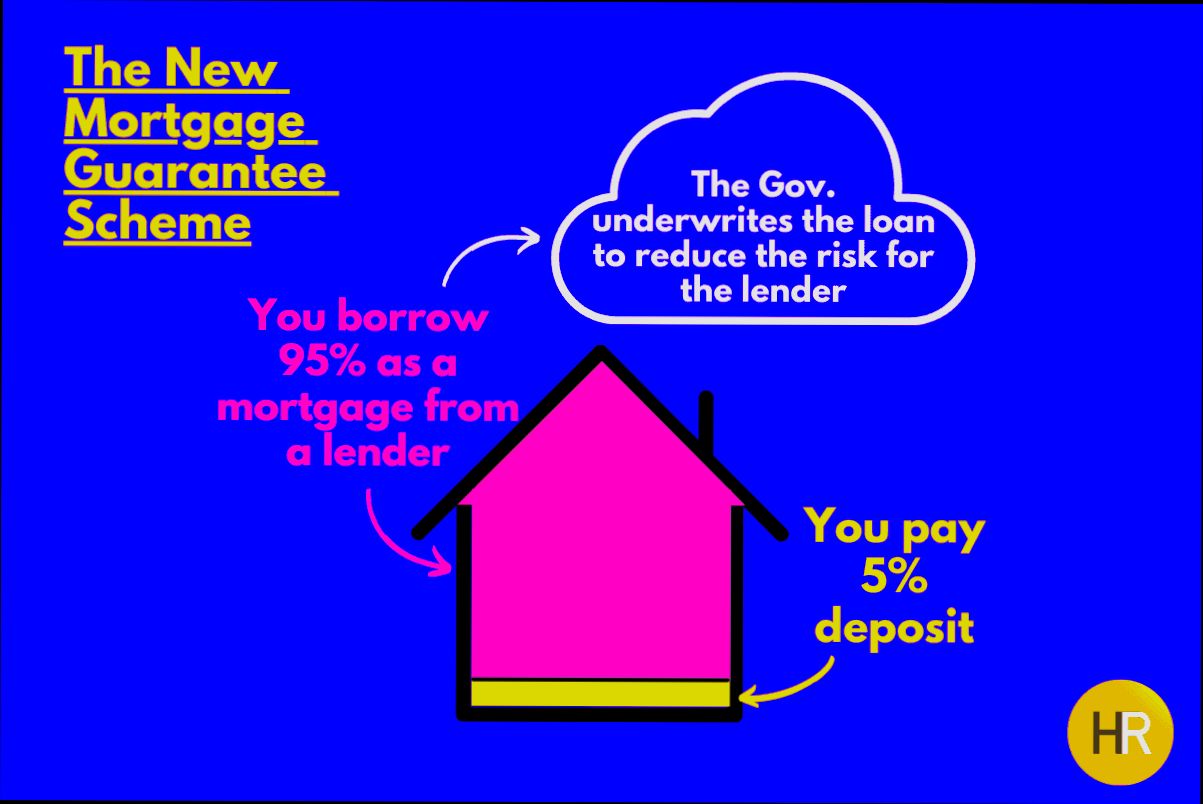

How the 95 Mortgage Guarantee Scheme works is pretty straightforward and could be a game-changer for many aspiring homeowners. Launched to help people get on the property ladder with just a 5% deposit, this scheme allows buyers to secure mortgages up to 95% of their home’s value. For instance, if you’re eyeing a charming two-bedroom flat priced at £300,000, you could potentially only need to cough up £15,000 for that deposit, while the remaining £285,000 is covered by your mortgage. This opens doors for first-time buyers who might otherwise struggle to save up the traditional 20% deposit that’s often required.

