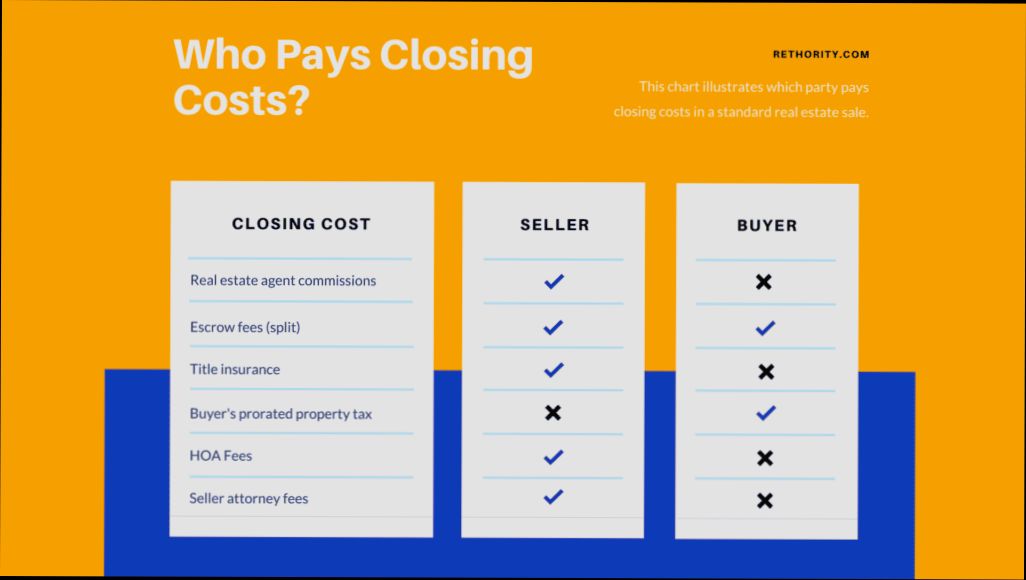

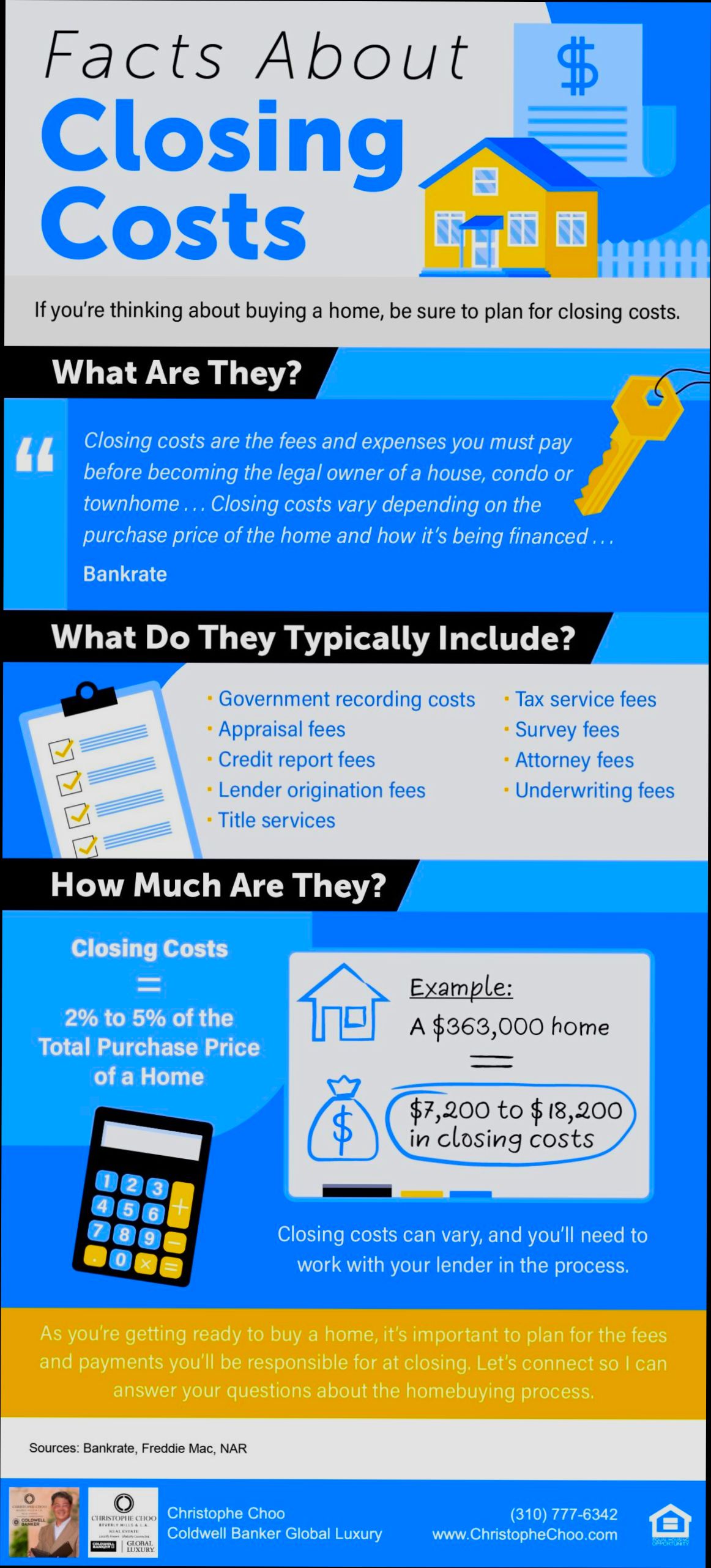

Who Pays Closing Costs in Real Estate can feel like a mystery, especially for first-time buyers and sellers. Did you know that closing costs typically range from 2% to 5% of the purchase price? For a $300,000 home, that could mean shelling out anywhere from $6,000 to $15,000. Ouch! It’s not just about the price tag; understanding who picks up this tab is crucial for your wallet. Buyers often assume they’re responsible for most of these fees—like lender fees, appraisal costs, and title insurance. However, it’s not quite so cut and dry.

On the flip side, sellers also have a significant stake in closing costs. They usually cover the real estate agent’s commissions, which can eat up 5% to 6% of the sale price, along with potential concessions or repair costs. In some cases, buyers might negotiate to have sellers cover a portion of their closing costs as an incentive to close the deal. So, if you’re planning to jump into the real estate game, knowing the ins and outs of who pays what can save you a pretty penny and make the whole process a little less daunting.

Who Typically Covers Closing Costs

Understanding who pays closing costs in a real estate transaction is crucial as it impacts your overall budget. Typically, both buyers and sellers incur costs, but the specific expenses each party pays can vary significantly.

Who Pays Which Closing Costs?

In general, buyers are responsible for the majority of closing costs related to the mortgage and home purchase. However, sellers often come into play as well. Here’s a breakdown of the typical closing costs each party may cover:

- Buyers are likely responsible for:

- Lender fees: These fees usually account for the costs associated with originating and processing the mortgage.

