costs.

3. Property Taxes: These can add a significant amount to your monthly expenses. For example, property tax rates can vary widely—around 1% to 3% of the home’s assessed value annually.

4. Maintenance and Repairs: It’s wise to budget for future upkeep. A common recommendation is to set aside 1% to 2% of the home’s value each year for maintenance.

5. Utilities In Advance: Some homes may require you to pay utilities upfront on closing, which can range from $200 to $500 depending on your service providers.

Breakdown of Estimated Additional Expenses

| Expense Type | Estimated Range |

|---|---|

| Homeowners Insurance | $600 - $2,000 annually |

| Closing Costs | 2% - 5% of loan amount |

| Property Taxes | 1% - 3% of property value |

| Maintenance and Repairs | 1% - 2% of home value |

| Utilities In Advance | $200 - $500 upfront |

Real-World Examples

Looking at real-world scenarios, let’s consider different instances of buyers facing additional expenses:

- Case Study 1: A couple purchasing a $300,000 home learned that homeowners insurance cost them $1,200 a year. They also incurred closing costs of about 3%, totaling $9,000, plus property taxes coming out to roughly 1.25% of their home’s value, adding another $3,750 annually.

- Case Study 2: An investor bought a rental property for $400,000. In addition to a $12,000 expense for closing costs, they had to allocate around $5,000 for immediate repairs to make the property tenant-ready, while budgeting 1% yearly for ongoing maintenance.

Practical Implications

Being aware of these additional expenses can help you avoid financial strain. Here are some practical steps you can take:

- Budget for Homeowners Insurance: Research local rates early in your home-buying journey to anticipate this recurring cost.

- Calculate Closing Costs: Use your home’s purchase price to calculate expected closing costs accurately, and consider this in your savings objectives.

- Set Aside Maintenance Funds: Develop a maintenance savings plan, starting with 1% of your home’s value long before you purchase.

- Prepare for Unforeseen Utility Costs: Include advance utility payments in your initial budgeting to manage cash flow better.

- Review Property Tax Assessments: Check local property tax rates and any exemptions you may qualify for, which can help manage those ongoing costs.

Familiarizing yourself with these additional expenses will empower you as a buyer and help you plan more effectively for this significant investment.

The Benefits of Foreseeing Property Costs

When it comes to purchasing a home, being proactive about property costs can save you from a world of financial surprises. Understanding potential expenses before you buy not only helps you budget better but also empowers you to make informed decisions throughout the buying process.

Key Points on the Benefits of Foreseeing Property Costs

1. Avoiding Financial Strain: By foreseeing property costs like property taxes and homeowners insurance, you can avoid unexpected financial strain. For instance, homeowners insurance can average $1,200 annually, while property taxes can vary widely by location, sometimes exceeding $5,000 per year. Having these figures ahead of time lets you prepare adequately.

2. Planning for Maintenance and Repair Costs: Homeowners often underestimate the costs associated with maintenance. On average, it’s recommended to budget 1%-3% of your home’s value annually for upkeep. For example, on a $300,000 home, that’s $3,000 to $9,000 in maintenance every year.

3. Understanding Closing Costs: Closing costs can range from 2% to 5% of the purchase price of your home. By anticipating this expense, you can save more efficiently. Knowing that on a $250,000 home, you might need to budget between $5,000 and $12,500 for closing costs can refine your mortgage financing plans.

4. Identifying Hidden Costs: By researching what to expect in terms of hidden costs—such as HOA fees, which can average $200 monthly, or odd days interest at closing—you help safeguard your financial future. Some buyers are caught off guard when these fees are added to their budget unexpectedly.