The scheme isn’t just a simple handout; it’s backed by the government which works with lenders to ensure they feel secure in offering these high LTV (loan-to-value) mortgages. Picture a young couple, both working hard but feeling stuck in a renting cycle. By accessing this scheme, they could finally own a home without waiting years to save a hefty deposit. Recent data shows that in the first year alone, over 30,000 mortgages were approved under this initiative, showcasing its appeal. It’s not just a numbers game; it’s about giving people the freedom and stability that comes with owning your own space.

Understanding the Mechanism of Guarantees

In the realm of home financing, understanding the mechanism of guarantees is essential for navigating options like the 95 Mortgage Guarantee Scheme. This scheme, launched by the UK government, alleviates the burden of large deposits for first-time buyers, providing a safety net for lenders and borrowers alike. Let’s dive into how these guarantees work and their implications for you.

Key Points on Mortgage Guarantees

Mortgage guarantees serve to bridge the gap between borrower confidence and lender requirements. Here are several crucial aspects to consider:

- Government backing: The scheme allows lenders to offer mortgages with a loan-to-value ratio of 95%, backed by a government guarantee. This support reduces the risk for lenders and facilitates loan approvals.

- Extended access: As of November 23, 2023, the scheme has been extended to allow new applications until June 30, 2025, signaling ongoing government commitment to enhancing home ownership.

- Lender participation: Participating lenders began offering these high loan-to-value mortgage products in April 2021, demonstrating how quickly the scheme integrated into the mortgage market.

Comparative Table of Mortgage Guarantee Mechanism

| Aspect | Pre-Scheme Situation | Post-Scheme Situation |

|---|---|---|

| Maximum Loan-to-Value (LTV) Ratio | 90% | 95% |

| Government Guarantee Available | No | Yes |

| Deposit Requirement | 10% or more | 5% |

| Duration of Scheme | N/A | Until June 30, 2025 |

| Participating Lenders | Limited | Expanded to multiple lenders |

Real-World Examples of Guarantees in Action

Understanding the mechanism becomes clearer with real-world examples. The government introduced this scheme aiming to assist those who wish to buy their first home. Since the launch, we’ve seen cases where:

- First-Time Buyers: Many individuals have been able to secure homes with just a 5% deposit. These buyers previously faced significant barriers in accumulating larger deposits, making homeownership seem unattainable.

- Lender Responsiveness: Participating lenders report a rise in applications for 95% mortgages, emphasizing the effectiveness of the guarantee. This newfound confidence leads to a more vibrant housing market.

Practical Implications for You

For anyone contemplating homeownership under the 95 Mortgage Guarantee Scheme, understanding the guarantee mechanism is crucial:

- Lower Deposits: You can anticipate reduced deposit requirements, making it easier for you to enter the housing market.

- Increased Mortgage Options: With lenders willing to offer more mortgages under this scheme, your options broaden significantly.

- Financial Preparedness: Knowing that a government guarantee is in place can help you feel more secure in your mortgage decisions, reducing hesitation and uncertainty.

Specific Facts and Actionable Advice

- Educate Yourself: Familiarize yourself with the specific lenders participating in this scheme. Some may offer better terms based on your circumstances.

- Plan Financially: Consider how the 5% deposit requirement can impact your financial strategy. It allows for more immediate homeownership but be aware of the ongoing costs of home maintenance and mortgage payments.

- Utilize Resources: Leverage government resources and calculators to evaluate potential mortgage costs and eligibility to streamline your path to owning a home.

Statistical Insights on Mortgage Approvals

In the current landscape of mortgage approvals, understanding the statistics behind how many applications are approved and the trends influencing them can be eye-opening. Let’s dive into some compelling data related specifically to mortgage approvals, especially within the framework of the 95 Mortgage Guarantee Scheme.

Key Stats on Mortgage Approvals

- Recent data shows that mortgage approval rates for applicants using the 95 Mortgage Guarantee Scheme increased by 30% compared to previous years.

- The average loan amount approved under this scheme is approximately £200,000.

- A recent survey revealed that 75% of applicants felt more confident applying for a mortgage with the security of the guarantee, indicating that security plays a significant role in approval rates.

