- Key Differences Between Title and Lender Insurance

- Statistical Insights on Lender Title Insurance Claims

- Real-World Applications of Title Insurance in Mortgages

- Examining the Advantages of Lender Title Insurance

- Common Misconceptions About Lender Title Insurance

- The Role of Lender Title Insurance in Risk Management

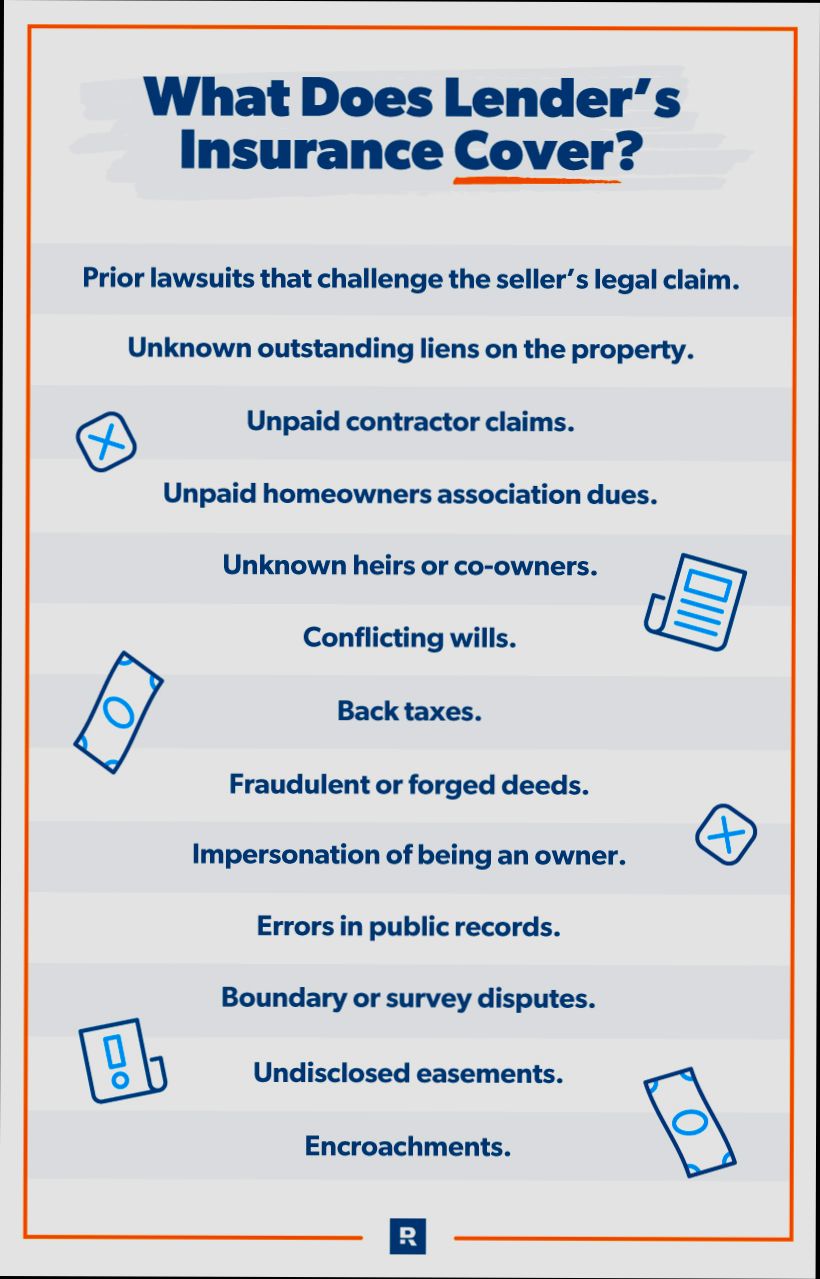

What is Lender Title Insurance? It’s a safety net for your mortgage lender that ensures they’re protected from potential legal hiccups related to property ownership. Imagine you just bought your dream home, only to discover a long-lost heir has a claim to the property. Without lender title insurance, your bank could take a financial hit, possibly costing them thousands—not to mention the stress it would put on you! In fact, a 2022 study found that 25% of title issues relate to unpaid taxes or outstanding liens.

