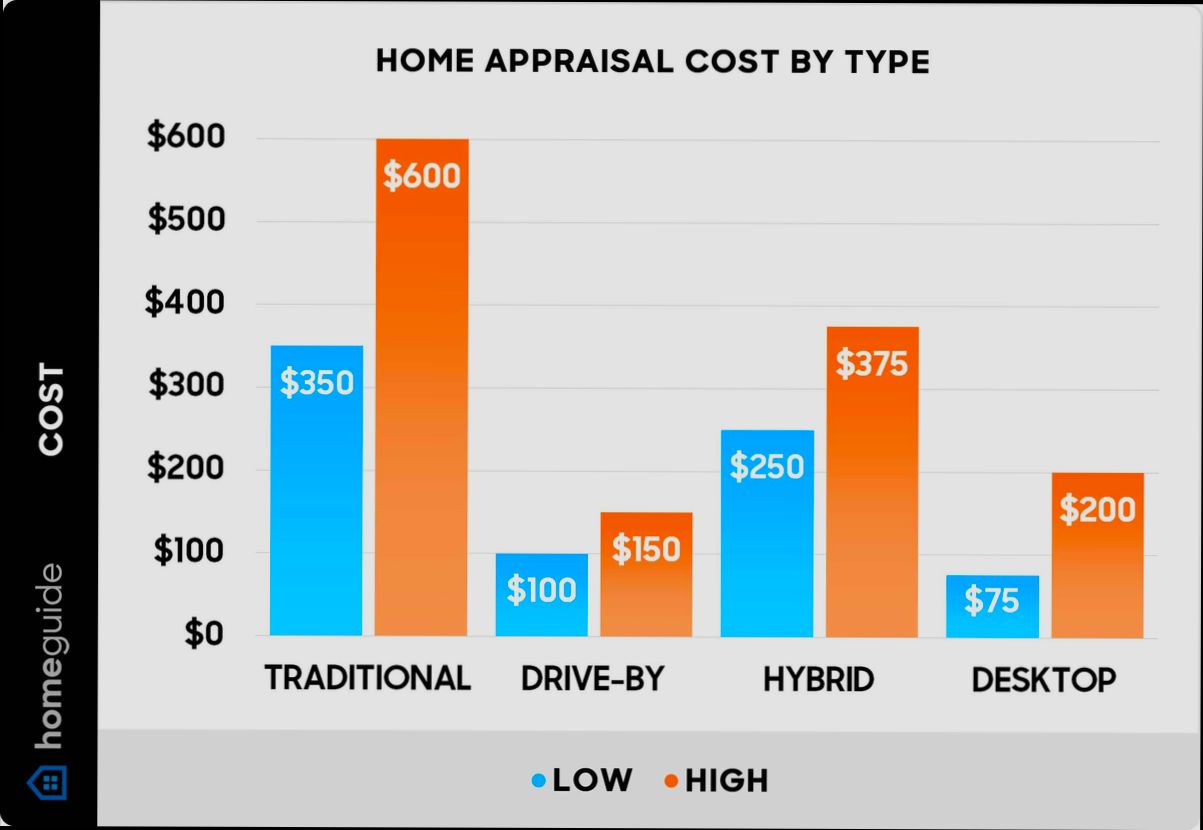

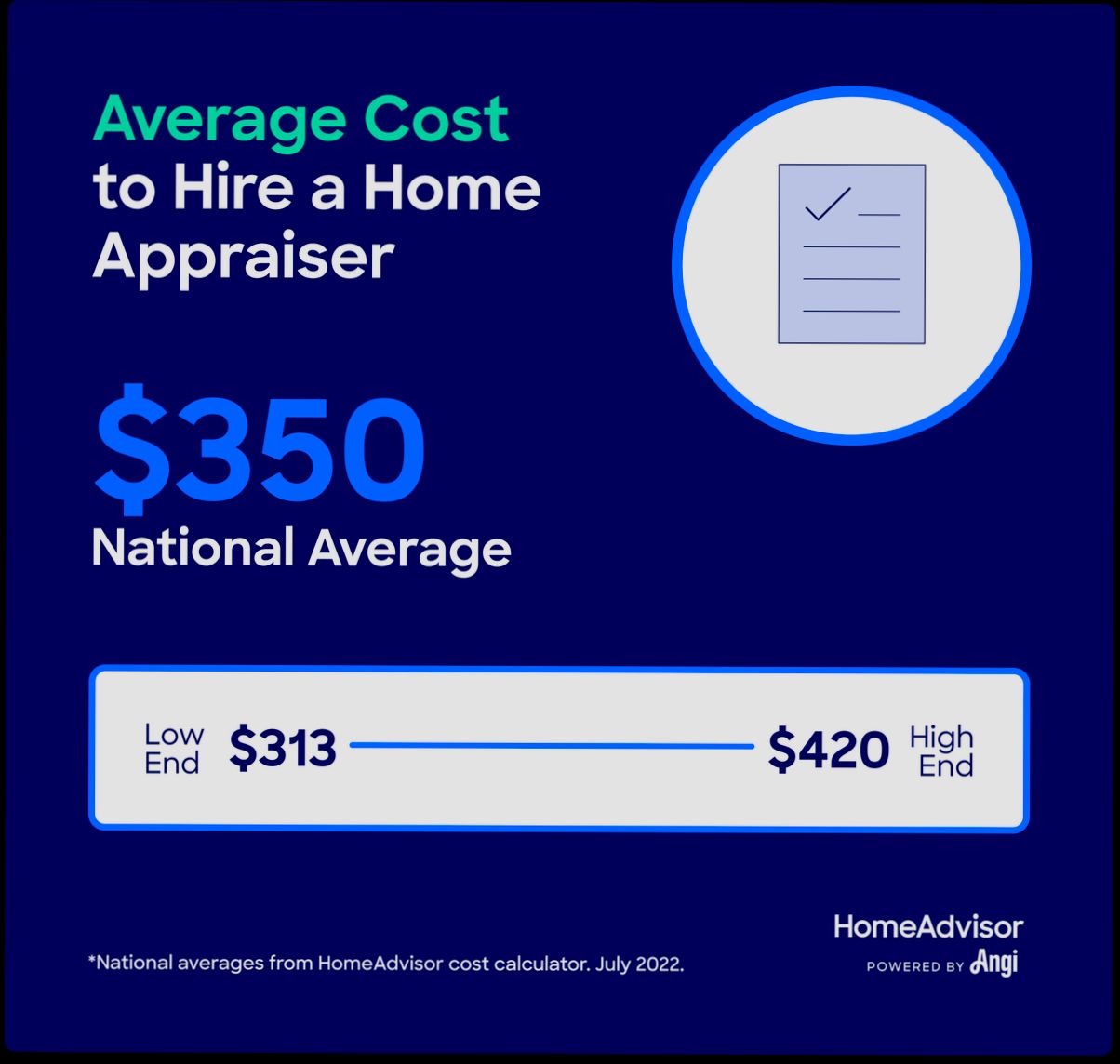

How Much Does a Home Appraisal Cost? If you’re eyeing a new home or looking to refinance, you’ll want to nail down that appraisal fee right off the bat. On average, homeowners can expect to shell out between $300 to $600 for a standard single-family home appraisal. If your place is larger or located in a high-cost area, those numbers can bump up to $800 or more! For instance, in cities like San Francisco and New York, where real estate prices soar, appraisal fees can push even higher, making it essential to factor these costs into your budget.

But it doesn’t stop at the price alone; the type of appraisal matters too. A basic drive-by appraisal might cost less than a full interior inspection, which is often necessary for more complicated properties. Specialty appraisals, like those for historic homes or unique builds, can demand a higher price tag due to their complexity and the time needed to research. It’s all part of the game when you’re navigating the housing market. Knowing what you might pay can help you prepare better and avoid any surprises down the road.

Understanding Home Appraisal Pricing Factors

Understanding what influences home appraisal pricing can empower you during your real estate journey. Several key factors contribute to the costs associated with appraisals, and recognizing these can help you budget more effectively and choose the right appraiser for your needs.

Key Factors Influencing Appraisal Costs

Various elements can drive the costs of a home appraisal beyond the standard fees. Here are some crucial factors to consider:

- Property Type: Different types of properties have different appraisal fees. For instance:

- Single-family homes generally range from $300 to $400.

- Multi-family properties can cost between $600 and $1,000.

- Commercial properties significantly increase the price, ranging from $1,500 to $10,000+.

- Location: The location of the property plays a significant role in the appraisal cost.

- Urban areas tend to have lower fees due to easier access and more comparable sales data.

- Conversely, rural properties can have higher costs due to limited market data and travel time for appraisers.