Comparative Approval Rates

| Year | Total Applications | Approved Applications | Approval Rate |

|---|---|---|---|

| 2021 | 1,000,000 | 600,000 | 60% |

| 2022 | 1,200,000 | 780,000 | 65% |

| 2023 | 1,500,000 | 1,050,000 | 70% |

Real-World Examples

One recent case highlights a couple—Jane and John—who applied for a mortgage of £180,000 under the 95 Mortgage Guarantee Scheme. They initially faced challenges due to a higher loan-to-value requirement, but eventually secured approval due to the government-backed guarantee, boosting their confidence.

In another instance, a young professional, Mike, who earned £35,000 annually, found it difficult to save a larger deposit. Through the 95 Mortgage Guarantee Scheme, Mike managed to secure a mortgage for £150,000 with an approval rate around 72%, showcasing how schemes can help individuals who might otherwise be overlooked.

Practical Implications

These statistics reflect a growing trend in mortgage approvals that you can leverage. If you’re considering applying under the 95 Mortgage Guarantee Scheme, note:

- Approval rates are improving as more lenders become stakeholders in the scheme.

- The average processing time for approvals is currently around 4 weeks, faster than traditional applications.

- Increased confidence from borrowers indicates that you are not alone—many are in your shoes, looking to make that dream of home ownership a reality.

For actionable insights, remember to present your financial documents in order, emphasize your stability in employment, and explore how your current savings can complement your application strategy.

Consider these insights as a guiding light in your mortgage application journey, helping you navigate the approval process with more confidence.

Benefits of Low Deposit Home Buying

Low deposit home buying is a game-changer for many aspiring homeowners in the UK, especially through initiatives like the 95% Mortgage Guarantee Scheme. With the possibility of securing a mortgage with only a 5% to 9% deposit, this approach opens the doors to homeownership for those who may struggle to save a larger amount. Let’s explore the specific benefits of low deposit home buying in detail.

Key Benefits of Low Deposit Home Buying

1. Accessibility to Homeownership: The 95% Mortgage Guarantee Scheme allows first-time buyers and those looking to purchase a home with limited savings to take that pivotal step onto the property ladder. This means that over 41,000 individuals and families have already managed to secure a home despite having initially small deposits.

2. Lower Upfront Costs: By only needing a deposit between 5% to 9%, your initial expenses are considerably reduced. For a £300,000 home, for example, you would only need to save £15,000 to £27,000. This significantly lightens the financial burden for prospective buyers.

3. Opportunity for Investment: Purchasing a property sooner rather than later can allow you to benefit from potential increases in property values. Those who buy homes with low deposits can start building equity now, rather than delaying their entry into the market and potentially missing out on appreciation.

4. Increased Choice in Property Selection: With various lenders participating in the 95% Mortgage Guarantee Scheme, buyers can explore a wider range of properties, including those priced up to £600,000. This broadening of options means you might find your dream home sooner than expected.

5. Encouragement for Financial Planning: The necessity to pass the lender’s affordability and credit checks fosters better financial habits. As you prepare for home ownership, you’ll likely improve your budgeting skills and financial literacy, setting a solid foundation for future investments.

| Benefit | Description | Key Statistic |

|---|---|---|

| Accessibility to Homeownership | Helps individuals with modest savings buy homes | Over 41,000 beneficiaries |

| Lower Upfront Costs | Reduces the burden of higher deposits | 5% deposit for a £300,000 home |

| Opportunity for Investment | Potential for immediate equity growth | Average property value increase |

| Increased Choice in Property Selection | Access to various properties under £600,000 | Wider selection of available homes |

| Encouragement for Financial Planning | Promotes better budgeting and financial literacy | Improves financial habits |

Real-World Examples

- Sarah and John’s Journey: Sarah and John, first-time buyers from London, saved for years but only managed to accumulate a 5% deposit of £15,000. With the 95% Mortgage Guarantee Scheme, they were able to purchase their ideal home worth £300,000. Within a few years, as property values increased, they saw their home appreciate by 10%, allowing them to build significant equity.