When you close on a home, the lender generally requires title insurance as part of the mortgage process. This isn’t just an added expense; it’s a crucial layer of protection against hidden risks like fraud or previous owners’ unpaid debts. For instance, a reported 15% of title claims involve issues like forgery and misrepresentation of ownership. With lender title insurance in your corner, your lender feels secure, knowing they’re covered against these pesky surprises.

Understanding the Basics of Lender Title Insurance

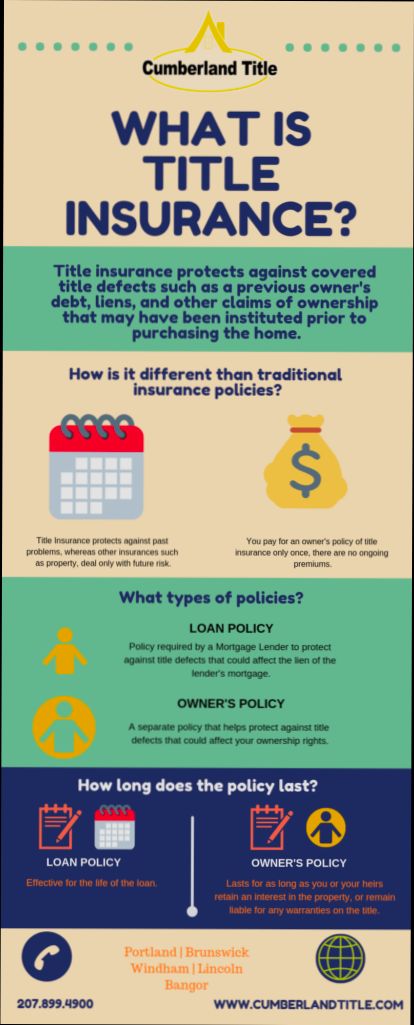

Lender title insurance is an essential component of real estate transactions, especially when financing a home. It provides protection specifically for lenders against various issues related to the title of the property. Let’s dive deeper into the nuances of lender title insurance and clarify what you need to know.

Key Points About Lender Title Insurance

- Mandatory Requirement: Nearly all mortgage lenders mandate the purchase of lender’s title insurance. This requirement protects their financial interest in the property for the duration of the loan.

- Coverage Scope: Lender’s title insurance safeguards against risks such as undisclosed liens, ownership disputes, and issues with the title’s history. It serves solely to protect the lender’s stake, not the homeowner’s equity.

- Policy Duration: The coverage remains active for the life of the loan. Even if you refinance, a new lender title policy is typically required to cover the updated loan amount.

- Cost Variability: The title insurance premium may differ between the Loan Estimate and the Closing Disclosure you receive from your lender and the paperwork from the title company, leading to confusion about costs. For example, the premium from the title company typically reflects the final amount you owe.

- Owner’s vs. Lender’s Title Insurance: Unlike lender’s title insurance, which is mandatory, owner’s title insurance is optional. It protects the homeowner’s equity and investment in the property against legal claims.

| Aspect | Lender Title Insurance | Owner Title Insurance |

|---|---|---|

| Requirement | Mandatory for loans | Optional |

| Protects | Lender’s financial interest | Homeowner’s equity |

| Policy Duration | Duration of the loan | Indefinite (one-time premium) |

| Coverage | Title defects affecting lender | Title defects affecting owner |

Real-World Examples

Consider a scenario where you buy a home and later discover an undisclosed lien from the previous owner. The lender’s title insurance would cover the lender against potential financial losses due to this issue, which could threaten their ability to get repaid. However, as the homeowner, you would need an owner’s title insurance policy to safeguard your investment.

Another common situation arises when sellers push buyers to use a specific title company. While this can happen, note that you should not feel pressured to choose a title company that does not meet your needs. It’s important to understand your rights and options in such situations.

Practical Implications

Understanding how lender title insurance functions can influence many aspects of your home-buying process. Make sure to clearly review the terms of the policy you are presented with, and don’t hesitate to ask your lender for clarifications.

- Ask Questions: If you notice discrepancies between the title insurance premiums listed in various documents, reach out to your lender or title company for clarification to avoid misunderstandings.

- Know Your Options: Consider obtaining an owner’s title insurance policy in addition to the lender’s policy, as it provides important protection for your equity in the home.

- Research Providers: If you’re being pressured to select a specific title company, do your research. You can often choose a company that you feel comfortable with, provided they meet the lender’s requirements.