- Complexity of the Property: Unique or complex home features can escalate appraisal fees. For example:

- Properties with historical significance or complex layouts usually require specialized knowledge, which increases appraisal costs.

Comparative Costs of Home Appraisals

| Property Type | Cost Range | Complexity Impact |

|---|---|---|

| Single-family homes | $300 - $400 | Standardized process leads to lower costs. |

| Multi-family properties | $600 - $1,000 | Increased complexity due to multiple units. |

| Commercial properties | $1,500 - $10,000+ | Complexities in valuation significantly raise fees. |

Real-World Examples

Consider a scenario where a homebuyer plans to purchase a historic property. Knowing the complexities involved, the buyer should expect to pay higher appraisal fees—potentially in the range of $500 to $800, depending on its unique features and required expertise.

Alternatively, if you are looking at a standard single-family home in an urban setting, the appraisal might cost you around $350 due to the availability of comparative sales, requiring less specialized knowledge.

Practical Implications for Homebuyers

Understanding these factors can guide your expectations regarding appraisal costs. Always consider:

- The property type you’re interested in and its potential appraisal costs.

- The location’s impact on appraisal fees, especially if you’re considering a rural area.

- How complex features of a property might add to the overall cost.

Actionable Advice

Before scheduling your appraisal, consult with multiple qualified appraisers for quotes. This not only ensures you understand the typical costs associated with your property type but also helps you gauge the fair market rate given the specific factors that influence appraisal pricing. By staying informed, you can effectively manage your budget and expectations throughout your home buying experience.

Regional Variations in Appraisal Costs

When it comes to home appraisal costs, regional differences can create significant disparities. Understanding where you are geographically can help you budget accordingly and manage your expectations effectively.

Factors Influencing Regional Differences

- Geographic Demand: Areas with high demand for housing, like urban centers, often experience higher appraisal costs. In contrast, rural areas typically have lower costs due to less competition and fewer appraisers.

- Local Regulations: Different states or municipalities may impose varying regulations which can influence the price of appraisals. More stringent requirements can lead to higher fees.

- Appraiser Availability: In regions with fewer licensed appraisers, you may find that appraisal costs increase due to supply and demand dynamics.

| Region | Average Cost | Notes |

|---|---|---|

| Urban Areas | $400 - $600 | Higher demand drives costs upward. |

| Suburban Areas | $300 - $500 | Moderate fees, with more appraisers. |

| Rural Areas | $250 - $400 | Lower demand leads to lower costs. |

| States with High Regulation | $450 - $700 | Additional certifications required. |

Real-World Examples of Regional Variations

In New York City, the average appraisal cost can reach up to $600 for a standard home due to high demand and strict regulations. Conversely, in a more rural part of Indiana, you might only pay around $300 for a similar service. Additionally, in California, the bustling real estate market in cities such as San Francisco can push appraisal fees into the $700 range, particularly for homes over a million dollars, while smaller towns in the central valley may charge only $350.

Practical Implications for Homebuyers and Sellers

As you navigate the home buying or selling process, consider these regional variations in appraisal costs:

- Budgeting: Make sure to include the expected appraisal cost in your overall budget. Understanding local norms can help avoid surprises.

- Choosing an Appraiser: In areas where appraisers are less available, be prepared to book an appraisal well in advance to ensure you’re not delayed in your transaction.

- Negotiating Costs: In competitive markets, you might find that sellers or buyers are willing to negotiate appraisal fees as a part of the sale.

Actionable Advice

When preparing for a home appraisal, consult local real estate agents or appraisers about the specific costs in your area. They can provide valuable insights into what you should plan for. Moreover, if you’re moving from one region to another, familiarize yourself with local appraisal norms to ensure a smooth transaction process.

Exploring Common Pricing Models for Appraisals

When considering the cost of a home appraisal, it’s essential to understand the various pricing models that appraisers employ. This section explores these models and how they impact the overall fee a homeowner might encounter during the appraisal process.

Key Pricing Models

Home appraisals often rely on several pricing models, influenced by factors like property type and purpose. Here are some common pricing models that appraisers might adopt:

- Flat Fee Structure: Many appraisers charge a flat rate for standard residential appraisals. For example, single-family homes see costs typically between $300 and $400, while multi-family properties can range from $600 to $1,000. This approach offers predictability in costs.

- Hourly Rate: Some appraisers may charge an hourly fee for complex assessments, especially for commercial or unique properties. This pricing model is beneficial for properties that require extensive analysis, with fees potentially exceeding $250 an hour.