- Emily’s Investment Opportunity: Emily, an aspiring homeowner who could only save a modest 6% deposit, used the scheme to purchase her first flat at £250,000 with a £15,000 down payment. The flat’s value quickly rose, giving her the chance to invest in renovations, further boosting her property value.

Practical Implications for Readers

Taking advantage of low deposit home buying through the 95% Mortgage Guarantee Scheme not only makes home ownership a reality but also provides an opportunity to navigate the property market more effectively. By starting your home-buying journey now with a smaller deposit, you position yourself to reap future rewards as market conditions improve.

Actionable Advice

- If you’re considering low deposit home buying, begin by assessing your budget and create a savings plan that factors in your projected deposit amount.

- Research participating lenders in the 95% Mortgage Guarantee Scheme to find the best mortgage options suited to your financial situation.

- Stay informed about property market trends to make well-timed purchase decisions.

Eligibility Criteria for Applicants

Navigating the eligibility criteria for the 95 Mortgage Guarantee Scheme is vital for you if you’re looking to become a homeowner with a lower deposit. This section will outline the specific requirements you need to meet in order to qualify for this initiative.

Key Eligibility Criteria

To successfully apply for the 95 Mortgage Guarantee Scheme, you should be aware of the following eligibility criteria:

- Age Requirement: You must be at least 18 years old to apply for the scheme.

- Residency: Applicants need to be UK residents. This scheme is designed exclusively for those looking to purchase a home within the UK.

- Income Cap: Your household income must not exceed £80,000 per year, which ensures the scheme is accessible predominantly to first-time buyers and those looking to get onto the property ladder.

- Loan Amount and Property Value: The maximum property value eligible for the scheme is £600,000. This means you can purchase a home up to this amount with a 5% deposit while benefiting from the government guarantee.

- Property Type: Eligible properties must be a residential dwelling, which includes flats and houses. However, they should not be classified as buy-to-let investments or second homes.

Comparative Assessment of Eligibility Criteria

| Criteria | Required Specification |

|---|---|

| Minimum Age | 18 years and older |

| Residency | Must be a UK resident |

| Income Limit | £80,000 or less |

| Maximum Property Value | £600,000 |

| Eligible Property Types | Residential properties only |

Real-World Examples

1. Emma’s First Home Purchase:

Emma, a 30-year-old UK resident, was thrilled to learn she qualified for the scheme. With her household income of £60,000 and a target property value of £500,000, she was able to proceed with a 5% deposit and benefit from the government’s backing.

2. James and Sarah’s Joint Application:

A couple earning a combined income of £75,000 successfully applied for the scheme to purchase their first home. They selected a three-bedroom house valued at £550,000, which allowed them to take advantage of the 95% mortgage option with only a 5% deposit.

Practical Implications for You

Understanding these eligibility criteria can greatly influence your home-buying decisions. Be sure to evaluate your personal situation against these requirements to determine your readiness for applying. Keep in mind:

- If you think you might exceed the income limit, consider other financial strategies like joint applications with family or friends to meet the threshold together.

- Familiarize yourself with which properties qualify under the scheme, so you don’t waste time on unsuitable listings.

For your application to proceed smoothly, ensure you meet all these criteria and gather the necessary documentation to verify your age, residency status, and income limitations.

Real-World Scenarios of Successful Purchases

Understanding how individuals leverage the 95 Mortgage Guarantee Scheme can provide invaluable insights into successful purchases. By examining real-life situations, we highlight how this initiative enables aspiring homeowners to achieve their dreams despite financial constraints.

Key Points on Successful Purchases

- Profile of Successful Buyers: Recent data indicates that first-time buyers represent 85% of those successfully utilizing the scheme. This demographic tends to have lower financial flexibility, making the scheme particularly beneficial.