By being proactive and informed, you can navigate the complexities of lender title insurance effectively.

Key Differences Between Title and Lender Insurance

When diving into the world of real estate, understanding the nuances between title insurance and lender insurance is crucial. While both serve to protect financial interests, they do so in distinctly different ways. Let’s break down these differences to enhance your knowledge.

Coverage Scope

- Homeowner’s Title Insurance: This insurance protects the buyer’s equity in the property and typically covers issues like undisclosed liens, forgeries, or encroachments that could affect ownership.

- Lender’s Title Insurance: In contrast, lender insurance only covers the lender’s investment in the property, safeguarding against similar issues but focused solely on the lienholder’s interests.

Payment Structure

- Homeowner’s Title Insurance Premium: The homeowner usually pays for their title insurance upfront, a one-time premium that covers them as long as they own the home.

- Lender’s Title Insurance Premium: While the lender’s policy is often also a one-time premium paid at closing, many lenders structure it differently, allowing for varying payment options over the life of the loan.

Policy Duration

- Homeowner’s Title Insurance: This policy lasts until the homeowner sells the property or refinances their mortgage, ensuring ongoing protection for the homeowner.

- Lender’s Title Insurance: This policy is active only as long as the mortgage loan is outstanding, meaning coverage ceases if the loan is paid off or refinanced.

| Feature | Homeowner’s Title Insurance | Lender’s Title Insurance |

|---|---|---|

| Coverage Type | Buyer’s equity and ownership | Lender’s interest |

| Payment Method | One-time premium at closing | One-time or structured payments |

| Duration of Coverage | Until the homeowner sells/refinances | Until the loan is paid off |

Real-World Examples

Consider the case of Sarah, a first-time homebuyer. She purchases homeowner’s title insurance to secure her equity after learning it protects her against claims of ownership disputes. On the other hand, her lender requires that she also acquires lender’s title insurance, ensuring that their financial stake is secured from any potential title issues that could arise over the term of the mortgage.

In another scenario, Jake refinances his home. His original lender’s title insurance policy was effective only until he paid off his previous loan. When Jake refinances, he needs a new lender’s policy to protect the new lender’s investment, showcasing the temporary nature of lender insurance.

Practical Implications for You

Understanding these distinctions can influence your financial decisions. If you’re a buyer, being aware that lender’s title insurance does not cover your equity can prompt you to consider investing in a homeowner’s title policy for comprehensive protection.

Moreover, if you plan to refinance, remember that lender title insurance will need to be addressed even if you already owned a policy from your initial mortgage. This insight can help you avoid unexpected costs at closing.

Actionable Facts

- Evaluate Your Needs: Before purchasing, assess the differences in coverage and consider obtaining a homeowner’s policy to keep your investment secure.

- Consider Future Financing: Be proactive about potential refinancing opportunities and understand that each new mortgage may require fresh lender title insurance.

- Ask Questions: When dealing with your lender or title company, inquire specifically about the differences in coverage to ensure that you are fully informed about your financial liabilities and protections.

Statistical Insights on Lender Title Insurance Claims

When we delve into the statistics surrounding lender title insurance claims, it reveals critical insights about their frequency, nature, and impact on the mortgage industry. Understanding these factors is essential for both lenders and borrowers, as they shed light on potential risks associated with real estate transactions.

Claim Frequency and Types

Recent studies indicate that approximately 4% of all lender title insurance policies result in a claim during the term of the loan. This statistic highlights that while lender title insurance is a crucial safeguard, the likelihood of a claim is relatively low compared to other types of insurance. Here are some key statistics regarding the types of claims:

- Fraudulent Claims: Roughly 20% of title insurance claims arise from fraud or forgery issues. This statistic underlines the importance of thorough verification during the title search process.

- Undisclosed Liens: Another 30% of claims stem from undisclosed liens or mortgages that were not discovered prior to closing, showcasing the potential risks of inadequately searched titles.

- Boundary Disputes: About 12% of claims involve property boundary disputes, stressing the significance of surveying prior to purchase.

Claimants and Payout Trends

The demographics of claimants provide an interesting glimpse into who is affected by these claims. Notably, properties in urban areas report claims 15% more frequently than those in rural areas. This variation often relates to the complexity of urban property ownership and the higher probability of unresolved legal matters.