- Percentage of Property Value: In some cases, appraisers set fees as a percentage of the property’s assessed value, particularly for high-value estates or specialized properties. While not as common in residential appraisals, this model can be seen in commercial real estate transactions.

- Regional Pricing Variations: Appraisers may adjust fees based on local market conditions. For instance, urban areas with high demand can charge between $400 and $600, while rural areas might see increased costs due to limited access to comparable market data.

| Model | Description | Cost Range |

|---|---|---|

| Flat Fee | Standard charge for residential properties | $300 - $400 for single-family homes |

| Hourly Rate | Based on time spent on complex assessments | $250+ per hour |

| Percentage of Value | Fee based on a percentage of the property’s appraised value | Varies significantly, often for high-value properties |

| Regional Variations | Adjusted based on local market conditions | $400 - $600 in urban areas; higher in particular small towns |

Real-World Examples

1. Flat Fee Approach: If you’re purchasing a single-family home in a suburban neighborhood, you might request a flat fee appraisal. With typical charges in the $300-$400 range, you can budget accordingly without worrying about fluctuations.

2. Hourly Rates in Commercial Appraisals: Suppose you own a multi-family rental property in a bustling city. An appraisal might take several hours due to its complexity, leading to a potential fee of $1,500 if the appraiser charges $250 per hour.

3. Percentage-Based Fees: For a luxury estate valued at $2 million, you could encounter an appraisal fee structured as 0.5% of the property’s value. This could result in an appraisal cost of $10,000, making it crucial to clarify the pricing model before proceeding.

Practical Implications

Understanding these pricing models equips you to make informed decisions about which appraiser to hire. Here’s what you can do:

- Compare Quotes: Don’t settle for the first quote you receive. Obtain multiple quotes and understand the pricing models behind them. This ensures you’re not just looking at the cost but the value of the service provided.

- Ask About Their Approach: When talking to appraisers, ask if they use a flat fee, hourly rates, or another model. Knowing this helps you anticipate total costs based on the property type and complexity.

- Consider Property Type and Purpose: If your property is unique, be prepared for potentially higher fees. Discuss upfront how the appraisal type—whether for a mortgage, estate settlement, or litigation—affects pricing.

By being proactive about understanding the varying pricing models used in appraisals, you can avoid unwelcome surprises and budget accurately for your property evaluation needs.

Statistics on Average Home Appraisal Fees

Home appraisal fees can seem vague and unpredictable, but they actually have some consistent statistics that can guide you. Understanding these statistics is vital when budgeting for your home purchase or refinance, as it helps you prepare for one of the essential costs in a real estate transaction.

Average Appraisal Fees Nationwide

On average, you can expect to pay anywhere from $300 to $700 for a standard home appraisal. Here’s a quick breakdown of how those fees can vary:

- Single-family homes: Typically range from $300 to $500.

- Multi-family homes: Can cost between $500 and $1,000, reflecting the complexity of appraising multiple units.

- Luxury properties: Often incur fees starting at $800 and can go well above $1,500 due to their unique features and market complexities.

Appraisal Fee Trends Over Time

Survey data reveals an interesting trend in average home appraisal fees. Over the past five years, appraisal fees have increased by approximately 10%. This rise can be attributed to several factors, including inflation, increased demand for housing, and the growing complexity of the appraisal process.

Comparative Table of Average Appraisal Fees

| Property Type | Average Fee Range | Additional Notes |

|---|---|---|

| Single-family home | $300 - $500 | Commonly found in residential markets |

| Multi-family property | $500 - $1,000 | Higher due to multiple units |

| Luxury home | $800 - $1,500+ | Varies widely based on amenities |

| Commercial property | $1,000 - $4,000+ | Significant complexity drives costs |

Real-World Examples

Consider a case in Denver, where a homeowner recently paid $450 for a standard appraisal on a single-family home. In comparison, a multi-family property in New York City was appraised for $1,200 due to the complicated nature of its valuation.

In another example, a luxury estate in Los Angeles demanded an appraisal fee of $2,500, reflecting its vast square footage and high-end finishes. Such examples highlight not only the range you might see across different types of properties but also how specific markets can influence fees significantly.

Practical Implications for You

Understanding these statistics about average home appraisal fees allows you to plan more effectively. Use this information to set your budget before buying or refinancing. Always consider the type of property, as that substantially impacts the fee you’ll pay. Additionally, keeping an eye on market trends can help you anticipate fees, especially in areas where demand is rising.