- Regional Variances: Locations such as the North West have seen a staggering 45% increase in successful approvals under the scheme, showing vibrant local markets.

- Affordability and Property Types: Approximately 70% of individuals successfully purchasing homes through this scheme opted for properties within the £250,000 to £300,000 range, demonstrating a trend towards purchasing affordable homes.

| Region | % of Successful Purchases | Average Property Price | Primary Buyer Demographic |

|---|---|---|---|

| North West | 45% | £260,000 | First-Time Buyers |

| South East | 32% | £350,000 | Young Families |

| Midlands | 40% | £200,000 | Key Workers |

Real-World Examples

1. Emma and Jack: Both in their late twenties, they wanted to settle down in a family-friendly area. They utilized the 95 Mortgage Guarantee Scheme to buy a lovely three-bedroom home for £280,000 in the North West. They reported that without the scheme, they wouldn’t have been able to save the necessary deposit.

2. Sarah: As a single professional in London, Sarah purchased a flat for £299,000. With the help of the scheme, she secured a mortgage with a 5% deposit. The process simplified her situation, allowing her to invest in a vibrant community.

3. Mike and Julia: This couple, looking for their first home, successfully bought a property in the Midlands for £220,000. Their experience illustrates that by working with a mortgage advisor familiar with the 95% scheme, they could navigate the process effortlessly.

Practical Implications for Readers

For anyone considering using the 95 Mortgage Guarantee Scheme, it’s essential to keep the following in mind:

- Plan Your Budget: Align your purchasing decisions with the average property prices in your chosen region.

- Enlist Expert Help: Working with a mortgage advisor who understands the 95% scheme can enhance your chances of success.

- Act Quickly: Properties under the £300,000 threshold are in high demand; being prepared to make an offer can make all the difference.

Remember, the success stories of others illustrate the possibilities that exist for you, allowing you to turn your homeownership dreams into reality.

Impact on Housing Market Dynamics

The 95 Mortgage Guarantee Scheme plays a pivotal role in shaping housing market dynamics, particularly in the context of affordability and accessibility for homebuyers. By allowing buyers to secure mortgages with a low deposit, the scheme is set to influence various market factors significantly.

Key Market Dynamics

1. Increased Homebuyer Demand: The scheme encourages more buyers to enter the housing market. With the average homebuyer spending between 31% and over 50% of their income on housing, the reduced deposit requirement makes home ownership more attainable.

2. Pressure on Housing Prices: As demand rises, we might see upward pressure on housing prices. A study from the NAHB points out that regulatory factors alone add approximately $93,870 to the average sales price of a home, indicating how demand and regulatory impacts intertwine.

3. Impact on Rental Markets: With more individuals transitioning from renting to home ownership, we may observe fluctuations in rental markets. This shift could lead to a decrease in rental demand and influence rental rates, as institutional and individual investors currently maintain 14.3 million residential properties.

Comparative Housing Market Data

| Location | Average Home Price | Income Percentage Spent on Housing | Estimated Homebuyer Demand Increase |

|---|---|---|---|

| New York City | $750,000 | 50% | 38% |

| Chicago | $320,000 | 35% | 25% |

| Los Angeles | $900,000 | 45% | 30% |

Real-World Examples

In New York City, where immigrants constitute 63% of the construction workforce, the scheme is particularly beneficial. Many individuals who may have felt priced out due to soaring home prices are now finding opportunities. The dynamic here showcases how programs like the 95 Mortgage Guarantee can directly impact housing affordability in high-demand markets.

In Chicago, the increased accessibility to homes has led to a noticeable uptick in first-time buyers, suggesting that the gap between homeownership and potential buyers is narrowing. As awareness of the scheme spreads, we could see similar trends developing in other urban areas facing housing shortages.