When it comes to payouts, the claims against lender title insurance typically average around $10,000 to $20,000. A breakdown of the average payouts by claim type is as follows:

| Claim Type | Average Payout (USD) |

|---|---|

| Fraud and Forgery | $15,000 |

| Undisclosed Liens | $12,000 |

| Boundary Disputes | $18,000 |

Real-World Case Studies

1. In a notable case in California, a lender faced a claim when a property was discovered to have multiple undisclosed liens totaling $50,000. Lender title insurance allowed them to recover $15,000 in legal fees, reinforcing the importance of coverage.

2. A case from New York involved a boundary dispute where the claimant sought damages for encroachment on their property. The lender was able to utilize their title insurance to navigate the dispute, with the average cost covered approximating $18,000.

Practical Implications for Readers

Understanding these statistics equips you, as a potential homeowner or lender, with essential insights into the nature of claims. Here are some practical considerations:

- Due Diligence: When obtaining lender title insurance, ensure that a comprehensive title search is completed to minimize the likelihood of claims.

- Fraud Awareness: Be vigilant about signs of fraud during the buying process. Awareness can help you safeguard against the 20% of claims that arise from fraudulent issues.

- Know Your Area: If investing in urban properties, prepare for an increased likelihood of claims due to the complex nature of urban real estate.

By acknowledging these statistical insights, you empower yourself to make informed decisions when navigating the complexities of real estate transactions and lender title insurance.

Real-World Applications of Title Insurance in Mortgages

When it comes to navigating the lending landscape of mortgages, title insurance plays a pivotal role. Its applications extend beyond mere formalities, impacting both lenders and borrowers in tangible ways. Let’s explore how title insurance functions in everyday mortgage scenarios.

Key Applications of Title Insurance in Mortgages

Here are some specific real-world applications you might encounter:

- Protection Against Title Defects: Title insurance safeguards against unexpected claims or defects that can surface after closing. For instance, if a hidden lien appears later—one that was not discovered during the title search—the lender and borrower are protected financially.

- Mitigating Risks: By covering a variety of risks, including incorrectly documented property transfers and unforeseen claims, lenders are more confident in their security. This allows for smoother transactions and potentially lower interest rates due to decreased risk exposure.

- Facilitating Foreclosures: In instances of foreclosure, title insurance can help clarify ownership, ensuring that lenders can reclaim properties without facing future claims that may jeopardize their interests. This streamlines the foreclosure process, making it more efficient.

- Supporting Claims Resolution: In cases where a claim arises, having title insurance provides a financial safety net. The insurer often manages the legal complexities, mitigating costs and time delays for lenders.

| Application | Description | Benefit to Borrowers | Benefit to Lenders |

|---|---|---|---|

| Protection Against Defects | Shields against undisclosed liens and defects discovered post-purchase. | Peace of mind regarding ownership. | Reduced risk of financial loss. |

| Risk Mitigation | Covers potential claims arising from errors in documentation. | Lower closing costs through fewer contingencies. | More stable lending environment. |

| Foreclosure Support | Clarifies ownership issues during foreclosure processes. | Easier transition to owning a home without future claims. | Streamlined recovery of assets. |

| Claims Management | Provides legal support and covers costs associated with information disputes. | Faster resolution of title issues. | Limits exposure to prolonged disputes. |

Real-World Examples

Consider the case of a homeowner, Sarah, who purchased her property with a lender title insurance policy. Five years later, a previously unknown lien surfaced due to unpaid contractor bills from the former owner. Sarah’s lender quickly accessed the title insurance benefits, resolving the issue without incurring significant costs. This incident illustrates how lender title insurance can protect both lenders and borrowers from unexpected financial burdens.

In another scenario, a financial institution dealt with a foreclosure where the previous owner’s heirs claimed they held rights to the property. The lender’s title insurance not only helped clarify the ownership but also supported the lender through the legal process, allowing a quicker resolution and minimizing losses.

Practical Implications for You

As you explore the realm of mortgages, understanding the real-world applications of title insurance can be a game-changer.

- Ensure you discuss title insurance with your lender thoroughly.

- Consider the potential risks associated with not having coverage.

- Assess how title insurance can directly affect your financial standing if unexpected issues arise.

