How much rent can you afford? That’s a question many of us wrestle with as we navigate the daunting landscape of monthly expenses. Let’s say your monthly income is $3,500—common in many cities today. Experts often recommend that you spend no more than 30% of your income on rent, which means you should ideally aim for something around $1,050. But wait! What if you live in a bustling city like New York or San Francisco, where even a shoebox apartment can easily eat up half your paycheck? Suddenly, that 30% rule feels like a distant dream.

Now, consider your unique situation. If you’re juggling student loans, maybe you’ve got a car payment, and let’s not forget those sneaky utility bills that pop up. Research from the Bureau of Labor Statistics shows that housing is just one part of your budget puzzle. For instance, a typical 25-year-old renter today might find themselves spending closer to 50% of their income on rent—particularly in hot markets. Real-life scenarios vary widely, but understanding your financial landscape can make all the difference in what feels affordable versus what’s stretching your limits.

Determining Your Budget for Rent

When finding a rental property, one of the most crucial steps is determining your rent budget. This decision affects not just your monthly payments but also your overall financial health. By understanding how much of your income can realistically go towards rent, you can avoid financial strain while still enjoying your space.

Understanding Your Income and Expenses

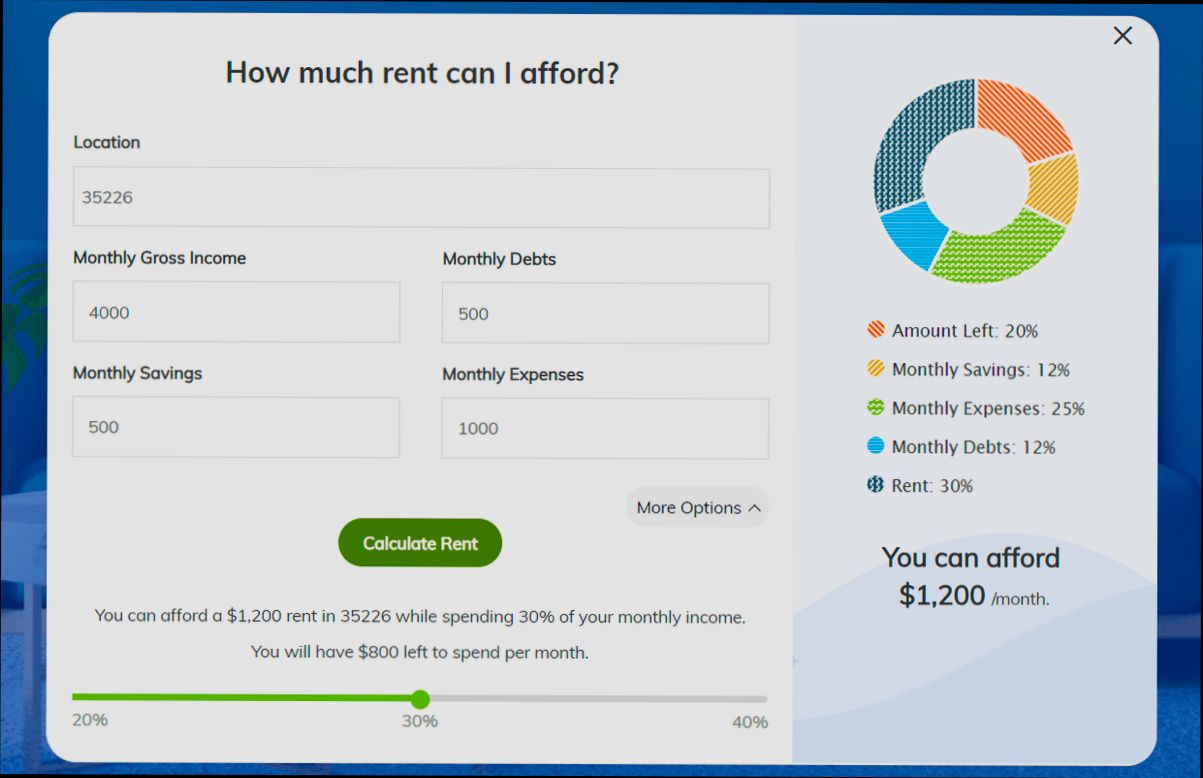

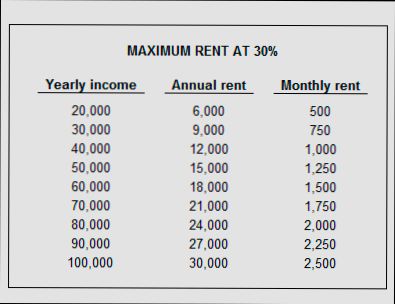

A widely accepted guideline is the 30% rent rule, which suggests that you should aim to spend about 30% of your gross income on rent. For instance, if your gross monthly income is $4,000, this means you would allocate $1,200 for rent. However, this guideline may require adjustments based on your unique circumstances.

- Income Variables: If you earn less than the average, such as $3,000 monthly, your maximum rent should be around $900, whereas someone making $5,000 could afford to spend $1,500.

- Higher Living Costs: In high-cost cities, sticking strictly to the 30% rule could push you into neighborhoods that don’t meet your safety or quality-of-life needs.

Using the 50/30/20 Budgeting Model

Another effective budgeting strategy is the 50/30/20 rule, which divides your take-home pay into three categories:

- 50% for needs (essentials like rent, utilities, groceries, etc.)

- 30% for wants

- 20% for savings and debt repayment

If your take-home pay is $4,000, this breakdown would leave you with $2,000 for needs. Knowing this, your rent budget ideally should not exceed that amount.