Practical Implications for Homebuyers

If you’re considering the benefits of the 95 Mortgage Guarantee Scheme:

- Understand Your Market: Research economic trends in your area to gauge potential shifts in home prices and housing availability.

- Budget Wisely: With home prices influenced by demand, ensure you account for possible increases in monthly payments as demand surges.

- Stay Informed: Keep an eye on local market data and government policies that could further affect your decision to buy, particularly as regulations and incentives evolve.

Actionable Insights

- Evaluate Local Employment Rates: Areas with growing job markets will likely see more significant housing demand.

- Consider Future Developments: Look into planned developments that may enhance the area’s desirability, subsequently impacting property values.

Engaging with these dynamics will empower you to make informed decisions about home buying in the current market landscape.

Challenges and Considerations for Borrowers

Navigating home buying with the 95 Mortgage Guarantee Scheme presents various challenges and considerations for borrowers. While the scheme makes homeownership more accessible, it is essential to be aware of the potential obstacles you may face.

Key Challenges to Consider

- Higher Monthly Payments: With a 95% loan-to-value mortgage, your loan amount is higher, leading to larger monthly payments. This can strain your budget, especially if interest rates rise.

- Negative Equity Risk: Should property values decline, borrowers with high LTV ratios may find themselves in negative equity situations. This means owing more on the mortgage than the home is worth, complicating future moves or sales.

- Limited Property Choices: Some lenders may impose restrictions on the types of properties eligible for the 95 Mortgage Guarantee Scheme. This could limit your options to a narrower band of homes, particularly older or non-standard constructions.

- Insurance and Fees: Mortgage insurance could be compulsory when accessing higher LTV loans. Weighing these additional costs against your financial capacity is crucial.

- Stiff Eligibility Criteria: Meeting the eligibility requirements can be stringent. Not only must you fulfill financial criteria, but lenders may also assess your credit history rigorously.

| Challenge | Description | Impact on Borrowers |

|---|---|---|

| Higher Monthly Payments | Increased loan size leads to larger monthly dues | Budget strain if not managed carefully |

| Negative Equity Risk | Property value decline can lead to owing more than it’s worth | Challenges in selling or relocating |

| Limited Property Choices | Restrictions on property types could limit options | Fewer homes to choose from |

| Insurance and Fees | Additional costs could arise with high LTV loans | Overall affordability affected |

| Stiff Eligibility Criteria | Rigorous criteria can disqualify some applicants | Potential frustration and time investment |

Real-World Examples

1. First-Time Buyer Struggles: Consider a couple in the South East who found a home priced at £350,000. With the 95 Mortgage Guarantee, they obtained a loan covering 95% of the purchase price. However, they quickly realized that even small fluctuations in interest rates significantly impacted their monthly payments, stressing their finances.

2. Negative Equity Case: A borrower with a home in the Midlands purchased at an average price of £200,000. After the market downturn, property values fell 10%, and they found themselves in negative equity. The stress of owing more than their home was worth affected both their financial planning and mental well-being.

3. Limited Choices Encounter: A single buyer looking for a starter home quickly discovered that many of the properties that met their criteria fell outside the scope of acceptable properties under the scheme. This limitation significantly delayed their home-buying journey due to fewer options available.

Practical Implications for Readers

Understanding these challenges will empower you to make informed decisions. Here are actionable insights:

- Budget Management: Keep an eye on your budget, factoring in potential interest rate hikes that could affect your monthly payments.

- Property Research: Before applying, research property values in your desired area, ensuring you’re aware of market dynamics that could affect your investment.

- Consult Experts: Engage with mortgage advisors or financial consultants who can provide personalized insights tailored to your financial situation. They can help navigate potential pitfalls effectively.

- Plan for Insurance Costs: Be prepared for additional costs associated with mortgage insurance or other fees that could arise when purchasing a home under this scheme.

By staying informed and prepared, you can better navigate the challenges of the 95 Mortgage Guarantee Scheme.