- Home inspection costs: Buyers often pay for this to assess property condition, providing leverage for negotiations.

- Home insurance premiums: Typically due at closing, ensuring coverage begins immediately for the new homeowner.

- Sellers frequently cover:

- Title-related fees: In many places, sellers pay for the owner’s title insurance, especially in states like Florida.

- Transfer taxes: These taxes formally cover the transfer of ownership and are often the seller’s responsibility.

- HOA fees: Sellers must ensure that any homeowners association fees are current up until the day of closing.

| Cost Type | Typically Paid By | Notes |

|---|---|---|

| Lender Fees | Buyer | Includes underwriting and application fees. |

| Home Inspection Fees | Buyer | Optional, but very useful to identify potential issues. |

| Title Insurance (Owner’s) | Seller (in some states) | Protects against future claims related to ownership. |

| Transfer Taxes | Seller | Varies by state; commonly a seller’s cost. |

| Property Taxes | Seller | Paid up until the closing date. |

| Realtor Commissions | Seller (often) | Typically between 2.5% and 3% of the sale price. |

Real-World Examples

To illustrate, let’s consider a case where someone buys a $350,000 home. If the buyer puts down less than 20% (a common scenario), they can expect to pay approximately 2% to 5% in closing fees, which would equate to between $7,000 and $17,500. This includes costs such as lender fees and home insurance premiums.

In contrast, if we look at a seller in Florida, they might be responsible for the owner’s title insurance, which can add up to significant expenses as well. For instance, if the total fee is around $1,500, that amount will be subtracted from their sale proceeds at closing.