| Monthly Income | 30% Rent Budget | 50% Needs Budget |

|---|---|---|

| $3,000 | $900 | $1,500 |

| $4,000 | $1,200 | $2,000 |

| $5,000 | $1,500 | $2,500 |

Evaluating Personal Circumstances

Sometimes life doesn’t fit neatly into rules. Here are specific scenarios where you might adjust your rent budget:

- Unstable Living Situation: If you’re in a dangerous or unstable rental setting, it might be worth allocating more of your budget toward a safer place, even if it’s a stretch.

- Job Relocation: Relocating for work often necessitates a higher rent budget, especially if it leads to a shorter commute or better job stability.

Practical Money-Saving Strategies

To maximize your budget for rent, consider these actionable suggestions:

- Get a Roommate: This can dramatically reduce your monthly rent and utility payments. For example, instead of paying $1,200 for a one-bedroom, you might find a two-bedroom where both parties only pay $800 each.

- Negotiate Bills: Since certain expenses like heat and electricity are classified as needs, look for ways to decrease these spending categories. Cutting out things like premium cable can help keep your budget on track.

- Plan Groceries Carefully: By budgeting around $225 for groceries, I recommend using coupons and planning meals effectively to reduce unnecessary spending.

Final Considerations

When determining how much rent you can afford, always keep your overall financial picture in mind. The percentage of income you allocate to rent might need to change based on:

- Wage growth or fluctuation in income

- Increase in living costs in your area

- Unforeseen expenses that might arise

Ultimately, ensure you’re balancing necessary expenses with a safe and enjoyable living situation.

Understanding Income-to-Rent Ratio

When it comes to figuring out how much rent you can realistically afford, understanding the income-to-rent ratio is crucial. This ratio compares your monthly income to the amount you plan to spend on rent, helping you assess your affordability in a more nuanced way.

Key Points about Income-to-Rent Ratio

The income-to-rent ratio is generally expressed as a percentage and provides a clear picture of your financial landscape. Here are some valuable data points to keep in mind:

- 50% Threshold: Some financial experts suggest that spending up to 50% of your income on rent may be acceptable under certain conditions, such as when you have significant savings or additional sources of income.

- 35% Suggested Maximum: If you want to maintain a comfortable budget without stretching your finances, aim for an income-to-rent ratio of 35%. This allows more room for other expenses like utilities, groceries, and savings.