Comparative Table of Common Property Costs

| Cost Type | Estimated Annual Cost |

|---|---|

| Property Taxes | $5,000 (varies by location) |

| Homeowners Insurance | $1,200 (average) |

| HOA Fees | $2,400 ($200/month) |

| Maintenance | $3,000 to $9,000 (1%-3% of home value) |

| Utilities | $2,400 (approx. $200/month) |

| Closing Costs | $5,000 to $12,500 (2%-5% of home price) |

Real-World Examples of Property Cost Foreseeing

Consider the case of Lisa, a first-time homebuyer, who meticulously researched the typical hidden costs associated with her target neighborhood. She learned that the local HOA fee was $250 monthly and that property taxes were higher than the national average, around $6,000. With this foresight, Lisa adjusted her budget accordingly, avoiding any financial strain after her purchase.

In another example, Tom, buying in a coastal area, knew that the maintenance costs for flood insurance would add $1,000 to his yearly expenses, in addition to regular homeowners insurance. By factoring this into his overall budget, he found the right home while staying within his financial limits.

Practical Implications for Foreseeing Costs

To make the most of these benefits, engage in thorough research before making an offer on a property. Gather estimates from trusted sources, including speaking to current homeowners in the area and local real estate professionals. This will not only give you a clearer picture of expected costs but will also help you negotiate better terms during the buying process.

Actionable Advice on Foreseeing Property Costs

- Always include a buffer in your budget for unexpected expenses. Aim for 10%-15% above your estimated totals.

- Use online calculators to assess property taxes based on your target area, and don’t forget to factor in seasonal changes in utility costs.

- Consult with a financial advisor to better organize your budget concerning hidden charges; even small amounts can add up over time and influence your long-term financial health.