Practical Implications

When entering the home buying or selling process, it’s important to clarify who will cover each of the closing costs. This will not only help you budget effectively but also prepare for negotiations. Remember, while many costs are typical for one party to pay, everything is often negotiable. Buyers can discuss asking the seller to cover a portion of their closing costs to make the deal more appealing or equitable.

If you find those closing costs daunting, consider negotiating concessions where sellers might agree to pay some costs or fix repairs found during a home inspection, which can also elevate your bargaining power.

Actionable Advice

- Before the closing date, ensure you have a clear understanding of which costs you will be responsible for and those that may be negotiable.

- Leverage your realtor’s experience to identify potential areas for negotiation regarding closing costs.

- Always request a closing cost estimate ahead of time; this will provide clarity about what to expect and assist both parties in preparing adequately for a smoother transaction.

Impact of Closing Costs on Buyers

Understanding the impact of closing costs on you as a buyer is essential for budgeting your home purchase. These costs can add a significant amount to your overall expenses, and knowing how they affect you can help you make informed financial decisions.

Key Factors in Closing Costs

Several specific fees you incur as a buyer can significantly affect your total closing costs:

- Appraisal Fees: You usually pay this fee, which averages between $300 and $700. It ensures the property’s value meets the loan amount, directly linking to how much you can borrow.

- Home Inspection Fees: Typically ranging from $300 to $500, you bear this cost, which helps identify potential issues with the property before the sale is finalized. Problems found can lead to negotiations that affect the purchase price.

- Title Insurance: Though this can be a seller’s responsibility, buyers often pay for their own policy, typically costing around 0.5% to 1% of the home’s purchase price. This insurance protects you against any legal issues related to ownership.

- Other Third-Party Charges: These include escrow, courier, and recording fees. While their individual amounts may seem small—averaging around $100 or less each—they can add up to hundreds of dollars collectively.

Table of Common Closing Costs for Buyers

| Fee Type | Average Cost | Description |

|---|---|---|

| Appraisal Fee | $300 - $700 | Required to confirm the home’s value matches loan amount. |

| Home Inspection Fee | $300 - $500 | Assesses the home’s condition and identifies necessary repairs. |

| Title Insurance | 0.5% - 1% of Price | Protects against ownership-related legal issues. |

| Escrow Fee | $300 - $700 | Facilitates the transfer of funds and documents. |

| Courier/Notary Fees | $100 each | Necessary administrative costs for document handling. |

Real-World Examples

Let’s consider a scenario where you’re purchasing a home for $350,000. Here’s how closing costs might impact your finances:

- Appraisal Scenario: If the appraisal comes in at $340,000, you might face negotiation challenges, as the lender may not approve the loan for the originally agreed price. This can lead to extra costs or the need for a larger down payment.

- Inspection Findings: Suppose your inspection uncovers major issues that require repairs costing $5,000. As a buyer, you can negotiate with the seller to either reduce the purchase price or handle repairs before closing, effectively lowering your upfront expenses.

Practical Implications for Buyers

As a buyer, these closing costs significantly impact your budget, often totaling between 2% to 5% of the purchase price. Here are some actionable insights:

- Budget Accordingly: Always factor in these additional costs when determining how much house you can afford. Include both expected fees and a buffer for surprises or necessary repairs.

- Negotiate Wisely: Use findings from the home inspection to negotiate better terms or concessions from the seller, which can reduce your overall closing costs.

- Shop Around for Services: Some third-party fees can vary based on the providers. For services like home inspections or title insurance, consider obtaining multiple quotes to choose the most cost-effective options.

Being knowledgeable about these fees helps you navigate the process more efficiently and supports your financial preparedness when buying a home. Understanding their potential impact might even lead you to negotiate better terms or find ways to reduce certain fees.

Statistics on Closing Costs Across States

When diving into the real estate world, understanding the statistics on closing costs across states can greatly impact your financial planning. Closing costs can vary significantly based on geographical location, so it’s essential to be informed.

Variations in Closing Costs by State

Across the United States, closing costs can differ drastically depending on the state. Here are some key statistics that highlight these differences:

- The average closing costs in the U.S. range from $3,000 to $5,000.

- In states like Texas and New York, closing costs can exceed 5% of the home’s purchase price due to higher fees and taxes.

- In contrast, states like Mississippi and Arkansas often see closing costs around 3% of the purchase price.

- A recent survey showed that California ranks among the highest, with buyers potentially facing up to $25,000 in closing costs for more expensive properties.