- Income Variability Impact: If your monthly income fluctuates, adjust your acceptable rent accordingly. For example, a steady income of $4,000 might allow for a rent commitment of up to $1,400 at a 35% ratio—but during lean months, you may wish to reduce your rent commitment to 25%, or $1,000.

| Income Level | Suggested Rent (50%) | Suggested Rent (35%) | Suggested Rent (25%) |

|---|---|---|---|

| $3,000 | $1,500 | $1,050 | $750 |

| $4,000 | $2,000 | $1,400 | $1,000 |

| $5,000 | $2,500 | $1,750 | $1,250 |

Real-World Examples

Let’s say you earn $3,500 monthly:

- 50% Rent Commitment: You could technically afford $1,750 in rent. However, this would leave little for other personal expenses.

- 35% Rent Commitment: At this ratio, your ideal rent would be around $1,225, allowing you a healthier budget for savings and lifestyle needs.

- 25% Rent Commitment: Aiming for $875 per month can offer you a significant cushion during unpredictable financial months.

On the flip side, if your income is $6,000, you might consider:

- 50% Rent: $3,000 becomes your maximum rent, which could lead to financial strain.

- 35% Rent: You target $2,100, balancing housing costs with other living expenses better.

- 25% Rent: By settling for $1,500, you can save more for future investments or unexpected bills.

Practical Implications

Understanding your income-to-rent ratio helps in making informed decisions about housing. Here’s how you can make sense of it:

- Personal Financial Assessment: Regularly review your income and expenses to find your ideal income-to-rent ratio.

- Emergency Fund Consideration: A lower rent relative to your income can create a buffer for emergencies, ensuring that you stay afloat during tough times.

- Future Financial Goals: Think about how your current rent aligns with your saving goals for future investments, retirement, or homeownership.

Actionable Advice

- Calculate Your Ratio: Take your monthly income and divide it by the anticipated rent amount to determine your income-to-rent ratio.

- Adjust Accordingly: If your ratio exceeds your comfort zone of 35% to 50%, consider looking for more affordable housing options.

- Monitor Changes: Ensure you re-evaluate your ratio every six months or after any significant income change.

Understanding your income-to-rent ratio provides you with a clearer financial roadmap and helps you align your housing choices with your overall financial health.

Analyzing Rental Market Trends

Understanding rental market trends is vital for determining how much rent you can afford. By analyzing these trends, you can make informed decisions about your housing options and avoid overspending in a fluctuating market. Let’s dive into some key points to guide your analysis.

Key Trends in the Rental Market

1. Rental Price Growth: Nationally, rental prices have increased by approximately 6% over the past year, with some urban areas seeing growth rates as high as 10%. This growth affects affordability, particularly among low to middle-income renters.

2. Vacancy Rates: Current vacancy rates are hovering around 5% nationally, which indicates a balanced market. However, rates differ significantly by region. For instance, larger cities like New York exhibit lower vacancy rates of about 2.8%, leading to higher competition and price increases.

3. Rental Demand Surge: The demand for rental properties has surged post-pandemic, with statistics showing that new rental applications have risen by 25% compared to pre-pandemic levels. This trend can strain the supply and push average rents even higher.

Comparative Analysis of Rental Markets

| City | Average Rent (1-Bedroom) | Rent Change (Year-over-Year) | Vacancy Rate | Rental Demand Change |

|---|---|---|---|---|

| New York | $2,800 | +10% | 2.8% | +30% |

| Los Angeles | $2,400 | +8% | 4.2% | +20% |

| Chicago | $1,800 | +5% | 5.5% | +15% |

| Miami | $2,200 | +7% | 3.5% | +18% |

| San Francisco | $3,200 | +9% | 3.0% | +25% |

Real-World Examples

- New York City: The 10% increase in rental prices over the last year means that previously affordable options are slipping out of reach for many. A one-bedroom that may have rented for $2,500 last year now averages about $2,800. This sharp rise can influence prospective tenants’ budget considerations significantly.