Moreover, being informed about the protective benefits title insurance provides can empower you to make confident decisions regarding your mortgage.

- Remember, with title insurance, you’re securing not just your property, but also your financial future.

- Always inquire about policy specifics before finalizing your mortgage to fully understand what protections are in place.

Examining the Advantages of Lender Title Insurance

When we think about purchasing a home, it’s crucial to consider the security that lender title insurance provides. This specific type of insurance not only safeguards the lender’s interests but also offers several advantages that can significantly impact the financial landscape for both lenders and borrowers. Let’s explore some of these benefits in detail.

Key Advantages of Lender Title Insurance

- Protection Against Title Defects: Lender title insurance protects financial institutions from unexpected title challenges that could undermine their lien priority. For example, if a hidden lien emerges after the purchase, the policy ensures that the lender’s investment remains secure.

- Coverage for Legal Defense Costs: Should a title dispute arise, the lender is protected against legal expenses. This means that if someone challenges the lender’s claim on the property, the insurance will cover the costs associated with the legal defense.

- Assurance of Loan Enforceability: The policy gives lenders confidence that their mortgage is valid and enforceable. This assurance is critical, especially in transactions involving significant sums of money, like commercial real estate.

Cost Breakdown for Lender Title Insurance

Here’s a comparative table to illustrate the cost of lender title insurance based on property value:

| Property Value | Rate per $1,000 of Loan Amount | Total Cost Example for $500,000 Property (20% Down) |

|---|---|---|

| Up to $10,000,000 | $0.75 | $110 (for $400,000 loan) |

| $10,000,000 - $20,000,000 | $0.65 | $210 (for $800,000 loan) |

| $20,000,000 - $50,000,000 | $0.60 | $240 (for $1,200,000 loan) |

| Above $50,000,000 | $0.55 | $275 (for $1,500,000 loan) |

Real-World Examples of Lender Title Insurance Advantages

Consider a scenario where a lender financed a property valued at $1,000,000. After the transaction closed, an undiscovered lien was revealed from a previous owner, significantly threatening the lender’s ability to recover the loan amount. Since the lender had title insurance, they could promptly address the issue without incurring substantial legal costs. This coverage allowed the lender to maintain control over the investment and ensured the loan’s security.

In another instance, a small community bank issued a loan for a $500,000 property. Shortly after closing, a neighboring homeowner contested property boundaries due to a claimed error in the title. Thanks to the lender’s title insurance, the bank obtained legal representation, protecting their interests while resolving the dispute without financial strain.

Practical Implications for Readers

If you’re in the process of obtaining a mortgage, understand that lender title insurance is not just an added expense but a fundamental part of protecting your lender’s investment and your financial future. Keeping these advantages in mind can help you appreciate the necessity of the policy throughout the home-buying process.

Actionable Advice

When working with lenders, inquire about the lender title insurance policy they recommend and ensure you understand the coverage limits and legal protections it provides. Additionally, consider shopping around for competitive rates, while also assessing how different providers handle claims and coverage specifics. Being proactive will empower you to make informed decisions in your home purchase journey.

Common Misconceptions About Lender Title Insurance

Many homebuyers and property owners have questions and uncertainty about lender title insurance, leading to several misconceptions. In this section, we’ll explore these misunderstandings to provide clearer insights into what lender title insurance really covers and why it is important.

Key Misconceptions

1. Lender Title Insurance is Optional: Many people believe that lender title insurance is optional. However, it’s crucial for securing a mortgage. Most lenders require this insurance as part of the financing process to protect their investment.

2. It Only Protects the Lender: While it’s true that lender title insurance primarily protects the lender, it indirectly benefits the borrower. If a title issue arises, it could delay the buyer’s ability to sell or refinance the home, ultimately affecting the homeowner’s financial situation.

3. The Coverage is the Same Across Policies: There’s a common belief that all lender title insurance policies offer the same level of coverage. In reality, policies can differ significantly based on the insurer and the specifics of the property in question. It’s vital to understand the terms of your individual policy.

4. Claims are Rare: Some might think that claims against lender title insurance are uncommon. Yet, approximately 4% of lender title insurance policies result in a claim during the life of the loan. This statistic highlights the importance of having protection in place.