Comparisons of Average Closing Costs by State

| State | Average Closing Costs | Percentage of Purchase Price |

|---|---|---|

| Texas | $4,667 | 3.5% |

| New York | $7,000 | 5.1% |

| California | $25,000 | 4% |

| Mississippi | $3,000 | 2.9% |

| Arkansas | $3,250 | 3% |

Real-World Examples

In a recent real estate transaction in New York City, a buyer faced closing costs totaling around $10,000 on a property priced at $200,000, showcasing a whopping 5% cost burden. Similarly, in Dallas, a buyer of a $300,000 home encountered closing costs of approximately $9,000, amounting to 3%.

Another case involved a buyer in San Francisco, where the closing costs on a $1 million property reached an astounding $30,000. This correlates with California’s noted average of high closing costs that can easily overwhelm first-time buyers.

Practical Implications for Readers

Understanding these statistics allows you to better anticipate and prepare for closing costs when buying a home. For instance, if you’re planning to purchase in a high-cost state like New York, budgeting an additional 5% of your total purchase price specifically for closing costs is wise.

Awareness of these variations enables you to negotiate more effectively during the home-buying process. For example, knowing that closing costs are negotiable can empower you to request the seller to cover some fees, particularly in slower markets.

Specific Facts for Actionable Advice

- Always research your specific state’s closing costs before proceeding with a purchase.

- Getting a detailed estimate during the loan application process can give you a clearer idea of potential expenses.

- Consider looking into state-specific programs that assist buyers with closing costs; some states may offer grants or reduced fees that can alleviate your financial burden.

Advantages for Sellers Paying Closing Costs

When it comes to closing costs in real estate, there’s a surprising benefit for sellers who choose to cover these expenses. Paying part or all of the closing costs can ultimately make a property more attractive to potential buyers. Let’s explore the key advantages.

Enhancing Buyer Appeal

By offering to pay closing costs, you instantly make your listing more enticing. This strategy speaks directly to potential buyers, particularly first-time buyers who may be cash-strapped. A survey revealed that nearly 60% of first-time homebuyers cite closing costs as a significant barrier to purchasing a home. By alleviating this burden, you can differentiate your property in a competitive market.

Quick Sales and Increased Offers

Opting to pay closing costs can lead to quicker sales. Homes that make such offers tend to attract more attention and can generate multiple offers. A recent analysis showed that homes with seller-paid closing costs sold 10% faster on average than those without. This rapid sale can be crucial in a market where time is of the essence.

Greater Negotiation Flexibility

Covering closing costs can provide leeway in negotiations. By offering to chip in on these expenses, you can negotiate other terms of the sale, such as a higher sale price. According to data, 30% of sellers who paid closing costs managed to negotiate a sale price that was at least 5% above their initial asking price.

Financial Incentive for Buyers

Sellers who pay closing costs can create a win-win situation by providing buyers with additional financial flexibility. This often allows buyers to channel extra funds toward home improvements or moving expenses. Research shows that 75% of buyers express that seller concessions influence their purchase decision positively. As a seller, this means your home could be their top choice.

| Advantage | Percentage Impact | Summary |

|---|---|---|

| Buyer Appeal | 60% of first-time buyers | Reduces buyer hesitation over costs |

| Quick Sales | 10% faster sales | Attracts more interested buyers |

| Negotiation Flexibility | Up to 5% more in sale price | Allows for better deal structure |

| Positive Buyer Incentive | 75% buyer preference | Encourages buyers to view the property as desirable |

Real-World Examples

Consider the case of a property in Austin, Texas, where the seller agreed to cover up to $5,000 in closing costs. This tactic led to a substantial uptick in interest. Within two weeks, the property received three offers, all above the asking price. The seller successfully closed the deal at 8% more than they anticipated, proving that investing in closing costs can lead to increased profits.

Another example is a home in Los Angeles whose seller offered to pay buyer closing costs. This strategy resulted in a quicker sale, with the home going under contract in just ten days compared to an average of 30 days for similar listings. The local market analysis found that homes with this offer were significantly more likely to attract serious buyers willing to negotiate on other terms.

Actionable Insights

If you’re looking to sell your home, consider the following strategies regarding closing costs:

- Market Analysis: Research local trends to see if paying closing costs would enhance your property appeal.

- Financial Planning: Assess your financial situation to determine the potential ROI on paying these costs.

- Communicate Offer: Clearly state your willingness to cover closing costs in listings and marketing materials.