- Los Angeles: With an 8% annual rental increase and a vacancy rate of 4.2%, many renters face stiff competition. Application rates have surged by 20%, signaling a demand that could continue to outstrip supply, pushing prices higher.

Practical Implications to Consider

- Keep Track of Local Trends: Regularly monitoring your local rental market will help you spot trends and anticipate potential price changes. Websites offering rental listings can be great resources for real-time data.

- Consider Upcoming Developments: New construction can influence future rental prices. Areas with planned developments may see an influx of options, potentially stabilizing or lowering current rental prices.

- Utilize Market Reports: Make use of market reports from real estate agencies or housing authorities. These reports often provide insights into current trends, including projected rent growth and changes in consumer preferences.

Actionable Advice

To navigate the rental market effectively, always set alerts for rental listings in your desired area and engage with local real estate groups online. By staying informed about market trends, you can better time your rental search, negotiate effectively, and ensure that you find a living situation aligning with your financial capabilities.

Real-Life Scenarios of Rent Affordability

Understanding how rent affordability plays out in real life can be eye-opening. We often hear guidelines and theories, but seeing these concepts in action makes them more relatable. Let’s dive into some real-life scenarios that highlight how different incomes and living situations impact rent affordability.

Key Points and Data

- According to recent studies, approximately 60% of renters face challenges in affording their rent, especially in metropolitan areas.

- Research indicates that around 40% of renters are spending more than 30% of their income on housing, one of the commonly recommended thresholds.

- A notable finding shows that 20% of renters are forced to allocate more than half of their income to rent, often leading to financial strain.

- In some cities, rent prices have increased by over 10% year-on-year, making it difficult for families with fixed incomes to keep up.

Comparative Table: Rent Affordability Scenarios

| Income Level | Recommended Rent (30%) | Average Market Rent | Rent-to-Income Ratio |

|---|---|---|---|

| $2,500 | $750 | $1,000 | 40% |

| $3,500 | $1,050 | $1,400 | 40% |

| $5,000 | $1,500 | $1,800 | 36% |

| $7,000 | $2,100 | $2,800 | 40% |

Real-World Examples

1. Emily earns $3,000 a month and lives in a bustling city where average rents around her are $1,200. Although her budget should ideally keep her at $900 a month, she ends up spending 40% of her income on housing. This forces her to cut back on groceries and discretionary spending.

2. John makes $4,500 monthly. He finds a rental at $1,450, which is just about 32% of his income. While it appears manageable on paper, John’s high transportation costs mean he has little left over for savings, illustrating the strain that other expenses can place on the rent budget.

3. A family of four earns a combined income of $6,000. They secure an apartment for $2,000 a month, hitting 33% of their income. However, with increasing childcare and education expenses, they discover they have little left for leisure activities, highlighting how varying life circumstances can affect rent affordability.

Practical Implications

When considering your housing options, it helps to think beyond just the base rent. Consider the following:

- Always factor in utilities and additional expenses (transportation, groceries), as they can drastically affect your overall budget.

- Look for community resources like housing assistance programs if you find yourself near the 50% threshold. These can ease the burden.

- Understand that different locations will inherently have varying rental markets. If moving to a less expensive area, calculate how much you’d save and weigh it against potential job accessibility or commute times.

It isn’t just about knowing the dollar figures; understanding your rent-to-income ratio, how other costs impact your finances, and recognizing the community landscape can help you make informed choices about where and how to live affordably.

Navigating Hidden Costs of Renting

When looking for a rental property, understanding the hidden costs can significantly impact your affordability. These hidden costs often extend beyond the rent price you initially see, influencing your overall financial picture as a renter.

Understanding Hidden Costs

Hidden costs in renting can vary widely, and they significantly affect your budget. Here are some common expenses to consider:

- Utilities: While many expect to pay rent, utilities such as electricity, gas, water, and trash services can add up. The average monthly utility cost is estimated to be around $200, which can be a substantial addition to your rent.