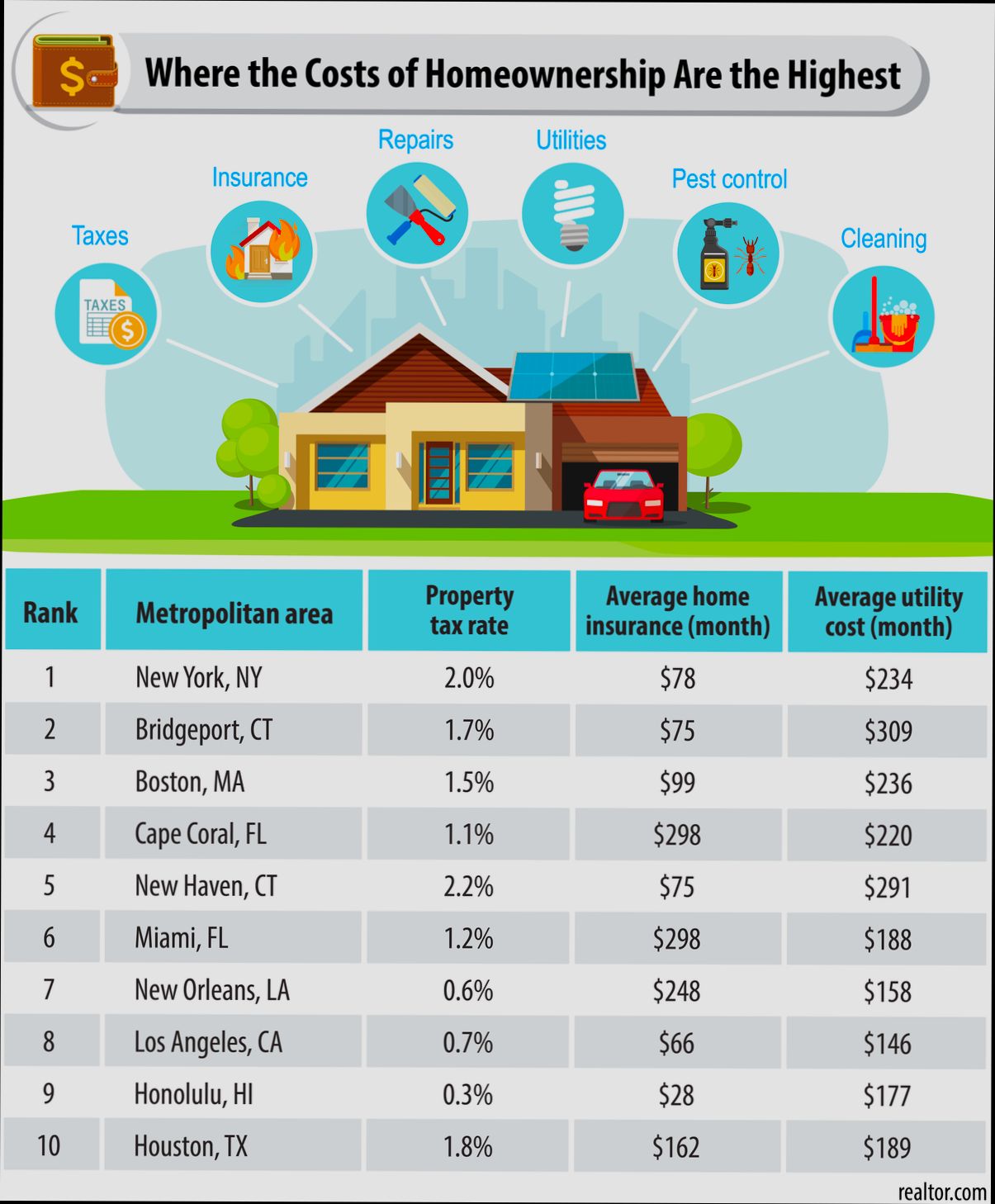

Impact of Local Taxes on Home Buying

When you’re considering buying a home, it’s essential to understand how local taxes can dramatically influence your decision-making. Local taxes include various types of levies like property taxes and land value taxes (LVT), which can affect overall affordability and market dynamics.

Key Impacts of Local Taxes on Home Buyers

- Influence on Home Prices: Research indicates that homes located in areas with high property taxes often face a decreased demand. In contrast, properties in low-tax areas can see a rise in prices due to higher attractiveness to buyers. For instance, areas with a property tax rate exceeding 2% can experience a sharp decline in home buyer interest.

- Affordability Concerns: Elevated local taxes increase monthly mortgage payments, which can stretch your budget thin. For example, if a property has an annual tax of $3,000, that adds approximately $250 to your monthly costs, affecting your purchasing power.

- Long-Term Financial Planning: Taxes based on property value can shift your financial strategy. If the assessed value of your potential home rises significantly, as can be the case in rapidly appreciating markets, you may need to suddenly reassess your financial capabilities for future payments.

- Market Variation and Local Economies: Local taxes not only contribute to public services but can also dictate the vibrancy of local economies. Municipalities that rely heavily on property taxes might limit their growth through high tax burdens, pushing buyers to seek opportunities in neighboring, lower-tax areas.

Comparative Overview of Property Tax Rates

| State/Region | Average Property Tax Rate (%) | Median Home Price ($) | Monthly Property Tax ($) |

|---|---|---|---|

| Coastal States | 1.2% | 500,000 | 500 |

| Midwestern States | 1.5% | 250,000 | 312.50 |

| Southern States | 0.9% | 300,000 | 225 |

| Northeastern States | 2.1% | 400,000 | 700 |

In this table, you can see how property tax rates vary by state and how they directly impact your monthly tax burden based on median home prices. Understanding these differences allows you to evaluate your options more clearly.

Real-World Examples

Consider the case of a family looking to move to a suburb of Chicago, where local property taxes are known to be high. They find a charming neighborhood with a property tax rate of 2.1%. Although the home price is attractive at $400,000, the tax liability translates to a staggering $700 a month, forcing them to consider other areas with lower taxes. In contrast, a similar family relocating to a southern state like Texas finds a property with a median price of $300,000 and pays only $225 monthly in taxes, leaving them with more disposable income.