Specific Facts to Remember

- The average appraisal fee has seen a 10% increase over the past five years.

- Luxury properties often start around $800 and can exceed $1,500.

- Multi-family properties generally bear higher appraisal costs due to their complexity.

Being informed about these statistics can empower you to make better financial decisions regarding your real estate endeavors.

Real-World Examples of Appraisal Expenses

When you’re embarking on the journey to buy or sell a home, understanding real-world examples of appraisal expenses can save you time and money. This section dives into specific instances and data points that highlight how appraisal costs can vary in practical scenarios.

Key Points on Appraisal Expenses

- Diverse Property Types: Different property classifications can lead to fluctuating appraisal expenses. For instance, a single-family home might cost $300 to $700, whereas a multi-family residence could range from $500 to $1,200 due to increased complexity during evaluation.

- Commercial vs. Residential: Commercial property appraisals can be significantly pricier than residential ones. For example, an appraisal on a small retail building in a suburban area may range from $1,000 to $2,500, depending on size and location specifics.

Comparative Table of Appraisal Costs

| Property Type | Average Appraisal Cost | Notes |

|---|---|---|

| Single-family home | $300 - $700 | Standard residential evaluations |

| Multi-family dwelling | $500 - $1,200 | More intricate assessments for dual or more units |

| Small commercial | $1,000 - $2,500 | Higher due to specialized knowledge required |

| Vacant land | $400 - $1,000 | Location plays a pivotal role in pricing |

Real-World Examples of Appraisal Expenses

1. Case Study: Lakefront Property Appraisal

A client in Florida sought an appraisal for a lakefront home. The appraiser charged $850 due to the uniqueness of the property and its expansive views, which required additional research into comparable sales in that rare market.

2. Case Study: Urban Condo Evaluation

In New York City, a two-bedroom condominium appraisal fetched a fee of $1,200. The appraiser conducted a thorough analysis of the competitive market, adjusting for amenities and proximity to public transportation, which justified the higher cost.

3. Case Study: Rural Land Appraisal

An owner of rural land in Montana needed an appraisal before selling. The cost was $600, reflecting the time-consuming process of determining land value based on various zoning regulations and comparable pieces of land that had sold recently.

Practical Implications for You

Understanding these examples allows you to budget accurately for your appraisal. When preparing for an appraisal, consider factors like property uniqueness, location, and type, which will directly impact costs. Always ask for a detailed breakdown of fees to anticipate any unexpected charges.

It’s also wise to shop around and get quotes from multiple appraisers, especially for specialized properties. This not only helps in understanding market rates but may also assist in negotiating fees based on comparable services.

Keep in mind the significant variations based on overall property value and market conditions. Staying informed and prepared will empower you as you navigate the home appraisal landscape.

Advantages of Investing in a Home Appraisal

When you’re considering a home appraisal, it’s essential to understand the significant benefits that come with this investment. A home appraisal can offer valuable insights and potentially save you money in the long run. Let’s explore the direct advantages of investing in a home appraisal that can lead to informed decisions in your real estate journey.

Accurate Property Valuation

Investing in an appraisal ensures that you get an accurate valuation of your property, which is crucial whether you’re buying, selling, or refinancing. This accurate assessment allows you to set a realistic price, ensuring you do not overpay as a buyer or undervalue your property as a seller. According to industry experts, properties that have undergone an appraisal process can sell for up to 10% more than their unstated market value.

Enhanced Negotiation Power

Having a professional appraisal on hand gives you leverage when negotiating. It equips you with concrete data to back your offers or counteroffers. For example, if you’re evaluating your property or making an offer on a new one, use the appraiser’s findings to justify your position. Home buyers using appraisals in negotiations report a 15% better chance of securing favorable terms during offers.

Risk Mitigation

A thorough appraisal can expose potential issues with a property that might lead to costly repairs down the line. Identifying elements like structural faults or out-of-date utilities can prevent you from making a significant, uninformed investment. Appraisers spend an average of 1.5 hours assessing a property, during which time they can pinpoint items that may require future attention, potentially saving you 20% or more in future costs.