- Renter’s Insurance: This can cost anywhere from $15 to $30 a month, protecting your belongings from theft or damage. It’s also often required by landlords.

- Maintenance Fees: If you’re renting in a managed property, you may have to pay monthly maintenance fees or special assessments. These fees can average around $100 a month, depending on the amenities.

- Parking Fees: In urban areas, parking can be a hidden cost that sneaks up on you. Monthly parking fees can range from $50 to $300 based on location.

- Application and Move-in Fees: Be ready for initial costs like application fees (averaging $50 to $100), and move-in fees, which can range from $200 to $500.

Comparative Cost Table

| Cost Type | Estimated Monthly Cost |

|---|---|

| Utilities | $200 |

| Renter’s Insurance | $20 |

| Maintenance Fees | $100 |

| Parking Fees | $150 |

| Application Fees | $75 |

Real-World Examples

According to the latest data from the American Community Survey, low-income renters were reported to spend larger portions of their incomes on rent and utilities. In 2021, renters with the lowest annual income faced an increase in the percentage of their income spent on these essentials, highlighting how hidden costs can severely impact financial stability.

For example, if someone with an annual income of $30,000 finds a rental for $1,000 a month, their rent will consume 40% of their gross income—this figure grows even higher when including additional monthly costs like utilities and renter’s insurance.

Practical Implications

Being aware of these hidden costs can help you prepare better financially. Here are some actionable steps:

- Research Local Utility Costs: Check average utility rates in your prospective rental areas to factor this into your budget.

- Negotiate Rent and Fees: If you find an apartment with higher-than-expected fees, consider negotiating with the landlord. Sometimes, they may lower fees to secure a tenant.

- Budget for the Unexpected: Always set aside an emergency fund for unanticipated expenses. This can alleviate stress when unexpected repairs or utility spikes occur.

- Seek Holistic Information: Use platforms like Census.gov and the American Community Survey to gather data on rental costs and trends in your area.

Finally, remember that navigating hidden costs requires diligence. By fully understanding what you might incur, you set yourself up for a more accurate picture of how much rent you can genuinely afford.

Benefits of Calculating Rent Affordability

Calculating rent affordability is a crucial step that can significantly impact your financial wellness and overall quality of life. By understanding how much you can afford, you empower yourself to make informed decisions when searching for a rental property. Let’s explore the benefits of this essential calculation.

Financial Security

1. Avoiding Financial Strain: Knowing your rent affordability helps you avoid stretching your budget too thin. Research indicates that more than 60% of renters struggle to meet their rental payments. By calculating what you can truly afford, you reduce the risk of falling into debt or financial crisis.

2. Buffer Against Emergencies: When you set a rent limit within your income parameters, it leaves room in your budget for unforeseen expenses—like medical bills or car repairs. This buffer is essential for maintaining peace of mind and ensuring financial stability.

Better Housing Choices

1. Focus on Suitable Options: By understanding your affordability, you can narrow down your options to properties that fit your budget. This targeted approach helps you save time and reduces frustration when searching.

2. Better Quality Rentals: When you know how much rent you can afford, you can prioritize quality over cost. Instead of settling for a subpar apartment simply to save money, you can seek accommodations that offer value, comfort, and amenities.

Improved Relationship with Money

1. Enhanced Financial Literacy: Calculating rent affordability engages you in financial planning, enhancing your overall financial literacy. This knowledge can extend beyond housing budgets to other areas of your financial life.

2. Confidence in Negotiation: Understanding your financial boundaries equips you with the confidence to negotiate rent terms or seek financial assistance if necessary. This preparedness can lead to better leasing outcomes.

| Income Level | Recommended Rent (30%) | Average Market Rent | Rent-to-Income Ratio |

|---|---|---|---|

| $2,500 | $750 | $1,000 | 40% |

| $3,500 | $1,050 | $1,400 | 40% |

| $5,000 | $1,500 | $1,800 | 36% |

| $7,000 | $2,100 | $2,800 | 40% |

Real-World Example

Consider Sam, who has a monthly income of $3,500. After calculating his affordability, he determines that he should ideally spend $1,050 on rent. However, his dream apartment’s market rent is $1,400. With this knowledge, Sam can make a more informed choice: he may consider looking for a roommate to share costs or negotiate the rent with the landlord. This strategic approach keeps him within his financial limits and allows him to find a more affordable solution.