Practical Implications for Home Buyers

As you navigate the home-buying process, keep the following points in mind regarding local taxes:

1. Evaluate Tax Burdens: When reviewing properties, factor in the property tax rates to accurately assess your total monthly costs.

2. Research Local Tax Trends: Analyze trends in property valuations and tax rates in the neighborhoods you are considering, to project any potential future tax increases.

3. Consider Resale Value: Buying in higher tax areas might affect the home’s future marketability. Research if the tax burden negatively impacts demand in that locale.

Actionable Insights

- If you’re eyeing a property with a high land value tax, check if the local government offers any relief programs for property owners, especially for first-time buyers or those on fixed incomes.

- Before making your final decision, consult with a local tax advisor to better understand how property taxes will impact your budget and long-term financial health.

By actively assessing how local taxes affect your home-buying journey, you can make well-informed decisions that suit your financial landscape.

Navigating Mortgage Insurance and Its Charges

Understanding mortgage insurance is key when diving into the costs associated with buying property. It protects lenders in case you default on your loan, especially if your down payment is less than 20%. Let’s break it down so you can navigate this often-misunderstood terrain with confidence.

What Is Mortgage Insurance?

Mortgage insurance comes into play primarily when you’re borrowing a significant amount and don’t have a large down payment. It’s designed to reduce the risk for lenders, allowing them to offer loans to individuals who may not meet traditional lending criteria. The insurance can vary in cost and structure, so it’s essential to know your options.

Types of Mortgage Insurance

- Private Mortgage Insurance (PMI): Required for conventional loans, PMI protects the lender if you default. Rates generally range from 0.3% to 1.5% of the original loan amount annually.

- Mortgage Insurance Premium (MIP): For FHA loans, borrowers pay MIP regardless of their down payment. Annual rates can be around 0.45%, making it a potentially more affordable avenue compared to PMI for some buyers.

Cost and Payment Options

The costs of mortgage insurance can add up quickly. Here’s how you can pay for it:

- Monthly Payments: You can opt to pay mortgage insurance monthly, typically rolled into your escrow account.

- Upfront Payments: Alternatively, you could make a lump sum payment when the loan is originated.

- Split Payments: Some borrowers choose to split the cost, paying part upfront and the remainder monthly.

- Lender-Paid Insurance: You could let the lender pay for it, but be cautious—the rate may be higher throughout the life of the loan.

Comparative Costs Table

| Type of Mortgage Insurance | Annual Rate Range | Upfront Payment Requirement | Payable Monthly Option | Loan Type |

|---|---|---|---|---|

| Private Mortgage Insurance (PMI) | 0.3% - 1.5% | No | Yes | Conventional |

| FHA Mortgage Insurance (MIP) | Approx. 0.45% | Yes (in some cases) | Yes | FHA Loans |

Real-World Examples

Consider Jane, who is buying her first home for $300,000. She can only afford a 10% down payment. That means she would likely face PMI. If her PMI rate is set at 1%, she’d pay approximately $3,000 annually or $250 monthly.

On the flip side, David is going the FHA route with a lower annual MIP of 0.45%. His $300,000 loan with a similar 10% down payment would result in an MIP of roughly $1,350 annually, or about $112.50 monthly. This illustrates the impact of selecting different mortgage insurance types on your overall payments.

Practical Implications

As you move forward in your property buying journey, it’s crucial to evaluate the type of mortgage insurance that fits your financial situation. Here are some actionable tips:

- Understand Your Options: Always inquire about both PMI and FHA MIP rates. Depending on your financial health, one may be significantly more beneficial than the other.

- Negotiate with Lenders: Some lenders may offer lower rates for PMI based on your credit score. You might qualify for reductions.

- Consider Total Costs: Look beyond the monthly mortgage payments. Compute your total mortgage costs, factoring in insurance, to weigh your full financial commitment.

Leveraging this knowledge about mortgage insurance can help you make a more informed decision as you progress in your home-buying process.