- Consult Professionals: Discuss options with your real estate agent for tailored strategies in your specific market.

Understanding these advantages can significantly shape how you approach selling your property, providing a pathway to faster sales and potentially better offers.

Negotiating Closing Costs in Real Estate Transactions

When it comes to buying a home, negotiating closing costs can significantly save you money. Understanding how to navigate these costs effectively will empower you to get the best deal possible when you close on your new home. Let’s delve into the strategies you can employ to negotiate these expenses.

Key Strategies for Negotiating Closing Costs

1. Know the Costs Involved: Familiarize yourself with the typical closing costs involved in your transaction. Closing costs can include fees for title insurance, inspections, and attorney services. Being informed about these fees allows you to negotiate from a position of strength.

2. Request Seller Contributions: One effective strategy is to request that the seller covers part or all of the closing costs. By including this request in your offer, you can lessen your financial burden when finalizing the deal.

3. Be Flexible with Your Offer: If you notice a seller is motivated to close quickly, consider presenting a compelling offer. For instance, you might offer to pay slightly more for the home in exchange for the seller covering some closing costs.

4. Shop Around for Services: Don’t hesitate to compare various service providers involved in the closing process. For example, differences in lender fees could be significant, and some lenders may be willing to lower their fees for competitive advantage.

5. Negotiate with Lenders: Sometimes, lenders can offer loan options that help cover closing costs. Ask your lender about any programs they offer that could help defer these costs, such as rolling them into your mortgage.

Example of Commonly Negotiated Closing Costs

| Closing Cost Item | Average Cost | Negotiation Potential |

|---|---|---|

| Title Insurance | $1,000 | Medium |

| Escrow Fees | $500 | High |

| Attorney Fees | $1,500 | Medium |

| Home Inspection | $300 - $500 | High |

| Appraisal Fees | $400 - $700 | Low |

Real-World Examples of Negotiation Success

Case Study 1: A first-time homebuyer in Florida successfully negotiated with the seller to cover $5,000 in closing costs, as the seller was eager to expedite the sale due to a job relocation. This negotiation was pivotal in helping the buyer stick to their budget.

Case Study 2: Another buyer in California switched lenders after receiving a higher than expected fee quote. The new lender not only provided a better rate but also offered to cover part of the buyer’s closing costs, demonstrating the importance of shopping around.

Practical Implications for Your Negotiations

- Be Prepared to Walk Away: If the seller is unwilling to meet your closing cost requests, don’t hesitate to reconsider your options. This mindset can often encourage the seller to come back with a better offer.

- Use the Market to Your Advantage: In a buyer’s market, where there are more homes for sale than interested buyers, you have a stronger position to negotiate closing costs. Conversely, if you’re in a seller’s market, you might need to get creative with your offers.

- Consult with Professionals: Engaging a knowledgeable real estate agent can provide valuable insights into which costs are most negotiable and typical practices in your area, enhancing your negotiation strategy.

Actionable Advice for Negotiating Closing Costs

- Prepare a Negotiation Plan: List the closing costs you want to negotiate and prioritize them based on what you think is most feasible to change.

- Communicate Openly: When discussing costs, be transparent about your financial limits. Sellers appreciate honesty and may be more inclined to accommodate your requests.

- Consider Timing: If possible, align your negotiation efforts with broader market trends to increase your chances of success.

Real-World Examples of Closing Cost Arrangements

When it comes to closing costs in real estate transactions, real-world examples can illustrate the diverse arrangements that buyers and sellers can experience. Understanding these arrangements helps you navigate financing and negotiations effectively.

Common Closing Cost Arrangements

- Buyer Credits: In many cases, sellers offer closing cost credits to buyers to make a sale more appealing. For instance, a seller could agree to cover up to 3% of the purchase price, allowing buyers to save significantly on upfront expenses.

- Split Closing Costs: Some agreements involve sharing closing costs between buyers and sellers. A common arrangement sees both parties cover specific fees, such as title insurance or inspection costs, which might equal 1.5% to 2% of the sale price.

| Arrangement Type | Percentage Paid by Buyers | Percentage Paid by Sellers |

|---|---|---|

| Full Buyer Credit | 100% | 0% |

| Split Arrangement | 50% | 50% |

| Seller Pays All Costs | 0% | 100% |

Real-World Examples

1. First-Time Buyers: Consider a family purchasing their first home for $300,000. The seller agreed to cover 3% of the closing costs, amounting to $9,000. This arrangement allowed the buyers to allocate their savings towards moving expenses instead of closing costs.