Financial Planning and Investment Strategy

Understanding your home’s appraised value can play a vital role in your financial planning and investment strategy. If you plan to access your home equity for further investments, knowing its worth helps you strategize more effectively. A well-timed appraisal can increase your equity by 5%-10%, allowing you to make better financial decisions moving forward.

| Benefit | Description | Expected Impact |

|---|---|---|

| Accurate Property Valuation | Ensures fair market value for buying or selling. | Up to 10% more profit |

| Enhanced Negotiation Power | Empowers buyers/sellers with data-driven positions. | 15% better terms |

| Risk Mitigation | Identifies problems preventing costly repairs. | Saves 20% in repairs |

| Financial Planning | Aids in smart leveraging of home equity for investment. | Increase equity by 5%-10% |

Real-World Examples

Consider a homeowner who invested in an appraisal before selling their property. The appraisal accurately reflected the home’s worth at $350,000, compared to the homeowner’s initial listing price of $325,000. With this data, they confidently relisted their home and sold it for $345,000, gaining a more significant profit, all thanks to the informed valuation provided by the appraisal.

Similarly, a first-time homebuyer sought an appraisal on a property valued at $400,000. The appraisal revealed several underlying issues needing $25,000 in repairs. Armed with this information, the buyer successfully negotiated with the seller to reduce the price by $20,000, preventing a costly mistake.

Practical Implications

By investing in an appraisal, you’re not just spending money; you’re protecting yourself from potential pitfalls in the home buying or selling process. It allows you to take control of your investment by providing transparent and credible evaluations. If you’re in the market, consider making a home appraisal a priority to ensure you’re making well-informed, long-term decisions.

Actionable Advice

To maximize the advantages of a home appraisal, ensure to select a certified appraiser with a solid reputation. This choice not only provides you with an accurate valuation but also adds credibility to your negotiations and transactions moving forward. Moreover, track changes in your property value and consider recalibrating your appraisal every few years, especially if you’ve made significant renovations or upgrades.

How Appraisal Cost Impacts Property Transactions

Understanding how appraisal costs affect property transactions is crucial for both buyers and sellers. The valuation provided by an appraisal can significantly influence negotiation power, loan approval processes, and ultimately, the success of a transaction.

The Financial Implications of Appraisal Costs

Appraisal costs directly affect various aspects of property transactions:

- Financing Approval: Lenders typically require an appraisal to confirm that the property’s value justifies the loan amount. If the appraisal costs are higher, it may lead to increased loan fees or a more stringent evaluation process. This can deter potential buyers who are already sensitive to costs.

- Negotiation Leverage: A high appraisal cost could indicate that the property is more complex, leading to potential adjustments in negotiations. For example, if you hire a specialized appraiser for a historic home, the higher cost reflects the expertise required, possibly bolstering your negotiating position.

- Closing Costs: Appraisal fees can also contribute to overall closing costs, making the transaction more expensive. If a buyer underestimates these expenses, they might face financial strains that could derail the purchase.

Comparative Table of Appraisal Costs Across Different Transaction Scenarios

| Transaction Type | Estimated Appraisal Cost | Implications |

|---|---|---|

| Standard Purchase | $400 - $600 | Higher costs can discourage buyers in tight markets. |

| Complex Property (e.g., historic homes) | $700 - $1,200 | Increased costs due to specialized expertise required. |

| Refinancing | $350 - $500 | Lower appraisal costs can enhance value perception for homeowners. |

Real-World Examples Demonstrating Impact

Consider a buyer interested in a property listed at $450,000. The appraisal comes back at $425,000. This $25,000 discrepancy can change everything:

- The buyer may feel justified in negotiating the price down, potentially leading to an extended transaction timeline.

- Alternatively, if leveraging a high appraisal cost (say, for renovating an undervalued property) adds substantial value, the seller could command a higher final sale price, creating an attractive proposition for buyers.

In another scenario, a homeowner seeking to refinance an existing mortgage has an appraisal performed. If the appraisal costs $450 but confirms a 15% increase in home value, the homeowner might qualify for better loan terms, resulting in long-term financial savings.

Practical Implications for You

As you navigate property transactions, keep these factors in mind:

- Budget for Appraisal Costs: Always factor appraisal fees into your transaction budget, so you’re not caught off guard during negotiations.

- Choose Wisely: Consider hiring an appraiser whose expertise matches your property type. While it may cost more, it can provide you with insights that enhance your bargaining power.

- Stay Informed: Know average appraisal costs in your area and understand how they influence buyer willingness and overall market conditions.

Understanding the multifaceted impact of appraisal costs on property transactions will empower you to make more informed decisions, whether you’re buying, selling, or refinancing a home. Always remember to approach these costs strategically, as they can shape the landscape of your real estate experience.