Practical Implications

Understanding rent affordability strengthens your overall financial positioning. By calculating what you can comfortably spend on rent, you can:

- Prioritize savings and investments.

- Make informed decisions during economic fluctuations.

- Position yourself better for financial stability in the long run.

By being diligent in calculating rent affordability, you not only protect your current financial situation but also pave the way toward a secure financial future.

Impact of Location on Rent Prices

The location where you choose to rent can significantly influence your monthly expenses. If you’ve ever wondered why similar apartments can vary so widely in price based solely on location, you’re not alone. Understanding these geographical influences on rent prices can help you make more informed decisions about where to live.

Key Factors Influencing Rent by Location

1. Urban vs. Rural Areas:

- Urban areas tend to have a higher cost of living, which directly affects rent prices. In metropolitan regions, rents can be 30-50% higher compared to similar apartments in rural locations.

2. Neighborhood Demand:

- Areas with a high demand for housing, like trendy neighborhoods or those near prominent businesses, can see rent prices spike. For instance, average rents in high-demand neighborhoods have been reported to increase by 10-20% annually.

3. Proximity to Amenities:

- Living near schools, parks, public transportation, and shopping centers can raise rent prices. Properties close to major amenities can be priced 15-25% higher than those that are further away, making access to conveniences a key factor in rent assessments.

4. Economic Conditions:

- Regions experiencing job growth or economic expansion often correlate with rising rent prices. In areas where the unemployment rate drops below 4%, it’s common to see rent increases of 5-15% due to heightened demand for housing.

5. Cost of Living Index:

- Cities with a high cost of living—like San Francisco or New York—regularly report average rent costs that can exceed $3,000 for a one-bedroom apartment. In contrast, lower-cost regions may have apartments priced around $1,200 for similar setups.

Comparative Rent by Location

| Location Type | Average Rent (1-Bedroom) | Rent Increase % (Yearly) |

|---|---|---|

| Urban (High Demand) | $3,000 | 10-20% |

| Urban (Low Demand) | $2,000 | 5-10% |

| Suburban | $1,500 | 5-15% |

| Rural | $1,200 | 2-5% |

| High Cost Living City | $3,500 | 15% |

Real-World Examples

Consider two friends, Alex and Jamie, who decided to rent in different areas. Alex chose to live in a bustling urban center with a monthly rent of $2,800. Meanwhile, Jamie opted for a quieter suburb where rent is only $1,500. Despite being a relatively short commute apart, Alex spends nearly $1,300 more each month, essentially for the benefits of urban living.

Similarly, another scenario features two neighborhoods within the same city—one affluent and the other less so. In the affluent area, one-bedroom apartments average $3,000, while just a few blocks away, comparable units rent for $2,000. This stark difference highlights how neighborhood reputation and desirability can significantly impact rental costs.

Practical Implications for Renters

When considering where to rent, you should evaluate the balance between cost and location. Here are some actionable tips:

- Research Local Markets: Before committing, investigate the rent prices in various neighborhoods to gauge where you can get the most bang for your buck.

- Consider Commute Times: Sometimes, living slightly further away can save you significant amounts on rent while still maintaining a reasonable commute.

- Check Future Developments: Areas slated for future development may experience price hikes. Understanding potential changes can guide you in choosing a location.

- Weigh Amenities vs. Cost: Determine which amenities matter most to you, and see if sacrificing proximity to certain amenities can grant you lower rent.

- Stay Informed on Trends: Local economic conditions can directly influence rent. Staying updated on job growth and infrastructure developments can provide insights into potential rent shifts.

By acknowledging the impact of location on rent prices, you can better strategize your housing decision, ultimately leading to smarter financial choices.