2. Negotiated Seller Concessions: In a competitive market, another buyer offered $250,000 for a home, but negotiations led to the seller agreeing to pay 1.5% of closing costs. In this case, the buyer saved $3,750 based on a reduced upfront cash requirement due to the seller’s concessions.

3. Investor Financing: An investor looking to purchase multiple properties in a short time frame agreed with the seller to split the closing costs. This arrangement, where both parties covered 2% each on a $200,000 property, resulted in savings of $8,000 in total closing costs shared between them.

Practical Implications

Understanding these arrangements can empower you in negotiations, ensuring you maximize savings or leverage seller contributions effectively. When you approach a real estate deal, consider proposing an arrangement that aligns with your financial goals, whether that’s securing a seller credit or splitting costs.

- Be aware of local market trends: Some areas are more open to seller credits than others. Research your local market’s conditions to optimize your strategy.

- Communicate openly with your agent: Your real estate agent can provide insights into typical arrangements in your area, guiding you on what to request during negotiations.

By familiarizing yourself with these examples and arrangements, you can take proactive steps to influence the outcome of your real estate transaction. Stay informed about what negotiations might be possible and negotiate wisely to reduce your financial burden during the closing process.

Understanding Lender Contributions to Closing Costs

When stepping into the world of real estate, understanding lender contributions to closing costs can significantly impact your purchase. These contributions, often called lender credits, are amounts that your lender can provide to help offset your out-of-pocket expenses during closing. Let’s dive into the details surrounding these contributions and how they work for you as a buyer.

What Are Lender Contributions?

Lender contributions can be beneficial as they lower the amount of cash you’ll need to bring to closing. These contributions occur in various forms, and their presence often depends on the mortgage type, lender policies, and your specific circumstances.

- Lender Credits: This is a common method where lenders provide a specific dollar amount or percentage of the loan amount to cover closing costs.

- Rate Adjustment: Sometimes, lenders will increase your interest rate slightly in exchange for a higher credit amount at closing. This approach can provide immediate relief from upfront costs.

Studies show that in certain cases, lenders can contribute up to 3% of the home’s purchase price towards closing costs, depending on the loan type and your negotiation power.

How Lender Contributions Work

When you decide to accept lender contributions, the process can unfold in predictable ways:

1. Down Payment Impact: Contributions can allow you to allocate more of your funds to your down payment, which is especially helpful if you’re looking to reduce your mortgage insurance costs.

2. Loan Type Variability:

- Conventional loans may offer lower contribution limits compared to FHA or VA loans, which may allow more flexible contributions.

- For FHA loans, you might see lender contributions that can cover up to 6% of the sale price towards closing costs.

3. Risks and Rewards: While accepting higher rates for credits can ease initial costs, it’s crucial to weigh this against long-term mortgage payment implications.

Example Contribution Scenarios

To illustrate how lender contributions can play out, consider the following cases:

| Loan Type | Lender Contribution Percentage | Possible Closing Cost Offset |

|---|---|---|

| Conventional Loan | Up to 3% | $6,000 on a $200,000 home |

| FHA Loan | Up to 6% | $12,000 on a $200,000 home |

| VA Loan | Up to 4% | $8,000 on a $200,000 home |

Real-World Examples

Imagine a buyer who purchases a $250,000 home with an FHA loan. If their lender offers a 4% contribution towards closing costs, they’d receive up to $10,000 to help cover those expenses. This contribution can significantly lighten the immediate financial burden.

Alternatively, consider a buyer utilizing a conventional mortgage. If they negotiate 2% from their lender on a $300,000 home, they would save $6,000 in closing costs—freed up funds that may be redirected towards renovations or other expenses.

Practical Implications

Understanding your options for lender contributions can not only ease the stress of closing costs but can also sculpt your financial landscape for years ahead.

- Ask About Customization: When discussing your loan options, inquire about various ways your lender can contribute to your closing costs and compare the long-term effects on your mortgage.

- Evaluate Interest Rate Trade-offs: Consider being proactive by calculating the differences in payments and overall expenses between taking a higher interest rate with credits versus accepting lower credits.

Being educated on lender contributions equips you with the tools to strategize your home purchasing journey effectively. It’s always advisable to engage in thorough discussions with your lender to understand the offerings and implications tailored to your unique financial scenario.