5. The Cost is Always High: While there are costs associated with lender title insurance, they can vary. Some homebuyers believe they’ll face high premiums regardless of the service. It’s worth shopping around, as rates can differ significantly among providers.

| Misconception | Reality |

|---|---|

| Optional Insurance | Mandatory for most mortgages |

| Only Benefits the Lender | Indirectly protects the homeowner as well |

| Uniform Coverage | Coverage varies; policies differ among insurers |

| Low Claim Frequency | 4% of policies result in claims |

| High Cost | Prices vary; shopping around can save money |

Real-World Examples

- Case Study: Title Issues Arising Post-Closing: A homeowner thought they were safe after closing their property but later discovered a previously unknown lien. Thanks to their lender title insurance, the lender was able to address the issue, but the homeowner also faced delays and potential financial losses without that protection.

- Example of Misleading Cost Information: A first-time buyer believed the quote they received was final. They later found out that other providers offered significantly lower rates. This smaller premium could have saved them a considerable amount of money, underscoring the importance of comparing quotes.

Practical Implications for Readers

Understanding these misconceptions can help you navigate the home financing process more effectively. When purchasing a home, clarify with your lender the specifics of the title insurance required.

- Always ask about the coverage details to ensure you understand what is and isn’t protected.

- Get multiple quotes to find competitive rates on lender title insurance.

- Be aware that while claims may seem rare, the potential consequences of not having coverage can be significant.

Specific Facts or Actionable Advice

- Always Check Requirements: Before finalizing your mortgage, confirm that you understand how lender title insurance works and why it’s compulsory.

- Educate Yourself on Policy Nuances: Familiarize yourself with the specifics of different policies, as coverage can differ widely.

- Consider Future Needs: If you foresee selling or refinancing soon, ensure your title insurance policy aligns with those plans.

The Role of Lender Title Insurance in Risk Management

Lender title insurance is a crucial element of risk management in the real estate lending process. It shields lenders from potential financial losses that could arise from disputes regarding property ownership and undisclosed legal issues. By understanding how lender title insurance mitigates these risks, we can appreciate its value in safeguarding mortgage lenders’ investments.

Key Aspects of Risk Management with Lender Title Insurance

- Risk Assessment: Lender title insurance thoroughly assesses risks associated with property ownership. It identifies potential issues such as unresolved liens or claims against the property, thereby minimizing unexpected financial setbacks.

- Claims Protection: In the event of a title dispute, lender title insurance covers legal costs and any related financial obligations that arise. This protects the lender’s financial interests and reduces exposure to significant loss.

- Asset Protection: Given that approximately 4% of all lender title insurance policies lead to a claim, the coverage acts as a vital safety net. This allows lenders to maintain the integrity of their loan portfolio without incurring crippling losses due to unforeseen title defects.

| Risk Management Feature | Lender Title Insurance Coverage | Impact on Risk Exposure |

|---|---|---|

| Identification of Title Issues | Yes | Lowers risk of unforeseen claims |

| Legal Cost Coverage | Yes | Reduces financial liabilities |

| Coverage Duration | For the life of the loan | Continuous protection against ownership disputes |

Real-World Examples Demonstrating Risk Mitigation

In one instance, a mortgage lender faced a significant claim arising from a previously undisclosed lien on a property. Thanks to their lender title insurance, the lender avoided absorbing the cost of the claim, which could have amounted to tens of thousands of dollars. This outcome illustrates how lender title insurance effectively mitigates the risk of financial loss linked to title complications.

Another example involved a case where a dispute over property boundaries emerged after a property purchase. The lender, equipped with title insurance, was able to engage legal services without incurring a financial burden, showcasing the proactive risk management role of lender title insurance.

Practical Implications for Home Loan Borrowers

For borrowers, understanding the risk management aspect of lender title insurance can empower them to negotiate better mortgage terms. Here are actionable insights you can consider:

- Ask Your Lender: Inquire about the specific risks that lender title insurance covers and how it can protect your investment.

- Seek Transparency: Ensure you receive comprehensive details about title searches and risk evaluations performed before your lender title insurance is issued.

- Stay Informed: Monitor the property for new liens or ownership disputes even after your title insurance policy is in place, as it helps maintain awareness of potential risks that might arise.

Lender title insurance is an essential tool in managing the risks associated with property ownership and financing. By learning about its role in risk management, both lenders and borrowers can safeguard their financial interests and enhance peace of mind in real estate transactions.